La Société Ivoirienne de Banque (SIBC) a publié son rapport d’activité pour le premier trimestre 2024.

Malgré des conditions économiques difficiles, la banque a démontré sa résilience avec des indicateurs clés de rentabilité en croissance par rapport au premier trimestre 2023.

Cette analyse offre un regard approfondi sur la performance financière de la SIBC et ses perspectives stratégiques pour les investisseurs potentiels.

Points financiers marquants

Principaux indicateurs financiers :

Produit Net Bancaire :

- T1 2024 : 24,0

- T1 2023 : 23,7

- Variation : +2 % (0,6)

Résultat avant impôts :

- T1 2024 : 14,0

- T1 2023 : 14,3

- Variation : -2 % (0,3)

Résultat net :

- T1 2024 : 12,0

- T1 2023 : 11,6

- Variation : +6 % (0,7)

Les valeurs sont en milliards de FCFA.

Principaux points à retenir

Croissance des revenus :

SIBC a atteint un Produit Net Bancaire de 24 milliards FCFA au T1 2024, reflétant une augmentation de 2 % par rapport au T1 2023. Cette croissance est principalement due à la solide performance de la marge d’intérêt client et des commissions de service.

Rentabilité :

Le résultat net de la banque a atteint 12 milliards FCFA, marquant une augmentation de 6 % par rapport au T1 2023. Cette amélioration est attribuée à une gestion efficace des coûts et à une gestion robuste des risques.

Gestion des coûts :

La légère baisse du résultat avant impôts (-2 %) indique des défis dans le maintien de la rentabilité avant impôts. Cependant, la croissance positive du résultat net global suggère que la banque a bien géré ses dépenses opérationnelles et maintenu une structure de coûts solide.

Perspectives stratégiques

Dynamique commerciale :

La SIBC continue de montrer un fort dynamisme commercial, comme en témoigne la croissance régulière du Produit Net Bancaire. L’accent mis sur l’amélioration des marges d’intérêt client et des commissions de service a été un facteur clé de ce succès.

Gestion des risques :

Une gestion efficace des coûts opérationnels et le maintien d’un coût du risque stable ont contribué de manière significative à la rentabilité de la banque. Cela démontre la capacité de la SIBC à naviguer efficacement dans des conditions économiques difficiles.

Perspectives d’avenir :

Les équipes de la SIBC restent déterminées à atteindre les objectifs financiers pour l’exercice en cours. Le maintien de la croissance des revenus, la gestion des coûts et le contrôle des risques positionnent bien la banque pour une rentabilité durable.

Performance boursière de la SIBC

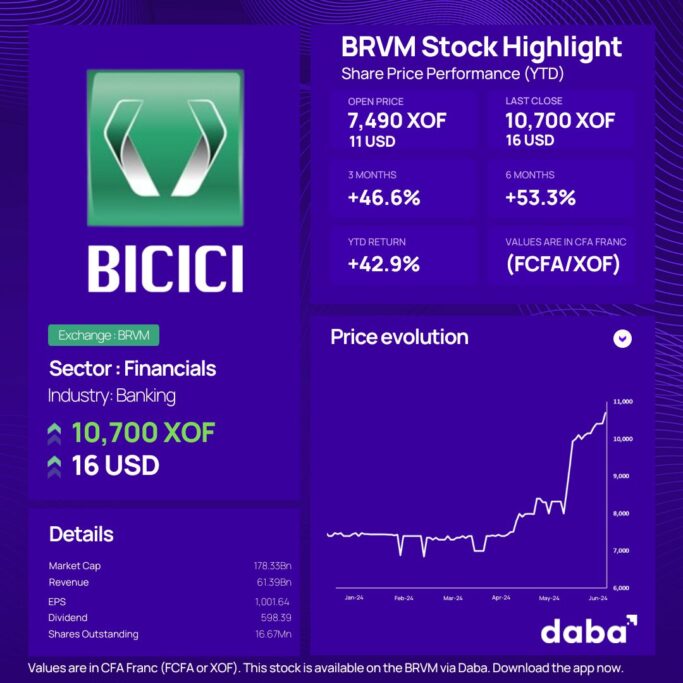

La Société Ivoirienne de Banque (SIBC) est actuellement la cinquième action la plus valorisée de la BRVM avec une capitalisation boursière de 336 milliards FCFA, soit environ 3,79 % de l’ensemble du marché.

SIBC a commencé l’année avec un prix de l’action de 5 350 FCFA et a depuis gagné 25,6 % sur cette valorisation, la classant huitième sur la BRVM en termes de performance depuis le début de l’année.

Cette performance boursière impressionnante reflète les solides résultats financiers de la banque. Les actionnaires peuvent être optimistes quant aux perspectives futures de la SIBC compte tenu de sa trajectoire de croissance solide.

Ce que cela signifie pour les investisseurs potentiels

La solide performance de la SIBC au T1 2024 souligne la résilience et le potentiel du secteur bancaire ivoirien.

La capacité de la banque à réaliser une croissance des revenus et à améliorer sa rentabilité malgré des défis économiques met en évidence son cadre opérationnel solide et son sens stratégique.

Pour les investisseurs potentiels, la SIBC présente une opportunité d’investissement prometteuse. Les solides performances financières de la banque, sa gestion efficace des coûts et son accent stratégique sur l’amélioration des revenus en font une option attrayante pour ceux qui cherchent à investir dans le secteur bancaire africain.

Les investisseurs peuvent facilement acheter et négocier des actions de la BRVM telles que la SIBC en utilisant la plateforme mobile Daba. Daba offre un moyen pratique d’investir dans des actions performantes sur la BRVM, offrant un accès à des marchés dynamiques et en forte croissance.

Alors que certains investisseurs ont peut-être manqué ce rallye, Daba Pro est conçu pour vous aider à repérer des opportunités comme celle-ci à l’avance, vous assurant de rester en avance sur le marché et de prendre des décisions d’investissement éclairées.

Conclusion

Le rapport du T1 2024 de la SIBC reflète une solide santé financière avec une croissance significative du résultat net et une expansion régulière des revenus. La gestion efficace des coûts de la banque et son accent stratégique sur l’amélioration des marges client et des commissions de service la positionnent bien pour un succès continu.

Pour les investisseurs, les performances impressionnantes de la société et ses initiatives stratégiques soulignent son potentiel de croissance et de rentabilité à long terme. Des plateformes comme Daba offrent un moyen pratique d’investir dans la SIBC et d’autres actions performantes de la BRVM, offrant un accès à des opportunités d’investissement prometteuses sur les marchés dynamiques de l’Afrique.

Embrassez l’avenir de la croissance économique de l’Afrique et explorez les nombreuses opportunités d’investissement disponibles sur ce continent résilient et prometteur avec Daba.