NSIA a réussi non seulement à maintenir, mais aussi à améliorer sa performance financière, se positionnant ainsi comme un acteur clé du secteur bancaire ivoirien.

NSIA Banque Côte d’Ivoire (NSIA) a démontré sa résilience financière et sa croissance au cours du premier semestre 2024, malgré un environnement économique mondial difficile.

Alors que le monde se remet lentement des perturbations causées par les crises mondiales des dernières années, NSIA a réussi à non seulement maintenir, mais aussi à améliorer sa performance financière, se positionnant ainsi comme un acteur clé du secteur bancaire ivoirien.

Performance Financière et Croissance des Bénéfices

La performance financière de NSIA Banque au premier semestre 2024 a été impressionnante. Le Produit Net Bancaire de la banque a augmenté de 10,3 % d’une année sur l’autre, atteignant 45,7 milliards de FCFA (78 millions de dollars), contre 41,4 milliards de FCFA au même trimestre de 2023. Cette croissance reflète la capacité de la banque à générer plus de revenus grâce à ses activités bancaires principales malgré les incertitudes économiques plus larges.

Un aspect notable des bénéfices de NSIA est l’augmentation significative de son revenu net. La banque a enregistré un bénéfice net de 14,528 milliards de FCFA, marquant une hausse substantielle de 27,5 % par rapport aux 11,4 milliards de FCFA gagnés au premier semestre 2023. Cette augmentation de la rentabilité souligne la gestion efficace des coûts de NSIA et les initiatives stratégiques visant à stimuler la croissance des revenus tout en maîtrisant les coûts opérationnels.

Rentabilité et Efficacité Opérationnelle

L’efficacité opérationnelle de la banque a également enregistré des progrès positifs. Les charges d’exploitation ont augmenté de 9 %, passant de 21,3 milliards de FCFA en juin 2023 à 23,2 milliards de FCFA en juin 2024.

Malgré cette augmentation des coûts, NSIA a réussi à améliorer légèrement son ratio coût/revenu, qui est désormais de 59,9 %, contre 60,4 % un an plus tôt. Cette amélioration, bien que marginale, indique que NSIA devient plus efficace dans la conversion de ses revenus en bénéfices, ce qui est un bon signe pour les actionnaires à la recherche de création de valeur.

De plus, le résultat brut d’exploitation a augmenté de 12 %, passant de 16,4 milliards de FCFA en juin 2023 à 18,3 milliards de FCFA en juin 2024. Cette augmentation reflète la capacité de la banque à maintenir des gains solides avant impôts et coûts de risque, renforçant ainsi sa rentabilité.

Un des signes les plus encourageants pour les investisseurs est la réduction significative du coût du risque. Le coût net du risque est passé de -3,7 milliards de FCFA en juin 2023 à -2,7 milliards de FCFA en juin 2024. Cette réduction d’environ 27 % met en évidence les efforts réussis de la banque pour gérer le risque de crédit, ce qui est crucial pour maintenir la rentabilité à long terme et protéger la valeur actionnariale.

Solidité du Bilan et Qualité des Actifs

Le bilan de NSIA Banque reflète une base solide qui soutient sa rentabilité continue. Le total des actifs a augmenté de 6 % passant de 2 037 milliards de FCFA en décembre 2023 à 2 159 milliards de FCFA en juin 2024. Cette croissance des actifs est principalement due à une augmentation de 6 % des prêts aux clients, qui sont passés de 1 307 milliards de FCFA à 1 382 milliards de FCFA au cours de la même période.

La capacité de la banque à accorder plus de crédits, en particulier aux petites et moyennes entreprises (PME), démontre son engagement à favoriser la croissance économique en Côte d’Ivoire tout en augmentant ses actifs générateurs de revenus.

Du côté des passifs, les dépôts de la clientèle ont augmenté de 7 %, passant de 1 415,9 milliards de FCFA en décembre 2023 à 1 511,4 milliards de FCFA en juin 2024. Cette augmentation des dépôts, en particulier dans les comptes à vue, les comptes d’épargne et les dépôts de garantie, indique une confiance croissante des clients dans la stabilité et les offres de services de NSIA Banque.

Il convient toutefois de noter que le portefeuille de titres de NSIA a diminué de 5 %, reflétant une approche prudente face à la volatilité des marchés et un éventuel changement stratégique vers des activités bancaires plus traditionnelles, qui offrent généralement des rendements plus stables.

Performance Boursière et Implications pour le Marché

D’un point de vue boursier, l’action NSIA Banque (NSBC) a offert des rendements remarquables à ses investisseurs.

Le prix de l’action de la banque a commencé l’année à 6 000 XOF et a depuis augmenté de 8,25 %, surpassant de nombreux concurrents sur la Bourse Régionale des Valeurs Mobilières (BRVM). Cette appréciation des prix place NSIA Banque comme la 26e action la plus performante sur la BRVM en termes de performance annuelle, ce qui est une réalisation notable compte tenu du paysage concurrentiel.

De plus, NSIA Banque est actuellement la 11e action la plus valorisée sur la BRVM, avec une capitalisation boursière de 161 milliards XOF. Cette valorisation représente environ 1,72 % du marché total des actions sur la BRVM, soulignant le rôle significatif de NSIA dans l’écosystème financier régional.

Pour les actionnaires, la solide performance financière et l’appréciation de l’action de NSIA Banque présentent une proposition d’investissement attrayante.

La capacité de la banque à augmenter ses bénéfices, à améliorer son efficacité opérationnelle et à maintenir la qualité de ses actifs dans un contexte d’incertitude économique est susceptible de continuer à alimenter l’appréciation du prix des actions et à créer de la valeur pour les actionnaires. La rentabilité soutenue et les stratégies de gestion prudente des risques renforcent encore l’attrait de NSIA Banque en tant qu’investissement fiable dans les marchés financiers de l’Afrique de l’Ouest.

Conclusion

La performance financière de NSIA Banque Côte d’Ivoire au premier semestre 2024 reflète une institution bien gérée qui non seulement résiste aux défis économiques de l’ère post-pandémique, mais prospère également. La croissance significative des bénéfices, combinée à l’amélioration de la rentabilité et à un bilan solide, positionne NSIA Banque comme un acteur de premier plan dans le secteur bancaire ivoirien.

Pour les actionnaires, la santé financière robuste de la banque et l’impressionnante performance boursière sont synonymes de rendements prometteurs et de création de valeur à long terme. À mesure que NSIA Banque continue de mettre en œuvre ses initiatives stratégiques et d’améliorer son efficacité opérationnelle, elle reste une opportunité d’investissement convaincante sur le marché des actions de la BRVM.

NSIA has managed to not only sustain but also enhance its financial performance, positioning itself as a key player in the Ivorian banking sector.

Nsia Banque Côte d’Ivoire (NSIA) has demonstrated financial resilience and growth in the first half of 2024, despite operating in a challenging global economic environment.

As the world slowly recovers from the disruptions caused by the global crises of recent years, NSIA has managed to not only sustain but also enhance its financial performance, positioning itself as a key player in the Ivorian banking sector.

Financial Performance and Earnings Growth

NSIA Banque’s financial performance in the first half of 2024 has been nothing short of impressive. The bank’s Net Banking Product (Produit Net Bancaire) rose by 10.3% year-over-year, reaching 45.7 billion FCFA ($78 million), up from 41.4 billion FCFA in the same period of 2023. This growth reflects the bank’s ability to generate more revenue from its core banking activities despite the broader economic uncertainties.

A notable aspect of NSIA’s earnings is the significant increase in its net income. The bank recorded a net profit of 14.528 billion FCFA, marking a substantial 27.5% rise from the 11.4 billion FCFA earned in the first half of 2023. This surge in profitability underscores NSIA’s effective cost management and strategic initiatives aimed at driving revenue growth while keeping operational costs in check.

Profitability and Operational Efficiency

The bank’s operational efficiency has also seen positive strides. The operating expenses increased by 9%, from 21.3 billion FCFA in June 2023 to 23.2 billion FCFA in June 2024.

Despite this rise in costs, NSIA has managed to slightly improve its cost-to-income ratio, which now stands at 59.9%, down from 60.4% a year earlier. This improvement, albeit marginal, indicates that NSIA is becoming more efficient in converting its income into profit, which is a good sign for shareholders looking for value creation.

Moreover, the gross operating income grew by 12%, rising from 16.4 billion FCFA in June 2023 to 18.3 billion FCFA in June 2024. This increase reflects the bank’s ability to maintain strong earnings before taxes and risk costs, further bolstering its profitability.

One of the most encouraging signs for investors is the significant reduction in the cost of risk. The net risk cost decreased from -3.7 billion FCFA in June 2023 to -2.7 billion FCFA in June 2024. This reduction by approximately 27% highlights the bank’s successful efforts in managing credit risk, which is crucial for maintaining long-term profitability and protecting shareholder value.

Balance Sheet Strength and Asset Quality

NSIA Banque’s balance sheet reflects a solid foundation that supports its ongoing profitability. The total assets increased by 6% from 2,037 billion FCFA in December 2023 to 2,159 billion FCFA as of June 2024. This growth in assets is primarily driven by a 6% increase in loans to customers, which rose from 1,307 billion FCFA to 1,382 billion FCFA during the same period.

The bank’s ability to extend more credit, particularly to small and medium enterprises (SMEs), demonstrates its commitment to fostering economic growth in Côte d’Ivoire while enhancing its income-generating assets.

On the liabilities side, customer deposits grew by 7%, from 1,415.9 billion FCFA in December 2023 to 1,511.4 billion FCFA in June 2024. This increase in deposits, particularly in demand deposits, savings accounts, and guarantee deposits, indicates growing customer confidence in NSIA Banque’s stability and service offerings.

However, it is worth noting that NSIA’s securities portfolio declined by 5%, reflecting a cautious approach to market volatility and a possible strategic shift towards more traditional banking activities, which typically offer more stable returns.

Stock Performance and Market Implications

From a market perspective, NSIA Banque’s stock (NSBC) has delivered commendable returns for its investors.

The bank’s share price started the year at 6,000 XOF and has since appreciated by 8.25%, outperforming many of its peers on the Bourse Régionale des Valeurs Mobilières (BRVM). This price appreciation places NSIA Banque as the 26th best-performing stock on the BRVM in terms of year-to-date performance, a notable achievement considering the competitive landscape.

Moreover, NSIA Banque is currently the 11th most valuable stock on the BRVM, with a market capitalization of 161 billion XOF. This valuation accounts for approximately 1.72% of the total equity market on the BRVM, underscoring NSIA’s significant role in the regional financial ecosystem.

For shareholders, NSIA Banque’s strong financial performance and stock appreciation present an attractive investment proposition.

The bank’s ability to grow earnings, improve operational efficiency, and maintain asset quality amidst economic uncertainties is likely to drive continued share price appreciation and deliver value to shareholders. The sustained profitability and prudent risk management strategies further enhance NSIA Banque’s appeal as a reliable investment in the West African financial markets.

Conclusion

NSIA Banque Côte d’Ivoire’s financial performance in the first half of 2024 reflects a well-managed institution that is not only weathering the economic challenges of the post-pandemic era but is also thriving. The significant growth in earnings, combined with improved profitability and a strong balance sheet, positions NSIA Banque as a leading player in the Ivorian banking sector.

For shareholders, the bank’s robust financial health and impressive stock performance signal promising returns and long-term value creation. As NSIA Banque continues to implement its strategic initiatives and enhance its operational efficiency, it remains a compelling investment opportunity in the BRVM equity market.

Contributed by Mathias Léopoldie, Co-Founder of Julaya via Realistic Optimist.

Optimizing for home runs

It is said that the first venture capital (VC) firm was founded in 1946, in the USA. The American Research & Development Corporation (ARDC) became famous for its $70,000 investment in Digital Equipment Corporation, a computer manufacturer, which went public in 1967 at a whopping $355M valuation. Investors taking risky bets on companies wasn’t new, but the computer era put venture capital’s singular “power law” on full display.

A baseball game is an apt analogy to conceptualize how venture capital works. The most exciting play, which also brings outsized returns, is when the ball skyrockets over the fence resulting in a home run.

VC is quite similar, as the power law nature implies that a few investments (<5%) will drive most of a fund’s returns. While the number of home runs in baseball might not guarantee winning the season, it does in VC.

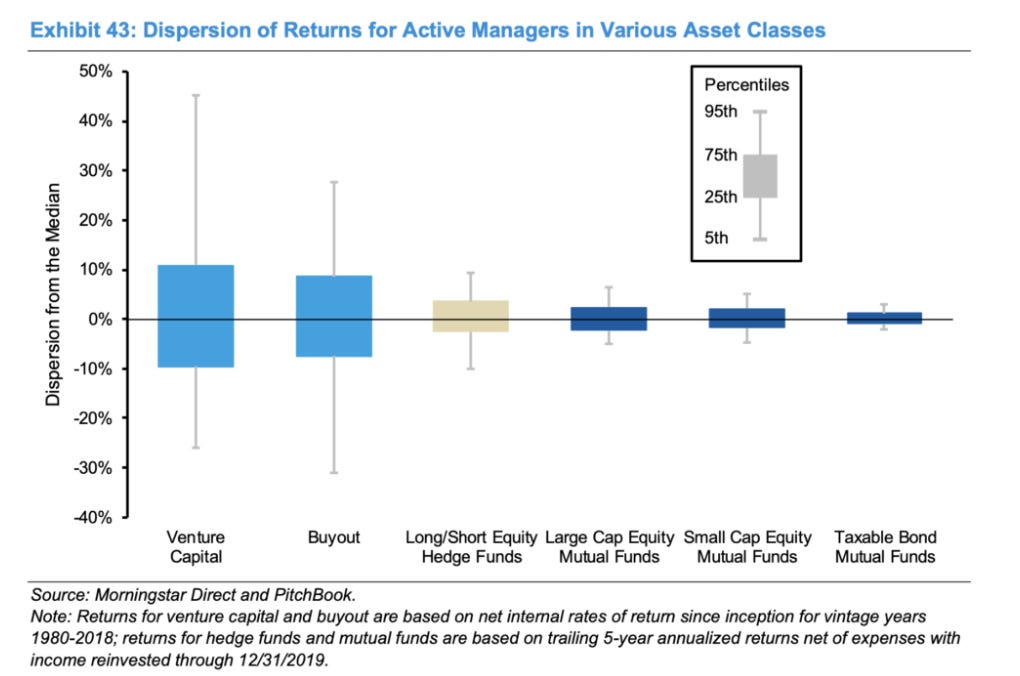

This is why VC is an exciting asset class: sharp skill and experience are necessary, but luck plays a non-negligible role. It is no surprise that, amongst asset classes, VC has the highest dispersion of returns. Participants can either win big or lose a lot.

The African VC ecosystem is young, inching past its first decade of existence. The African internet revolution took a different shape than it did elsewhere: between 2005 and 2019, the share of African households possessing a computer went from 4% to 8%, while other developed economies witnessed a 55% to 80% jump over the same period.

One can’t expect a VC industry to suddenly flourish in an economy where microchip-equipped computer and smartphone ownership is so scarce. The heart of the VC industry is called “Silicon Valley” for a reason.

Another trend, however, calls our attention. Namely, the rise of mobile phones on the continent. Currently, over 80% of Africans own a mobile phone, a figure that reaches close to 100% in some countries. The 2000s-2010s feature phone mass production era is to thank. Transsion Holdings, a Chinese public company, tops the leaderboard in terms of mobile phones sold in Africa, through its portfolio of brands (Tecno, Itel, and Infinix).

This offline, ‘computerized’ revolution of sorts is significant for the continent, as a large part of Sub-Saharan Africa’s population still lacks internet access. This includes people who own a feature phone but no smartphone, or people for whom the cost of internet data is prohibitively expensive. Internet’s geographical reach in Africa also remains patchy, further complicating the equation.

Unsurprisingly, telecom operators have emerged as this mobile phone revolution’s winners. The mobile money industry is a striking example: a fertile mix of USSD technology and agent networks enabled telecom operators to become fintech companies as far back as 2007. Those same telcos now derive a significant amount of their business from the financial services they ushered in. M-Pesa, Kenya’s leading mobile money service provider, now accounts for more than 40% of Safaricom’s (its parent telecom operator) mobile service revenue.

In Sub-Saharan Africa, 55% of the population possesses a financial account, with mobile money’s rise boosting that number in recent years. That’s approximately double the amount of Africans with an internet connection.

Too early to call

In this context, many are the Cassandras lamenting venture capital’s failure in Africa. These conclusions seem premature, both because the industry itself is novel but also because the digital ecosystem it operates in is still nascent.

Even by removing Africa from the picture, venture capital is a long-term industry, and its illiquidity can lead to prolonged exit times. According to Dealroom, only 17% of portfolio startups globally exit within the investment period of 10 years. Initial, tangible VC investments in Africa debuted around 2012. We believe that the pessimists are neither right nor wrong: they’re just pontificating too early.

That being said, the past decade has drawn the contours of what can be improved and highlighted what has worked.

# years it takes for portfolio startups to exit, along with exit size (Dealroom)

The casino analogy

Casinos constitute another pertinent venture capital analogy. Addiction and money laundering aside, a casino is a fascinating business. In a casino, a few people win exuberant amounts, while the many ‘losers’ subsidize the entire operation. In return for setting up the infrastructure, applying rules, and mediating disputes, the casino pockets a handsome amount of the proceeds as profits.

Venture capital’s logic is similar to a casino’s. “Winners” are the top decile of skilled VC funds reaping outsized returns. “Losers” are the VC funds that don’t return the amount of money they promised their investors (LPs). The casino itself is the government, collecting tax revenue in return for organizing the game.

Without casinos’ power law gains distribution, no one would play. It is by design that ‘returns’ are extremely skewed, enabling the casino economy to work. VC is similar: it is by design that most of the returns come from the top decile funds and companies because winning in venture capital is hard. It wouldn’t be possible without the entire ecosystem structure, and failing companies still provide tremendous value to the other players.

Mixing profitability and venture scale

While far from a solely African problem, the confusion between these two terms may cause damage. In light of hostile, macroeconomic conditions, many Africa-focused VCs have started demanding that their startups reach “profitability” even if this means compromising on hyper-growth.

This is partly a mistake: if investors want to invest in profitable African businesses, they can invest in African banks for example, which exhibit fantastic ROIs. Or switch to private equity. But that isn’t the VC game.

VCs demanding that their portfolio companies, especially young ones (pre-seed and seed stages), become profitable quasi-eliminates any potential “home-run” companies. The latter can only emerge through market share dominance, a process facilitated by operating at a company-level loss when competitors can’t. Those home-run companies are the only way a VC can reach the outsized returns it promised its LPs.

Herein lies the confusion between profitability as a whole and positive unit economics at the marginal level. VCs should be encouraging their portfolio companies to reach “venture scale”. Venture scale is the ability to grow at a decreasing and very efficient marginal cost. This implies tinkering and getting unit economics to a point where the revenue generated from each unit sold is superior to what it costs to make it. This metric is referred to as the “contribution margin”.

A company with a positive contribution margin, which can be unprofitable as a whole because it has very high fixed costs (such as R&D), has a clear path to long-term profitability. This justifies pumping large amounts of money into it, enabling the company to reach the economies of scale it needs to win.

Companies continuing their fundraising route, and even going public, with iffy contribution margins either speed-run their death (Airlift) or make their lives significantly harder (SWVL). Those are the business models VCs should be wary of. However, a blind focus on company-level profitability for the sake of profitability doesn’t make much sense in the VC context. There are very useful data points that companies can follow to see if they are on the right path, such as the “burn multiple” or the “magic number”.

VCs investing in African startups should be cognizant of this difference as they hit the brakes during the current funding winter.

African VC: Expensive and risky, replete with singular challenges

The early innings of the African venture capital ecosystem have made two things clear: venture capital in Africa is expensive and risky.

It is expensive because lagging infrastructure might nudge startups to build out their own, which costs money, additional time, and expertise. If the infrastructure needed can’t be built in-house, such as public infrastructure (roads, etc…), the startup will have to contend with the higher prices resulting from the existing infrastructure’s inefficiencies. This is a salient problem for logistics startups, for example.

Funding high-growth businesses in Africa can thus turn out to be an expensive endeavor, generating infrastructure costs that wouldn’t be necessary in other, more developed markets.

It is riskier if funded by international funds in international currencies (USD, Euros, GB Pounds, etc…). Take Nigeria for example, one of the continent’s venture capital darlings. Earlier last year, the Central Bank of Nigeria floated the local currency (the naira) away from its traditional peg to the USD, in a bid to liberalize the economy. The move led to the naira’s sharp and sudden devaluation, revealing overarching uncertainty about its strength.

This was a disaster for Nigerian startups, especially those that reported their revenue numbers in dollars (a given if foreign investors are on the cap table). The devaluation meant that similar revenue in naira from one month to another could render just half the value in dollars.

If Nigerian startups had converted any USD from their funding rounds into naira, their buying power was also drastically slashed. From the investor’s point of view, the startup’s $USD valuation got trimmed almost overnight, due to factors outside the founders’ control. This also creates currency translation issues, making reporting of actual performance of ventures in local and USD currencies trickier and less reliable.

This is not an issue in developed markets with stronger currencies and free capital flows, such as the US or Europe. It can be reasonably assumed that this issue has contributed to Nigeria’s drop in startup investment.

To sum it all up: African venture capital is expensive because startups have to build out or deal with decrepit infrastructure hence requiring specific business models, and comparatively riskier since valuations are subject to currency-induced volatility.

The past year was also punctuated by the downfall of some well-funded African startups, failures attributed to a nebulous mix of founder wrongdoing, financial mismanagement, and outright fraud. As is often the case, very few people will uncover the full story behind these crashes.

Some observers were quick to generalize the trend, using these failures as proxies to gauge the integrity of all other African founders. Shady founders do and will always exist, regardless of the ecosystem’s maturity. There is an argument to be made that the safeguards against those founders are potentially lower in young ecosystems such as Africa, where governance standards have not yet been standardized and where investors are less aware of African markets’ specific features. That is a solvable problem.

These are normal ecosystem growing pains that need to be rationally addressed but are no cause for doomsday rhetoric.

What’s needed: liquidity

Venture capital’s equation is simple: can you invest in startups that will exit, and will those exits return (much) more money than your LPs put in while creating economic value for the clients, suppliers, and all stakeholders?

Exits, meaning a startup getting acquired or going public, are crucial to the venture capital ecosystem’s health. VCs are investing with the intention of outsized exits, but sometimes those turn out to be impossible. Adverse market conditions, a non-scalable business model, founder conflict… Exits can be jeopardized for various reasons.

When such a situation arises, invested VCs will sometimes face the choice of either settling down for a smaller exit or losing their money outright. We believe that the importance of these small exits, such as “acquihires” should not be underestimated as they remain important for VCs required to distribute to their LPs. Typically, they will also provide cash-outs for angel investors, employees, public institutions, and founders. These cash-outs will hopefully convince these stakeholders to pour money back into the ecosystem, launching a virtuous flywheel.

While the number of exits has been increasing on the continent, actual numbers of their combined value are hard to come through (many deals don’t disclose their terms). Briter Bridges also interestingly notes that the countries and sectors receiving the most amount of funding aren’t necessarily the ones with the most lucrative exit paths.

Liquidity events are essential to Africa’s VC market. So far, most of the attention has gone toward fundraising numbers, a relevant proxy for market sentiment but not market viability or growth. More attention should be paid to the African exit market, its intricacies, its possibilities, and its obstacles.

The future of African M&A

An overwhelming majority of exits for African startups today entail a merger/acquisition (M&A).

Two African M&A trends are likely to materialize over the next couple of years.

First is the consolidation of African startups operating in the same sector yet different geographies, and struggling to live up to the valuation they raised. The recent Wasoko-MaxAB merger announcement is an example of such.

Second is the potential rise of “south-south” startup acquisitions. The socio-demographic similarities between emerging markets make the solution built in one place potentially applicable to another, even thousands of miles away. This seems to be truer for lesser regulated sectors, such as edtech or e-commerce, but harder for more supervised ones, like fintech. The recent Orcas-Baims acquisition is an example of such a deal.

Players such as Brazil’s Ebanx, Estonia’s Bolt, and Russia’s Yango Delivery all operate in Africa and represent new competitors (and potential acquirers) for local African startups. This could stimulate the local M&A scene, but more importantly, entice other well-capitalized startups in emerging markets to expand to Africa.

Conclusion

Venture capital in Africa is a recent phenomenon, one whose success can’t yet be pronounced due to the sector’s long-term nature. These early years have highlighted the specificities of African venture capital, some of which aren’t relatable to more developed markets or even other emerging markets. This means copy-pasting Western frameworks in the African context is a faulty and lazy approach.

Foreign and local VCs investing in African startups should seek to deeply understand the continent’s intricacies, and develop fresh strategies to deal with them.

The ecosystem should give itself time. Adopting a longer-term view discounts short-term pessimism and allows one to rationally solve the challenges that arise. African venture capital can be a fantastic locomotive for African growth, but railroads don’t get built overnight.

As the Bambara saying puts it, munyu tè nimisa : one never regrets patience.

Mathias Léopoldie is the co-founder of Julaya, an Ivory Coast-based startup that offers digital payment and lending accounts for African companies of all sizes. Julaya serves over 1,500 companies, processes $400M of transactions, and has raised $10M in funding.

Julaya has offices in Benin, Senegal, France, and Ivory Coast.

Mathias would like to thank Mohamed Diabi (CEO at AFRKN Ventures) and Hannah Subayi Kamuanga (Partner at Launch Africa Ventures) for their thorough advice on this piece.

Le paysage du capital-risque africain regorge d’opportunités passionnantes.

En tant qu’investisseur particulier, vous avez placé votre confiance dans un fonds de capital-risque, espérant qu’il propulsera votre portefeuille vers une croissance significative. Mais comment évaluer efficacement la performance de votre fonds dans un marché dynamique avec des horizons d’investissement longs ?

Cet article de blog, proposé par Daba, votre guichet unique pour les investissements en Afrique et sur les marchés émergents, vous fournira les connaissances nécessaires pour évaluer le succès de votre fonds de capital-risque.

Nous explorons les principaux indicateurs, les considérations de risque et comment interpréter les données pour prendre des décisions d’investissement éclairées.

Démystifier la Performance des Fonds : Comprendre le Terrain de Jeu

Par nature, les fonds de capital-risque investissent dans des startups à haut risque et à haute récompense. Bien que le potentiel de rendements explosifs existe, il y a aussi un risque significatif d’échec. Par conséquent, évaluer la performance nécessite une approche nuancée, prenant en compte à la fois les rendements absolus et le risque.

Voici quelques indicateurs fondamentaux à considérer :

Taux de Rentabilité Interne Brut (IRR) : Cet indicateur reflète le rendement annualisé d’un investissement sur sa durée de vie. Il prend en compte l’investissement initial et tous les flux de trésorerie reçus, y compris l’appréciation du capital et les dividendes. Pour les fonds de capital-risque, l’IRR est généralement calculé sur 10 ans, reflétant la nature à long terme de ces investissements.

Valeur Nette d’Inventaire (NAV) : Cela représente la valeur totale des actifs sous-jacents d’un fonds, moins ses passifs, divisée par le nombre d’actions en circulation. Suivre les fluctuations de la NAV dans le temps peut offrir des informations sur la performance globale du fonds et la santé du portefeuille.

Multiple sur le Capital Investi (MOIC) : Cet indicateur révèle combien un fonds a rapporté sur son capital investi. Il se calcule en divisant la valeur totale du fonds (y compris les gains non réalisés) par le capital total engagé par les investisseurs.

Multiple Cash on Cash (CoC) : Cet indicateur montre le montant total de cash retourné aux investisseurs divisé par le montant total d’argent investi. Un multiple CoC supérieur à 1 indique une rentabilité, tandis qu’une valeur inférieure à 1 suggère une perte. Cet indicateur offre une vue pratique des flux de trésorerie réels.

Composition du Portefeuille de Transactions : Au-delà des chiffres bruts, la qualité et le stade des entreprises du portefeuille d’un fonds sont cruciaux. Un portefeuille bien diversifié à travers les secteurs et les stades d’investissement réduit le risque. Cherchez des fonds avec un solide historique d’identification de projets prometteurs.

Rappelez-vous : Aucun indicateur ne donne une image complète à lui seul. Une approche globale qui considère une combinaison de ces indicateurs clés, ainsi que la stratégie d’investissement du fonds et l’expertise de l’équipe de gestion, est idéale.

Prendre en Compte le Risque

Bien que les indicateurs comme l’IRR et le MOIC soient cruciaux, ils ne donnent pas une image complète sans considérer le risque. Le capital-risque implique intrinsèquement un degré élevé d’incertitude. Voici comment prendre en compte le risque :

Volatilité du Fonds : Mesurez la variabilité des rendements d’un fonds dans le temps. Une forte volatilité signifie que les rendements du fonds peuvent fluctuer de manière significative, indiquant un investissement plus risqué.

Ratio de Sharpe : Cet indicateur ajuste les rendements en fonction du risque en comparant le rendement excédentaire d’un fonds (rendement au-dessus du taux sans risque) à sa volatilité. Un ratio de Sharpe plus élevé suggère que le fonds génère des rendements supérieurs par rapport au niveau de risque entrepris.

Au-Delà des Chiffres : Les Facteurs Qualitatifs qui Comptent

Bien que les indicateurs quantitatifs soient essentiels, les facteurs qualitatifs influencent également la performance des fonds :

Expertise du Gestionnaire de Fonds : L’expérience et l’historique du gestionnaire de fonds sont primordiaux. Recherchez des gestionnaires avec une profonde compréhension du paysage du capital-risque africain et une capacité prouvée à identifier des startups à fort potentiel de croissance.

Stratégie d’Investissement et Focalisation : Une stratégie d’investissement claire et bien définie, alignée sur votre tolérance au risque, est cruciale. Le fonds se concentre-t-il sur des entreprises en phase de démarrage à haut risque, ou sur des entreprises en phase avancée avec un chemin plus clair vers la rentabilité ?

Réseau et Flux de Transactions : Un réseau solide au sein de l’écosystème des startups africaines peut fournir un accès aux transactions et des informations précieuses pour le gestionnaire de fonds. Ce réseau peut significativement influencer la capacité du fonds à identifier et investir dans des startups prometteuses.

Benchmarking de la Performance du Fonds pour Contexte

Évaluer la performance d’un fonds isolément ne suffit pas. Pour obtenir une compréhension plus holistique, comparez ses indicateurs avec des benchmarks pertinents.

Benchmarks Industriels : Comparez la performance de votre fonds aux moyennes de l’industrie pour les fonds de capital-risque à un stade d’investissement similaire (amorçage, early-stage, etc.) et dans la même région géographique.

Performance du Marché Public : Si le fonds investit dans des secteurs avec des entreprises cotées en bourse, considérez comment sa performance se compare aux indices boursiers pertinents.

Mettre Toutes les Données Ensemble : Interpréter les Données

Il n’existe pas de “nombre magique” unique pour définir un fonds de capital-risque réussi. Analysez les indicateurs collectivement, en tenant compte de la stratégie d’investissement du fonds, de son profil de risque et de vos propres objectifs d’investissement.

Voici quelques conseils :

Un IRR élevé ne garantit pas le succès. Recherchez un historique cohérent de génération d’IRR positifs sur plusieurs fonds gérés par la même équipe.

Les fluctuations de la NAV sont normales. Cependant, une NAV en baisse constante pourrait indiquer des problèmes sous-jacents dans le portefeuille.

Le MOIC devrait idéalement être supérieur à 1. Cela suggère que le fonds génère un rendement sur le capital investi.

La volatilité est attendue. Cependant, une volatilité excessivement élevée pourrait être préoccupante pour les investisseurs averses au risque.

Un ratio de Sharpe supérieur à 1 est généralement positif. Un ratio plus élevé indique de meilleurs rendements ajustés au risque.

L’Avantage Daba : Simplifier Votre Parcours d’Investissement

Évaluer la performance d’un fonds de capital-risque nécessite de l’expertise et un accès aux données. Daba vous permet de prendre des décisions d’investissement éclairées. Notre plateforme propose :

Listes de Fonds Sélectionnées : Nous offrons un accès à un annuaire complet de fonds de capital-risque africains, vous permettant de comparer et de contraster les stratégies d’investissement, les indicateurs de performance et les profils des équipes.

Analyses d’Experts : Notre équipe de professionnels de l’investissement publie régulièrement des articles et des analyses de marché perspicaces pour vous tenir informé des dernières tendances et développements dans le capital-risque africain.

Services de Gestion d’Investissement : Pour ceux qui recherchent une approche plus pratique, Daba propose des services de gestion d’investissement, où notre équipe expérimentée peut vous aider à construire un portefeuille diversifié aligné sur vos objectifs d’investissement.

Données et Analyses de Performance : Obtenez des informations sur la performance historique d’un fonds et des indicateurs clés pour prendre des décisions d’investissement basées sur les données.

Investir en Confiance

Mesurer la performance d’un fonds de capital-risque est une tâche multifacette. En comprenant les indicateurs clés, en tenant compte des facteurs de risque et en utilisant des benchmarks industriels, vous serez bien équipé pour évaluer le succès de votre fonds.

Daba est votre partenaire pour naviguer dans le monde passionnant du capital-risque africain. Avec notre plateforme complète et nos conseils d’experts, vous pouvez investir en toute confiance, sachant que vous avez les outils pour prendre les bonnes décisions.

The African venture capital landscape is brimming with exciting opportunities.

As a retail investor, you’ve placed your trust in a venture fund, hoping it will propel your portfolio towards significant growth. But how do you effectively gauge your fund’s performance with a dynamic market and long investment horizons?

This blog post, brought to you by Daba, your one-stop shop for African and emerging market investments, will equip you with the knowledge to assess your venture fund’s success.

We explore key metrics, risk considerations, and how to interpret the data to make informed investment decisions.

Demystifying Fund Performance: Understanding the Playing Field

By their very nature, venture capital funds invest in high-risk, high-reward startups. While the potential for explosive returns exists, there’s also a significant chance of failure. So, evaluating performance requires a nuanced approach, considering both absolute returns and risk.

Here are some fundamental metrics to consider:

Gross Internal Rate of Return (IRR): This metric reflects an investment’s annualized return over its lifetime. It considers initial investment and all cash flows received, including capital appreciation and dividends. For venture funds, IRR is typically calculated over 10 years, reflecting the long-term nature of these investments.

Net Asset Value (NAV): This represents the total value of a fund’s underlying assets, minus its liabilities, divided by the number of outstanding shares. Tracking NAV fluctuations over time can offer insights into the fund’s overall performance and portfolio health.

Multiple on Invested Capital (MOIC): This metric reveals how much a fund has returned on its invested capital. It’s calculated by dividing the fund’s total value (including unrealized gains) by the total capital investors commit.

Cash on Cash (CoC) Multiple: This metric showcases the total amount of cash returned to investors divided by the total amount of money invested. A CoC multiple greater than 1 indicates profitability, while a value less than 1 suggests a loss. This metric offers a practical view of actual cash flow.

Deal Portfolio Composition: Beyond raw numbers, the quality and stage of a fund’s portfolio companies are crucial. A well-diversified portfolio across sectors and investment stages mitigates risk. Look for funds with a strong track record of identifying promising ventures.

Remember: No single metric paints the whole picture. A comprehensive approach that considers a combination of these KPIs along with the fund’s investment strategy and management team expertise is ideal.

Factor in Risk

While metrics like IRR and MOIC are crucial, they paint an incomplete picture without considering risk. Venture capital inherently involves a high degree of uncertainty. Here’s how to factor in risk:

Fund Volatility: Measure the variability of a fund’s returns over time. High volatility signifies that the fund’s returns can fluctuate significantly, indicating a riskier investment.

Sharpe Ratio: This metric adjusts returns for risk by comparing a fund’s excess return (return above the risk-free rate) to its volatility. A higher Sharpe Ratio suggests the fund is generating superior returns relative to the level of risk undertaken.

Beyond the Numbers: Qualitative Factors that Matter

While quantitative metrics are essential, qualitative factors also influence fund performance:

Fund Manager Expertise: The experience and track record of the fund manager are paramount. Look for managers with a deep understanding of the African VC landscape and a proven ability to identify high-growth potential startups.

Investment Strategy and Focus: A clear and well-defined investment strategy that aligns with your risk tolerance is crucial. Does the fund focus on early-stage, high-risk ventures, or later-stage companies with a clearer path to profitability?

Network and Deal Flow: A strong network within the African startup ecosystem can provide deal flow access and valuable insights for the fund manager. This network can significantly impact the fund’s ability to identify and invest in promising startups.

Benchmarking Fund Performance for Context

Evaluating a fund’s performance in isolation isn’t enough. To gain a more holistic understanding, compare its metrics with relevant benchmarks.

Industry Benchmarks: Compare your fund’s performance against industry averages for venture capital funds in a similar investment stage (seed, early-stage, etc.) and geography.

Public Market Performance: If the fund invests in sectors with publicly traded companies, consider how its performance stacks up against relevant stock market indices.

Putting it All Together: Interpreting the Data

There’s no single “magic number” to define a successful venture fund. Analyze the metrics collectively, considering the fund’s investment strategy, risk profile, and your own investment goals.

Here are some pointers:

High IRR doesn’t guarantee success. Look for a consistent track record of generating positive IRRs over multiple funds managed by the same team.

NAV fluctuations are normal. However, a consistently declining NAV could indicate underlying portfolio issues.

MOIC should ideally be greater than 1. This suggests the fund is generating a return on invested capital.

Volatility is expected. However, excessively high volatility might be concerning for risk-averse investors.

Sharpe Ratio above 1 is generally positive. A higher ratio indicates better risk-adjusted returns.

The Daba Advantage: Simplifying Your Investment Journey

Evaluating venture fund performance requires expertise and access to data. Daba empowers you to make informed investment decisions. Our platform provides:

Curated Fund Listings: We provide access to a comprehensive directory of African VC funds, allowing you to compare and contrast investment strategies, performance metrics, and team profiles.

Expert Insights: Our team of investment professionals regularly publishes insightful articles and market analyses to keep you informed about the latest trends and developments in African VC.

Investment Management Services: For those seeking a more hands-on approach, Daba offers investment management services, where our experienced team can help you build a diversified portfolio that aligns with your investment goals.

Performance Data & Analytics: Gain insights into a fund’s historical performance and key metrics to make data-driven investment choices.

Invest with Confidence

Measuring venture fund performance is a multi-faceted endeavor. By understanding key metrics, considering risk factors, and utilizing industry benchmarks, you’ll be well-equipped to evaluate your fund’s success.

Daba is your partner in navigating the exciting world of African venture capital. With our comprehensive platform and expert guidance, you can invest with confidence, knowing you have the tools to make the right decisions.

The African continent is rapidly becoming one of the newest — and most promising — destinations for emerging markets investors.

In fact, for upwards of 20 years, the World Economic Forum has identified that more than half of the world’s fastest-growing economies are on the continent. With extensive natural resources, a young and increasingly educated workforce, relative political stability, and undeniable prospects for economic growth, there’s no question of vitality for investors.

Image from IMCS

Through and through, Africa is among the handful of emerging markets globally; the phrase coined by economists in the early 1980s defines investing in developing countries. Like any investment decision, there are inherent risks but here are five reasons our leadership believes Africa is worth a shot:

1. Potential for Growth 📈

Presently, Africa accounts for around 17% of the world’s population, but only 3% of global GDP. This data not only attests to a historical failure to tap into the continent’s developmental potential but also highlights the tremendous opportunities that lie ahead. Should Africa continue to sustain and accelerate its structural reforms, many believe the continent can emulate China’s rapid rise over the last 50 years.

2. Innovation 💡

Industrial revolutions, whether driven by steam, assembly lines or computers, have historically been slow to sweep the African continent. However, the era of Industry 4.0, clean energy, artificial intelligence, and digital innovation promises to be different. Unlike previous waves of industrial change, having a stake in the digital age doesn’t require extensive expertise or massive capital investment. Instead, innovators and entrepreneurs in emerging markets are in a position to tap into flows of talent and digital knowledge and convert them into goods, services, and business models.

Image from Enterprise

3. Lower Valuations 📉

In the last decade, African equities have not been a success story — at least not when compared to similar regions. The MSCI US and the MSCI Developed World index rose 232% and 159% respectively in the last ten years, while the MSCI South Africa and MSCI EFM Africa ex. South Africa only gained 33% and 23%. With that in mind, some question whether Africa’s equities have lagged because of problems on the continent. Short answer: not really. However, it does present a unique opportunity for investors — more equity stake in the companies you choose to invest in.

4. Diversification 📊

Diversification is the practice of spreading out investments to reduce exposure to risks associated with just one type of asset. The practice is intended to reduce the volatility of your investment portfolio over time. If you’ve been patiently waiting on an opportunity to invest in international stocks, Africa presents itself as a worthy option.

Image from Kubera

5. Rising Middle Class 💼

According to the World Economic Forum, by 2030, more than 40% of Africans will belong to the middle or upper classes; as a result, there will be an increased demand for goods and services. Not to mention, household consumption is expected to reach $2.5 trillion (yes, trillion), more than double that of 2015 at $1.1 trillion. An increase in capital can only mean more opportunities for economic growth and development throughout the continent leading to more and more inventors flocking to Africa.

That’s where daba comes in. Our simplified platform provides what we call “everyday investors” with investment analysis and wealth-building resources to make their investment decisions in the African private and public capital markets sustainable.

Image from daba

To learn more about daba and how to join our growing global community of investors, visit dabafinance.com or connect with us on LinkedIn!