Medium – depends on company earnings and overall market sentiment

Passive or Active?

Active business (hands-on)

Passive investment

Worst-Case Scenario

Full flock loss → total capital depletion

Portfolio decline → temporary or partial loss

Best-Case Scenario

60%+ annual ROI if cycles run well and mortality is low

100%–400%+ on high-performing stocks; plus dividends

Suitability for Beginners

Not ideal unless trained or supervised

Very suitable — beginner-friendly

Final Verdict

For the average retail investor in Côte d’Ivoire, investing in the BRVM is a safer, easier, and more consistent way to build wealth.

A chicken farm can generate high returns, but it requires:

high discipline,

daily operations,

risk tolerance for disease and mortality, and

solid working capital.

A balanced strategy could be:

👉 Build savings and investment cash flow through BRVM investments first, 👉 then expand into a chicken farm once you have the time, capital, and experience to manage it professionally.

Pour de nombreux investisseurs particuliers en Côte d’Ivoire, la question est simple : est-il plus judicieux d’investir dans un élevage de poulets ou de placer son argent sur le BRVM ?

Les deux options peuvent créer une véritable richesse — mais leurs profils de risque, leurs besoins en capital et l’effort requis sont très différents. Nous analysons ci-dessous les deux possibilités.

Option 1 : Le BRVM – Fort potentiel, effort minimal

Le BRVM a été l’un des marchés boursiers les plus performants d’Afrique en 2025. Indice Composite du BRVM : +24,73 % YTD (2025)

De nombreuses actions individuelles ont affiché des performances de 100 % à 400 % depuis le début de l’année, comme le montre la liste ci-dessous :

Unilever CI : +486 %

SITAB : +300 %

SILOX / CFI / SAPH : également des gains à trois chiffres

Banques (BOA, BICICI, Ecobank) : rendements annuels de 30 % à 70 %

Pourquoi le BRVM est attractif aujourd’hui

Forte liquidité pour un marché frontière, grâce aux plateformes d’investissement digitales

Culture solide du dividende : banques et biens de consommation offrent souvent 5 % à 10 % par an

Stabilité du franc CFA, indexé à l’euro, réduisant le risque de change

Aucun stress opérationnel : pas de personnel, pas de maladies, pas de pénurie de matières premières

Capital requis

Possibilité de commencer dès 10 000 FCFA

Rendements potentiels

Scénario de base (performance de l’indice) : 20 % à 25 % par an

Scénario optimiste (sélection de titres) : 40 % à 100 % ou plus par an

Revenus de dividendes : 5 % à 8 % par an

Risques

Volatilité des marchés

Chocs spécifiques aux entreprises (fraude, mauvais résultats, régulation)

Contraintes de liquidité sur les petites capitalisations

Dans l’ensemble, investir sur le BRVM demande très peu de temps et offre historiquement de solides performances.

Option 2 : Lancer un élevage de poulets

Un petit élevage (300 à 500 poulets de chair ou 200 à 300 poules pondeuses) est une idée d’activité courante, mais bien plus complexe qu’on ne l’imagine.

Étapes clés pour lancer un élevage de poulets

A. Planification et installation

Choisir entre poulets de chair (cycle de 6 à 8 semaines) ou poules pondeuses (cycle d’environ 18 mois)

Trouver un site adapté (en dehors des zones densément peuplées)

Construire ou louer un bâtiment d’élevage

Coûts d’installation

Éléments

Coût estimé (FCFA)

Poulailler basique (500 sujets)

500 000 – 1 500 000

Mangeoires et abreuvoirs

100 000 – 250 000

Système d’eau

50 000 – 150 000

Éclairage et ventilation

50 000 – 200 000

Matériel de désinfection

30 000 – 60 000

Poussins (chair)

500 – 700 FCFA par poussin

Vaccins et soins vétérinaires

40 – 70 FCFA par poussin

Aliment du premier cycle

350 000 – 600 000

Investissement initial total

1 300 000 – 3 000 000 FCFA

B. Exploitation : travail hebdomadaire requis

Achat d’aliments (prix volatils)

Nettoyage quotidien du poulailler

Gestion de la température et de la ventilation

Vaccination et suivi sanitaire

Gestion des déchets

Négociation avec les acheteurs (restaurants, marchés, grossistes)

Il s’agit d’un travail manuel, presque quotidien.

C. Rendements potentiels

Exemple : 500 poulets de chair

Prix d’achat : 500 – 700 FCFA par poussin

Prix de vente (après 6 à 8 semaines) : 2 500 – 3 500 FCFA par poulet

Bénéfice net par cycle : → 450 000 – 550 000 FCFA tous les 45 jours → Équivalent mensuel : 360 000 – 450 000 FCFA

Estimation du rendement annuel

Si tous les cycles se déroulent sans problème : → 30 % à 60 % de rendement annuel sur le capital

Mais les risques réels sont importants

Épidémies (Newcastle, grippe aviaire) pouvant anéantir le cheptel

Volatilité du prix des aliments (poste de coût principal)

Forte mortalité en cas de défaillance de la ventilation, de la vaccination ou de l’hygiène

Risque d’accès au marché : vendre à bon prix n’est pas garanti

Activité très chronophage

Tensions de trésorerie : revenus cycliques, coûts permanents

Un seul cycle raté peut faire passer un rendement annuel de +40 % à −20 %.

Comparaison pour un investisseur particulier

Capital requis

BRVM : dès 10 000 FCFA

Élevage de poulets : environ 1,3 à 3,0 millions FCFA

Charge opérationnelle

BRVM : quasi nulle

Élevage : travail quotidien et suivi vétérinaire

Fiabilité des rendements

BRVM : volatil mais historiquement solide

Élevage : rentable mais fragile et irrégulier

Liquidité

BRVM : immédiate (vente possible à tout moment)

Élevage : faible (vente uniquement à maturité)

Risques

BRVM : fluctuations de prix, performance des entreprises

Élevage : maladies, coût de l’aliment, mortalité, main-d’œuvre, climat, réglementation

Alors… lequel est le meilleur choix ?

Si tu recherches des rendements passifs, liquides et évolutifs : ✔️ L’investissement sur le BRVM est la meilleure option. Tu peux faire croître ton capital progressivement avec de solides rendements et très peu d’effort.

Si tu veux une activité active pouvant générer des profits plus élevés mais instables : ✔️ Un élevage de poulets peut surperformer, mais uniquement avec de l’expertise, de la discipline et une bonne gestion des risques. C’est une véritable entreprise, pas un simple complément de revenu.

Comparatif : élevage de poulets vs investissement BRVM

Pour l’investisseur particulier moyen en Côte d’Ivoire, investir sur le BRVM est une solution plus sûre, plus simple et plus régulière pour construire un patrimoine.

Un élevage de poulets peut générer des rendements élevés, mais il exige :

une discipline stricte,

une gestion quotidienne,

une forte tolérance au risque sanitaire,

et un fonds de roulement solide.

Stratégie équilibrée recommandée :

👉 Construire d’abord une épargne et un flux d’investissement via le BRVM, 👉 Puis se lancer dans un élevage de poulets lorsque le temps, le capital et l’expérience permettent une gestion réellement professionnelle.

Contributed by Ajibola Awojobi, founder and CEO of BorderPal.

As the sun rises over Lagos, Adebayo, a young Nigerian fintech entrepreneur, stares at his computer screen. His brow furrowed in concentration and his startup, a mobile money platform to bring financial services to the unbanked, has just secured significant funding from a Silicon Valley venture capital firm. It should be a moment of triumph, but Adebayo feels a gnawing sense of unease. The numbers on his screen tell a troubling story: his company is spending $20 to acquire each new customer, yet the average revenue per user is a mere $7.

Adebayo’s predicament is not unique. Across Africa, fintech startups are grappling with a challenging reality: the cost of customer acquisition often far outweighs the immediate returns. This scenario raises a critical question: Is Africa’s venture capital-backed fintech model sustainable or fundamentally broken?

VCs and the Promise of African Fintech

The African continent has long been considered the next frontier for fintech innovation. With a large unbanked population and rapidly increasing mobile phone penetration, the potential for transformative financial services seemed boundless. Venture capitalists, enticed by the prospect of tapping into a market of over a billion people—half without any formal bank account—have poured billions of dollars into African fintech startups over the past decade.

These investments have fueled remarkable innovations. From mobile money platforms that allow users to send and receive funds with a simple text message, to AI-powered credit scoring systems that enable microloans for small businesses, African fintechs have been at the forefront of financial inclusion efforts.

However, as Adebayo’s experience illustrates, translating these innovations into sustainable businesses has proven to be a formidable challenge.

While Adebayo grapples with his early-stage startup’s challenges, a major African fintech player with a customer base of 300,000 users has just raised a mammoth $150 million, which brings its total funding to nearly $600 million. Based on a customer acquisition cost and revenue per customer established earlier, the economics of this deal seem precarious at best. A quick calculation reveals that the company would have spent around $6 million just to acquire its current user base while generating only $2.1 million. The funding, while impressive, thus raises serious questions about the sustainability of this model and the investors’ expectations.

These scenarios serve as a stark illustration of the broader challenges facing the African fintech sector. It highlights the disconnect between the vast sums of venture capital flowing into the industry and the on-the-ground realities of customer acquisition and revenue generation. For a company to justify such a massive investment, it would need to dramatically increase its user base, significantly reduce its customer acquisition costs, or find ways to generate substantially more revenue per user. Achieving any one of these goals in the complex African market is a tall order; achieving all three simultaneously is unarguably a Herculean task.

The funding also underscores the potential for overvaluation in the African fintech space. While such large investments can provide companies with the runway needed to scale and innovate, they also create immense pressure to deliver returns that may not be realistic given the current state of the market. This pressure could lead to unsustainable growth strategies, prioritizing user acquisition over building a solid economic foundation.

Balancing Profitability & Cost of Growth

The core of the problem lies in the high cost of customer acquisition. According to a McKinsey analysis, some fintech companies in Africa spend up to $20 to onboard a single customer, only to generate $7 in revenue from that customer. This imbalance is staggering and points to deeper structural issues in the market.

Several factors contribute to these high acquisition costs. First, there’s the challenge of digital literacy. Many potential customers, particularly those in rural areas, are unfamiliar with digital financial services. This necessitates extensive education and handholding, driving up the cost of onboarding.

Secondly, Africa’s diverse linguistic and cultural landscape requires tailored marketing approaches for different regions. A strategy that works in urban Lagos may fall flat in rural Tanzania, forcing companies to invest heavily in localized marketing efforts.

Infrastructure challenges also play a significant role. The lack of robust digital infrastructure in many African countries is partly responsible for the high customer acquisition costs. Poor internet connectivity, limited smartphone penetration, and unreliable power supply in some areas make digital onboarding processes more difficult and expensive. Moreover, many consumers are wary of new financial services, requiring significant investments in building trust and credibility.

The high customer acquisition costs are reflected in the overall profitability of digital banks globally. A BCG Consulting analysis revealed that only 13 out of 249 digital banks worldwide, or 5%, are profitable, with 10 of those firms being in the Asia Pacific region. This statistic underscores the challenges digital banks face, particularly in emerging markets like Africa.

This reality presents a conundrum for venture capital firms accustomed to the rapid scaling and quick returns seen in other tech sectors. The traditional VC model, focusing on exponential growth and relatively short investment horizons, may not be well-suited to the realities of building sustainable financial services in Africa.

Rethinking the Model

As awareness of these challenges grows, both entrepreneurs and investors need to rethink their approaches to fintech in Africa, taking into consideration the high cost of acquiring customers and the state of the continent’s digital infrastructure.

One promising avenue is the development of white-label infrastructure. By creating common technological solutions that can be customized and branded by different companies, fintechs can significantly reduce their development costs. This approach could be particularly effective for services like Know Your Customer (KYC) systems or payment processing platforms.

Taking the white-label concept further, an innovative solution is emerging: white-labeled services provided by community leaders with large networks in rural settings. This approach could help fintechs lower the cost of building their customer base. By leveraging the trust and influence of local leaders, companies can reduce the cost of onboarding and education. Word of mouth spreads faster in close-knit communities, potentially accelerating adoption rates and lowering acquisition costs.

Partnerships with established institutions are another strategy gaining traction. By collaborating with banks, telecom companies, or large retailers, fintech startups can leverage existing customer bases and distribution networks, potentially lowering acquisition costs.

Some companies are shifting their focus from B2C to B2B services. Targeting businesses rather than individual consumers could lead to lower acquisition costs and higher average revenue per user. For instance, providing payment processing services to small businesses or offering financial management tools to cooperatives could be more cost-effective than trying to onboard individual users one by one.

There’s also growing interest in impact-focused investment models. These approaches prioritize long-term social impact alongside financial returns, potentially allowing for longer runways and more sustainable growth strategies. Such models might be better suited to the realities of building financial infrastructure in emerging markets.

What Does the Future Hold?

As Adebayo contemplates his startup’s future, he realizes the path forward will require a delicate balance between growth and sustainability. The dream of bringing financial services to millions of unbanked Africans remains as compelling as ever, but the route to achieving that dream may need to be recalibrated.

The future of African fintech likely lies in a more nuanced approach to growth and funding. Rather than pursuing rapid scaling at all costs, successful companies must focus on building sustainable unit economics from the ground up. This might mean slower growth in the short term, but it could lead to more robust and impactful companies in the long run.

This shift may require adjusting their expectations and investment strategies for venture capital firms. Longer investment horizons, more hands-on operational support, and a greater focus on a path to profitability rather than just user growth could become the norm.

The story of African fintech is far from over. The potential for transformative impact remains enormous, and the ingenuity and determination of entrepreneurs like Adebayo continue to drive innovation across the continent.

However, realizing this potential will require a reimagining of the current VC-fintech model. By addressing the challenges of high customer acquisition costs, exploring alternative business models, and fostering more supportive regulatory environments, the industry can evolve into a more sustainable and impactful force for financial inclusion.

As the sun sets on another day of hustle and innovation in Africa’s tech hubs, one thing is clear: the future of fintech on the continent will be shaped not just by technological breakthroughs, but by the ability to create sustainable, profitable businesses that truly serve the needs of Africa’s diverse populations. It’s a challenge that will require patience, creativity, and a willingness to rethink established models – but for those who succeed, the rewards could be transformative, not just for their businesses, but for millions of Africans seeking access to vital financial services.

Contributed by Mathias Léopoldie, Co-Founder of Julaya via Realistic Optimist.

Optimizing for home runs

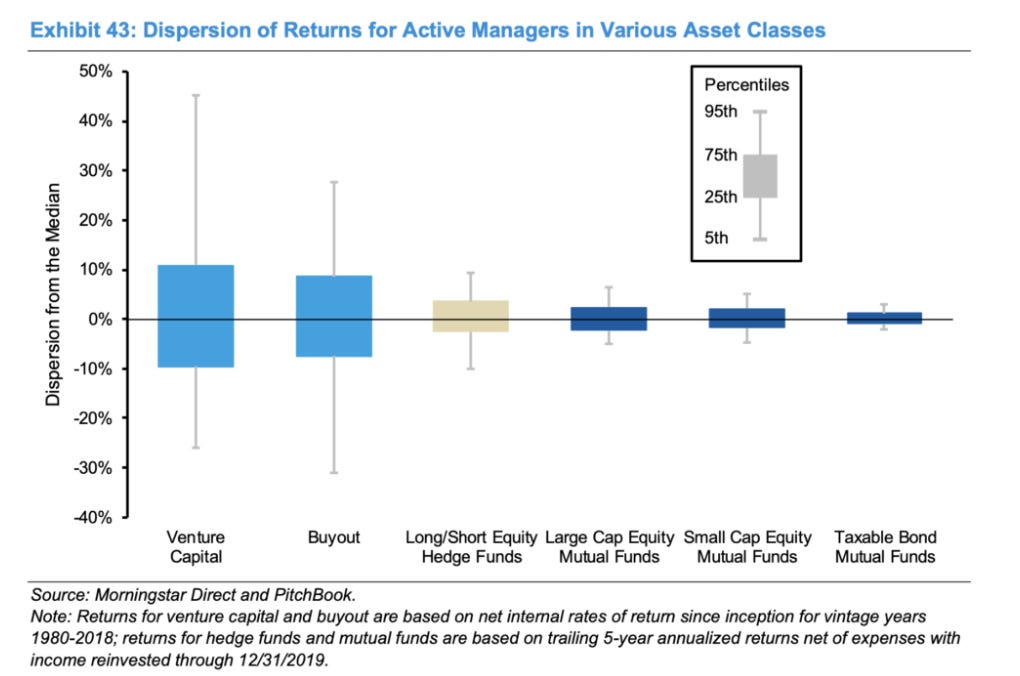

It is said that the first venture capital (VC) firm was founded in 1946, in the USA. The American Research & Development Corporation (ARDC) became famous for its $70,000 investment in Digital Equipment Corporation, a computer manufacturer, which went public in 1967 at a whopping $355M valuation. Investors taking risky bets on companies wasn’t new, but the computer era put venture capital’s singular “power law” on full display.

A baseball game is an apt analogy to conceptualize how venture capital works. The most exciting play, which also brings outsized returns, is when the ball skyrockets over the fence resulting in a home run.

VC is quite similar, as the power law nature implies that a few investments (<5%) will drive most of a fund’s returns. While the number of home runs in baseball might not guarantee winning the season, it does in VC.

This is why VC is an exciting asset class: sharp skill and experience are necessary, but luck plays a non-negligible role. It is no surprise that, amongst asset classes, VC has the highest dispersion of returns. Participants can either win big or lose a lot.

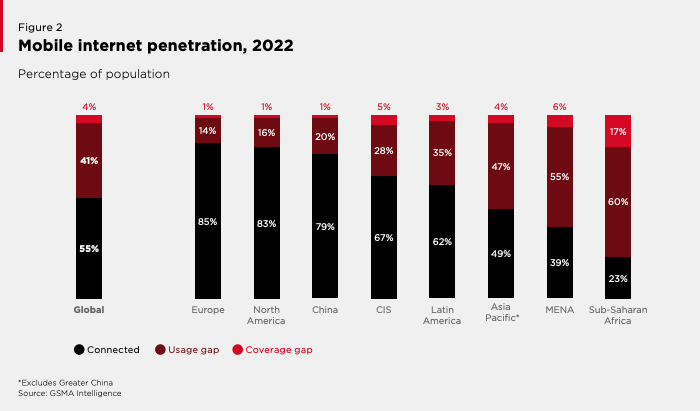

The African VC ecosystem is young, inching past its first decade of existence. The African internet revolution took a different shape than it did elsewhere: between 2005 and 2019, the share of African households possessing a computer went from 4% to 8%, while other developed economies witnessed a 55% to 80% jump over the same period.

One can’t expect a VC industry to suddenly flourish in an economy where microchip-equipped computer and smartphone ownership is so scarce. The heart of the VC industry is called “Silicon Valley” for a reason.

Another trend, however, calls our attention. Namely, the rise of mobile phones on the continent. Currently, over 80% of Africans own a mobile phone, a figure that reaches close to 100% in some countries. The 2000s-2010s feature phone mass production era is to thank. Transsion Holdings, a Chinese public company, tops the leaderboard in terms of mobile phones sold in Africa, through its portfolio of brands (Tecno, Itel, and Infinix).

This offline, ‘computerized’ revolution of sorts is significant for the continent, as a large part of Sub-Saharan Africa’s population still lacks internet access. This includes people who own a feature phone but no smartphone, or people for whom the cost of internet data is prohibitively expensive. Internet’s geographical reach in Africa also remains patchy, further complicating the equation.

Unsurprisingly, telecom operators have emerged as this mobile phone revolution’s winners. The mobile money industry is a striking example: a fertile mix of USSD technology and agent networks enabled telecom operators to become fintech companies as far back as 2007. Those same telcos now derive a significant amount of their business from the financial services they ushered in. M-Pesa, Kenya’s leading mobile money service provider, now accounts for more than 40% of Safaricom’s (its parent telecom operator) mobile service revenue.

In Sub-Saharan Africa, 55% of the population possesses a financial account, with mobile money’s rise boosting that number in recent years. That’s approximately double the amount of Africans with an internet connection.

Too early to call

In this context, many are the Cassandras lamenting venture capital’s failure in Africa. These conclusions seem premature, both because the industry itself is novel but also because the digital ecosystem it operates in is still nascent.

Even by removing Africa from the picture, venture capital is a long-term industry, and its illiquidity can lead to prolonged exit times. According to Dealroom, only 17% of portfolio startups globally exit within the investment period of 10 years. Initial, tangible VC investments in Africa debuted around 2012. We believe that the pessimists are neither right nor wrong: they’re just pontificating too early.

That being said, the past decade has drawn the contours of what can be improved and highlighted what has worked.

# years it takes for portfolio startups to exit, along with exit size (Dealroom)

The casino analogy

Casinos constitute another pertinent venture capital analogy. Addiction and money laundering aside, a casino is a fascinating business. In a casino, a few people win exuberant amounts, while the many ‘losers’ subsidize the entire operation. In return for setting up the infrastructure, applying rules, and mediating disputes, the casino pockets a handsome amount of the proceeds as profits.

Venture capital’s logic is similar to a casino’s. “Winners” are the top decile of skilled VC funds reaping outsized returns. “Losers” are the VC funds that don’t return the amount of money they promised their investors (LPs). The casino itself is the government, collecting tax revenue in return for organizing the game.

Without casinos’ power law gains distribution, no one would play. It is by design that ‘returns’ are extremely skewed, enabling the casino economy to work. VC is similar: it is by design that most of the returns come from the top decile funds and companies because winning in venture capital is hard. It wouldn’t be possible without the entire ecosystem structure, and failing companies still provide tremendous value to the other players.

Mixing profitability and venture scale

While far from a solely African problem, the confusion between these two terms may cause damage. In light of hostile, macroeconomic conditions, many Africa-focused VCs have started demanding that their startups reach “profitability” even if this means compromising on hyper-growth.

This is partly a mistake: if investors want to invest in profitable African businesses, they can invest in African banks for example, which exhibit fantastic ROIs. Or switch to private equity. But that isn’t the VC game.

VCs demanding that their portfolio companies, especially young ones (pre-seed and seed stages), become profitable quasi-eliminates any potential “home-run” companies. The latter can only emerge through market share dominance, a process facilitated by operating at a company-level loss when competitors can’t. Those home-run companies are the only way a VC can reach the outsized returns it promised its LPs.

Herein lies the confusion between profitability as a whole and positive unit economics at the marginal level. VCs should be encouraging their portfolio companies to reach “venture scale”. Venture scale is the ability to grow at a decreasing and very efficient marginal cost. This implies tinkering and getting unit economics to a point where the revenue generated from each unit sold is superior to what it costs to make it. This metric is referred to as the “contribution margin”.

A company with a positive contribution margin, which can be unprofitable as a whole because it has very high fixed costs (such as R&D), has a clear path to long-term profitability. This justifies pumping large amounts of money into it, enabling the company to reach the economies of scale it needs to win.

Companies continuing their fundraising route, and even going public, with iffy contribution margins either speed-run their death (Airlift) or make their lives significantly harder (SWVL). Those are the business models VCs should be wary of. However, a blind focus on company-level profitability for the sake of profitability doesn’t make much sense in the VC context. There are very useful data points that companies can follow to see if they are on the right path, such as the “burn multiple” or the “magic number”.

VCs investing in African startups should be cognizant of this difference as they hit the brakes during the current funding winter.

African VC: Expensive and risky, replete with singular challenges

The early innings of the African venture capital ecosystem have made two things clear: venture capital in Africa is expensive and risky.

It is expensive because lagging infrastructure might nudge startups to build out their own, which costs money, additional time, and expertise. If the infrastructure needed can’t be built in-house, such as public infrastructure (roads, etc…), the startup will have to contend with the higher prices resulting from the existing infrastructure’s inefficiencies. This is a salient problem for logistics startups, for example.

Funding high-growth businesses in Africa can thus turn out to be an expensive endeavor, generating infrastructure costs that wouldn’t be necessary in other, more developed markets.

It is riskier if funded by international funds in international currencies (USD, Euros, GB Pounds, etc…). Take Nigeria for example, one of the continent’s venture capital darlings. Earlier last year, the Central Bank of Nigeria floated the local currency (the naira) away from its traditional peg to the USD, in a bid to liberalize the economy. The move led to the naira’s sharp and sudden devaluation, revealing overarching uncertainty about its strength.

This was a disaster for Nigerian startups, especially those that reported their revenue numbers in dollars (a given if foreign investors are on the cap table). The devaluation meant that similar revenue in naira from one month to another could render just half the value in dollars.

If Nigerian startups had converted any USD from their funding rounds into naira, their buying power was also drastically slashed. From the investor’s point of view, the startup’s $USD valuation got trimmed almost overnight, due to factors outside the founders’ control. This also creates currency translation issues, making reporting of actual performance of ventures in local and USD currencies trickier and less reliable.

This is not an issue in developed markets with stronger currencies and free capital flows, such as the US or Europe. It can be reasonably assumed that this issue has contributed to Nigeria’s drop in startup investment.

To sum it all up: African venture capital is expensive because startups have to build out or deal with decrepit infrastructure hence requiring specific business models, and comparatively riskier since valuations are subject to currency-induced volatility.

The past year was also punctuated by the downfall of some well-funded African startups, failures attributed to a nebulous mix of founder wrongdoing, financial mismanagement, and outright fraud. As is often the case, very few people will uncover the full story behind these crashes.

Some observers were quick to generalize the trend, using these failures as proxies to gauge the integrity of all other African founders. Shady founders do and will always exist, regardless of the ecosystem’s maturity. There is an argument to be made that the safeguards against those founders are potentially lower in young ecosystems such as Africa, where governance standards have not yet been standardized and where investors are less aware of African markets’ specific features. That is a solvable problem.

These are normal ecosystem growing pains that need to be rationally addressed but are no cause for doomsday rhetoric.

What’s needed: liquidity

Venture capital’s equation is simple: can you invest in startups that will exit, and will those exits return (much) more money than your LPs put in while creating economic value for the clients, suppliers, and all stakeholders?

Exits, meaning a startup getting acquired or going public, are crucial to the venture capital ecosystem’s health. VCs are investing with the intention of outsized exits, but sometimes those turn out to be impossible. Adverse market conditions, a non-scalable business model, founder conflict… Exits can be jeopardized for various reasons.

When such a situation arises, invested VCs will sometimes face the choice of either settling down for a smaller exit or losing their money outright. We believe that the importance of these small exits, such as “acquihires” should not be underestimated as they remain important for VCs required to distribute to their LPs. Typically, they will also provide cash-outs for angel investors, employees, public institutions, and founders. These cash-outs will hopefully convince these stakeholders to pour money back into the ecosystem, launching a virtuous flywheel.

While the number of exits has been increasing on the continent, actual numbers of their combined value are hard to come through (many deals don’t disclose their terms). Briter Bridges also interestingly notes that the countries and sectors receiving the most amount of funding aren’t necessarily the ones with the most lucrative exit paths.

Liquidity events are essential to Africa’s VC market. So far, most of the attention has gone toward fundraising numbers, a relevant proxy for market sentiment but not market viability or growth. More attention should be paid to the African exit market, its intricacies, its possibilities, and its obstacles.

The future of African M&A

An overwhelming majority of exits for African startups today entail a merger/acquisition (M&A).

Two African M&A trends are likely to materialize over the next couple of years.

First is the consolidation of African startups operating in the same sector yet different geographies, and struggling to live up to the valuation they raised. The recent Wasoko-MaxAB merger announcement is an example of such.

Second is the potential rise of “south-south” startup acquisitions. The socio-demographic similarities between emerging markets make the solution built in one place potentially applicable to another, even thousands of miles away. This seems to be truer for lesser regulated sectors, such as edtech or e-commerce, but harder for more supervised ones, like fintech. The recent Orcas-Baims acquisition is an example of such a deal.

Players such as Brazil’s Ebanx, Estonia’s Bolt, and Russia’s Yango Delivery all operate in Africa and represent new competitors (and potential acquirers) for local African startups. This could stimulate the local M&A scene, but more importantly, entice other well-capitalized startups in emerging markets to expand to Africa.

Conclusion

Venture capital in Africa is a recent phenomenon, one whose success can’t yet be pronounced due to the sector’s long-term nature. These early years have highlighted the specificities of African venture capital, some of which aren’t relatable to more developed markets or even other emerging markets. This means copy-pasting Western frameworks in the African context is a faulty and lazy approach.

Foreign and local VCs investing in African startups should seek to deeply understand the continent’s intricacies, and develop fresh strategies to deal with them.

The ecosystem should give itself time. Adopting a longer-term view discounts short-term pessimism and allows one to rationally solve the challenges that arise. African venture capital can be a fantastic locomotive for African growth, but railroads don’t get built overnight.

As the Bambara saying puts it, munyu tè nimisa : one never regrets patience.

Mathias Léopoldie is the co-founder of Julaya, an Ivory Coast-based startup that offers digital payment and lending accounts for African companies of all sizes. Julaya serves over 1,500 companies, processes $400M of transactions, and has raised $10M in funding.

Julaya has offices in Benin, Senegal, France, and Ivory Coast.

Mathias would like to thank Mohamed Diabi (CEO at AFRKN Ventures) and Hannah Subayi Kamuanga (Partner at Launch Africa Ventures) for their thorough advice on this piece.

How data & technology are ushering a new era of business financing, from the lessons of M-Kopa to the success of Untapped Global.

The Internet promised us a dematerialized society, where information, services, and money would travel through its digital rails at the speed of light.

Software – with almost zero cost of replication and distribution – would be the new oil.

The world would be a global village where prosperity & democracy would triumph.

LMAO 😅

There is some truth to this early 2000s tecno-optimism.

I am writing this article from my bedroom. Thanks to LinkedIn, Substack, and Gmail, I can distribute my content for free and be part of global conversations.

If I push hard on data analytics, I can learn how to better engage with my audience and eventually upsell a paid subscription (at best), or cross-sell healthy ginger drinks and productivity courses (at worst).

How many gatekeepers have I avoided thanks to a bunch of geeks wearing pajamas, writing code in their dorms, and playing Dungeons & Dragons?

And even if we zoom out and think about the continent, we can say the Internet Revolution has partly delivered on its promise. How many Africans have benefited from access to financial services, remote job opportunities, better & tailored education, and free entertainment? A whole lot!

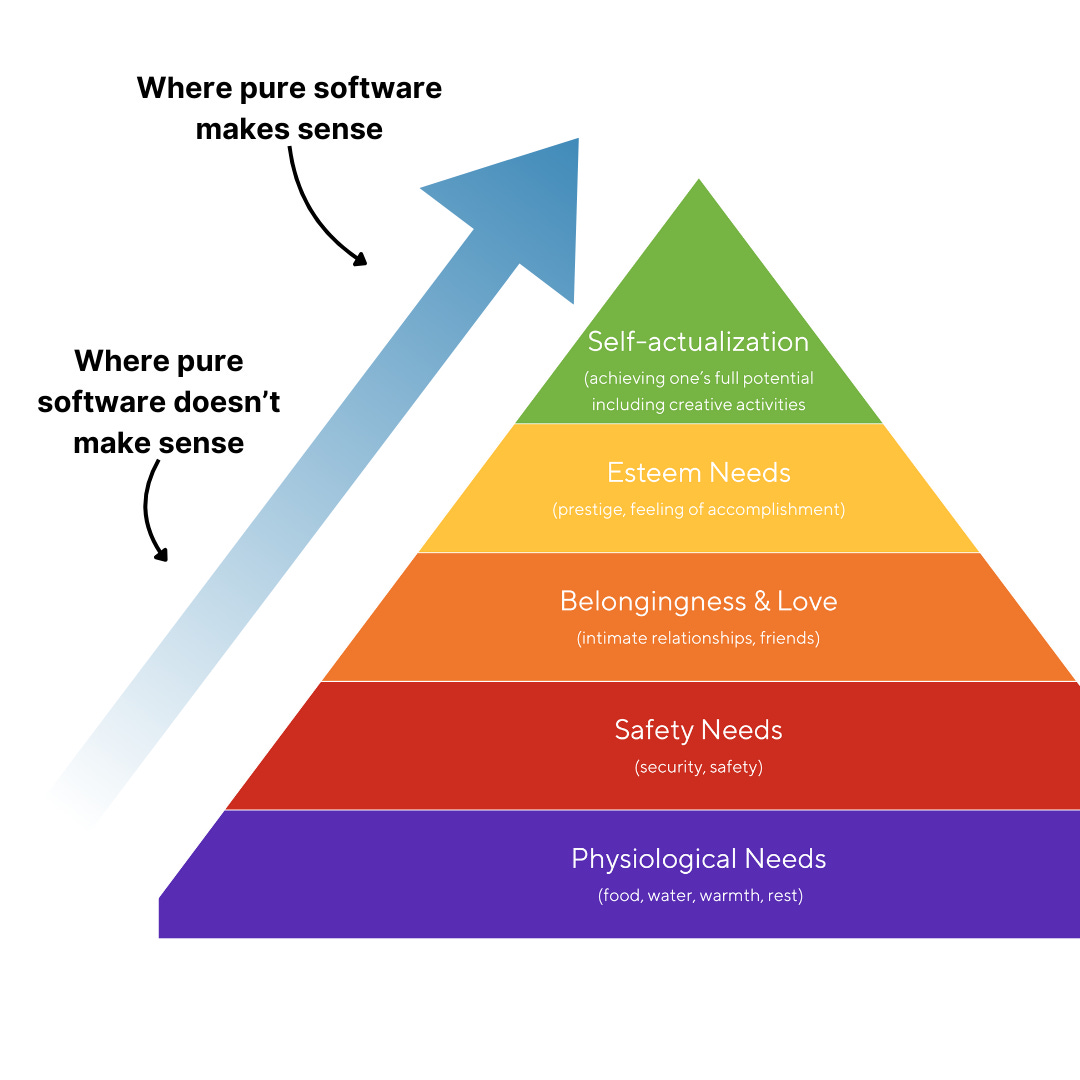

There is a problem with this story, though. The problem with the Digital Eden narrative is that it omits one crucial, underlying assumption: software is only useful when it sits “on top” of something.

We don’t eat software, we don’t shelter with software, we don’t commute with software, we don’t irrigate our lands with software.

Software enables, software improves. Software does not make.

To say with the Maslow Pyramid: pure software is useful at the top, not at the bottom.

You can leapfrog landline internet because everyone has a mobile phone, fine.

But you can’t leapfrog the two fundamental layers on top of which software can unlock its benefits: physical assets and business structures, to move atoms & transform raw stuff.

Digital technology comes as a booster/equalizer. We might not eat software, but we can improve the productivity of agricultural land with software. Sure, once we have functioning water pipes and businesses taking care of them.

It is hard to move backward

In short, as much as we’d love to live in the metaverse, the economy needs physical, productive assets to deliver your food to the table, your 🍑 to the office, and even your email to the server. And it needs business structures that organize these assets, maintain them, and invest in them, from microscopes to trucks to refrigerators.

And…. here we come to the ❤️ of this article:

In Africa, most of these “business structures” are small-sized, informal businesses.

They desperately need financing to buy, upgrade, and maintain these physical assets.

They can’t get it (SMEs’ finance gap accounts for $136 billion 🥲)

So let me raise the following question then: if software cannot replace tractors & sewing machines, can it at least make us better at funding them? Can technology help us respond to African businesses’ capital needs?

Big Problems 🗻 x Old Incumbents 👴🏽 =New Opportunities 🦋

When we think of financing, we instinctively think of banks.

In Africa, they don’t always have a good reputation.

“African banks mobilize deposits from big enterprises, governments, and high net worth individuals, and deploy these deposits in treasury bills and federal debt. That’s their business model. They are not interested in lending to consumers or small businesses”.

It’s a punchline, but there is some truth to it.

Private credit levels are pretty low in Africa, and when it comes to SMEs, things get even dryer. As the infamous report from Proparco highlights, banks’ loans devoted to small firms in Africa “represent half of that of their counterparts in developing economies” (5% vs 13%). On top of that, only 68.7 % of SME loan applications are approved by banks in Africa, against 81.4 % in other developing countries.

So what are banks even doing with their time? Why don’t they just go out there and finance these businesses?

Of course, the answer is “complex”. But apart from banks’ problems with upstream access to capital (read: global investor shying away and crazy high interest rates), I think the main reason is:

ineffective due diligence: the methodology used to assess the credit risk of the borrower

lack of data: the data input needed for the risk management models to work

Collateral-based lending relies on tangible assets, such as real estate or equipment, that the borrower pledges as security for the loan.

This is an obstacle for many SMEs in the continent as:

they lack eligible assets to pledge as collateral;

the value of collateral assets can be required to be up to 80-100% of the value of the loan (IFC);

movable assets – like inventory and receivables – are not accepted as collateral;

assets’ appraisal is complex and can lead to operational overhead and increased risk

This makes collateral-based lending complex, expensive, and often unfeasible.

Cash flow-based lending focuses on the borrower’s ability to generate sufficient cash flow from operations to meet debt obligations.

To do that, you usually need two things:

income statements & balance sheets: to assess the future cash flows of the borrower

market data & market intelligence: to assess the health of the sector the company operates in

Guess what? Both things are very hard to find in the context of African SMEs.

Many SMEs barely maintain the financial records needed for income statements.

And and if you’ve ever tried to do some market research on the region you know that market intelligence is non-parvenu.

So what?

Lack of collaterals and hard-to-predict cash flows make these businesses 1) riskier according to banks’ current credit risk models, and 2)costly, in terms of due diligence costs, which are not justified by the size of the loan.

This is why, ultimately, African banks prefer to finance large enterprises (who usually don’t face these problems) and resort to relationship-based lending practices, which stress the borrower’s history, character, and overall trustworthiness developed through previous interactions.

#saaaad 😢

If we could find a way to lighten lending operations, access data more easily, and upgrade risk-management models, would we be able to finance more physical assets?

Is there a way technology can help us overcome these challenges?

Welcome to the world of “smart” assets… 🧠🛠️

During the past decade, several companies have come up with unique approaches to solve the finance drought of the “unbanked.

An interesting case, making the headlines for its innovative approach to financing, is Kenya’s gemstone: M-Kopa.

They have pioneered a new way to finance high-value consumer goods such as off-grid solar systems, smartphones, TVs, and refrigerators.

How did M-Kopa solve for lowering operations costs and improving data availability? With the clever combination of 3 technologies: mobile money, IoT (SIM cards) embedded in their products, and remote locking technologies.

If I borrow a smartphone with M-Kopa:

the loan is secured by the asset provided, i.e. the smartphone;

I pay daily installments with mobile money;

If I fail to pay, a remote trigger will lock my phone, so that I won’t be able to use it anymore (except for charging money to pay the amount due 😅)

The same holds for a solar system and any other product. Transparent data on assets’ usage and repayments, coupled with remote control over the asset, has proved an effective instrument in establishing initial trust with borrowers.

My repayment rates are then used for credit scoring, enabling me to access further cash loans once the smartphone is paid in full, with the phone resecured as collateral (again).

As simple as it seems, this model alone unleashed a lot of money and a lot of impact. As the GSMA report says:

“The explosive rise of pay-as-you-go (PAYG) in the off-grid energy sector, for example, has played a significant role in widening access to energy. Combining mobile money systems with machine-to-machine (M2M) communication and remote locking has made off-grid energy products more accessible and affordable to billions worldwide, bringing power for the first time to 25-30 million people worldwide between 2015 and 2020”

The recipe for success: a mix of operational excellence, IoT technology, and digital payments.

Great!

While this model proved valuable for consumers, we must remember that we want to finance businesses!

M-Kopa lends essentials with a relatively low price tag.

Is there a way we can draw from the lessons of this model and apply them to finance physical, productive assets that cost more money?

…& the world of Untapped’s smart financing 🧠✨

Back in 2021, I tried to put money into an investing vehicle by the name of Untapped Global.

I was intrigued by their model as it combined all the ingredients I was looking for at the time: a data-driven approach; a high-returns portfolio; and a tangible, positive social impact.

It turned out that I wasn’t an accredited investor and I couldn’t invest with them (sigh 😞), so I eventually ended up switching to Daba (who I didn’t know yet at the time).

However, I’ve kept an eye on them over the years, until I could finally sit down with Lundie Strom, Untapped’s Investor Relations & Partnerships Head, to chat and get a better overview of their model.

The fascinating conversation that followed convinced me that they may be on the right track: taking the best of M-Kopa and adding their own twist to it.

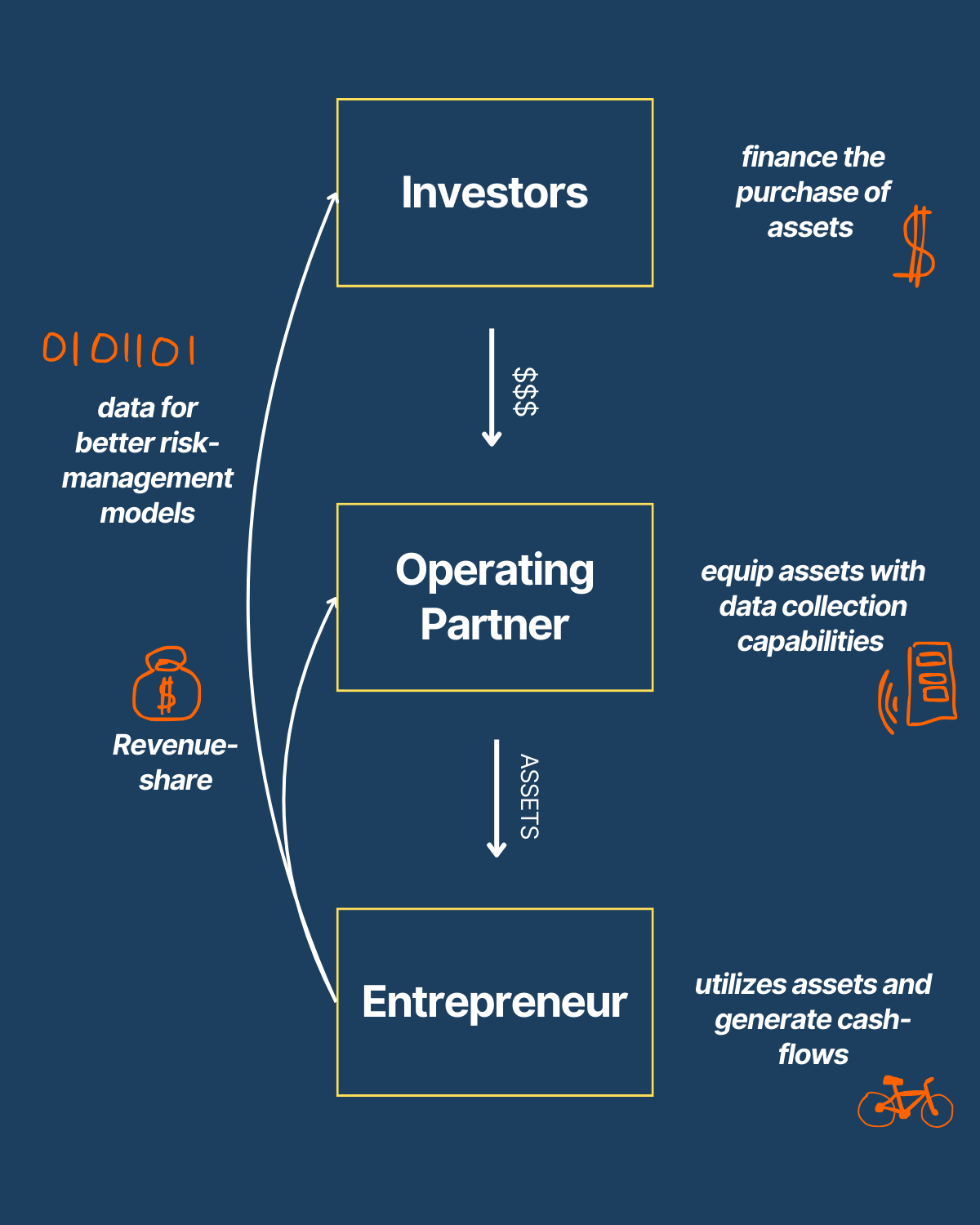

I’ll go through what I consider to be the four pillars of their model:

Revenue-share

Operating partners

Iterative approach

Real-time data

1) Revenue-based financing 💸💸💸

One of Africa’s most-funded startups, Moove, recently made the headlines as it received a 100M investment from Uber, valuing the company at 750M.

Its main business model? Revenue-based vehicle financing.

In a revenue-based financing (or revenue-share) agreement, a business receives funding in exchange for a percentage of its future revenue until a specified amount is repaid.

Instead of a fixed amount of money (+ interest rate) to be paid at regular intervals, as with traditional loans, revenue-share repayments fluctuate with the business’s income, providing flexibility during low-revenue periods and faster repayment times during bonanza: investors’ returns are aligned with the company’s performance.

In the case of Moove, they finance cars for Uber drivers. The loan is repaid with a share of the revenues the Uber driver makes: as simple as that.

At a high level, Untapped does the same. It finances productive assets and gets paid back with the revenues these assets generate.

What type of assets does Untapped finance? Cars? Motorbikes? Generators? Well, all of them. It doesn’t really matter.

And here is what distinguishes Untapped from Moove, and what makes their model more interesting and more scalable.

2) Operating partners ⛑️⛑️⛑️

Moove is good at financing cars for Uber drivers. It is not a trivial task and they had to become good at it.

Why? Two reasons.

First ☝🏽, managing a fleet of vehicles demands domain expertise and operational overhead.

Moove needs to develop proprietary tech & manage the integration with Uber to have visibility on how the vehicles are utilized, how much revenue is generated, and receive timely payments. It is a lot of plumbing.

They also need to partner with car manufacturers for steady supply & support services, and create a system to onboard drivers and evaluate their creditworthiness and performance. Again, a lot of plumbing.

Second ✌🏽, Moove itself is subject to credit risk. They don’t purchase the vehicles from their balance sheet money: it would be too capital-intensive. They have to take up loans/financing from creditors. And given they offer revenue-share deals to their drivers, they have to juggle between variable repayments from drivers vs fixed installments they owe their creditors.

This is the main reason we don’t see many companies like Moove around. While revenue-share agreements are attractive to drivers, part of their business risk rolls up to the company borrowing them.

Now, how does Untapped fit in this picture?

“We don’t know how to manage a fleet of vehicles”, says Lundie.

“We partner with the likes of Moove, who know the realities on the ground, and relieve them from part of their credit risk by striking a revenue-share agreement with them”.

“We don’t want to replace Moove. We want to invest in dozens of the best Mooves across multiple industries, geographies, currencies – and be their complementary source of capital”.

In this sense, an operating partner is a company focused on one vertical (like Moove with cars).

has the technical skills to collect & integrate data from the assets and the underlying businesses

Untapped can invest in it!

As a result, the interests of all the actors, from the drivers to the Mooves, to the ultimate investors in the physical assets, are aligned. Aligned along what? Well, the revenues the assets generate!

A little sketch:

Ok cool, so how does Untapped manage its own risk?

3) Iterative approach 🌀🌀🌀

“We always invest in two stages. No matter the size of the company, at the beginning every operating partner starts with a pilot”.

This means $50-100k as a first check for a 4 to 6-month period: “We put money in your hands and see what you can do”.

In practice, this helps the team tick some boxes: how many assets can you deploy? What is the quality of your data? Can you integrate data with our platform? Can you pay it back in time?

If the results are good, the company enters a scaleup stage, where investments range from 500k to 5M.

At this stage, the operating partner is expected to have already managed the data integration and be working on the payment integration, which is the hardest part (moving money from local wallets in Ghana to local wallets in the US, for example).

Out of 59 companies, only 7 have entered the scaleup phase.

“Our goal is to really pick up the best ones, those who need 5 million a year, and can achieve that scale and the impact”.

This approach of spreading the seeds and harvesting the good ones allows Untapped to manage risk efficiently while gathering loads of data.

And it’s ultimately in the data that lies the core competitive advantage of this model.

4) Real-time data 📈📈📈

Imagine a world where, when you invest in an African entrepreneur, you can have visibility on where each asset is deployed and how much money it’s making, in real-time. This is the vision of the Smart Asset Financing platform developed by Untapped.

How hard is it to integrate data from assets and businesses across different regions?

“This is our real edge. We want to be tech-driven, so our data team is working to do what currently no one is doing”.

What no one is doing is the following:

integrate data from physical assets

with data from underlying businesses using these assets (i.e. revenues),

from multiple operating partners who deployed them (i.e. tens of Moove, across business verticals);

To do what?

Monitor your entire portfolio in real-time,

paying your investors as the money comes in,

develop proprietary risk management models

To me, it sounds a bit like a command center, where you can say: “OK, we financed 10,000 entrepreneurs. What is happening on the ground? How well the money is moving around? How much are we making? Should we scale back on something?”

It’s a pretty compelling vision.

The question then is, how far are we from a world like this?

“Data integration and especially payment integration, is still hard. We need to provide technical assistance to some of our earlier stage operating partners because not everyone has those capabilities yet”. Also, “moving money from local wallets to regional wallets to the US, is still a headache, and a problem that no one completely solved yet”.

Smart Asset Financing is the first iteration aiming to deliver on this promise, and challenges of this kind can only be solved with tunnel vision.

So what’s in it for us? 🤷🏽🤷🏽🤷🏽

After the conversation I had with Lundie, my brain was like “There needs to be more of this”. If we take it back from where we started, it’s a no-brainer.

SMEs are the lifeblood of the African economy.

To continue delivering products and services each of us needs, they need capital to purchase and maintain physical assets.

IoT, digital payments, and the smart distribution of risk & operational overhead have paved the way in solving the two major bottlenecks preventing traditional banks from helping them: credit risk modeling and data availability.

Untapped has worked its way through novel ways of addressing this challenge. Others are doing that too. We need to learn from them, copy and iterate.

How much more wealth would there be if there wasn’t just one Moove, but one hundred Mooves?

How much more resilient our economies would be, if, instead of just cars, we could finance irrigation systems, trucks, and medical devices?

I don’t know, but I definitely want to hear more stories like this.

Contributed by Ajibola Awojobi, founder of BorderPal.co by ErrandPay.

Flashy new tech companies and cutting-edge tech get a lot of buzz. But for investors, the real excitement lies in booming tech hubs, areas where new companies are constantly popping up, fueled by money from around the world. These up-and-coming hubs offer a chance for quick profits compared to the crowded tech industries in more advanced markets.

That has been the tale of fintech in Africa over the past few years. Many in the global investment community have looked at the continent as the “future” or “next frontier” of financial technology, with investments flooding into the sector at an unprecedented rate.

From 2016 to 2022, funding for African startups grew 18.5x, 45% of which was attributable to fintech, per a McKinsey report. In the eight years to 2023, nearly $4 billion in equity funding was poured into fintech startups, while the sector accounted for around half of the total financing raised last year.

The surge in funding is partly behind the boom in Africa’s fintech, propelling it to rank as one of the fastest-growing in the world. But the concentration of investor capital on a select few players (in 2023, 75% of all equity funding secured by African fintech startups went to just ten companies) has inadvertently made the sector a “land of giants” of some sort. This top-heavy ecosystem may overlook a vast untapped potential.

A handful of well-known names dominate fintech headlines and funding. Companies like Flutterwave, Chipper Cash, MNT Halan, TymeBank, Wave, Jumo, and OPay have become household names, nearly all valued at over $1 billion. While their success is commendable, this concentration of resources raises a crucial question about the broader impact on financial inclusion across the continent. It limits innovation and creates a narrow funnel for financial services distribution, potentially leaving millions underserved.

Despite the growth of fintech, financial exclusion remains a significant challenge in Africa. Sub-Saharan Africa’s banked population jumped from only 23% in 2011, but most Africans still do not have bank accounts.

Around 360 million adults in the region do not have access to any form of account—roughly 17% of the global unbanked population, per World Bank estimates. This vast number represents not just a challenge but an enormous opportunity for a different kind of financial innovation and venture building.

“Undiscovered Founders”

Traditional financial institutions and even fintech startups have struggled to reach these populations due to various factors, including low urbanization rates, infrastructure limitations, high operational costs, and a lack of tailored products. This is where the power of undiscovered founders lies.

These religious leaders, community leaders, and small business owners have established trust, credibility, and deep connections within their local communities. Still, they may lack the technical expertise or capital to launch fintech ventures. They understand their neighbors’ financial needs and challenges, acting as bridges between the formal and informal economic sectors.

The power of these untapped networks cannot be overstated. In many African communities, trust is currency, and these leaders have spent years building social capital. For instance, a pastor in a rural Nigerian village might have more influence over financial decisions in their community than any glossy marketing campaign from a Lagos-based fintech company.

While these potential founders hold immense potential through their network and trust, they face significant challenges in leveraging these to provide tech-driven financial services.

Access to capital is a major obstacle. Banks view them as high-risk borrowers, while traditional venture capital rarely reaches these individuals, making it difficult to secure funding for starting or expanding financial service offerings. In addition, many lack the technical skills to build and maintain fintech platforms, while navigating the complex world of financial regulations can be daunting.

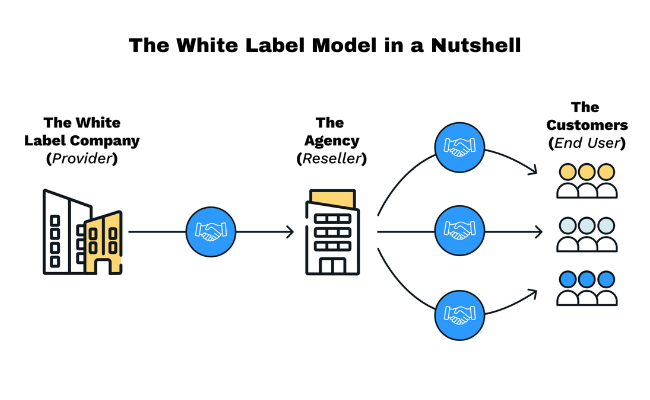

Here’s where the concept of white labeling emerges as a game-changer. Put simply, white labeling is the practice of one company making a product or service that other companies rebrand and sell as their own. This model could be adapted to empower undiscovered founders by providing them with ready-made, compliant fintech solutions (technological infrastructure and core services) that they can brand and distribute within their networks.

Imagine a community leader partnering with a fintech company to offer their congregation or local businesses branded mobile wallets or microloans. The established company handles the complex back-end technology and regulatory compliance, while the community leader leverages their trusted network for customer acquisition.

This approach solves several problems simultaneously: undiscovered founders get affordable access to advanced technology, existing trust networks are leveraged for customer acquisition, and regulatory compliance is ensured through the central platform. It also offers a distinct advantage over traditional funding models. Empowering multiple “mini-startups” across the continent through this model could prove more cost-effective than pouring resources into a single large-scale venture.

The analogy of Coca-Cola’s distribution system comes to mind. Its success in reaching even the most remote parts of Africa is attributed to its micro-distribution centers (MDCs) in Africa — small hubs that distribute beverages to small retailers.

Over 3,000 are usually run by individuals who live in the community; they employ local people and handle the last-mile distribution. They create around 20,000 jobs and generate millions of dollars in annual revenue. Similarly, empowering undiscovered founders creates a capillary network of financial service providers, reaching the farthest corners of the continent.

Consider the cost-effectiveness: Imagine funding 100 local leaders, each reaching 1,000 individuals, compared to funding one large fintech startup aiming to reach 100,000. The white-labeling model fosters a more cost-efficient and geographically expansive approach to financial inclusion. Instead of one company trying to penetrate diverse markets, hundreds or thousands of local leaders could adapt services to their specific communities.

Beyond financial inclusion

Increasing account ownership and usage could increase GDP by up to 14% in economies like Nigeria. By leveraging undiscovered founders, we could accelerate this growth while ensuring it’s more evenly distributed. However, the implications of this model extend far beyond just increasing access to bank accounts or broad financial services.

Empowering local leaders as fintech distributors could increase job creation, as each mini-startup creates multiple jobs within its community. Profits from financial services would stay within local communities, and local founders would be best positioned to understand and meet their communities’ specific needs, thereby creating more tailored products.

As trusted figures introduce these services, they could play the crucial role of financial educators, dispelling myths and building trust around formal financial services. Financial literacy is essential for making informed financial decisions and avoiding predatory lending practices. Undiscovered founders can bridge the knowledge gap, fostering a financially responsible citizenry.

While promising, this model is challenging. Ensuring quality control across numerous mini-startups, managing regulatory compliance, and preventing fraud are all significant considerations. There’s also the question of identifying and vetting potential undiscovered founders, but these challenges are manageable. With proper systems in place, including rigorous vetting processes, ongoing training, and robust monitoring systems, these risks can be mitigated.

The concept of undiscovered founders represents a paradigm shift in our thinking about fintech distribution in Africa. We can create a more inclusive, resilient, and far-reaching financial ecosystem by leveraging existing trust networks and empowering local leaders.

This approach aligns with the African proverb, “If you want to go fast, go alone. If you want to go far, go together.” While the current model of concentrated investment may lead to rapid growth for a few companies, empowering undiscovered founders could take us much further in achieving true financial inclusion.

As we look to the future of fintech in Africa, it’s time to broaden our perspective. The next big innovation in financial inclusion might not come from a tech hub in Nairobi or Lagos but from a small shop owner in rural Tanzania or a community leader in suburban Ghana. By providing these undiscovered founders with the tools they need, we can unlock a new wave of innovation and inclusion, bringing financial services to millions who traditional models have left behind.

The potential is enormous for financial returns and social impact, economic empowerment, and the realization of Africa’s full potential in the global digital economy. It’s time to discover the undiscovered and rewrite the story of fintech in Africa.

Flagging. That’s how we would describe the African tech startup funding scene in 2023.

Global macro headwinds saw investors cut fewer checks and some reportedly backed down from commitments, forcing a slew of startup shutdowns and downsizing.

While on the surface, it seems Africa’s VC funding figures fell far from 2021 and 2022 levels, available estimates suggest the continent’s startups still managed to attract more than $5 billion.

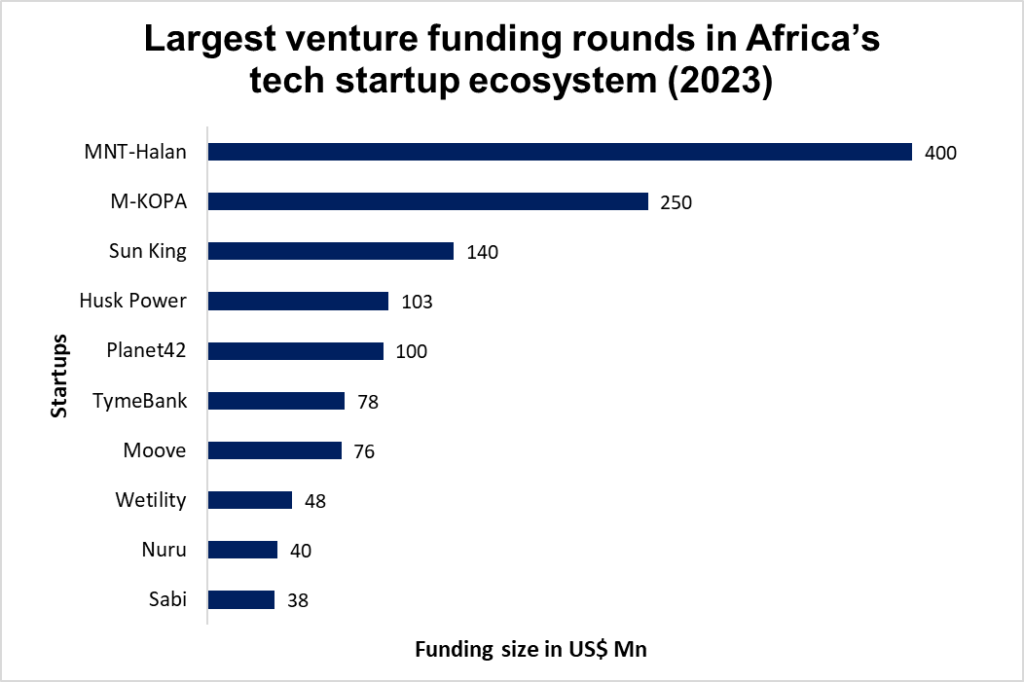

Before the year’s scorecards start to roll out, we take a look at the top 10 largest fundraising rounds in the African tech startup industry this year and the trends they reveal.

Fewer mega-deals (just four >$100m rounds vs nine in 2022):

This signifies a shift towards cautious optimism from investors.

While big bets still happen, they’re rarer, with investors preferring to spread their bets on multiple promising startups.

This could lead to a more sustainable ecosystem, with startups forced to focus on stronger fundamentals and traction before securing large funding rounds.

MNT-Halan‘s $400 million round in Egypt and M-KOPA‘s $250 million in Kenya are rare exceptions, highlighting their established market positions and potential for significant impact.

Fintech takes the top spot but the landscape is more diverse:

Fintech remains a dominant sector due to its potential to address financial inclusion challenges in Africa.

However, other sectors like cleantech and mobility are gaining traction, indicating diversification in investor interest.

This diversification can lead to a more balanced and resilient ecosystem, as the success of the startup scene is not solely dependent on one sector.

The presence of Husk Power, Wetility, Nuru, Planet42, and Moove in the top 10 shows the growing importance of these sectors in attracting investor attention.

The rising prominence of debt + equity rounds:

This hybrid approach combines the flexibility of equity with the stability of debt, offering startups a more tailored financing solution.

It can be particularly useful for startups with strong revenue models but limited access to traditional equity funding.

This trend could democratize access to funding for startups, especially in emerging markets, as it caters to startups at different stages of growth and risk profiles.

MNT-Halan, M-KOPA, Planet42, and Moove all used debt + equity rounds, demonstrating the growing popularity of this approach.

Geographical distribution

The top 10 deals primarily focus on South Africa, Kenya, and Nigeria, showcasing the continued dominance of these countries in the African startup scene.

The Democratic Republic of Congo (DRC) emerged as a surprise entry in the top 10 thanks to Nuru‘s sizable Series B round.

Series B dominance

The majority of deals being Series B raises indicates a focus on mature startups with proven traction and scalability, further highlighting likely investor risk aversion.

Overall, the top 10 fundraising rounds paint a picture of a resilient African tech ecosystem adapting to a challenging global environment.

While mega-deals were scarce, the diversity of sectors, financing models, and geographical representation suggests potential for sustainable growth in the long term.

Stay tuned to our blog for a broader piece that explores standout trends in Africa’s tech landscape in 2023 and our high-conviction themes for the new year—to be published soon!

Venmo, Cash App, and Zelle are familiar names in the world of mobile-based digital payments in the West, having revolutionized how money is transferred and received by millions of people.

But did you know that Africa has been ahead of the game with its own mobile money systems since as far back as 2007?!

That’s right.

Today, we take you on a journey of how Africa became the biggest mobile money player in the world.

Where it all began

Once upon a time, not too long ago, accessing financial services was a challenge for many Africans. Unlike in the U.S. or Europe, traditional banking services were often very limited, especially in remote and rural areas.

But then mobile money.

In 2007, Safaricom, a leading mobile network operator in Kenya, launched a mobile money service called M-Pesa. Little did they know that this innovative concept would spark a digital revolution that would sweep across the continent.

M-Pesa, meaning “mobile money” in Swahili, allowed users to save, send, and receive money using just their mobile phones. This groundbreaking innovation proved to be a game-changer, enabling people without bank accounts to participate in the formal financial system.

In 2007, Safaricom, a leading telecommunications company in Kenya, launched a mobile money service called M-Pesa. Image credit: African Markets

The initial idea behind M-Pesa was to create a convenient way for Kenyans to transfer money securely. The service quickly gained popularity, as people in remote areas, where traditional banking services were scarce, embraced it as a means to conduct financial transactions with ease.

In no time, mobile money took root and started to grow, not only in Kenya but also in neighboring countries.

M-Pesa was launched in Tanzania the following year and is now present in at least 10 countries.

So, what made mobile money so popular?

Well, let’s unravel its magic!

Imagine a scenario: a hardworking individual in a rural village wants to send money to their family in the city.

Historically, this would involve a long and costly journey, with the risk of loss or theft. But with a mobile money account, a few taps on a phone screen can instantly transfer funds to their loved ones, efficiently.

One of the key factors that contributed to the rapid adoption of mobile money was its simplicity: all you needed was a basic mobile phone, and suddenly, you had a bank in the palm of your hand.

No more long queues or complicated paperwork. Money transfers could be done with a few simple clicks.

For deposits and withdrawals, mobile money agents, often found in local shops, act as the bridge between the digital and physical worlds, allowing users to convert cash into digital currency and vice versa.

An M-Pesa agent attends to a user. Image credit: HBS Digital Initiative

By 2010, M-Pesa had acquired 10 million active users and by 2016, it served almost 29.5 million active customers through a network of more than 287,400 agents. In the same year, the service processed around 6 billion transactions, peaking in December at 529 transactions every second.

The success of M-Pesa in Kenya sparked a wave of enthusiasm. As word spread about the convenience and reliability of mobile money, its impact began to reverberate throughout the continent.

Impressed by the service, other African countries eagerly jumped on the mobile money revolution, building theirs in M-Pesa’s image.

Over the next few years, the service spread to countries like Uganda, Ghana, Rwanda, and South Africa as mobile network operators and financial institutions started realizing the immense potential of mobile money.

MTN launched its MoMo service in Uganda in March 2009 and in Rwanda in February 2010. Telesom ZAAD in Somaliland in 2009 and Hormuud launched EVC Plus in Somalia in 2011.

By 2011, more than 100 mobile money services were operating in Africa, reaching people who previously had limited access to formal financial services.

Africa continues to lead global adoption

Fast forward to today, more mobile money services have emerged in Africa while mobile money accounts and transaction value on the continent continue to skyrocket.

Africa accounted for up to 70% of the world’s $1 trillion mobile money value in 2021 after mobile money transactions on the continent jumped 39% from $495 billion in 2020 to $701.4 billion.

Last year, that rose a further 22% to a jaw-dropping $836.5 billion (bigger than the GDP of Nigeria, Africa’s largest economy!) but its share of the global $1.26 trillion mobile money value fell to 66.4%.

Per GSMA’s 2023 State of the Industry Report, mobile money is growing faster in sub-Saharan Africa than in other regions except for the Middle East & North Africa.

However, it’s not just about the numbers

Perhaps its greatest achievement, mobile money has brought financial inclusion to millions of Africans who were previously excluded from the formal economy.

Data from the World Bank shows that around 45% of people living in Sub-Saharan don’t have access to a bank account. But mobile phones are widespread across the continent and are helping to bridge the financial gap.

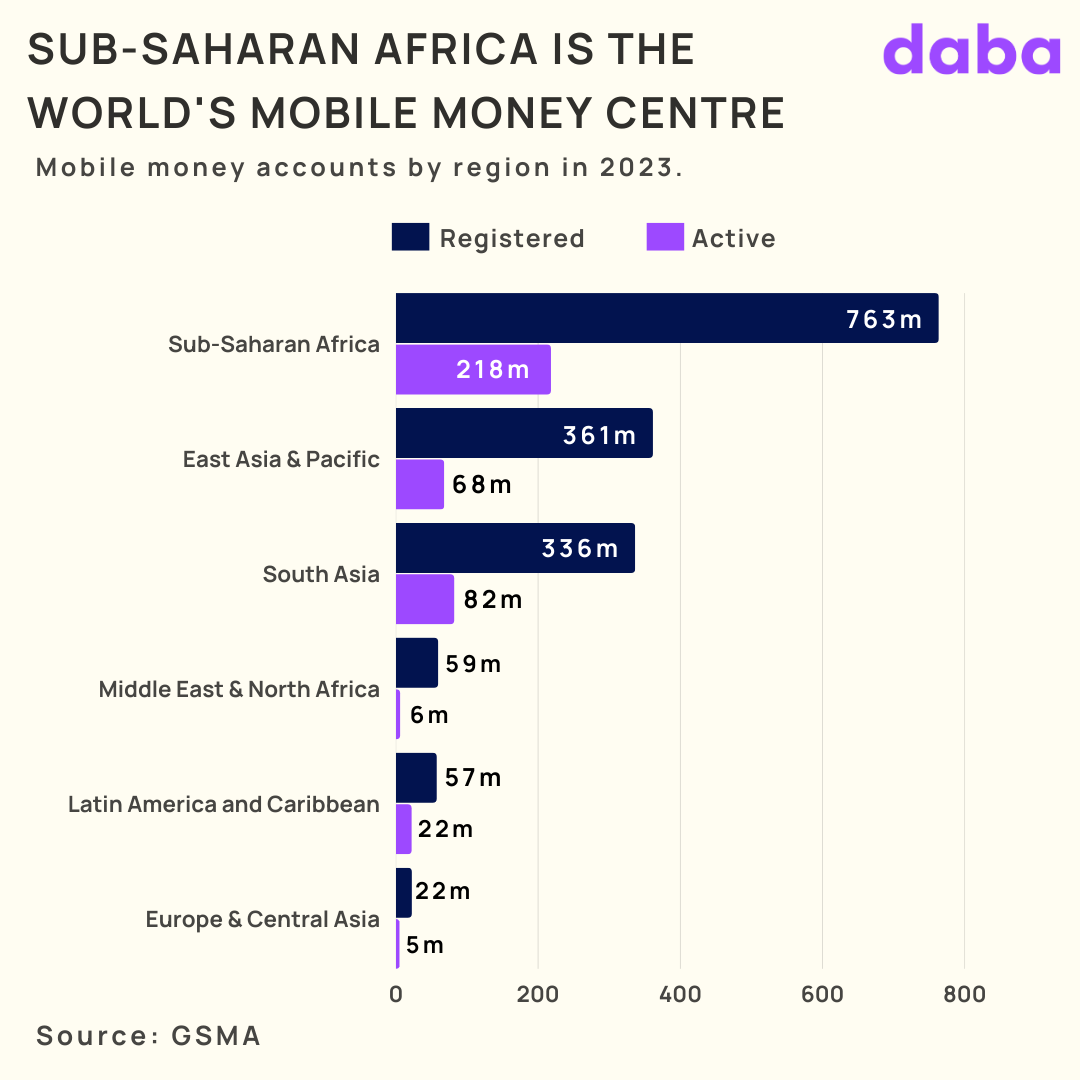

As of 2022, Sub-Saharan Africa had up to 763 million registered mobile money accounts, more than double the figures in the next closest region, and more Africans now enjoy access to a whole range of financial services that were previously out of reach.

The innovative service has empowered women entrepreneurs, allowing them to take charge of their finances and contribute to their families’ well-being; facilitated access to education and healthcare; paved the way for exciting innovations such as mobile banking apps and digital wallets.

Beyond money transfers…

Mobile money services in Africa have also quickly evolved beyond simple person-to-person money transfers and cash in-cash out.

Providers have continually expanded their services, introducing innovative features to meet the diverse needs of their users.

For instance, mobile micro-loans and savings accounts empower individuals to access credit and save money, fostering entrepreneurship.

In Kenya, M-Shwari allows users to save money and access micro-loans directly from their mobile wallets, creating opportunities for entrepreneurs and small business owners.

Partnerships between mobile money providers and other companies have expanded the range of services available, with users now able to pay their electricity and water bills via mobile money and purchase airtime from network operators.

Health organizations have integrated mobile money into their operations, enabling payments for medical services and health insurance premiums.

Despite its transformative effect across the continent so far, it’s clear that the mobile money revolution in Africa is far from over.

Innovations continue to emerge, including interoperability between different mobile money platforms, making transactions even more convenient.

The potential for digital lending, savings, and insurance services on mobile money platforms holds great promise for the future.

As the mobile money landscape continues to evolve, so is the competition. Telecom companies, financial institutions, and fintech startups are all in the race to capture a share of this rapidly expanding market.

This healthy competition will only lead to improved services, lower transaction costs, and increased accessibility for users.

The growth of mobile money in Africa is nothing short of awe-inspiring.

From humble beginnings in Kenya, it has spread like wildfire, empowering individuals, driving economic development, and transforming societies across the continent.

As mobile money continues to evolve and expand its horizons, it remains one shining example of how technology is being harnessed to drive positive change in Africa.

Africa’s fintech industry is thriving, driven by several trends including rising venture capital investments and increasing smartphone adoption on the continent. Fintech penetration in some African countries exceeds global markets and players generated revenues of around $4-6 billion in 2020, a figure that could potentially hit $30 billion by 2025.

Revenues in the financial services sector at large could grow at about 10% per annum to $230 billion by 2025. A McKinsey report examines how fintech players are carving out a share of this expanding market and what the future could look like for these innovators.

Last year marked a continued growth of mobile money worldwide. The 2023 State of the Industry Report on Mobile Money by GSMA finds that global mobile money accounts grew by 13% to 1.6 billion in 2022 from 1.4 billion in 2021, with the total transaction value surging to around $1.26 trillion.

Up to $832 billion of that came from sub-Saharan Africa, a region home to two large markets—Nigeria and Ethiopia—that spearheaded global industry growth thanks to their liberalized regulatory regimes. In addition, West Africa was the world’s fastest-growing region for mobile money adoption.