NSIA a réussi non seulement à maintenir, mais aussi à améliorer sa performance financière, se positionnant ainsi comme un acteur clé du secteur bancaire ivoirien.

NSIA Banque Côte d’Ivoire (NSIA) a démontré sa résilience financière et sa croissance au cours du premier semestre 2024, malgré un environnement économique mondial difficile.

Alors que le monde se remet lentement des perturbations causées par les crises mondiales des dernières années, NSIA a réussi à non seulement maintenir, mais aussi à améliorer sa performance financière, se positionnant ainsi comme un acteur clé du secteur bancaire ivoirien.

Performance Financière et Croissance des Bénéfices

La performance financière de NSIA Banque au premier semestre 2024 a été impressionnante. Le Produit Net Bancaire de la banque a augmenté de 10,3 % d’une année sur l’autre, atteignant 45,7 milliards de FCFA (78 millions de dollars), contre 41,4 milliards de FCFA au même trimestre de 2023. Cette croissance reflète la capacité de la banque à générer plus de revenus grâce à ses activités bancaires principales malgré les incertitudes économiques plus larges.

Un aspect notable des bénéfices de NSIA est l’augmentation significative de son revenu net. La banque a enregistré un bénéfice net de 14,528 milliards de FCFA, marquant une hausse substantielle de 27,5 % par rapport aux 11,4 milliards de FCFA gagnés au premier semestre 2023. Cette augmentation de la rentabilité souligne la gestion efficace des coûts de NSIA et les initiatives stratégiques visant à stimuler la croissance des revenus tout en maîtrisant les coûts opérationnels.

Rentabilité et Efficacité Opérationnelle

L’efficacité opérationnelle de la banque a également enregistré des progrès positifs. Les charges d’exploitation ont augmenté de 9 %, passant de 21,3 milliards de FCFA en juin 2023 à 23,2 milliards de FCFA en juin 2024.

Malgré cette augmentation des coûts, NSIA a réussi à améliorer légèrement son ratio coût/revenu, qui est désormais de 59,9 %, contre 60,4 % un an plus tôt. Cette amélioration, bien que marginale, indique que NSIA devient plus efficace dans la conversion de ses revenus en bénéfices, ce qui est un bon signe pour les actionnaires à la recherche de création de valeur.

De plus, le résultat brut d’exploitation a augmenté de 12 %, passant de 16,4 milliards de FCFA en juin 2023 à 18,3 milliards de FCFA en juin 2024. Cette augmentation reflète la capacité de la banque à maintenir des gains solides avant impôts et coûts de risque, renforçant ainsi sa rentabilité.

Un des signes les plus encourageants pour les investisseurs est la réduction significative du coût du risque. Le coût net du risque est passé de -3,7 milliards de FCFA en juin 2023 à -2,7 milliards de FCFA en juin 2024. Cette réduction d’environ 27 % met en évidence les efforts réussis de la banque pour gérer le risque de crédit, ce qui est crucial pour maintenir la rentabilité à long terme et protéger la valeur actionnariale.

Solidité du Bilan et Qualité des Actifs

Le bilan de NSIA Banque reflète une base solide qui soutient sa rentabilité continue. Le total des actifs a augmenté de 6 % passant de 2 037 milliards de FCFA en décembre 2023 à 2 159 milliards de FCFA en juin 2024. Cette croissance des actifs est principalement due à une augmentation de 6 % des prêts aux clients, qui sont passés de 1 307 milliards de FCFA à 1 382 milliards de FCFA au cours de la même période.

La capacité de la banque à accorder plus de crédits, en particulier aux petites et moyennes entreprises (PME), démontre son engagement à favoriser la croissance économique en Côte d’Ivoire tout en augmentant ses actifs générateurs de revenus.

Du côté des passifs, les dépôts de la clientèle ont augmenté de 7 %, passant de 1 415,9 milliards de FCFA en décembre 2023 à 1 511,4 milliards de FCFA en juin 2024. Cette augmentation des dépôts, en particulier dans les comptes à vue, les comptes d’épargne et les dépôts de garantie, indique une confiance croissante des clients dans la stabilité et les offres de services de NSIA Banque.

Il convient toutefois de noter que le portefeuille de titres de NSIA a diminué de 5 %, reflétant une approche prudente face à la volatilité des marchés et un éventuel changement stratégique vers des activités bancaires plus traditionnelles, qui offrent généralement des rendements plus stables.

Performance Boursière et Implications pour le Marché

D’un point de vue boursier, l’action NSIA Banque (NSBC) a offert des rendements remarquables à ses investisseurs.

Le prix de l’action de la banque a commencé l’année à 6 000 XOF et a depuis augmenté de 8,25 %, surpassant de nombreux concurrents sur la Bourse Régionale des Valeurs Mobilières (BRVM). Cette appréciation des prix place NSIA Banque comme la 26e action la plus performante sur la BRVM en termes de performance annuelle, ce qui est une réalisation notable compte tenu du paysage concurrentiel.

De plus, NSIA Banque est actuellement la 11e action la plus valorisée sur la BRVM, avec une capitalisation boursière de 161 milliards XOF. Cette valorisation représente environ 1,72 % du marché total des actions sur la BRVM, soulignant le rôle significatif de NSIA dans l’écosystème financier régional.

Pour les actionnaires, la solide performance financière et l’appréciation de l’action de NSIA Banque présentent une proposition d’investissement attrayante.

La capacité de la banque à augmenter ses bénéfices, à améliorer son efficacité opérationnelle et à maintenir la qualité de ses actifs dans un contexte d’incertitude économique est susceptible de continuer à alimenter l’appréciation du prix des actions et à créer de la valeur pour les actionnaires. La rentabilité soutenue et les stratégies de gestion prudente des risques renforcent encore l’attrait de NSIA Banque en tant qu’investissement fiable dans les marchés financiers de l’Afrique de l’Ouest.

Conclusion

La performance financière de NSIA Banque Côte d’Ivoire au premier semestre 2024 reflète une institution bien gérée qui non seulement résiste aux défis économiques de l’ère post-pandémique, mais prospère également. La croissance significative des bénéfices, combinée à l’amélioration de la rentabilité et à un bilan solide, positionne NSIA Banque comme un acteur de premier plan dans le secteur bancaire ivoirien.

Pour les actionnaires, la santé financière robuste de la banque et l’impressionnante performance boursière sont synonymes de rendements prometteurs et de création de valeur à long terme. À mesure que NSIA Banque continue de mettre en œuvre ses initiatives stratégiques et d’améliorer son efficacité opérationnelle, elle reste une opportunité d’investissement convaincante sur le marché des actions de la BRVM.

NSIA has managed to not only sustain but also enhance its financial performance, positioning itself as a key player in the Ivorian banking sector.

Nsia Banque Côte d’Ivoire (NSIA) has demonstrated financial resilience and growth in the first half of 2024, despite operating in a challenging global economic environment.

As the world slowly recovers from the disruptions caused by the global crises of recent years, NSIA has managed to not only sustain but also enhance its financial performance, positioning itself as a key player in the Ivorian banking sector.

Financial Performance and Earnings Growth

NSIA Banque’s financial performance in the first half of 2024 has been nothing short of impressive. The bank’s Net Banking Product (Produit Net Bancaire) rose by 10.3% year-over-year, reaching 45.7 billion FCFA ($78 million), up from 41.4 billion FCFA in the same period of 2023. This growth reflects the bank’s ability to generate more revenue from its core banking activities despite the broader economic uncertainties.

A notable aspect of NSIA’s earnings is the significant increase in its net income. The bank recorded a net profit of 14.528 billion FCFA, marking a substantial 27.5% rise from the 11.4 billion FCFA earned in the first half of 2023. This surge in profitability underscores NSIA’s effective cost management and strategic initiatives aimed at driving revenue growth while keeping operational costs in check.

Profitability and Operational Efficiency

The bank’s operational efficiency has also seen positive strides. The operating expenses increased by 9%, from 21.3 billion FCFA in June 2023 to 23.2 billion FCFA in June 2024.

Despite this rise in costs, NSIA has managed to slightly improve its cost-to-income ratio, which now stands at 59.9%, down from 60.4% a year earlier. This improvement, albeit marginal, indicates that NSIA is becoming more efficient in converting its income into profit, which is a good sign for shareholders looking for value creation.

Moreover, the gross operating income grew by 12%, rising from 16.4 billion FCFA in June 2023 to 18.3 billion FCFA in June 2024. This increase reflects the bank’s ability to maintain strong earnings before taxes and risk costs, further bolstering its profitability.

One of the most encouraging signs for investors is the significant reduction in the cost of risk. The net risk cost decreased from -3.7 billion FCFA in June 2023 to -2.7 billion FCFA in June 2024. This reduction by approximately 27% highlights the bank’s successful efforts in managing credit risk, which is crucial for maintaining long-term profitability and protecting shareholder value.

Balance Sheet Strength and Asset Quality

NSIA Banque’s balance sheet reflects a solid foundation that supports its ongoing profitability. The total assets increased by 6% from 2,037 billion FCFA in December 2023 to 2,159 billion FCFA as of June 2024. This growth in assets is primarily driven by a 6% increase in loans to customers, which rose from 1,307 billion FCFA to 1,382 billion FCFA during the same period.

The bank’s ability to extend more credit, particularly to small and medium enterprises (SMEs), demonstrates its commitment to fostering economic growth in Côte d’Ivoire while enhancing its income-generating assets.

On the liabilities side, customer deposits grew by 7%, from 1,415.9 billion FCFA in December 2023 to 1,511.4 billion FCFA in June 2024. This increase in deposits, particularly in demand deposits, savings accounts, and guarantee deposits, indicates growing customer confidence in NSIA Banque’s stability and service offerings.

However, it is worth noting that NSIA’s securities portfolio declined by 5%, reflecting a cautious approach to market volatility and a possible strategic shift towards more traditional banking activities, which typically offer more stable returns.

Stock Performance and Market Implications

From a market perspective, NSIA Banque’s stock (NSBC) has delivered commendable returns for its investors.

The bank’s share price started the year at 6,000 XOF and has since appreciated by 8.25%, outperforming many of its peers on the Bourse Régionale des Valeurs Mobilières (BRVM). This price appreciation places NSIA Banque as the 26th best-performing stock on the BRVM in terms of year-to-date performance, a notable achievement considering the competitive landscape.

Moreover, NSIA Banque is currently the 11th most valuable stock on the BRVM, with a market capitalization of 161 billion XOF. This valuation accounts for approximately 1.72% of the total equity market on the BRVM, underscoring NSIA’s significant role in the regional financial ecosystem.

For shareholders, NSIA Banque’s strong financial performance and stock appreciation present an attractive investment proposition.

The bank’s ability to grow earnings, improve operational efficiency, and maintain asset quality amidst economic uncertainties is likely to drive continued share price appreciation and deliver value to shareholders. The sustained profitability and prudent risk management strategies further enhance NSIA Banque’s appeal as a reliable investment in the West African financial markets.

Conclusion

NSIA Banque Côte d’Ivoire’s financial performance in the first half of 2024 reflects a well-managed institution that is not only weathering the economic challenges of the post-pandemic era but is also thriving. The significant growth in earnings, combined with improved profitability and a strong balance sheet, positions NSIA Banque as a leading player in the Ivorian banking sector.

For shareholders, the bank’s robust financial health and impressive stock performance signal promising returns and long-term value creation. As NSIA Banque continues to implement its strategic initiatives and enhance its operational efficiency, it remains a compelling investment opportunity in the BRVM equity market.

Le franc CFA est devenu une couverture stratégique pour naviguer dans la crise des devises en Afrique. Voici pourquoi cette monnaie indexée sur l’euro est un refuge sûr.

Face à l’instabilité monétaire généralisée à travers l’Afrique, le franc CFA se distingue comme un phare de stabilité relative.

Cette monnaie, utilisée par 14 pays africains, est devenue une couverture stratégique pour les commerçants et les investisseurs cherchant à naviguer dans les eaux turbulentes de la crise monétaire en cours sur le continent.

Pour comprendre son importance, il faut d’abord explorer l’histoire et la structure du système du franc CFA, avant d’examiner son fonctionnement dans le contexte des défis économiques plus larges de l’Afrique.

Qu’est-ce que le franc CFA ?

Le franc CFA, qui signifie « Communauté Financière Africaine » en Afrique de l’Ouest et « Coopération Financière en Afrique Centrale » en Afrique centrale, a une histoire qui remonte à l’ère coloniale.

Créé par la France en 1945 pour ses colonies après la Seconde Guerre mondiale, la monnaie a évolué tout en conservant sa structure de base.

Aujourd’hui, le franc CFA est divisé en deux monnaies distinctes mais de valeur similaire : le franc CFA de l’Afrique de l’Ouest (XOF) utilisé par huit pays de l’Union économique et monétaire ouest-africaine (UEMOA), et le franc CFA de l’Afrique centrale (XAF) utilisé par six pays de la Communauté économique et monétaire de l’Afrique centrale (CEMAC).

La caractéristique clé du franc CFA est son taux de change fixe avec l’euro.

Initialement indexé sur le franc français, il a été réorienté vers l’euro en 1999 lorsque la France a adopté l’euro. Cette transition a maintenu la stabilité de la monnaie tout en déplaçant son ancrage vers le système monétaire européen plus large.

Bien que les XOF et XAF aient la même valeur et le même ancrage à l’euro, ce sont des monnaies distinctes utilisées dans des régions différentes.

Le XOF circule en Afrique de l’Ouest (pays de l’UEMOA), tandis que le XAF est utilisé en Afrique centrale (pays de la CEMAC). Bien qu’ils soient théoriquement interchangeables, ils ne sont généralement pas utilisés en dehors de leurs zones respectives.

Malgré le fait qu’il s’agisse de monnaies distinctes, les XOF et XAF ont la même valeur et sont indexés sur l’euro à un taux fixe de 1 euro pour 655,96 francs CFA.

Ce système monétaire unique en Afrique offre un niveau de stabilité rare dans de nombreuses économies africaines, souvent confrontées à une volatilité sévère des devises, mais il a également suscité des débats sur la souveraineté économique.

Quels sont les pays qui utilisent le franc CFA ?

Le franc CFA est utilisé par 14 pays regroupés en deux unions monétaires.

L’Union économique et monétaire ouest-africaine (UEMOA) comprend le Bénin, le Burkina Faso, la Côte d’Ivoire, la Guinée-Bissau, le Mali, le Niger, le Sénégal et le Togo.

La Communauté économique et monétaire de l’Afrique centrale (CEMAC) regroupe le Cameroun, la République centrafricaine, le Tchad, la République du Congo, la Guinée équatoriale et le Gabon.

Ces nations représentent collectivement une part significative de l’économie de l’Afrique subsaharienne.

Au moment de la rédaction de cet article, le taux de change est d’environ 595 francs CFA pour 1 dollar américain.

Cependant, il est important de noter que la valeur du franc CFA est directement liée à l’euro, et non au dollar, de sorte que ce taux peut fluctuer en fonction des taux de change euro-dollar.

Néanmoins, cette stabilité a rendu le franc CFA attrayant pour les commerçants et les investisseurs opérant dans la région.

Le débat sur le franc CFA

Les partisans du système du franc CFA soutiennent qu’il fournit une stabilité monétaire, contrôle l’inflation et facilite le commerce régional. Le soutien du Trésor français confère de la crédibilité à la monnaie, attirant potentiellement des investissements étrangers.

Les critiques, cependant, soutiennent qu’il limite la souveraineté économique, entravant la capacité des pays membres à mettre en œuvre des politiques monétaires indépendantes.

L’obligation de conserver 50 % des réserves de change auprès du Trésor français est perçue par certains comme une continuation du contrôle économique de l’ère coloniale. Certains affirment que cela a entravé l’industrialisation et la diversification économique dans les pays membres.

De plus, le taux de change fixe peut rendre les exportations des pays du CFA moins compétitives lorsque l’euro est fort.

Le contraste entre la zone franc CFA et le reste de l’Afrique est frappant en ce qui concerne la stabilité monétaire.

Alors que des pays comme le Ghana, la Sierra Leone et le Nigeria sont confrontés à une inflation galopante et ont vu leurs monnaies se déprécier de plus de 45 % par rapport au dollar américain depuis janvier 2022, le franc CFA a maintenu sa valeur grâce à son ancrage à l’euro.

La stabilité offerte par le franc CFA en fait une option attrayante pour les entreprises et les investisseurs cherchant à se prémunir contre les risques de change dans la région.

Un exemple de ce phénomène peut être observé dans le comportement des commerçants nigérians. Des rapports récents indiquent que les commerçants du nord du Nigeria vendent de plus en plus de grains et d’autres produits à des pays du franc CFA comme le Niger, le Cameroun et le Tchad.

Cette tendance est motivée par la stabilité relative du franc CFA par rapport à la volatilité du naira nigérian.

Alors que le naira a connu une dépréciation significative, les commerçants trouvent que vendre en francs CFA leur permet de préserver la valeur de leurs revenus. Dans certains cas, un commerçant vendant des grains au Niger peut potentiellement doubler ou tripler son profit par rapport à la vente au Nigeria, simplement en raison des différences de taux de change.

Cependant, cette situation met également en lumière des dynamiques économiques régionales complexes. Bien qu’elle soit bénéfique pour les commerçants individuels à court terme, de telles pratiques peuvent entraîner des pénuries alimentaires et des hausses de prix dans des pays comme le Nigeria, déstabilisant potentiellement les marchés et les économies locales.

Se couvrir avec le franc CFA : Implications pour les investisseurs

Pour les investisseurs et les entreprises opérant en Afrique, le franc CFA présente à la fois des opportunités et des défis. Sa stabilité en fait une option attrayante pour ceux qui cherchent à minimiser le risque de change.

Cependant, la flexibilité limitée de la monnaie et le potentiel de changements politiques soudains doivent être pris en compte lors de la prise de décisions d’investissement à long terme.

Les entreprises opérant dans plusieurs pays africains peuvent trouver que la zone franc CFA est une base utile pour les opérations régionales, leur permettant d’éviter certains des problèmes de conversion de devises rencontrés dans d’autres parties du continent. Mais elles doivent également être conscientes des limitations potentielles de croissance et de compétitivité liées à un taux de change fixe.

En 2019, il a été annoncé que le franc CFA de l’Afrique de l’Ouest serait renommé « Eco » dans le cadre d’un plan visant à réduire progressivement l’implication française dans la monnaie. Cependant, la mise en œuvre de ce changement a été retardée, et les détails de la transition restent flous.

Alors que les nations africaines continuent de rechercher une plus grande indépendance économique et une intégration régionale, l’avenir du franc CFA reste un sujet de discussion intense. L’histoire de cette monnaie est en fin de compte celle des compromis entre stabilité et souveraineté, entre intégration régionale et politique économique nationale.

À mesure que les économies africaines continuent de croître et d’évoluer, le rôle du franc CFA – et la question plus large de la politique monétaire dans la région – restera sans aucun doute au centre des discussions économiques et politiques dans les régions de l’UEMOA et de la CEMAC.

The CFA Franc has become a strategic hedge to navigate Africa’s currency crisis. Here’s why the euro-pegged currency is a safe haven.

In the face of widespread currency instability across Africa, the CFA Franc stands out as a beacon of relative stability.

This currency, used by 14 African countries, has become a strategic hedge for traders and investors seeking to navigate the turbulent waters of the continent’s ongoing currency crisis.

To understand its significance, we must first delve into the history and structure of the CFA Franc system, before examining how it functions in the context of Africa’s broader economic challenges.

What is the CFA Franc?

The CFA Franc, which stands for “Communauté Financière Africaine” (African Financial Community) in West Africa and “Coopération Financière en Afrique Centrale” (Financial Cooperation in Central Africa) in Central Africa, has a history dating back to the colonial era.

Created by France in 1945 for its colonies following World War II, the currency has evolved but maintained its core structure.

Today, the CFA Franc is divided into two distinct but similarly valued currencies: the West African CFA franc (XOF) used by eight countries in the West African Economic and Monetary Union (WAEMU), and the Central African CFA franc (XAF) used by six countries in the Central African Economic and Monetary Union (CEMAC).

The key feature of the CFA Franc is its fixed exchange rate with the euro.

Initially pegged to the French franc, it transitioned to a euro peg in 1999 when France adopted the euro. This transition maintained the currency’s stability while shifting its anchor to the broader European monetary system.

While XOF and XAF have the same value and euro peg, they are separate currencies used in different regions.

XOF circulates in West Africa (WAEMU countries), while XAF is used in Central Africa (CEMAC countries). Despite being theoretically interchangeable, they are typically not used outside their respective zones.

Despite being separate currencies, both XOF and XAF have the same value and are pegged to the euro at a fixed rate of 1 euro to 655.96 CFA francs.

This unique monetary system in Africa provides a level of stability that is rare in many African economies, which often face severe currency volatility but has also sparked debate about economic sovereignty.

Which Countries Use the CFA Franc?

The CFA Franc is used by 14 countries across two monetary unions.

The West African Economic and Monetary Union (WAEMU) includes Benin, Burkina Faso, Côte d’Ivoire, Guinea-Bissau, Mali, Niger, Senegal, and Togo.

The Central African Economic and Monetary Union (CEMAC) comprises Cameroon, Central African Republic, Chad, the Republic of Congo, Equatorial Guinea, and Gabon.

These nations collectively represent a significant portion of sub-Saharan Africa’s economy.

As of the time of writing, the exchange rate is approximately 595 CFA francs to 1 US dollar.

However, it’s important to note that the CFA franc’s value is directly tied to the euro, not the dollar, so this rate can fluctuate based on euro-dollar exchange rates.

Nevertheless, this stability has made the CFA Franc an attractive option for traders and investors operating in the region.

The CFA Franc Debate

Proponents of the CFA Franc system argue that it provides monetary stability, controls inflation, and facilitates regional trade. The backing by the French Treasury lends credibility to the currency, potentially attracting foreign investment.

Critics however argue that it limits economic sovereignty, hindering member countries’ ability to implement independent monetary policies.

The requirement to keep 50% of foreign exchange reserves with the French Treasury is seen by some as a continuation of colonial-era economic control. Some argue this has hindered industrialization and economic diversification in member countries.

In addition, the fixed exchange rate can make exports from CFA countries less competitive when the euro is strong.

The contrast between the CFA Franc zone and the rest of Africa is stark when it comes to currency stability.

While countries like Ghana, Sierra Leone, and Nigeria grapple with soaring inflation and have seen their currencies depreciate by over 45% against the US dollar since January 2022, the CFA Franc has maintained its value due to its euro peg.

The stability offered by the CFA Franc has made it an attractive option for businesses and investors looking to hedge against currency risks in the region.

An example of this phenomenon can be observed in the behavior of Nigerian traders. Recent reports indicate that traders in northern Nigeria are increasingly selling grains and other commodities to CFA Franc countries like Niger, Cameroon, and Chad.

This trend is driven by the relative stability of the CFA Franc compared to the volatility of the Nigerian naira.

As the naira has experienced significant depreciation, traders find that selling in CFA francs allows them to preserve the value of their earnings. In some cases, a trader selling grains in Niger can potentially double or triple their profit compared to selling in Nigeria, simply due to the exchange rate differences.

However, this situation also highlights complex regional economic dynamics. While beneficial for individual traders in the short term, such practices can lead to food shortages and price increases in countries like Nigeria, potentially destabilizing local markets and economies.

Hedging with CFA Franc: Implications for Investors

For investors and businesses operating in Africa, the CFA Franc presents both opportunities and challenges. Its stability makes it an attractive option for those looking to minimize currency risk.

However, the limited flexibility of the currency and the potential for sudden policy changes should be considered when making long-term investment decisions.

Companies operating across multiple African countries may find the CFA Franc zone a useful base for regional operations, allowing them to avoid some of the currency conversion issues faced in other parts of the continent. But they must also be aware of the potential limitations on growth and competitiveness that come with a fixed exchange rate.

The debate surrounding the CFA Franc continues to evolve.

In 2019, it was announced that the West African CFA Franc would be renamed the “Eco” as part of a plan to gradually decrease French involvement in the currency. However, the implementation of this change has been delayed, and the details of the transition remain unclear.

As African nations continue to seek greater economic independence and integration, the future of the CFA Franc remains a topic of intense discussion. The currency’s story is ultimately one of trade-offs between stability and sovereignty, between regional integration and national economic policy.

As Africa’s economies continue to grow and evolve, the role of the CFA Franc – and the broader question of monetary policy in the region – will undoubtedly remain at the forefront of economic and political discussions in the WAEMU and CEMAC regions.

Les membres du bloc régional comprennent les huit pays francophones de l’Afrique de l’Ouest et offrent des leçons pour les efforts d’intégration régionale sur le continent.

L’Union Économique et Monétaire Ouest-Africaine, communément connue sous son acronyme français UEMOA ou son acronyme anglais WAEMU (West African Economic and Monetary Union), est une organisation régionale importante en Afrique de l’Ouest.

Cet article fournit un aperçu de l’UEMOA, abordant les aspects clés de sa structure, de ses fonctions et de son impact sur l’intégration régionale.

Combien de pays font partie de l’UEMOA ?

L’UEMOA comprend huit États membres : le Bénin, le Burkina Faso, la Côte d’Ivoire, la Guinée-Bissau, le Mali, le Niger, le Sénégal et le Togo.

L’union a été officiellement établie le 10 janvier 1994, en s’appuyant sur les fondations de l’Union Monétaire Ouest-Africaine (UMOA) créée en 1962. La Guinée-Bissau a rejoint en 1997, portant le groupe initial de sept à huit membres.

Quel est le but et les fonctions de l’UEMOA ?

L’objectif principal de l’UEMOA est de promouvoir l’intégration économique entre ses États membres. Elle vise à créer un espace économique harmonisé et intégré en Afrique de l’Ouest, assurant la libre circulation des personnes, des capitaux, des biens, des services et des facteurs de production.

L’union s’efforce d’améliorer la compétitivité des économies membres dans le cadre d’un marché ouvert et compétitif, tout en simplifiant et harmonisant l’environnement juridique dans la région.

Les fonctions clés de l’UEMOA incluent :

La coordination des politiques économiques et monétaires

La mise en œuvre de politiques sectorielles communes

L’harmonisation de la législation, notamment en matière de fiscalité

La création d’un marché commun

La coordination des politiques macroéconomiques nationales

Quelle est la monnaie de l’UEMOA ?

Les pays de l’UEMOA partagent une monnaie commune, le franc CFA de l’Afrique de l’Ouest (XOF).

Cette monnaie est arrimée à l’euro, un héritage des liens coloniaux de la région avec la France. La Banque Centrale des États de l’Afrique de l’Ouest (BCEAO) gère la politique monétaire pour tous les membres de l’UEMOA.

L’utilisation d’une monnaie commune vise à faciliter le commerce et l’investissement au sein de l’union en éliminant les risques de change et en réduisant les coûts de transaction.

Cependant, cela signifie également que les pays membres ne peuvent pas ajuster indépendamment leurs politiques monétaires pour faire face à des défis économiques spécifiques à leur pays.

Le franc CFA est arrimé à l’euro, un héritage des liens coloniaux de la région avec la France.

Différences entre l’UEMOA et la CEDEAO

Alors que l’UEMOA se concentre sur l’intégration économique et monétaire entre ses huit membres francophones, la Communauté Économique des États de l’Afrique de l’Ouest (CEDEAO) est un groupe régional plus large qui comprend tous les pays de l’UEMOA plus sept autres.

La CEDEAO vise une coopération régionale et une intégration plus larges, au-delà des seules questions économiques.

Les différences clés incluent :

Portée : L’UEMOA se concentre principalement sur l’intégration économique et monétaire, tandis que la CEDEAO a un mandat plus large incluant la coopération politique et la sécurité.

Adhésion : L’UEMOA compte 8 membres, tous utilisant le franc CFA, tandis que la CEDEAO compte 15 membres avec diverses monnaies.

Niveau d’intégration : L’UEMOA a atteint une intégration économique plus profonde, y compris une monnaie commune et des politiques économiques harmonisées, tandis que la CEDEAO travaille encore à atteindre ces objectifs.

L’UEMOA offre plusieurs avantages potentiels à ses États membres :

Stabilité monétaire : La monnaie commune et la politique monétaire partagée visent à assurer la stabilité des prix et des taux d’inflation faibles dans toute la région.

Facilitation du commerce : L’élimination des risques de change et la réduction des coûts de transaction devraient théoriquement promouvoir le commerce intra-régional.

Coordination des politiques économiques : Des politiques économiques harmonisées peuvent conduire à des environnements d’affaires plus stables et prévisibles dans toute la région.

Pouvoir de négociation collectif : En tant que bloc, les pays de l’UEMOA peuvent avoir une position de négociation plus forte dans les affaires économiques internationales.

Développement des infrastructures régionales : L’union peut coordonner et financer des projets d’infrastructure régionaux qui bénéficient à plusieurs États membres.

Un élément important de l’intégration financière de l’UEMOA est la Bourse Régionale des Valeurs Mobilières (BRVM).

Établie en 1998 et ayant son siège à Abidjan, en Côte d’Ivoire, la BRVM est une bourse régionale unique au monde servant les huit pays membres de l’UEMOA. C’est la seule bourse au monde qui dessert plusieurs pays avec une monnaie commune.

La BRVM joue un rôle crucial dans l’écosystème financier de l’UEMOA en offrant une plateforme permettant aux entreprises de lever des capitaux et aux investisseurs d’échanger des titres dans toute la région. Elle propose une variété d’instruments financiers, y compris des actions, des obligations et d’autres titres.

La bourse fonctionne en français, reflétant la langue prédominante de la région de l’UEMOA, et toutes les transactions sont effectuées dans la monnaie commune du franc CFA.

Malgré son potentiel, la BRVM fait face à des défis typiques des marchés frontières, notamment une liquidité limitée et un nombre relativement restreint de sociétés cotées. Cependant, elle représente une étape significative vers l’intégration financière au sein de l’UEMOA et a le potentiel de devenir un outil de plus en plus important pour mobiliser des capitaux pour le développement régional.

À mesure que l’UEMOA poursuit son intégration économique, le rôle de la BRVM dans la facilitation de l’investissement transfrontalier et la fourniture d’une plateforme régionale pour la levée de capitaux est susceptible de croître en importance.

Leçons de l’UEMOA en matière d’intégration régionale

L’expérience de l’UEMOA offre plusieurs leçons importantes pour les efforts d’intégration régionale :

Une union monétaire à elle seule ne suffit pas : Malgré le partage d’une monnaie commune, les pays de l’UEMOA n’ont pas vu l’augmentation attendue du commerce ou de l’investissement intra-régional. Cela suggère que d’autres obstacles, tels que l’infrastructure inadéquate et les procédures douanières complexes, jouent un rôle important dans l’entrave à l’intégration économique régionale.

La diversité économique est importante : Les pays de l’UEMOA ont des structures économiques similaires, souvent en concurrence sur les mêmes marchés d’exportation plutôt que de se compléter. Cela limite le potentiel de commerce intra-régional et de diversification économique.

Les dépendances extérieures persistent : Les liens économiques continus de la région avec la France et l’ancrage à l’euro ont été critiqués pour limiter la souveraineté économique et la flexibilité.

La volonté politique est cruciale : Une intégration réussie nécessite un engagement politique soutenu de la part de tous les États membres pour mettre en œuvre et faire respecter les politiques convenues.

Équilibrer les intérêts nationaux et régionaux : L’expérience de l’UEMOA souligne les défis consistant à aligner les priorités économiques nationales diverses sur les objectifs d’intégration régionale.

Besoin d’une approche globale : Une intégration régionale efficace nécessite de s’attaquer simultanément à plusieurs facteurs, notamment le développement des infrastructures, l’harmonisation des réglementations et la suppression des barrières non tarifaires.

Importance de la surveillance et de l’application : La mise en œuvre des politiques et des accords régionaux doit être constamment surveillée et appliquée pour atteindre les résultats escomptés.

Malgré son existence de longue date, l’UEMOA fait face à plusieurs défis. Le commerce intra-régional reste relativement faible, et les économies des membres continuent d’être fortement dépendantes des exportations de matières premières vers les marchés en dehors de l’Afrique. La région est également confrontée à des problèmes de sécurité, en particulier dans la région du Sahel, qui affectent les activités économiques et les efforts d’intégration.

À l’avenir, l’UEMOA travaille à approfondir l’intégration grâce à des initiatives telles que la création d’une bourse régionale et les efforts pour harmoniser les lois commerciales. L’union se concentre également de plus en plus sur la coopération en matière de sécurité, reconnaissant le lien entre la stabilité et le développement économique.

En conclusion, l’UEMOA représente une tentative ambitieuse d’intégration économique régionale en Afrique de l’Ouest. Bien qu’elle ait obtenu certains succès, notamment en matière de stabilité monétaire, l’expérience de l’union souligne les complexités de l’intégration régionale.

Alors que l’Afrique se dirige vers une intégration continentale plus large grâce à des initiatives telles que la Zone de libre-échange continentale africaine (ZLECAf), les leçons de l’UEMOA seront précieuses pour façonner des stratégies efficaces de coopération économique et de développement à travers le continent.

The regional bloc’s members include the eight francophone West African countries and offers lessons for regional integration efforts on the continent.

The West African Economic and Monetary Union, commonly known by its French acronym UEMOA (Union Économique et Monétaire Ouest-Africaine) or its English acronym WAEMU, is a significant regional organization in West Africa.

This article provides an overview of WAEMU, addressing key aspects of its structure, functions, and impact on regional integration.

How Many Countries are in the WAEMU?

WAEMU comprises eight member states: Benin, Burkina Faso, Côte d’Ivoire, Guinea-Bissau, Mali, Niger, Senegal, and Togo.

The union was officially established on January 10, 1994, building upon the foundation of the West African Monetary Union (UMOA) created in 1962. Guinea-Bissau joined in 1997, expanding the initial group of seven to eight members.

What is the Purpose and Functions of WAEMU?

WAEMU’s primary objective is to foster economic integration among its member states. It aims to create a harmonized and integrated economic space in West Africa, ensuring the free movement of people, capital, goods, services, and factors of production.

The union works towards enhancing the competitiveness of member economies within an open and competitive market framework, while also streamlining and harmonizing the legal environment across the region.

WAEMU countries share a common currency, the West African CFA franc (XOF).

This currency is pegged to the euro, a legacy of the region’s colonial ties to France. The Central Bank of West African States (BCEAO) manages the monetary policy for all WAEMU members.

The use of a common currency is intended to facilitate trade and investment within the union by eliminating exchange rate risks and reducing transaction costs.

However, it also means that member countries cannot independently adjust their monetary policies to address country-specific economic challenges.

The CFA Franc is pegged to the euro, a legacy of the region’s colonial ties to France.

Differences Between WAEMU and ECOWAS

While WAEMU is focused on economic and monetary integration among its eight francophone members, the Economic Community of West African States (ECOWAS) is a larger regional group that includes all WAEMU countries plus seven others.

ECOWAS aims for broader regional cooperation and integration beyond just economic matters.

The key differences include:

Scope: WAEMU focuses primarily on economic and monetary integration, while ECOWAS has a broader mandate including political cooperation and security.

Membership: WAEMU has 8 members, all of which use the CFA franc, while ECOWAS has 15 members with various currencies.

Depth of integration: WAEMU has achieved deeper economic integration, including a common currency and harmonized economic policies, while ECOWAS is still working towards these goals.

An important element of WAEMU’s financial integration is the Bourse Régionale des Valeurs Mobilières (BRVM), or Regional Securities Exchange.

Established in 1998 and headquartered in Abidjan, Côte d’Ivoire, the BRVM is a unique regional stock exchange serving all eight WAEMU member countries. It’s the only stock exchange in the world that serves multiple countries with a common currency.

The BRVM plays a crucial role in WAEMU’s financial ecosystem by providing a platform for companies to raise capital and for investors to trade securities across the region. It lists a variety of financial instruments, including stocks, bonds, and other securities.

The exchange operates in French, reflecting the predominant language of the WAEMU region, and all transactions are conducted in the common CFA franc currency.

Despite its potential, the BRVM faces challenges typical of frontier markets, including limited liquidity and a relatively small number of listed companies. However, it represents a significant step towards financial integration within WAEMU and has the potential to become an increasingly important tool for mobilizing capital for regional development.

As WAEMU continues to pursue economic integration, the role of the BRVM in facilitating cross-border investment and providing a regional platform for capital raising is likely to grow in importance.

WAEMU’s experience offers several important lessons for regional integration efforts:

Currency union alone is not sufficient: Despite sharing a common currency, WAEMU countries have not seen the expected boost in intra-regional trade or investment. This suggests that other barriers, such as inadequate infrastructure and complex customs procedures, play a significant role in hindering regional economic integration.

Economic diversity matters: WAEMU countries have similar economic structures, often competing in the same export markets rather than complementing each other. This limits the potential for intra-regional trade and economic diversification.

External dependencies persist: The region’s continued economic ties to France and the euro peg have been criticized as limiting economic sovereignty and flexibility.

Political will is crucial: Successful integration requires sustained political commitment from all member states to implement and enforce agreed-upon policies.

Balancing national and regional interests: The experience of WAEMU highlights the challenges of aligning diverse national economic priorities with regional integration goals.

Need for comprehensive approach: Effective regional integration requires addressing multiple factors simultaneously, including infrastructure development, harmonization of regulations, and removal of non-tariff barriers.

Importance of monitoring and enforcement: The implementation of regional policies and agreements needs to be consistently monitored and enforced to achieve desired outcomes.

Despite its long-standing existence, WAEMU faces several challenges. Intra-regional trade remains relatively low, and member economies continue to be heavily dependent on commodity exports to markets outside Africa. The region also grapples with security issues, particularly in the Sahel, which impact economic activities and integration efforts.

Looking ahead, WAEMU is working on deepening integration through initiatives like the creation of a regional stock exchange and efforts to harmonize business laws. The union is also increasing its focus on security cooperation, recognizing the link between stability and economic development.

In conclusion, WAEMU represents an ambitious attempt at regional economic integration in West Africa. While it has achieved some successes, particularly in maintaining monetary stability, the union’s experience underscores the complexities of regional integration.

As Africa moves towards broader continental integration through initiatives like the African Continental Free Trade Area (AfCFTA), the lessons from WAEMU will be valuable in shaping effective strategies for economic cooperation and development across the continent.

I have long been a fan of DFS Lab, the “research-driven venture capital in Africa”.

It’s the only VC firm on the continent that consistently shares – publicly and transparently – nuanced, long-form reflections around its investment thesis.

By doing that, they gifted the ecosystem not just with high-quality articles, but new terms/concepts to describe & make sense of tech in Africa.

Kudos to them! 💥

In a world defined by information overload and sensationalism, mental clarity is one of the most underrated qualities we should consciously strive to cultivate.

How do you know what you know? What is the deep meaning of it? If you cut through the noise, what do you see?

Trying to answer these questions – peeling all the layers of opaqueness – most people would find themselves naked.

This is why, drawing inspiration from the Almanack of Naval Ravikant, I am happy to propose – for the first time – the Almanack of DFS Lab: 6 theoretical primitives to make sense of VC investing in Africa.

These are six concepts coined by the firm that I find extremely insightful/useful in my activities as a researcher/investor:

The Frontier Blindspot

Fortune at the middle of the pyramid

The B-side of African Tech

Cyborgs vs Androids

Invested infrastructure

African S-curves

The original articles are all available on the DFS Lab website and Medium page.

My contribution mainly consists of summarizing my understanding of them & complementing them with my own ideas.

Lessgò.

Subscribe

1) The Frontier Blindspot 👀

Premise: The world has developed “intuitions about how technology markets are structured and what successful technology companies look like”. Cool.

However: this learning process took place strictly in the context of Western economies.

Ergo: the same frameworks do not always apply to frontier markets (like Africa).

Thesis: the disconnect between how we think tech is supposed to work versus how it really works – in Africa & other frontier markets – is the Frontier Blindspot! 💥

It is a blindspot because we are partially clueless – how tech markets work or don’t work in Africa has yet to be demonstrated. As we cannot copy-paste, learning happens by trial and error, thorough research, and on-the-ground experience.

What type of bias did we borrow from the Global North when making our assumptions about tech in Africa?

we overestimated the pace of digitalization;

we underestimated the strength of informal markets;

we overlooked the state of infrastructure and consumer purchasing power

When you factor in low-paced digitalization, strong informal markets, and quirky infra, you’ll see that a lot of common startup wisdom about business models, distribution strategies, and growth projections, won’t apply to the continent.

However, local entrepreneurs are still finding unique ways to apply the “modern startup stack” to the specifics of the African environment.

This is where the real opportunities are, and the areas of excitement include:

Physical logistics

SME solution stack

Financial building blocks

Agent networks

Although these things may seem obvious today, I think they are still not obvious to many, and they certainly were not obvious in 2020 (when the article came out).

What I find particularly useful about this piece is stressing the differences in infrastructure and purchasing power. When looking at pitch decks, I try stress the following questions:

what needs to be there for your product to be made, consumed, or delivered? (read: infrastructure)

How many people can buy your product, regularly? How do you know it?

We are about to have a taste of it with the next concept ✨

Who is the African consumer & what is the real size of the African market for digital products?

Hashtag: debunking the (once) popular tag “Nigeria is a market of 200M people” with some rigorous thinking.

Why?

Because population size does not equal market size, we cannot boast “the youngest population in the world” without looking at income brackets too.

Let’s proceed in order.

“Most B2C tech startups are seeking to make money from people’s discretionary spending”

Discretionary spending is the spending power that remains once covered for necessities like food, clothing, and shelter.

The question asked is: among the 200M fellow Nigerians, how many have the discretionary spending for my type of product?

In the image below, we can look at income levels and their percentage of discretionary income (in Africa).

Source: Fortune at the middle of the pyramid

If you are a B2C startup, what is the juiciest segment?

As a fairly coherent group, the people earning between $5-$10 – while comprising only ~10% of the population – have one of the highest discretionary spending power combined.

This is the fortune at the middle of the pyramid: the segment having enough people, with enough discretionary spending power. To the left of the curve, there are a lot of people but with little money; to the right, they have a lot of money but they are too few.

Now, speaking of unit economics: how much does it cost to acquire these customers? Here things get trickier.

In Africa, higher incomes are usually digitally-fluent city dwellers. Their geographical concentration, professional status, and greater online life, make them perfect targets for digital acquisition strategies. The same doesn’t necessarily hold for lower-income prospects: acquiring them is harder and costs more (with traditional digital methods).

To this comes a paradox: if the cost of acquiring a new customer is way more than what you earn from them, you will soon move to serve higher-income consumers. However, if you only serve the +10$ income bracket, at some point, growth will stall and you’ll need to move cross-border (not easy).

What can we learn from all we just stayed?

purely consumer-focused apps that do not focus on necessities (read: targeting discretionary spending) face unique challenges with monetization in Africa. This is because

the largest economic opportunity sits within the 5-10$ bracket, but the cost of acquiring them is high due to lower digital presence.

Moving forward, I think two very important corollaries emerge about “how to be successful”:

build apps focused on necessities, or focused on the business equivalent of “necessities” (restocking, working capital, inventory etc..);

if you target consumers’ discretionary spending, invest in human agent networks, the physical point of entry to most digital experiences for middle-of-the-pyramid Africans.

Personally, whenever I look at the pitch deck of a B2C company:

if they target offline acquisition, it means they are serving the middle of the pyramid;

if they don’t mention offline acquisition, it means they are serving the top of the pyramid.

Hence, I’ll start to wonder. Given the risk and the complexities of moving cross-border, can they make money (read: positive operating profit) before moving cross-border?

Enjoying the article so far? Share it with bruvs and siss 💥

This article draws inspiration from Wang Huiwen, the co-founder of Meituan Dianping, the most successful Chinese food delivery company, turned super-app.

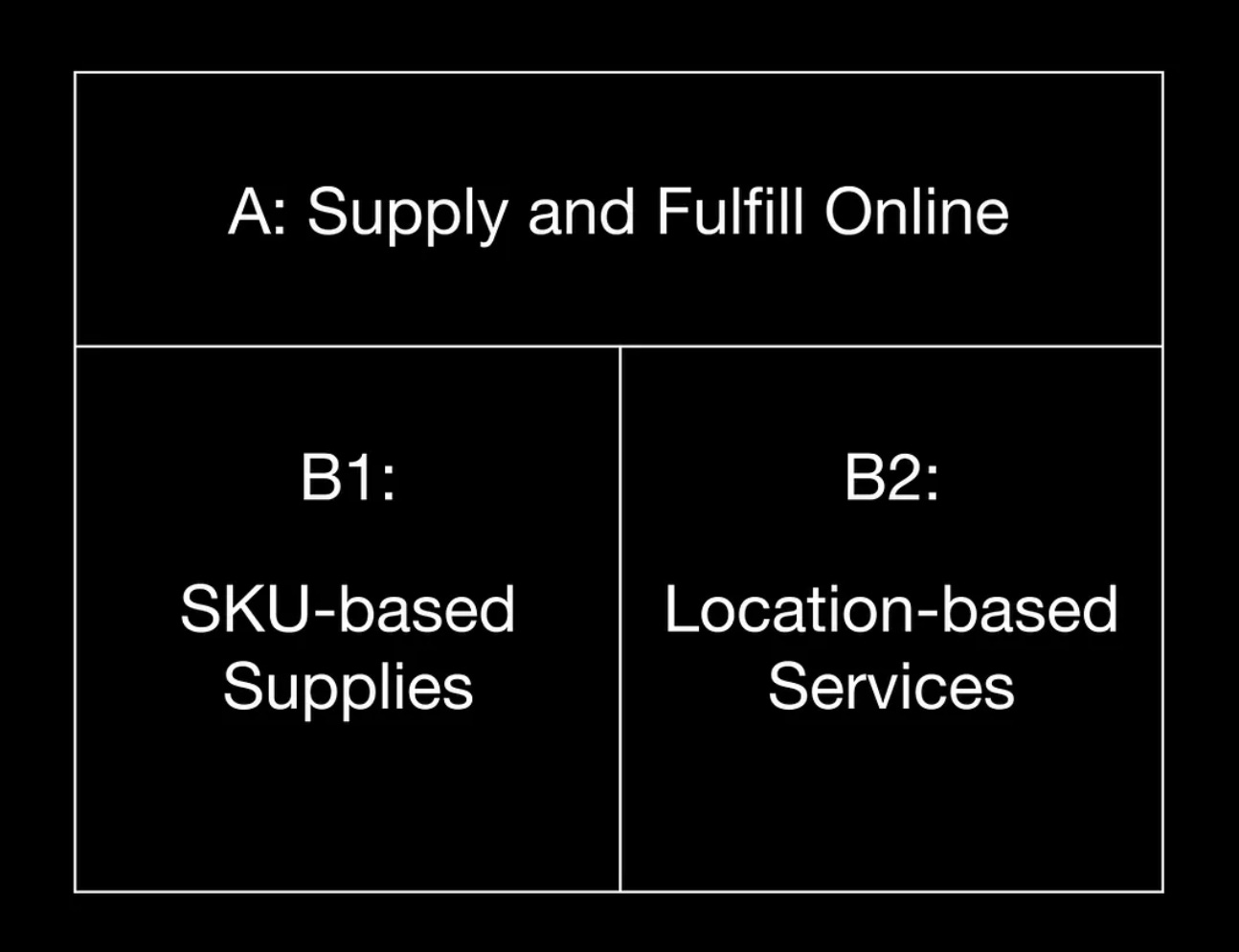

In an issue of the newsletter “The China Playbook”, Huiwen defines the internet industry as made of two sides:

A-side: Supply and Fulfill Online

B-Side: Supply and Fulfill Offline

Side-A is products and services that are “pure internet”, as they can be delivered and consumed entirely online. SaaS (Salesforce), video-games (Voodoo), streaming (Spotify), etc…

Side-B is products and services that are delivered offline and consumed offline. Think of retail (Amazon), mobility (Uber), ticketing (Ticketmaster), etc…

If we have to apply this distinction to African economies, we would see that side-A (online utility) is smaller, compared to side B (offline utility).

The reason is that “fully digital experiences are either inaccessible, unaffordable or don’t cover the primary consumption needs for those in the bottom 95%.”

Ok cool. Let’s have a closer look at the B-side then. The B-side can be further divided into two sub-sections:

B1: SKU-based supplies

B2: location-based services

B1 is companies like Wasoko, Omniretail, and other traditional marketplaces. As digital businesses positioning in between the sourcing & delivery of physical products, their core competencies lie in ”understanding SKUs (stock keeping unit), understanding the supply chain, and understanding pricing”.

B2 is companies like Hubtel and Wahu Mobility. They are location-centric, as the physical location of customers & partners is a key element of their value proposition. For example, a ride-hailing company like Uber will need to recruit drivers in your city and ensure there are enough in your area as you order a ride – otherwise, you won’t be able to access their service. B2 businesses demand a larger offline team to manage operations closer to the customers.

What learnings do we have here?

B1 leverages technology to “improve the efficiency of existing value flows and reorganize pricing power”. On the contrary, “B2 is physical ubiquity”.

Let’s stop here.

In the article, Stephen Deng (DFS Lab MP) expands on the original concept expressed by Meituan Dianping founder.

When Wang Huiwen talks about B2 “location-based businesses”, he is primarily referring to ride-hailing, bike-sharing, and food-delivery, products made accessible by smartphone proliferation, which unlocked & democratized location data. These businesses are useful because you can see your location with your phone, and other people can see it too.

Deng however, twists its meaning for the African context, attaching to it the familiar notion of physical ubiquity: B2 businesses are interesting because of their physical proximity to the customers, mobilizing people and resources last-mile. Other than delivery, one can think of mobile money agents and social commerce as a form of B2 businesses. Their utility comes from their ability to integrate kiosks and people from your neighborhood in their business model. They are relatable, they are next door.

In short, they are more similar to Cyborgs, instead of Androids. What?

You read correctly. The concept of “B-Side of African Tech” is strictly intertwined with that of “Androids vs Cyborgs”, that we explore in the next section (before wrapping up with my two cents on this stuff).

Androids: solutions that replace informal markets with digital, formalized parts and processes

Cyborgs: solutions that enhance informal markets by arming them with digital, formalized parts and processes

Androids use tech to replace a set of existing actors.

Cyborgs use tech to improve the work of a set of existing actors.

Stephen Deng claims that we cannot brute force androids into existence if we are incapable of replacing informal players with significantly better solutions. And if we can’t replace them, we’d better empower them by building cyborgs.

It might seem like a B2C (Android) vs B2B (Cyborgs) play, but it’s more nuanced than that. Examples?

The ultimate Android example is Jumia and all Amazon-inspired B2C marketplaces: “replacing the local market with an online option that is meant to be more convenient, have more options, and is fully digitized”.

However, I think the same holds for many agri-tech platforms (like Complete Farmer or Winich Farms) that aggregate farmers’ produce and facilitate access to market & agro-inputs. In almost every pitch deck you will read about them “cutting out the middlemen”, the set of informal buyers and sellers who move crops to markets, whose commissions eat out farmers’ margins and drive inefficiencies (btw these platforms raised a lot of funds, but it’s not clear to me how much money they are making).

Cyborgs, on the contrary, look like tools that empower small businesses, applying a mix of online and offline. Instead of replacing existing relationships, they “supercharge them with digital optionality when the need arises”.

Both B2-side businesses and Cyborgs, tell the same story: existing structures can be valuable when they are empowered, instead of substituted.

Ok, but empowered how?

In my opinion, an online-offline Cyborg approach, can only be one of two things:

cost-effective offline distribution and/or marketing – agents knocking on doors or setting up shops;

tech-enabled intermediaries/retailers – empowered by a digital backend or specialized hardware.

That’s it!

Moniepoint is Africa’s fastest-growing fintech. Its distribution model? An army of human agents armed with PoS devices, knocking on merchants’ doors. The company revolutionized the capacity for Nigerian businesses to collect digital payments.

→ a Cyborg approach to digital payments.

Retailers’ bookkeeping apps like Oze and supply-chain management tools like Jetstream, both started as digital super-charger of African businesses: I give you tools to better manage invoices and logistics. Fast forward a couple of years, and they both ended up embedding credit and solving the pain of access to capital.

→ a Cyborg approach to digital lending.

I think Cyborg either means giving more “legs and arms” for asset-light digital businesses, or making “legs and arms” (SMBs) more competitive with digital tools.

Digital solution → leave a digital trace → data + learning models → better decision making

Digital solution → relational database & data integration → operational efficiencies

Digital solution → composable software stack → APIs & integrations → new products/services delivered on top of the main product

🪄🪄🪄

More in general, I think that both the “B-Side” and “Android vs Cyborg” arguments tend to over-emphasize the promises of the physical ubiquitous approach, without addressing the elephant in the room: we need more hardware.

A lot of things can be done with your phone, but not everything can be done with your phone, and sometimes, a phone is too much.

Limited storage/memory, weak bandwidth, and high data costs still represent hard limits to app utility for the average African business operator. A phone can do a lot, but not everything.

Safiri is a Tanzanian company equipping bus companies with thermal printers, and customers with digital ticket purchase options. They record transactions “digitally”, and print tickets “physically”. A good blend of digital and physical coming together. No need for Industry 4.0 here, just basic hardware tools.

And yet, I am not seeing enough investors stressing how specialized hardware – as well as consumer hardware – can play its role in the tech landscape.

We need more hardware. We can’t expect to revolutionize the continent simply with apps running on cheap smartphones.

I feel we’ll see major shifts when large-scale hardware manufacturing that truly responds to local business needs comes to fruition.

And yes, somehow, I am still convinced this can be a VC play.

Enjoying the article so far? Subscribe to Data Bites & have more of this 💩Subscribe

The concept is simple, yet powerful: the infrastructure built in the past has a lasting, indelible influence on our present & future.

Economists call it “path dependency”: society builds on top of what has been built, and this process makes us drift toward a trajectory of development and away from others.

In the United States, payment infrastructure has been built “for a time when phones were not as ubiquitous and hard-wired ethernet was increasingly common.”

The proliferation of PoS devices & phone cables (& later fiber cables), gradually made up the physical network on top of which credit cards’ adoption became widespread.

The alternative to cash travels on rails that took a long time to build, but once in place, it is hard to replace. It’s the hidden cost of path dependency: the more we build on top of invested infrastructure, the higher the switching costs to a different system.

“They have since gained ubiquity, and because mobile phone-based services can only offer marginal improvements, the system stays resilient — it is challenging to overcome the inertia of this invested infrastructure”

What is the invested infrastructure in Africa and how will it impact its future?

It is an important question to ask because – as we have seen – companies that leverage invested infrastructure can have a competitive edge, reducing costs and frictions to adoption; those that try to replace it might sink under the weight of high switching costs & behavioral change (although in some cases – boom jackpot 🎰).

If we think of financial infrastructure, in Africa the equivalent of the US card network is a combination of:

a human agent network

phones & SIM cards

tower cells

It hasn’t always been the case. The capillary presence established by telco companies in the continent from the 90s onward, brought along the way important infrastructural development that served as the launchpad to mobile money: financial infrastructure borrowed from the already existing communication infrastructure.

A human agent network could now be used to on-ramp/off-ramp physical cash.

Phones and SIM cards became wallets.

Tower cells relayed information – and now value – across long distances.

Innovation on top of invested infrastructure.

But it’s not over.

As the new payments infrastructure emerged, further developments “up the ladder” could see the light of day: “The combination of USSD-based mobile accounts that worked on every phone and cash-in/cash-out agents in nearly every neighborhood and village proved to be powerful infrastructure on which to build new product offerings”.

The first wave of successful tech businesses on the continent – real “market-creating” innovations – are the product of it.

Examples:

First generation: pay-as-you-go solar (like M-Kopa)

Second generation: digital lending

Access to energy & access to credit. Both are built on top of mobile money infrastructure, built on top of telco’s invested infrastructure.

What lessons can we take home from this chapter?

invested infrastructure matters

it looks different in Africa than in other places

opportunities exist for those who build on top of it + those who make it more efficient

Personally, I find myself asking the question” What’s the invested infrastructure here?”. And not just for payments, but for commerce, logistics, agriculture etc.. In short, it translates to: how things are done now, how much does it cost to switch and who has interest in doing it?

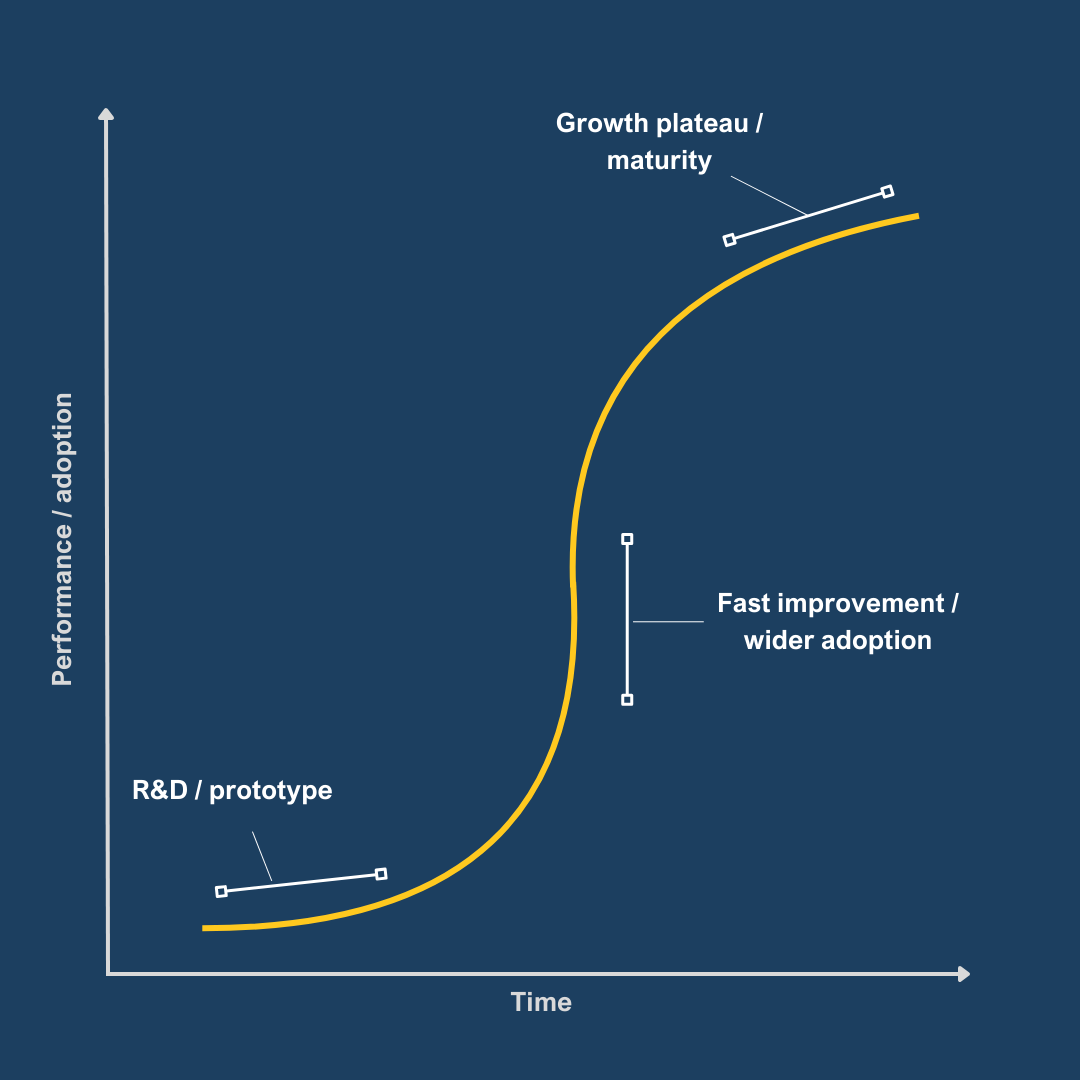

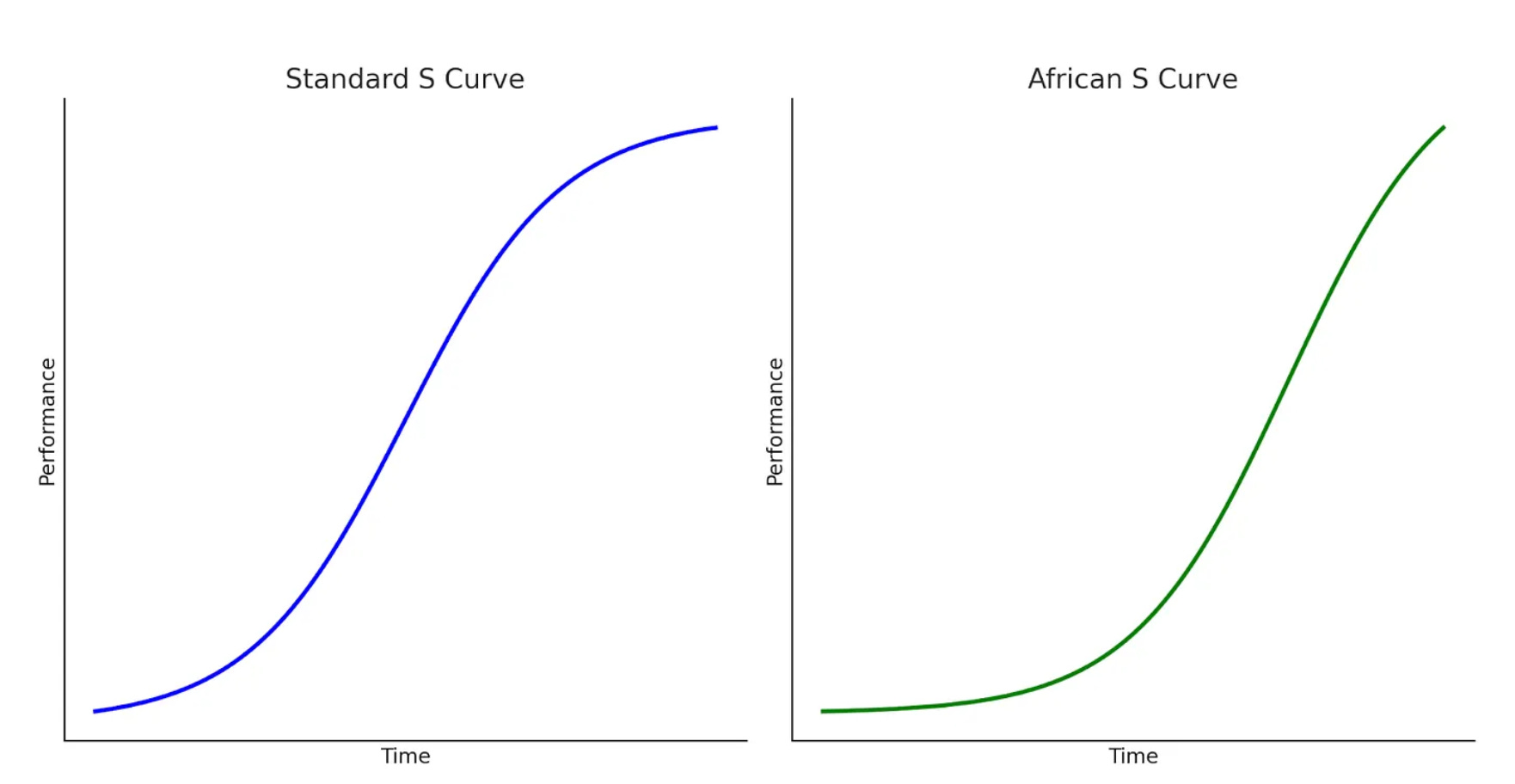

S-curves describe the performance of a new technology – or a technological toolset – over time.

In the beginning, during the R&D and prototyping phase, adoption is minimal and the potential of tech still needs to be validated. The curve is flat and growing slowly. Think of electric cars 15 years ago. It is the territory of university budgets, public finance, and research grants.

When the tech starts showing signs of improvement, it is followed by a steep acceleration in performance and increased adoption. Think of Generative AI one year ago. It is the land of VCs, profiting “by investing in emerging tech before it’s mainstream and exiting when growth plateaus”.

Finally, when a technology is mature, adoption widespread and there is little room for marginal improvements: the tail of the curve flattens. It is the PE and stock market game.

And then, onto the next technology, that will replace the incumbent with the next S-curve. Venture capital funding follows the S-curves cycle, the peak funding being when the curve is at its highest steep.

Now: in the wake of funding drought, startup bankruptcies, and crowding away of international investors, what can we say about the shape of the African S-curve?

One: African S curves have much longer tails.

This means that it takes more time for tech in Africa to see widespread adoption. Rather than a limit to technology performance, the problem lies in the lack of market readiness.

Read: “Customers don’t need new tech, or don’t trust new tech, or can’t afford new tech, or don’t have access to infrastructure for new tech, or don’t believe new tech provides enough value vs. old tech”

Two: African S curves have much steeper slopes

On the contrary, once adoption kicks in, the potential for improvements in technology can last for a very long time, going beyond what was once imagined.

The acceleration phase lasts a long time along with its benefits.

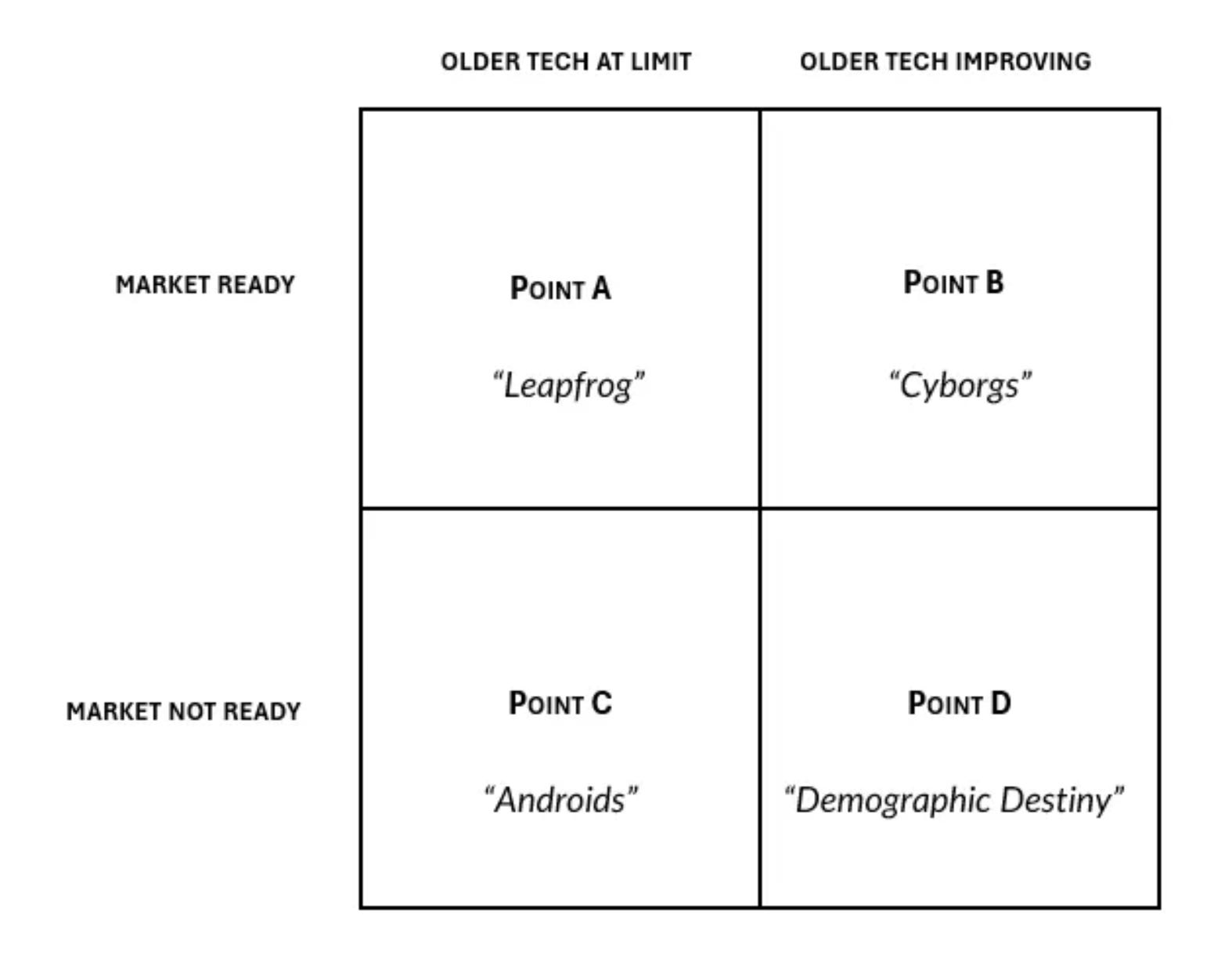

How do we change from one S-curve to the other? When will the new tech replace the old one?

There are 4 different scenarios.

If the old tech is not improving, and the market is ready for a novel solutions, then we’ll have a quick transition. This means heading towards Point A, and what people cheer as Africa’s technology leapfrog.

On the opposite side, if incumbents are delivering increasingly better utility to consumers, who are not ready to change for newcomers, then we’ll have a very gradual and slow transition. Ergo, heading towards Point D.

Many people either bought the point A narrative (technology leapfrog), or buys into point C one. They think old tech is crap, inefficient, and not making any progress. However, the market is not ready for new digital solutions yet. It’s a matter of time.

Stephen Deng, on the contrary, thinks we are heading towards point B. A situation where yes, the market is not ready, but the old tech – and the ecosystem around it – is still improving.

Think of mobile money. It is a fairly old technology ( and USSD codes), but it can still deliver innovation to its users. Telcos are blending digital offerings into their core model; traditional financial services are integrating with the mobile money ecosystem for seamless interactions; new products are developed on top of it every month.

If MoMo is the old tech, the new tech would be close to neo-banks like Djamo. How many customers does one have vs the other?

The shelf life of telecommunications technology has been pretty long. No surprise than that the true champions of tech in the continent are telcos. Companies like MTN, Airtel, Safaricom. This is in stark contrast with the Google, the Meta and the Microsoft of North America.

The main argument is the following: from now on, until we reach point B, a lot of incremental innovations will be built around the existing tech. We need to surf it 🏄🏽♂️

It is what Deng calls the “cybernetic commerce” area, yet another version of the Cyborg thesis.

The most interesting element of this article, to me, is the mental framework that comes with it: how many incremental innovations can still be built on top of the existing rails?

When you look at African markets overall, you’ll see that a lot of problems can be solved with existing technologies. There is no need for a breakthrough.

How to deliver the benefits of tech without losing money: this is the number one skill a founder must have.

This is the end, my friends. I hope you enjoyed the read. Writing this piece I’ve noticed that – as telcos in Africa – my essays have room for improvement. In particular, from now on I will try to deliver:

more real-life examples (what companies, what products etc…) → it helps with mental clarity when you have more than 1/2 examples

more exit simulations (revenues, potential returns) → VC exists where outsized returns exist, and we need to be more rigorous on that.

Contributed by Ajibola Awojobi, founder and CEO of BorderPal.

As the sun rises over Lagos, Adebayo, a young Nigerian fintech entrepreneur, stares at his computer screen. His brow furrowed in concentration and his startup, a mobile money platform to bring financial services to the unbanked, has just secured significant funding from a Silicon Valley venture capital firm. It should be a moment of triumph, but Adebayo feels a gnawing sense of unease. The numbers on his screen tell a troubling story: his company is spending $20 to acquire each new customer, yet the average revenue per user is a mere $7.

Adebayo’s predicament is not unique. Across Africa, fintech startups are grappling with a challenging reality: the cost of customer acquisition often far outweighs the immediate returns. This scenario raises a critical question: Is Africa’s venture capital-backed fintech model sustainable or fundamentally broken?

VCs and the Promise of African Fintech

The African continent has long been considered the next frontier for fintech innovation. With a large unbanked population and rapidly increasing mobile phone penetration, the potential for transformative financial services seemed boundless. Venture capitalists, enticed by the prospect of tapping into a market of over a billion people—half without any formal bank account—have poured billions of dollars into African fintech startups over the past decade.

These investments have fueled remarkable innovations. From mobile money platforms that allow users to send and receive funds with a simple text message, to AI-powered credit scoring systems that enable microloans for small businesses, African fintechs have been at the forefront of financial inclusion efforts.

However, as Adebayo’s experience illustrates, translating these innovations into sustainable businesses has proven to be a formidable challenge.

While Adebayo grapples with his early-stage startup’s challenges, a major African fintech player with a customer base of 300,000 users has just raised a mammoth $150 million, which brings its total funding to nearly $600 million. Based on a customer acquisition cost and revenue per customer established earlier, the economics of this deal seem precarious at best. A quick calculation reveals that the company would have spent around $6 million just to acquire its current user base while generating only $2.1 million. The funding, while impressive, thus raises serious questions about the sustainability of this model and the investors’ expectations.

These scenarios serve as a stark illustration of the broader challenges facing the African fintech sector. It highlights the disconnect between the vast sums of venture capital flowing into the industry and the on-the-ground realities of customer acquisition and revenue generation. For a company to justify such a massive investment, it would need to dramatically increase its user base, significantly reduce its customer acquisition costs, or find ways to generate substantially more revenue per user. Achieving any one of these goals in the complex African market is a tall order; achieving all three simultaneously is unarguably a Herculean task.

The funding also underscores the potential for overvaluation in the African fintech space. While such large investments can provide companies with the runway needed to scale and innovate, they also create immense pressure to deliver returns that may not be realistic given the current state of the market. This pressure could lead to unsustainable growth strategies, prioritizing user acquisition over building a solid economic foundation.

Balancing Profitability & Cost of Growth

The core of the problem lies in the high cost of customer acquisition. According to a McKinsey analysis, some fintech companies in Africa spend up to $20 to onboard a single customer, only to generate $7 in revenue from that customer. This imbalance is staggering and points to deeper structural issues in the market.

Several factors contribute to these high acquisition costs. First, there’s the challenge of digital literacy. Many potential customers, particularly those in rural areas, are unfamiliar with digital financial services. This necessitates extensive education and handholding, driving up the cost of onboarding.

Secondly, Africa’s diverse linguistic and cultural landscape requires tailored marketing approaches for different regions. A strategy that works in urban Lagos may fall flat in rural Tanzania, forcing companies to invest heavily in localized marketing efforts.

Infrastructure challenges also play a significant role. The lack of robust digital infrastructure in many African countries is partly responsible for the high customer acquisition costs. Poor internet connectivity, limited smartphone penetration, and unreliable power supply in some areas make digital onboarding processes more difficult and expensive. Moreover, many consumers are wary of new financial services, requiring significant investments in building trust and credibility.

The high customer acquisition costs are reflected in the overall profitability of digital banks globally. A BCG Consulting analysis revealed that only 13 out of 249 digital banks worldwide, or 5%, are profitable, with 10 of those firms being in the Asia Pacific region. This statistic underscores the challenges digital banks face, particularly in emerging markets like Africa.

This reality presents a conundrum for venture capital firms accustomed to the rapid scaling and quick returns seen in other tech sectors. The traditional VC model, focusing on exponential growth and relatively short investment horizons, may not be well-suited to the realities of building sustainable financial services in Africa.

Rethinking the Model

As awareness of these challenges grows, both entrepreneurs and investors need to rethink their approaches to fintech in Africa, taking into consideration the high cost of acquiring customers and the state of the continent’s digital infrastructure.

One promising avenue is the development of white-label infrastructure. By creating common technological solutions that can be customized and branded by different companies, fintechs can significantly reduce their development costs. This approach could be particularly effective for services like Know Your Customer (KYC) systems or payment processing platforms.

Taking the white-label concept further, an innovative solution is emerging: white-labeled services provided by community leaders with large networks in rural settings. This approach could help fintechs lower the cost of building their customer base. By leveraging the trust and influence of local leaders, companies can reduce the cost of onboarding and education. Word of mouth spreads faster in close-knit communities, potentially accelerating adoption rates and lowering acquisition costs.

Partnerships with established institutions are another strategy gaining traction. By collaborating with banks, telecom companies, or large retailers, fintech startups can leverage existing customer bases and distribution networks, potentially lowering acquisition costs.

Some companies are shifting their focus from B2C to B2B services. Targeting businesses rather than individual consumers could lead to lower acquisition costs and higher average revenue per user. For instance, providing payment processing services to small businesses or offering financial management tools to cooperatives could be more cost-effective than trying to onboard individual users one by one.

There’s also growing interest in impact-focused investment models. These approaches prioritize long-term social impact alongside financial returns, potentially allowing for longer runways and more sustainable growth strategies. Such models might be better suited to the realities of building financial infrastructure in emerging markets.

What Does the Future Hold?

As Adebayo contemplates his startup’s future, he realizes the path forward will require a delicate balance between growth and sustainability. The dream of bringing financial services to millions of unbanked Africans remains as compelling as ever, but the route to achieving that dream may need to be recalibrated.

The future of African fintech likely lies in a more nuanced approach to growth and funding. Rather than pursuing rapid scaling at all costs, successful companies must focus on building sustainable unit economics from the ground up. This might mean slower growth in the short term, but it could lead to more robust and impactful companies in the long run.

This shift may require adjusting their expectations and investment strategies for venture capital firms. Longer investment horizons, more hands-on operational support, and a greater focus on a path to profitability rather than just user growth could become the norm.

The story of African fintech is far from over. The potential for transformative impact remains enormous, and the ingenuity and determination of entrepreneurs like Adebayo continue to drive innovation across the continent.

However, realizing this potential will require a reimagining of the current VC-fintech model. By addressing the challenges of high customer acquisition costs, exploring alternative business models, and fostering more supportive regulatory environments, the industry can evolve into a more sustainable and impactful force for financial inclusion.

As the sun sets on another day of hustle and innovation in Africa’s tech hubs, one thing is clear: the future of fintech on the continent will be shaped not just by technological breakthroughs, but by the ability to create sustainable, profitable businesses that truly serve the needs of Africa’s diverse populations. It’s a challenge that will require patience, creativity, and a willingness to rethink established models – but for those who succeed, the rewards could be transformative, not just for their businesses, but for millions of Africans seeking access to vital financial services.

Un pays de 13 millions d’habitants en Afrique de l’Ouest, le Bénin, transforme ses exploitations de coton en une grande réussite. Voici comment de vastes réformes et projets transforment cette nation francophone.