Africa’s booming economic potential holds immense opportunities, but attracting increased foreign investment requires strategic positioning by companies across the continent.

By adopting the right strategies, African enterprises can boost their appeal to overseas investors and unlock a torrent of capital to fuel innovation, growth, and resilience.

Strategies for African companies to get more foreign investments

1. Build Investment Readiness

The foundation of attracting FDI lies in ensuring that your operations, financials, and governance adhere to international best practices. Investors seek companies with sound fundamentals, global standards, and a commitment to transparency.

African enterprises must prioritize professionalizing their operations before embarking on fundraising endeavors. This includes implementing robust financial reporting, strengthening corporate governance, and adhering to industry-specific compliance requirements.

2. Leverage Investment Access Platforms

Joining pan-African fundraising platforms like Daba can significantly expand visibility and provide vetted deal channels that overseas investors trust. These platforms streamline deal flow at scale, connecting African companies with a global network of investors actively seeking opportunities on the continent.

By leveraging these platforms, African enterprises can effectively showcase their potential to a targeted audience of interested parties.

Are you a startup or early-stage company seeking to fuel your expansion? Daba provides comprehensive capital-raising solutions to propel your business. Check out this page on our website now and discover how we can help you access the resources you need to thrive.

3. Highlight High-Potential Sectors

To captivate the attention of foreign investors, it is crucial to highlight the continent’s high-potential industries beyond traditional narratives of commodities and extraction. Africa boasts numerous promising sectors, including fintech, agribusiness, renewable energy, infrastructure, and information technology.

By showcasing the growth prospects and untapped opportunities within these sectors, African companies can effectively communicate the continent’s diverse economic landscape and attract investment aligned with global trends.

4. Promote Success Stories and Social Proof

When African ventures demonstrate strong returns to early overseas backers, promoting these success stories can inspire confidence and attract further investment.

Success breeds success, and by highlighting exemplary cases of profitable ventures, African companies can leverage social proof to convert skeptics and unlock additional capital inflows. These success stories serve as powerful testaments to the potential of investing in Africa.

5. Emphasize Inclusive Economic Impact

In an era where investors increasingly prioritize environmental, social, and governance (ESG) standards, African companies must emphasize how their enterprises drive sustainable job creation, skills development, women’s empowerment, and climate resilience.

By aligning with these global priorities, African businesses can position themselves as catalysts for inclusive economic growth, resonating with the values and objectives of socially responsible investors.

Unlock the doors to growth for your early-stage venture. Daba offers tailored capital-raising solutions to help startups secure the funding they need. Visit the startups page of our website today to explore our services.

With a strategic approach and a commitment to excellence, African companies can overcome historical barriers and unlock the vast potential that foreign direct investment holds for the continent’s economic transformation.

By adopting these strategies, Africa can pave the way for a future of prosperity, innovation, and sustainable growth, fueled by the influx of global capital.

Raising capital can be a daunting challenge for startups and early-stage companies. Daba is here to simplify the process with our expert capital-raising solutions. Reach out to us today to learn how our services can help you navigate the fundraising landscape and secure the investments that drive your growth.

La part relative du stock d’IDE de l’Afrique en provenance d’Europe a diminué au cours de la dernière décennie, tandis que celle de l’Asie a augmenté.

L’investissement direct étranger (IDE) se produit lorsqu’une personne ou une entreprise d’un pays investit dans une entreprise d’un autre pays et en prend le contrôle significatif, généralement en possédant 10 % ou plus de son pouvoir de vote.

L’IDE est crucial pour relier les économies à l’échelle mondiale, car il établit des liens durables entre elles. C’est un moyen vital pour que la technologie circule entre les pays, stimule le commerce international en offrant un accès à de nouveaux marchés, et joue un rôle majeur dans la croissance économique.

Ainsi, nous discutons des principaux pays qui représentent la plus grande part des flux d’IDE vers les marchés africains. Mais d’abord, pourquoi l’IDE est-il important pour l’Afrique, et quelles sont les dernières tendances en matière d’investissement direct étranger sur le continent ?

Pourquoi l’Investissement Étranger est-il Important pour l’Afrique ?

Pour l’Afrique, l’IDE est crucial pour plusieurs raisons. Premièrement, il apporte un capital indispensable pour le développement des infrastructures, la création d’emplois et le transfert de technologie, qui sont essentiels à la croissance économique.

L’IDE facilite également la diversification des économies en introduisant de nouvelles industries et en améliorant celles qui existent déjà. De plus, il favorise le commerce et renforce l’intégration économique mondiale en connectant les marchés africains aux réseaux internationaux.

En outre, l’IDE s’accompagne souvent d’expertise, de compétences en gestion et d’un accès aux marchés mondiaux, ce qui peut aider les entreprises locales à s’étendre et à devenir plus compétitives.

En outre, il favorise l’innovation et les améliorations de productivité grâce aux transferts de connaissances et à la diffusion de la technologie. Enfin, l’IDE contribue à la stabilité des économies africaines en fournissant une source stable de financement externe et en réduisant la dépendance à l’égard de sources volatiles telles que l’aide étrangère ou les exportations de produits de base.

Ne manquez pas les opportunités d’investissement exclusives en Afrique ! Téléchargez dès aujourd’hui l’application Daba et débloquez un monde de retours potentiels tout en ayant un impact positif.

Dernières Tendances des Flux d’IDE vers l’Afrique

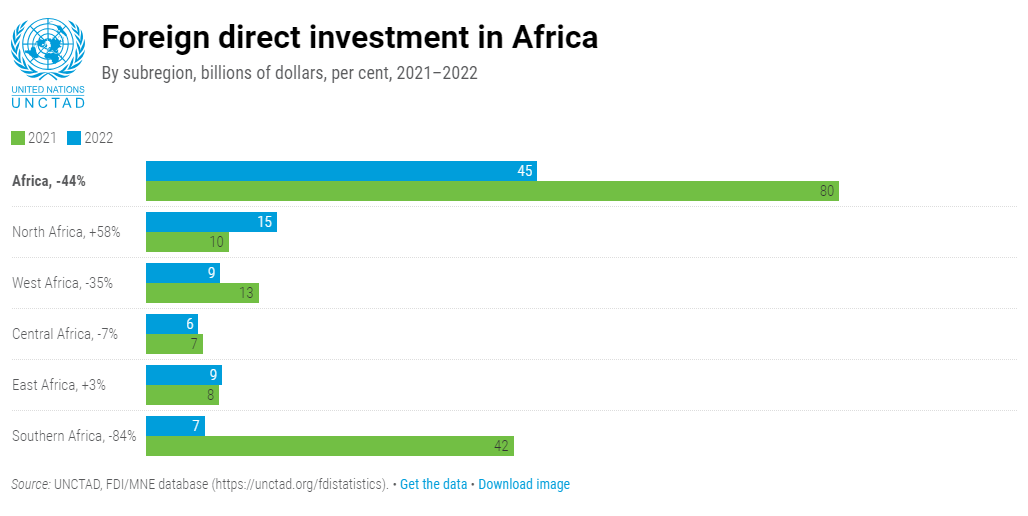

Le Rapport sur l’Investissement Mondial de la CNUCED pour l’année 2023 révèle que les investissements étrangers en provenance de l’étranger vers l’Afrique sont passés à 45 milliards de dollars en 2022, contre un record de 80 milliards de dollars en 2021. Cela représentait 3,5 % de l’investissement mondial total.

En Afrique du Nord, l’Égypte a vu un gros bond des investissements étrangers à 11 milliards de dollars en raison de plus d’entreprises achetant et fusionnant. Le nombre de nouveaux projets annoncés a plus que doublé pour atteindre 161. Les accords pour des projets internationaux ont également augmenté des deux tiers pour atteindre 24 milliards de dollars. Cependant, l’investissement au Maroc a légèrement baissé de 6 % pour atteindre 2,1 milliards de dollars.

En Afrique de l’Ouest, le Nigeria a enregistré un investissement étranger négatif de -187 millions de dollars car certains investisseurs se sont retirés. Mais le nombre de nouveaux projets a augmenté de 24 % pour atteindre 2 milliards de dollars. L’investissement au Sénégal est resté le même à 2,6 milliards de dollars, tandis que le Ghana a vu une diminution de 39 % pour atteindre 1,5 milliard de dollars.

En Afrique de l’Est, l’investissement en Éthiopie a chuté de 14 % pour atteindre 3,7 milliards de dollars, mais il a quand même reçu le deuxième investissement étranger le plus important sur le continent. L’investissement en Ouganda a augmenté de 39 % pour atteindre 1,5 milliard de dollars en raison d’investissements dans l’extraction de ressources. La Tanzanie a enregistré une augmentation de 8 % pour atteindre 1,1 milliard de dollars.

En Afrique Centrale, l’investissement en République Démocratique du Congo est resté le même à 1,8 milliard de dollars, principalement grâce aux investissements dans les champs pétrolifères et l’exploitation minière.

En Afrique Australe, l’investissement étranger en Afrique du Sud s’est élevé à 9 milliards de dollars, moins qu’en 2021 mais le double de la moyenne des dix dernières années. En Zambie, après deux années de pertes, l’investissement étranger a augmenté pour atteindre 116 millions de dollars.

Vous recherchez une chance de faire la différence tout en obtenant des retours. Rendez-vous sur notre application pour commencer à investir dans la croissance de l’Afrique dès aujourd’hui !

Au cours des cinq dernières années, l’investissement étranger a augmenté dans quatre des groupes économiques en Afrique.

L’investissement dans le Marché Commun de l’Afrique Orientale et Australe a augmenté de 14 % pour atteindre 22 milliards de dollars. Il a également augmenté dans la Communauté de Développement de l’Afrique Australe (multiplié par quatre pour atteindre 10 milliards de dollars), l’Union Économique et Monétaire Ouest Africaine (doublant pour atteindre 5,2 milliards de dollars), et la Communauté d’Afrique de l’Est (en hausse de 9 % pour atteindre 3,8 milliards de dollars).

De manière générale, les destinations de l’IDE en Afrique ont évolué au cours de la dernière décennie, avec l’Afrique du Nord et l’Afrique Australe – qui représentaient la majorité de l’IDE à mi-2000 – perdant des parts d’IDE au profit de l’Afrique de l’Est.

Sources des Flux d’IDE vers l’Afrique

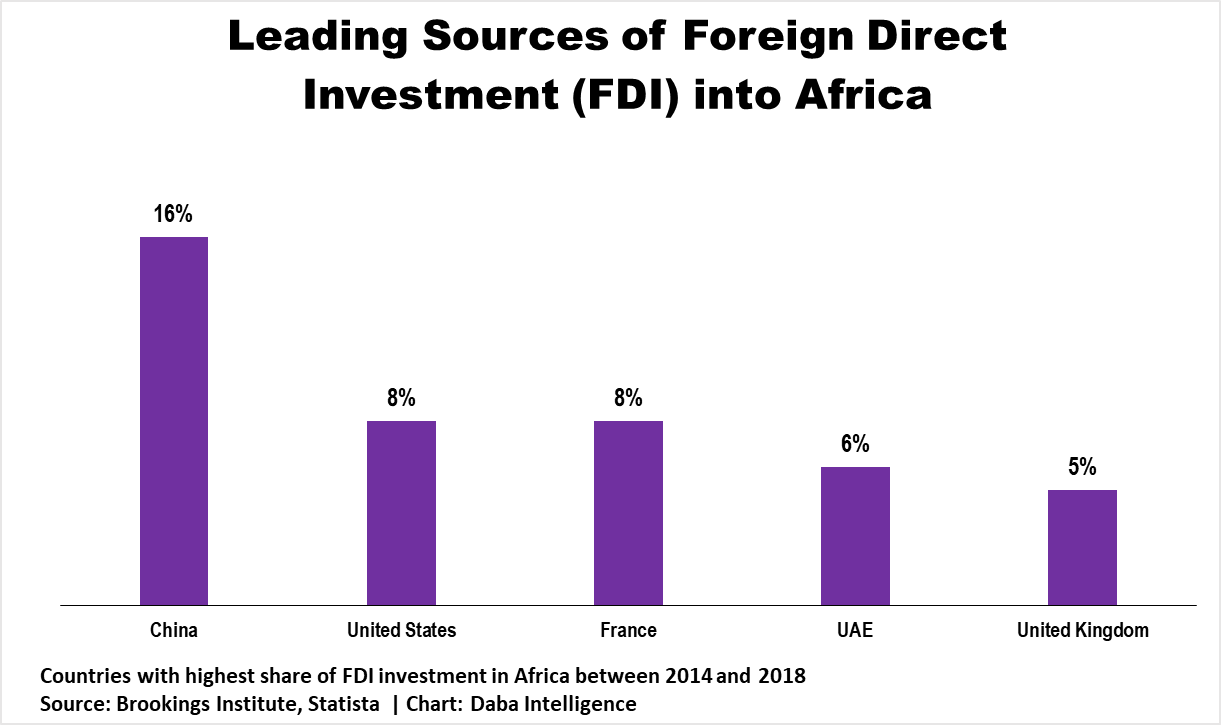

Les investisseurs européens restent la source la plus importante de stock d’IDE en Afrique, avec en tête le Royaume-Uni (60 milliards de dollars), la France (54 milliards de dollars), et les Pays-Bas (54 milliards de dollars) au cours des cinq dernières années.

Mais la part relative du stock d’IDE de l’Afrique provenant de l’Europe a diminué au cours de la dernière décennie, tandis que la part de l’Asie a augmenté – la Chine étant actuellement en tête.

Nous explorons les principales sources des flux d’IDE vers l’Afrique, sur la base des données de la recherche de l’Institut Brookings de l’année 2014 à 2018.

Chine

La Chine est le plus grand investisseur mondial en Afrique en termes de capital total. Elle a investi plus de 72 milliards de dollars sur le continent de 2014 à 2018. Cet investissement a créé plus de 137 000 emplois à travers 259 projets.

France

La France a investi 34 milliards de dollars en Afrique sur la même période, créant 58 000 emplois dans 329 projets. Les investissements de la France sont cruciaux pour ses anciennes colonies en Afrique, telles que le Nigeria, le Maroc, l’Algérie et la Côte d’Ivoire.

États-Unis

L’investissement direct américain en Afrique s’est élevé à près de 31 milliards de dollars de 2014 à 2018. Les États-Unis étaient responsables de 463 projets sur le continent, soit le plus grand nombre par rapport à tout autre pays. Ces projets ont créé 62 000 emplois. Les entreprises américaines continuent de rechercher des opportunités d’investissement en Afrique.

Vous voulez franchir la prochaine étape pour exploiter le potentiel d’investissement de l’Afrique ? Rendez-vous sur notre site Web ou téléchargez dès maintenant l’application Daba pour commencer votre voyage.

Émirats Arabes Unis

Les Émirats Arabes Unis (EAU) ont versé plus de 25 milliards de dollars en Afrique au cours de quatre années. Cela est logique étant donné la proximité des Émirats Arabes Unis avec l’Afrique de l’Est, car ils se trouvent à l’extrémité orientale de la péninsule arabique.

Les investissements en capital des Émirats Arabes Unis en Afrique devraient augmenter fortement dans les années à venir : Le gouvernement en 2020 a annoncé une initiative de 500 millions de dollars pour aider la jeunesse africaine et numériser les ressources.

Fin 2019, les Émirats Arabes Unis ont déclaré finaliser un accord de libre-échange avec un consortium de pays africains, et le mois dernier, ils ont signé un accord de 35 milliards de dollars avec l’Égypte pour développer un tronçon stratégique de la côte méditerranéenne du pays nord-africain.

Royaume-Uni

Le Royaume-Uni a investi près de 18 milliards de dollars en Afrique de 2014 à 2018, couvrant 286 projets et créant 41 000 emplois. Le Royaume-Uni, comme la France, entretient toujours des liens forts avec ses anciennes colonies en Afrique, telles que Sierra Leone, le Kenya, le Zimbabwe, l’Ouganda, la Zambie, la Tanzanie et l’Égypte.

Entre 2014 et 2018, l’investissement direct chinois sur le continent africain représentait la principale source d’IDE.

Pourquoi Plus de Pays Investissent en Afrique

L’Afrique représente un marché significatif et inexploité pour l’investissement étranger. Ses 54 pays abritent 1,3 milliard de personnes, dont beaucoup sont jeunes et auront besoin de bons emplois dans les années à venir, ainsi qu’une abondance de ressources naturelles, du pétrole à l’or en passant par les diamants et le lithium.

De plus, la Zone de Libre-Échange Continentale Africaine (ZLECAF), qui relie 1,3 milliard de personnes de 55 pays, offre une grande chance pour l’économie africaine de croître et entraînera très probablement plus d’investissements étrangers en Afrique en réduisant les règles et en facilitant l’accès aux nouveaux marchés.

Comment les investisseurs peuvent-ils se positionner au mieux pour saisir les opportunités découlant de ces développements rapides dans le paysage d’investissement en Afrique ?

Contactez-nous chez Daba pour vous guider dans le voyage de l’investissement en Afrique, que vous soyez un investisseur individuel ou institutionnel. Téléchargez notre application, remplissez ce formulaire sur notre site Web ou discutez avec notre équipe sur WhatsApp pour commencer.

The relative share of Africa’s FDI stock originating from Europe declined in the last decade, while Asia’s share increased—with China currently leading the pack.

Foreign direct investment (FDI) is when a person or business from one country invests in and gains significant control over a company in another country, typically by owning 10% or more of its voting power.

FDI is crucial for connecting economies globally, as it establishes lasting ties between them. It’s a vital way for technology to move between countries, boosts international trade by providing access to new markets, and plays a big role in driving economic growth.

As such, we discuss the top countries that account for the largest share of FDI flows into African markets. But first, why is FDI important to Africa, and what are the latest foreign direct investment trends on the continent?

Why Is Foreign Investment Important To Africa?

For Africa, FDI is crucial for several reasons. Firstly, it brings in much-needed capital for infrastructure development, job creation, and technology transfer, which are essential for economic growth.

FDI also facilitates the diversification of economies by introducing new industries and enhancing existing ones. Moreover, it promotes trade and strengthens global economic integration by connecting African markets with international networks.

In addition, FDI often comes with expertise, managerial skills, and access to global markets, which can help local businesses expand and become more competitive.

Furthermore, it fosters innovation and productivity enhancements through knowledge spillovers and technology diffusion. Lastly, FDI contributes to the stability of African economies by providing a stable source of external financing and reducing reliance on volatile sources like foreign aid or commodity exports.

Don’t miss out on exclusive investment opportunities in Africa! Download the Daba app today and unlock a world of potential returns while making a positive impact.

Latest Trends in FDI Flows to Africa

UNCTAD’s World Investment Report 2023 reveals that money invested from abroad into Africa dropped to $45 billion in 2022 from a record high of $80 billion in 2021. This made up 3.5% of the total global investment.

In North Africa, Egypt saw a big jump in foreign investment to $11 billion due to more companies buying and merging. The number of new projects announced more than doubled to 161. Deals for international projects also went up by two-thirds to $24 billion. However, investment in Morocco went down a bit by 6% to $2.1 billion.

In West Africa, Nigeria experienced negative foreign investment of -$187 million because some investors pulled out. But new projects increased by 24% to $2 billion. Investment in Senegal stayed the same at $2.6 billion, while Ghana saw a decrease of 39% to $1.5 billion.

In East Africa, investment in Ethiopia dropped by 14% to $3.7 billion, but it still received the second most foreign investment on the continent. Uganda’s investment went up by 39% to $1.5 billion due to investments in extracting resources. Tanzania saw an increase of 8% to $1.1 billion.

In Central Africa, investment in the Democratic Republic of the Congo stayed the same at $1.8 billion, mainly from investments in oil fields and mining.

In Southern Africa, foreign investment in South Africa was $9 billion, less than in 2021 but double the average of the last ten years. In Zambia, after two years of losses, foreign investment increased to $116 million.

Looking for a chance to make a difference while earning returns. Head over to our app to start investing in Africa’s growth today!

Over the past five years, foreign investment has increased in four of the economic groups in Africa.

Investment in the Common Market for Eastern and Southern Africa went up by 14% to $22 billion. It also increased in the Southern African Development Community (rising four times to $10 billion), the West African Economic and Monetary Union (doubling to $5.2 billion), and the East African Community (up by 9% to $3.8 billion).

Generally, the destinations of FDI in Africa have shifted over the last decade, with Northern and Southern Africa—which made up the majority of FDI stock in the mid-2000s—losing FDI share to Eastern Africa.

Sources of FDI Flows to Africa

European investors remain the most important source of FDI stock in Africa, led by the United Kingdom ($60 billion), France ($54 billion), and the Netherlands ($54 billion) over the past five years.

But the relative share of Africa’s FDI stock originating from Europe declined in the last decade, while Asia’s share increased—with China currently leading the pack.

We explore the leading sources of FDI flows to Africa, based on data from the Brookings Institute research from the year 2014 to 2018.

China

China is the world’s largest investor in Africa in terms of total capital. They invested more than $72 billion in the continent from 2014 to 2018. That investment created more than 137,000 jobs across 259 projects.

France

France invested $34 billion in Africa over the same period, creating 58,000 jobs in 329 projects. France’s investments are crucial to its former colonies in Africa, such as Nigeria, Morocco, Algeria, and the Ivory Coast.

The United States

American direct investment in Africa was nearly $31 billion from 2014 to 2018. The United States was responsible for a total of 463 projects on the continent, the most of any other country. These projects created 62,000 jobs. American companies continue to seek investment opportunities in Africa.

Want to take the next step in tapping Africa’s investment potential? Head over to our website or download the Daba app now to start your journey.

United Arab Emirates

The United Arab Emirates (UAE) poured more than $25 billion into Africa over four years. This makes sense given the UAE’s proximity to eastern Africa as it sits on the eastern edge of the Arabian peninsula.

The UAE’s capital investments in Africa are expected to rise sharply in the coming years: The government 2020 announced a $500 million initiative to help Africa’s youth and digitize resources.

In late 2019, the UAE said it was finalizing a free trade agreement with a consortium of African countries, and last month, it signed a $35 billion deal with Egypt to develop a prime stretch of the North African country’s Mediterranean coast.

United Kingdom

The United Kingdom invested nearly $18 billion in Africa from 2014 to 2018, covering 286 projects and creating 41,000 jobs. Britain, like France, still has strong ties to its former colonies in Africa, such as Sierra Leone, Kenya, Zimbabwe, Uganda, Zambia, Tanzania, and Egypt.

Between 2014 and 2018, Chinese direct investment in the African continent represented the main source of FDI.

Why More Countries Are Investing in Africa

Africa represents a significant untapped market for foreign investment. Its 54 countries are home to 1.3 billion people, many of whom are young and will need good jobs in the coming years, and an abundance of natural resources from oil and gold to diamonds and lithium.

In addition, the African Continental Free Trade Area (AfCFTA), which links 1.3 billion people from 55 countries, offers a big chance for Africa’s economy to grow and is poised to draw more foreign investment into its markets by cutting down rules and making it easier to reach new markets.

How can investors best position themselves to capture opportunities arising from these rapid developments in Africa’s investment landscape?

Reach out to us at Daba to guide you on the journey of investing in Africa, whether you’re an individual or institutional investor. Download our app, fill out this form on our website, or chat with our team on WhatsApp to get started.

Bien que les entreprises publiques dirigées par des femmes restent rares en Afrique, celles ayant une femme à leur tête surclassent financièrement leurs homologues par une marge considérable.

À travers le continent africain, seulement 5% des entreprises cotées sur les 29 bourses ont une femme comme PDG, comme révélé par une étude de 2 020 entreprises et les données de Bloomberg, présentées dans la Liste Définitive des PDG Féminines d’Africa.com et du Groupe Standard Bank.

L’analyse, qui a couvert 93 femmes dans 17 pays, a révélé que bien que les entreprises dirigées par des femmes restent rares en Afrique, celles dirigées par une femme surpassent financièrement de manière substantielle.

Cette tendance à la surperformance des grandes entreprises cotées dirigées par des femmes en Afrique reflète un schéma mondial. Les recherches de McKinsey de 2020 ont montré que les entreprises du quartile supérieur pour la diversité des genres au sein des équipes de direction étaient 25 % plus susceptibles d’avoir une rentabilité supérieure à la moyenne que celles du quartile inférieur.

Pour célébrer les performances exceptionnelles des entreprises dirigées par des femmes en Afrique et au-delà, nous répertorions les femmes qui ont accédé à des postes de leadership de premier plan à travers le continent selon le classement de la Liste Définitive, explorant leurs parcours vers le succès et leurs réalisations remarquables.

Une dirigeante minière chevronnée, Nompumelelo Zikalala (Mpumi), occupe le poste de PDG de Kumba Iron Ore, une filiale d’Anglo American, depuis janvier 2022. Avec plus de deux décennies d’expérience, elle a joué un rôle crucial dans la promotion de la diversité et de la durabilité dans l’industrie. Sous sa direction, Kumba, le plus grand producteur de minerai de fer d’Afrique, a livré des résultats financiers résilients en 2022 tout en se concentrant sur la sécurité et la durabilité.

La carrière de 20 ans de Mpumi chez De Beers l’a vue occuper des postes opérationnels et commerciaux de haut niveau, devenant la première femme GM en 2007. Elle était GM à la mine de Voorspoed, Directrice Générale Adjointe des Mines Consolidées de De Beers et Directrice Générale des Opérations Gérées par le Groupe De Beers supervisant les opérations sud-africaines et canadiennes. Classée parmi les 100 Femmes Inspirantes Mondiales dans l’Industrie Minière en 2018, Mpumi est passionnée par l’implication des femmes et des jeunes dans l’industrie.

Diplômée en génie chimique de l’Université du Witwatersrand, elle a commencé sa carrière en tant que boursière chez Anglo-American. L’expérience diversifiée de Mpumi et son engagement envers la transformation font d’elle une force pionnière dans le secteur minier.

Nompumelelo Zikalala (Mpumi) a fait l’histoire en 2020 lorsqu’elle est devenue la seule PDG noire parmi les 450 premières entreprises cotées à la Bourse de Johannesburg, juste avant son 40e anniversaire, en prenant les rênes du Bidvest Group. Malgré sa prise de fonction en pleine pandémie, Mpumi a dirigé avec succès le conglomérat industriel, avec des intérêts dans le fret, les biens de consommation et commerciaux, vers des bénéfices à deux chiffres – enregistrant une augmentation de 15 % pour atteindre 9,7 milliards de rands. Sous sa direction, Bidvest a également élargi son segment des énergies renouvelables et alternatives.

Avec quatre ans d’expérience chez Bidvest, occupant des postes tels que Directrice des Ventes et du Marketing de Groupe et Directrice Exécutive, Mpumi a gravi les échelons en tant que PDG en attente avant sa transition historique vers le poste de PDG. Ses “compétences de leadership exceptionnelles et sa profondeur d’expérience” ont été saluées par l’ancien PDG.

Avocate passionnée du mentorat et du leadership féminin, Mpumi s’est concentrée sur la création d’un environnement propice à la réussite des femmes et à leur avancement. Sa carrière pionnière, qui s’étend sur plus de deux décennies dans les secteurs minier et industriel, en fait une force pionnière pour la diversité et la transformation dans les affaires sud-africaines.

Bertina Engelbrecht a fait l’histoire au début de l’année 2022 lorsqu’elle est devenue la première femme noire à diriger un groupe de distribution coté en Afrique du Sud en tant que PDG de Clicks Group. Sous sa direction, Clicks a réalisé une croissance impressionnante du chiffre d’affaires et des bénéfices, a étendu son réseau de distribution au détail et a acquis sa première pharmacie ouverte 24 heures sur 24, avec des plans d’expansion agressifs pour 2023.

La nomination d’Engelbrecht a clôturé 15 années au sein de l’équipe de direction, où elle a joué un rôle crucial dans la croissance stratégique de Clicks en un leader de la santé et du bien-être. En tant que Directrice des Ressources Humaines de Groupe depuis 2006, elle a milité pour l’intégration de l’agenda des personnes dans les opérations et a lancé un régime de partage des bénéfices des employés très réussi.

Avant Clicks, Engelbrecht a occupé des postes de direction chez Shell SA Energy, Shell Oil Products Africa et Sea Harvest. Avocate admise avec un Master en Droit de l’Université du Cap, son parcours juridique et son expérience intersectorielle en RH et en efficacité organisationnelle l’ont préparée au rôle de PDG.

Engelbrecht dirige désormais la trajectoire de Clicks, tirant parti de sa combinaison unique d’expertise juridique, de sens des affaires et de passion pour le développement des personnes en tant que première femme noire à la tête du géant de la distribution.

Nombasa Tsengwa est largement considérée comme l’une des dirigeantes les plus travailleuses de l’industrie minière, ayant remporté de nombreux prix au cours de ses deux décennies d’expérience en gestion et au sein de conseils d’administration des secteurs public et privé. Parmi ceux-ci, le prix de la Femme d’Affaires de l’Année de la Standard Bank en 2017 et le titre de Femme la Plus Influente d’Afrique dans les Affaires et le Gouvernement dans l’Industrie Minière aux Pan African Awards de 2018.

Elle a passé 20 ans chez Exxaro Resources, l’une des principales entreprises minières et d’énergies renouvelables d’Afrique du Sud, occupant des postes de plus en plus importants comme la direction des opérations charbonnières et la direction du secteur minéral. Nombasa a joué un rôle clé dans la formulation de la stratégie bas-carbone d’Exxaro.

Dans le cadre d’un plan de succession minutieux, Nombasa a été nommée PDG désignée d’Exxaro, cotée à la Bourse de Johannesburg, dirigée et dirigée par des Noirs, en 2021, devenant PDG 18 mois plus tard. Depuis son arrivée à la tête de l’entreprise, elle a renforcé l’équipe de direction, élargi la présence géographique de l’entreprise et renforcé les capacités de gestion de projet, de contrôle des coûts et d’allocation des capitaux.

L’ascension de Nombasa dans la hiérarchie d’Exxaro, sa capacité à conduire des initiatives stratégiques comme la transition bas-carbone et sa reconnaissance en tant que l’une des dirigeantes minières les plus influentes d’Afrique soulignent qu’elle est une force pionnière dans l’industrie. Son leadership sera crucial alors qu’Exxaro poursuit sa transformation.

Depuis plus d’une décennie en tant que PDG de Royal Bafokeng Holdings, Albertinah Kekana a exécuté avec adresse la stratégie de diversification du portefeuille de la société d’investissement communautaire. Sa carrière de 20 ans couvre des postes exécutifs et non exécutifs dans les secteurs minier, des services financiers, du pétrole et du gaz, des télécommunications, de l’infrastructure numérique et de l’énergie.

L’expertise financière de Kekana est étendue, notamment des passages en banque d’investissement chez Rothschild et UBS, où elle était directrice des finances d’entreprise. Elle a passé huit ans en tant que directrice des opérations chez Public Investment Corporation, stimulant la performance de l’entreprise. Ses débuts de carrière comprenaient trois ans en tant que gestionnaire adjointe en finance d’entreprise chez PwC.

Comptable agréée de formation, Kekana détient un diplôme en commerce de l’Université du Cap et a suivi une formation en gestion avancée à Harvard. Son expérience de leadership intersectorielle, son flair pour l’investissement et son exécution stratégique en font une autorité dans le paysage de la gestion d’actifs et des investissements en Afrique du Sud. Sous sa direction, Royal Bafokeng s’est diversifié en une force d’investissement sectorielle redoutable.

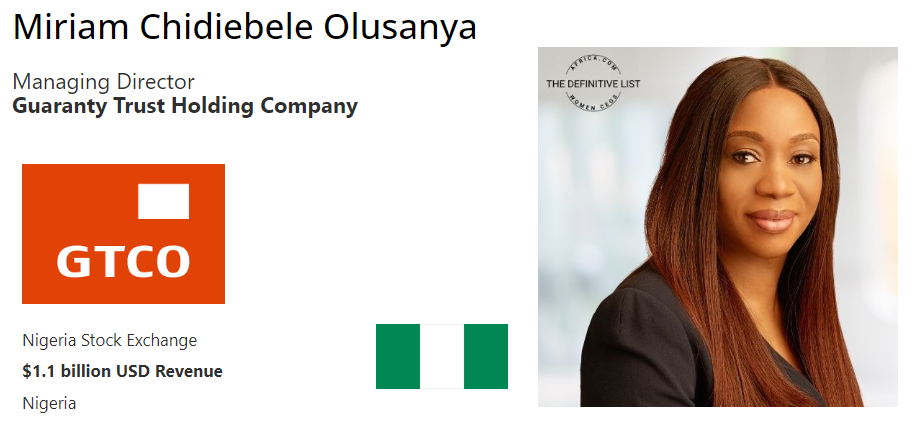

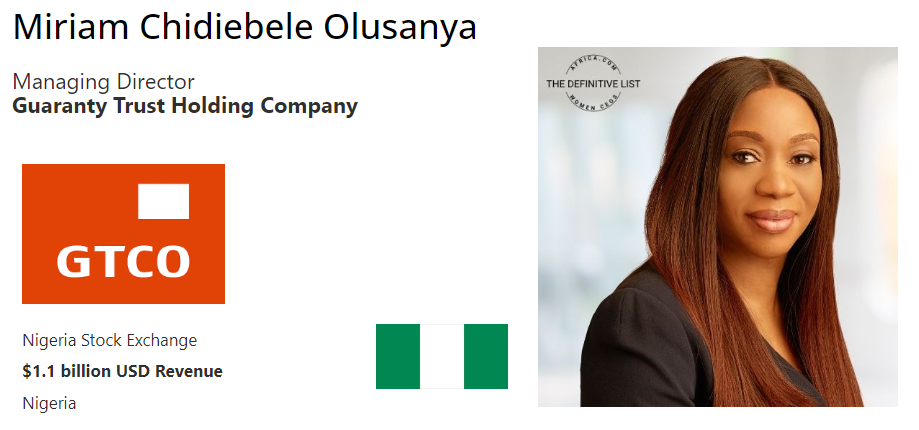

Miriam Chidiebele Olusanya, la Directrice Générale de la Guaranty Trust Bank, est une leader visionnaire dans le domaine financier, renommée pour son engagement envers l’excellence. Issu de modestes origines au Nigeria, son parcours a été marqué par une brillance académique et une affinité naturelle pour les chiffres. Grimpant les échelons avec ténacité et intelligence stratégique, elle dirige désormais l’institution avec confiance.

Sous la direction de Miriam, la Guaranty Trust Holding Company a connu une croissance remarquable, consolidant sa position dans le monde financier. Son regard perspicace sur les tendances du marché assure la résilience de l’entreprise dans des paysages économiques dynamiques. Au-delà de ses réalisations professionnelles, Miriam se consacre à l’encouragement de la prochaine génération de leaders à travers des initiatives de mentorat.

Connu pour sa chaleur et son humilité, Miriam inspire ses collègues à aspirer à la grandeur. Son histoire, d’un érudit de petite ville à une pionnière dans le domaine financier, est un témoignage de détermination et de résilience. Avec Miriam à sa tête, la Guaranty Trust Holding Company est prête pour un succès et une prospérité continus.

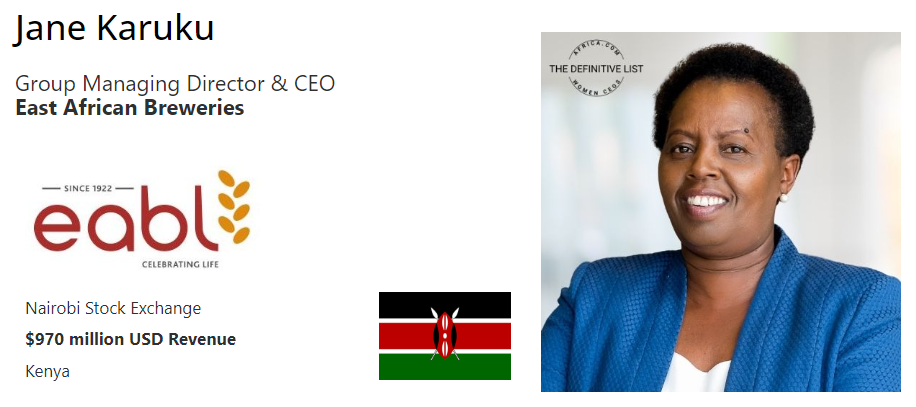

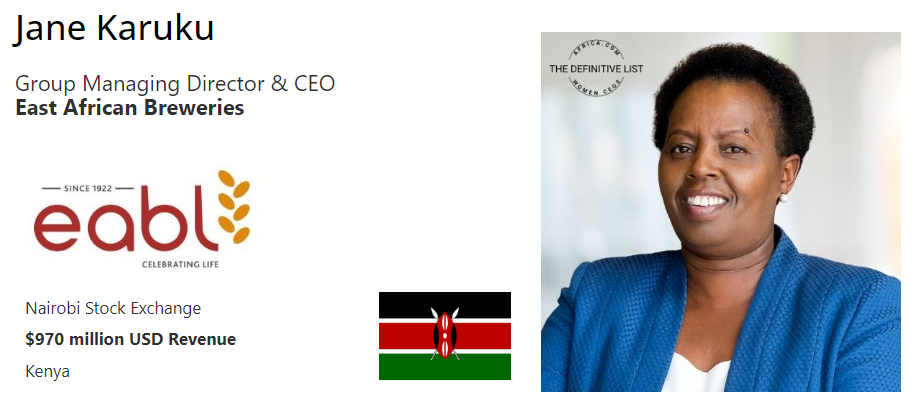

PDG et Directrice Générale du Groupe, East African Breweries PLC (EABL)

Chiffre d’affaires : 970 millions de dollars

Pays : Kenya

En tant que Directrice Générale et PDG de EABL depuis 2021, Jane Karuku a marqué l’histoire en devenant la première femme à diriger cette entreprise centenaire. Elle est l’une des dirigeantes d’entreprise les plus importantes d’Afrique de l’Est, dirigeant la plus grande et la plus rentable entreprise de fabrication de la région avec plus de 40 marques mondiales comme Johnnie Walker et Guinness.

Sous la direction de Karuku, EABL a connu un renversement financier et opérationnel remarquable. En 2021, elle a supervisé une augmentation de 15% des ventes nettes d’une année sur l’autre, atteignant 86 milliards de shillings, dépassant ainsi les niveaux d’avant la pandémie de 2019. Son leadership a également permis à EABL de publier son premier rapport de durabilité avec des initiatives comme un fonds de récupération de 5 millions de dollars pour les pubs/bars et une ambition d’approvisionnement local jusqu’à 80% des matières premières.

La carrière de 25 ans de Karuku comprend des entreprises de biens de grande consommation et des ONG, accumulant une expertise en stratégie, opérations, marketing et changement organisationnel. Elle a occupé des postes de direction chez Farmers Choice Kenya, Kenya Cooperative Creameries, Alliance for a Green Revolution in Africa, Telkom Kenya où elle a dirigé une transformation, et Cadbury avec un mandat multi-pays.

Son expérience solide en gestion et sa contribution au développement socio-économique du Kenya lui ont valu de nombreux prix, dont un prix présidentiel. Karuku est titulaire d’un MBA en Marketing de l’Université de Californie.

8. Ntombi Felicia Msiza

PDG, Raubex Group Ltd

Chiffre d’affaires : 781 millions de dollars

Pays : Afrique du Sud

La dirigeante chevronnée Ntombi Felicia Msiza a assumé le rôle de PDG du géant de la construction Raubex Group à la mi-2022, après cinq ans en tant que Directrice Exécutive responsable de la Gouvernance, du Risque et de la Conformité.

L’expertise étendue de Ntombi en matière d’éthique, de stratégie, de gestion des risques, de gouvernance d’entreprise, d’affaires juridiques et de conformité s’est avérée inestimable. Son orientation a permis à Raubex de renforcer ses structures et ses processus pour soutenir la croissance significative de l’entreprise au cours des six dernières années.

Avant de rejoindre Raubex, Ntombi a eu une longue carrière dans des postes d’audit et de gestion des risques. Elle a été Directrice du Risque et de l’Assurance à City Power SOC, Chef de l’Audit Interne à IDT, et Chef de l’Audit Exécutif de Groupe à Denel SOC.

Directrice de la Gouvernance, Ntombi est titulaire d’un diplôme en commerce et d’un MBA. Son expérience interfonctionnelle dans les domaines de la gouvernance, du risque, de la conformité, de l’audit et de la stratégie la positionne bien pour diriger l’expansion continue de Raubex dans le secteur de la construction.

La nomination de Ntombi en tant que PDG capitalise sur sa compréhension approfondie des opérations de Raubex de par son rôle exécutif précédent, combinée à son bilan éprouvé en matière de gouvernance et de gestion des risques pour des organisations majeures.

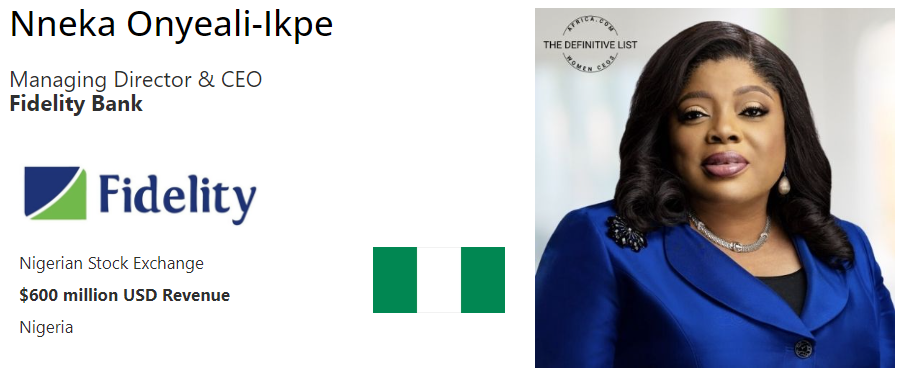

Depuis sa nomination en tant que PDG de la Fidelity Bank en 2021, Nneka Onyeali-Ikpe a remporté de nombreux prix, dont celui de Banquier de l’Année et a conduit Fidelity à remporter des prix comme la Meilleure Banque pour les PME Nigeria 2022. Leader transformationnelle, Nneka a dirigé le redressement de Fidelity sur six ans en tant que Directrice Exécutive, stimulant la rentabilité de la direction de Lagos et du Sud-Ouest et contribuant à hauteur de 28% aux bénéfices de la banque, aux dépôts et aux prêts.

Sa carrière bancaire de trois décennies a affiné son expertise stratégique, notamment des rôles dans le redressement réussi de l’Enterprise Bank. Nneka a une expérience de gestion interfonctionnelle couvrant le juridique, l’investissement, la vente au détail, les affaires commerciales et bancaires chez des institutions majeures comme Standard Chartered et Zenith Bank.

Autorité en matière de structuration de transactions dans les secteurs du pétrole et du gaz, de la fabrication, de l’aviation et de l’immobilier, Nneka est titulaire d’une licence en droit et d’une maîtrise de l’Université du Nigeria et de King’s College. Elle a suivi une formation exécutive approfondie à Harvard, INSEAD et à l’école de commerce Wharton.

L’acuité juridique de Nneka, son expérience de leadership interfonctionnel conduisant des initiatives de transformation et ses compétences éprouvées en redressement la préparent bien à diriger la croissance continue de la Fidelity Bank.

Le parcours de près de deux décennies de Zanele Matlala chez Merafe Resources a culminé avec sa nomination en tant que PDG il y a une décennie. Ayant rejoint la société minière cotée en bourse JSE en tant que directrice non exécutive indépendante en 2005 avant de devenir directrice financière en 2010, la compréhension approfondie de l’entreprise par Matlala s’est avérée inestimable.

Sous sa direction, Merafe a annoncé son deuxième plus gros bénéfice net en 2017 et a navigué avec habileté dans le rebond de la pandémie, restaurant la rentabilité. L’entreprise est maintenant l’une des meilleures “actions à dividendes” de la JSE, avec un rendement de 25 %, reflétant la direction prudente mais réussie de Matlala.

Expert-comptable de profession, l’expertise de Matlala en finance d’entreprise couvre des postes comme Directrice Financière chez Kagiso Trust Investments et Directrice Financière chez la Banque de Développement d’Afrique Australe. L’année dernière, son leadership et ses contributions ont été reconnus par le prestigieux Prix des Anciens Exceptionnels lors des Chancellor’s Calabash Awards.

L’acuité financière de Matlala, sa connaissance institutionnelle de Merafe à partir de postes d’administrateur et d’exécutif, et sa capacité avérée à diriger l’entreprise minière à travers les cycles de l’industrie la positionnent de manière unique pour conduire son succès continu.

Les réalisations remarquables de ces principales PDG féminines dirigeant les plus grandes entreprises publiques d’Afrique soulignent les contributions inestimables des femmes à la réussite financière et à la promotion de la diversité et de l’inclusion dans les affaires sur le continent.

À ceux qui souhaitent soutenir et investir dans des entreprises dirigées par des femmes, nous vous invitons à vous joindre à nous pour briser les barrières et promouvoir la diversité dans le leadership d’entreprise à travers les marchés africains.

Que vous soyez un investisseur individuel ou institutionnel, téléchargez dès maintenant l’application Daba ou remplissez un formulaire sur notre site web pour découvrir des opportunités d’investissement dans des entreprises visionnaires dirigées par des femmes exceptionnelles.

While women-led public companies remain scarce in Africa, those with a woman at the helm outperform financially by a substantial margin.

Across the African continent, only 5% of companies listed on the 29 stock exchanges have a woman as CEO, as revealed by a study of 2,020 companies and Bloomberg data, presented in the Definitive List of Women CEOs from Africa.com and Standard Bank Group.

The analysis, which covered 93 women across 17 countries, revealed that while women-led companies remain scarce in Africa, those with a woman at the helm outperform financially by a substantial margin.

This trend of outperformance by large-listed, women-led firms in Africa mirrors a global pattern. McKinsey research from 2020 showed that companies in the top quartile for gender diversity on executive teams were 25% more likely to have above-average profitability than those in the bottom quartile.

To celebrate the exceptional performance of female-led companies in Africa, we list the women who have ascended to top leadership roles across the continent as ranked by the Definitive List, exploring their journeys to success and their remarkable achievements.

A seasoned mining executive, Nompumelelo Zikalala (Mpumi), has served as CEO of Kumba Iron Ore, a subsidiary of Anglo American, since January 2022. With over two decades of experience, she has been instrumental in driving diversity and sustainability in the industry. Under her leadership, Kumba, Africa’s largest iron ore producer, delivered resilient financials in 2022 while focusing on safety and sustainability.

Mpumi’s 20-year career at De Beers saw her hold senior operational and commercial roles, becoming the first female GM in 2007. She was GM at Voorspoed Mine, Deputy CEO of De Beers Consolidated Mines, and MD of De Beers Group Managed Operations overseeing South African and Canadian operations. Listed among the Top 100 Global Inspirational Women in Mining in 2018, Mpumi is passionate about involving women and youth in the industry.

A chemical engineering graduate from the University of the Witwatersrand, she began her career as an Anglo-American bursar. Mpumi’s diverse experience and commitment to transformation make her a pioneering force in the mining sector.

Nompumelelo Zikalala (Mpumi) made history in 2020 when just shy of her 40th birthday, she became the only black female CEO among the top 450 companies listed on the Johannesburg Stock Exchange after taking the helm at Bidvest Group.

Despite assuming leadership amid the pandemic, Mpumi has successfully steered the industrial conglomerate, with interests in freight, consumer, and commercial products, to double-digit profits – posting a 15% increase to R9.7bn. Under her tenure, Bidvest has also expanded its renewables and alternative energy segment.

With four years of experience at Bidvest, including roles like Group Sales and Marketing Director and Executive Director, Mpumi worked her way up the ranks as the CEO-in-waiting before her historic transition to the top job. Her “exceptional leadership skills and depth of experience” were praised by the former CEO.

A passionate advocate for mentorship and female leadership, Mpumi has focused on creating an enabling environment for women to succeed and rise through the ranks. Her trailblazing career, spanning over two decades in mining and industrial sectors, has made her a pioneering force for diversity and transformation in South African business.

Bertina Engelbrecht made history in early 2022 when she became the first Black woman to lead a listed retail group in South Africa as CEO of Clicks Group. Under her leadership, Clicks has achieved impressive turnover and profit growth, expanded its retail network, and acquired its inaugural 24-hour pharmacy, with aggressive expansion plans for 2023.

Engelbrecht’s appointment capped off 15 years on the executive team, where she was instrumental in Clicks’ strategic growth into a health and wellness leader. As Group HR Director from 2006, she championed integrating the people agenda into operations and launched a highly successful employee share scheme.

Before Clicks, Engelbrecht held leadership roles at Shell SA Energy, Shell Oil Products Africa, and Sea Harvest. An admitted attorney with a Master’s in Law from the University of Cape Town, her legal background and cross-industry experience in HR and organizational effectiveness primed her for the CEO role.

Engelbrecht now spearheads Clicks’ trajectory, leveraging her unique combination of legal expertise, business acumen, and passion for people development as the retail giant’s pioneering first Black female chief executive.

Nombasa Tsengwa is widely regarded as one of the hardest-working leaders in the mining industry, having secured numerous accolades over her two decades of executive management and board experience across public and private sectors. These include the Standard Bank Business Woman of the Year award in 2017 and being named Africa’s Most Influential Woman in Business and Government in the Mining Industry at the 2018 Pan African Awards.

She has spent 20 years at Exxaro Resources, one of South Africa’s leading mining and renewable energy companies, holding increasingly senior roles like heading up coal operations and leading the minerals business. Nombasa played a key role in formulating Exxaro’s low-carbon strategy.

As part of a careful succession plan, Nombasa was appointed CEO Designate of the JSE-listed, black-empowered, and black-led Exxaro in 2021, becoming CEO 18 months later. Since taking the helm, she has strengthened the executive team, expanded the company’s geographical footprint, and bolstered project management, cost control, and capital allocation capabilities.

Nombasa’s rise through the ranks at Exxaro, ability to drive strategic initiatives like the low-carbon transition, and recognition as one of Africa’s most influential mining leaders underscore her as a trailblazing force in the industry. Her leadership will be critical as Exxaro continues its transformation.

For over a decade as Chief Executive of Royal Bafokeng Holdings, Albertinah Kekana has adeptly executed the community investment company’s portfolio diversification strategy. Her 20-year career spans executive and non-executive roles across mining, financial services, oil and gas, telecommunications, digital infrastructure, and energy.

Kekana’s financial expertise is extensive, including investment banking stints at Rothschild and UBS, where she was a corporate finance director. She spent eight years as COO at the Public Investment Corporation, driving corporate performance. Her early career included three years as an assistant corporate finance manager at PwC.

A chartered accountant by training, Kekana holds a commerce degree from the University of Cape Town and has advanced management training from Harvard. Her cross-industry leadership experience, investment acumen, and strategic execution make her an authority in South Africa’s asset management and investment landscape. Under her guidance, Royal Bafokeng has diversified into a formidable sector-spanning investment force.

Miriam Chidiebele Olusanya, the Managing Director of Guaranty Trust Bank, is a visionary leader in finance, renowned for her commitment to excellence. From humble beginnings in Nigeria, her journey was marked by academic brilliance and a natural affinity for numbers. Rising through the ranks with tenacity and strategic prowess, she now spearheads the institution’s vision with confidence.

Under Miriam’s leadership, Guaranty Trust Holding Company has experienced remarkable growth, solidifying its position in the financial world. Her keen insight into market trends ensures the company’s resilience in dynamic economic landscapes. Beyond her professional achievements, Miriam is dedicated to nurturing the next generation of leaders through mentorship initiatives.

Known for her warmth and humility, Miriam inspires colleagues to strive for greatness. Her story—from a small-town scholar to a trailblazer in finance—is a testament to determination and resilience. With Miriam at the helm, Guaranty Trust Holding Company is poised for continued success and prosperity.

CEO and Group MD, East African Breweries PLC (EABL)

Revenue: US$970 million

Country: Kenya

As EABL Group MD and CEO since 2021, Jane Karuku made history by becoming the first woman to lead the 100-year-old company. She is among the most senior business leaders in East Africa, driving the region’s largest and most profitable manufacturing business with over 40 global brands like Johnnie Walker and Guinness.

Under Karuku’s tenure, EABL has undergone a remarkable financial and operational turnaround. In 2021, she oversaw a 15% year-over-year jump in net sales to Sh86 billion, surpassing pre-pandemic 2019 levels. Her leadership also saw EABL publish its inaugural Sustainability Report with initiatives like a $5 million pub/bar recovery fund and an ambition to locally source up to 80% of raw materials.

Karuku’s 25-year career spans FMCG companies and NGOs, amassing expertise in strategy, operations, marketing, and organizational change. She has held senior roles at Farmers Choice Kenya, Kenya Cooperative Creameries, Alliance for a Green Revolution in Africa, Telkom Kenya where she led a transformation, and Cadbury with a multi-country remit.

Her strong management experience and contribution to Kenya’s socioeconomic development have earned her numerous accolades, including a presidential award. Karuku holds an MBA in Marketing from the University of California.

8. Ntombi Felicia Msiza

CEO, Raubex Group Ltd

Revenue: US$781 million

Country: South Africa

Seasoned executive Ntombi Felicia Msiza assumed the role of CEO at construction giant Raubex Group in mid-2022, following five years as the Executive Director responsible for Governance, Risk, and Compliance.

Ntombi’s extensive expertise in ethics, strategy, risk management, corporate governance, legal affairs, and compliance has proven invaluable. Her guidance enabled Raubex to strengthen its structures and processes to support the company’s significant growth over the past six years.

Before joining Raubex, Ntombi had a long career in audit and risk management roles. She served as Director of Risk and Assurance at City Power SOC, Head of Internal Audit at IDT, and Group Chief Audit Executive at Denel SOC.

A certified Chartered Director, Ntombi holds a commerce degree and an MBA. Her cross-functional experience across governance, risk, compliance, audit, and strategy positions her well to lead Raubex’s continued expansion in the construction sector.

Ntombi’s appointment as CEO capitalizes on her deep understanding of Raubex’s operations from her prior executive role, combined with her proven track record in governance and risk management for major organizations.

Since becoming Fidelity Bank’s CEO in 2021, Nneka Onyeali-Ikpe has earned numerous accolades, including Banker of the Year and leading Fidelity to wins like Best SME Bank Nigeria 2022. A transformational leader, Nneka spearheaded Fidelity’s turnaround over six years prior as Executive Director, driving the Lagos and South West directorate’s profitability and 28% contribution to the bank’s profits, deposits, and loans.

Her three-decade banking career has honed her strategic expertise, including roles in the successful turnaround of Enterprise Bank. Nneka has cross-functional management experience spanning legal, investment, retail, commercial, and corporate banking at major institutions like Standard Chartered and Zenith Bank.

An authority in transaction structuring across oil and gas, manufacturing, aviation, and real estate, Nneka holds a law degree and Master’s from the University of Nigeria and King’s College. She has extensive executive training from Harvard, INSEAD, and Wharton business schools.

Nneka’s legal acumen, cross-functional leadership experience driving transformation initiatives, and proven turnaround skills make her well-equipped to lead Fidelity Bank’s continued growth.

Zanele Matlala’s nearly two-decade journey at Merafe Resources culminated in her appointment as CEO a decade ago. Having joined the JSE-listed chrome and ferrochrome mining company as an independent non-executive director in 2005 before becoming CFO in 2010, Matlala’s deep understanding of the business has proven invaluable.

Under her stewardship, Merafe reported its second-highest headline earnings in 2017 and adeptly navigated the pandemic rebound, restoring profitability. The company is now one of the JSE’s top “dividend stocks” with a 25% yield, reflecting Matlala’s prudent yet successful guidance.

A chartered accountant by profession, Matlala’s corporate finance expertise spans roles like Financial Director at Kagiso Trust Investments and CFO at the Development Bank of Southern Africa. Last year, her leadership and contributions were recognized with the prestigious Outstanding Alumni Award at the Chancellor’s Calabash Awards.

Matlala’s finance acumen, institutional knowledge of Merafe from board and executive roles, and proven ability to steer the mining company through industry cycles position her uniquely to drive its continued success.

The remarkable achievements of these top female CEOs leading Africa’s biggest public companies underscore the invaluable contributions of women in driving financial success and fostering diversity in leadership roles across African markets.

Whether you’re an individual or institutional investor, download the Daba app or fill out a form on our website now to discover opportunities to invest in visionary companies led by exceptional women.

L’esprit entrepreneurial en Afrique est en plein essor, avec des startups et des petites entreprises stimulant en grande partie l’innovation, la création d’emplois et la croissance économique sur le continent.

En tant que membre de la diaspora africaine, investir dans ces ventures prometteuses offre une opportunité unique de générer des rendements financiers tout en ayant un impact social significatif dans les communautés qui vous tiennent à cœur.

Cependant, naviguer dans l’écosystème des startups africaines vaste et diversifié peut être intimidant pour les investisseurs. Par où commencer ? Comment identifier et accéder à des transactions à fort potentiel ? Et quels changements de mentalité sont nécessaires pour dépasser les perceptions obsolètes et débloquer l’immense potentiel entrepreneurial de l’Afrique ?

Voici 5 choses clés à savoir basées sur les idées partagées par les panelistes experts Jennifer Frimpong de Ma Adjaho & Co et le PDG de ARED Henri Nyakarundi lors de la récente partie 1 de notre série de webinaires axés sur l’investissement de la diaspora.

Les plateformes vérifiées comblent le fossé de confiance

1. Les plateformes vérifiées renforcent la confiance et élargissent les opportunités. Avec 54 pays, l’Afrique est un continent vaste et diversifié. Identifier et accéder à des opportunités d’investissement de haute qualité nécessite un accès fiable et une expertise locale.

Des plateformes comme Daba vérifient minutieusement les startups et les petites entreprises, effectuant des diligences raisonnables rigoureuses pour mettre en lumière des ventures prometteuses dans différents secteurs et pays. Cela permet aux investisseurs d’explorer en toute confiance des transactions au-delà des pays et régions familiers, élargissant ainsi leur ensemble d’opportunités.

Dépasser les perceptions obsolètes

2. Regardez au-delà des perceptions obsolètes du paysage des affaires en Afrique. Trop souvent, les investisseurs continuent de voir le continent à travers un prisme obsolète axé principalement sur les industries extractives telles que l’exploitation minière et le pétrole et le gaz. Mais de nouveaux secteurs dynamiques tels que l’agro-industrie, la technologie financière, la logistique et les énergies renouvelables offrent désormais un immense potentiel d’innovation et de croissance.

Évaluez chaque opportunité de startup ou de petite entreprise en fonction de ses mérites propres, plutôt que de rejeter des industries entières en raison de vieux stéréotypes sur le marché africain.

Favoriser le chemin vers la préparation à l’investissement

3. Il est important de comprendre que de nombreuses startups et petites entreprises africaines prometteuses nécessitent un accompagnement et un soutien pour atteindre l’échelle et la “préparation à l’investissement” qui les rendent attrayantes pour les investisseurs.

Elles ont des idées brillantes et un potentiel énorme, mais ont besoin d’aide pour optimiser leurs modèles d’affaires, sécuriser des tours de financement initiaux, construire des opérations et une gouvernance solides, et combler d’autres lacunes de capacités sur le chemin de devenir une entreprise établie et scalable.

C’est là que le partenariat avec des organisations expertes opérant sur le terrain à travers l’Afrique peut être inestimable. Les accélérateurs, les incubateurs, les réseaux d’anges investisseurs et d’autres acteurs profondément enracinés dans les écosystèmes locaux de l’entrepreneuriat peuvent aider à identifier les pépites, à fournir un mentorat et un soutien en matière de renforcement des capacités, et à accompagner les startups vers des étapes clés qui les rendent des propositions d’investissement convaincantes.

L’impératif d’impact

4. Pour les investisseurs de la diaspora, financer les startups et les petites entreprises africaines devrait être plus qu’une simple question de rendement financier. Ces entreprises catalysent une croissance économique inclusive, créent des emplois de qualité et permettent aux personnes et aux communautés de prospérer. Lorsque vous investissez, vous devenez un acteur clé de cet impact transformateur. Laissez l’impact social être une partie essentielle de votre thèse d’investissement et de vos critères de décision.

5. Raconter des success stories peut inspirer une marée montante d’investissement de la diaspora. En identifiant et en finançant des startups africaines prometteuses qui créent de la valeur et impulsent un changement positif, partagez ces exemples largement. Plus il y aura d’histoires de succès et de modèles à succès visibles dans cet écosystème, plus il sensibilisera et catalysera d’autres membres de la diaspora à s’impliquer en tant qu’investisseurs et partisans.

Catalyser l’avenir entrepreneurial du continent

Le moment est venu pour la diaspora de jouer un rôle catalyseur dans l’investissement dans le futur entrepreneurial de l’Afrique. Avec des projections selon lesquelles l’Afrique aura la plus grande population en âge de travailler au monde dans quelques décennies seulement, permettre et libérer l’ingéniosité des jeunes entrepreneurs du continent aujourd’hui peut tracer un cours prospère pour les générations à venir.

Suivez les idées ci-dessus pour vous engager de manière stratégique dans l’écosystème d’investissement des startups en Afrique. Adoptez la bonne mentalité et les bons partenariats pour aller au-delà des perceptions obsolètes. Utilisez des plateformes de confiance pour accéder aux opportunités dans la diversité des industries et marchés du continent. Et ancrez votre approche d’investissement dans la force motrice de la création d’un impact social positif à travers l’autonomisation économique.

Si vous n’avez pas pu assister au webinaire ou si vous souhaitez le revoir, vous pouvez visionner l’enregistrement sur notre chaîne YouTube. Et pour en savoir plus sur la façon dont Daba permet d’investir dans les opportunités en Afrique pour les investisseurs individuels et institutionnels, visitez notre page web ou téléchargez notre application mobile.

Africa’s entrepreneurial spirit is soaring, with startups and small businesses driving much of the innovation, job creation, and economic growth on the continent.

As a member of the African diaspora, investing in these promising ventures presents a unique opportunity to generate financial returns while creating meaningful social impact in the communities you care about.

But navigating the vast and diverse African startup ecosystem can be daunting for investors. Where do you start? How do you identify and access high-potential deals? And what mindset shifts are needed to see beyond outdated perceptions and unlock Africa’s immense entrepreneurial potential?

Here are 5 key things to know based on insights shared by expert panelists Jennifer Frimpong of Ma Adjaho & Co and ARED CEO Henri Nyakarundi during the recent Part 1 of our diaspora investment-focused webinar series.

Vetted Platforms Bridge the Trust Gap

1. Vetted platforms build trust and expand opportunity. With 54 countries, Africa is a vast and diverse continent. Identifying and accessing high-quality investment opportunities requires trusted access and local expertise.

Platforms like Daba thoroughly vet startups and small businesses, conducting rigorous due diligence to surface promising ventures across sectors and borders. This allows investors to confidently explore deals beyond just familiar countries and regions, expanding their opportunity set.

Shedding Outdated Perceptions

2. Look beyond outdated perceptions of Africa’s business landscape. Too often, investors still view the continent through an outdated lens focused primarily on extractive industries like mining and oil & gas. But vibrant new sectors like agribusiness, fintech, logistics, and renewable energy now offer immense potential for innovation and growth.

Evaluate each startup or small business opportunity on its own merits, rather than dismissing entire industries due to old stereotypes about the African market.

An in-session snapshot of our webinar this week. Catch the full conversation on our YouTube channel.

Nurturing the Path to Investment Readiness

3. It’s important to understand that many promising African startups and small businesses require nurturing and support to reach the scale and “investment readiness” that makes them attractive to investors.

They have brilliant ideas and massive potential but need help optimizing their business models, securing early funding rounds, building robust operations and governance, and bridging other capability gaps on the path to becoming a proven, scalable venture.

This is where partnering with expert organizations operating on the ground across Africa can be invaluable. Accelerators, incubators, angel networks, and other players deeply engrained in local entrepreneurship ecosystems can help identify diamonds in the rough, provide mentorship and capacity-building support, and nurture startups to key milestones that make them compelling investment propositions.

The Impact Imperative

4. For diaspora investors, funding African startups and small businesses should be about more than just financial returns. These enterprises are catalyzing inclusive economic growth, creating quality jobs, and empowering people and communities to thrive. When you invest, you become a key enabler of this transformative impact. Let social impact be a core part of your investment thesis and decision criteria.

5. Telling success stories can inspire a rising tide of diaspora investment. As you identify and fund promising African startups that go on to create value and drive positive change, share those examples widely. The more visible success stories and role models this ecosystem produces, the more it will raise awareness and catalyze other members of the diaspora to get involved as investors and supporters.

Catalyzing The Continent’s Entrepreneurial Future

The time is now for the diaspora to play a catalytic role in investing in Africa’s entrepreneurial future. With projections that Africa will have the world’s largest working-age population in just a few decades, empowering and unleashing the ingenuity of the continent’s young entrepreneurs today can set a thriving course for generations to come.

Follow the insights above to engage strategically in Africa’s startup investment ecosystem. Adopt the right mindset and partnerships to go beyond outdated perceptions. Leverage trusted platforms to access opportunities across the continent’s diversity of industries and markets. And anchor your investment approach in the driving force of creating positive social impact through economic empowerment.

If you could not join the webinar or would like to watch it again, you can catch the recording on our YouTube channel. And to find more about how Daba enables investing in Africa opportunities for individual and institutional investors, visit our webpage or get our mobile app.

Contributed by Kyle Schutter, a Partner at Grant & Co.

To go public, or not…

I attended the Ibuka accelerator, a program to help get private companies listed, kickoff event in October at the Nairobi Securities Exchange.

The Kenyan stock exchange, being the largest in the region, is worth a close look.

The requirements for listing in Nairobi are minimal and it is not nearly as hard to list as people make it out to be. A company needs only 1 year of track record, doesn’t need to be profitable, only needs to list 15% of its shares, only needs a capitalization of about $100,000, and only needs to have 25 shareholders within a few months of listing.

So why aren’t more companies doing it?

The Lagos, Johannesburg, Mauritius, and Nairobi stock exchanges are the most promising places to go public in Africa. We will focus on the Nairobi Securities Exchange as a case study to enable us to deep dive.

Note: nothing here should be construed as an insult to Africa, Kenya, or the Nairobi Securities Exchange. I love Kenya and hope to work together to find solutions that keep increasing investment in and wealth of Africa.

Brand Problem

Listing is only one part of the problem; you must have someone buy your shares. Is there a market that wants to buy shares in these particular companies?

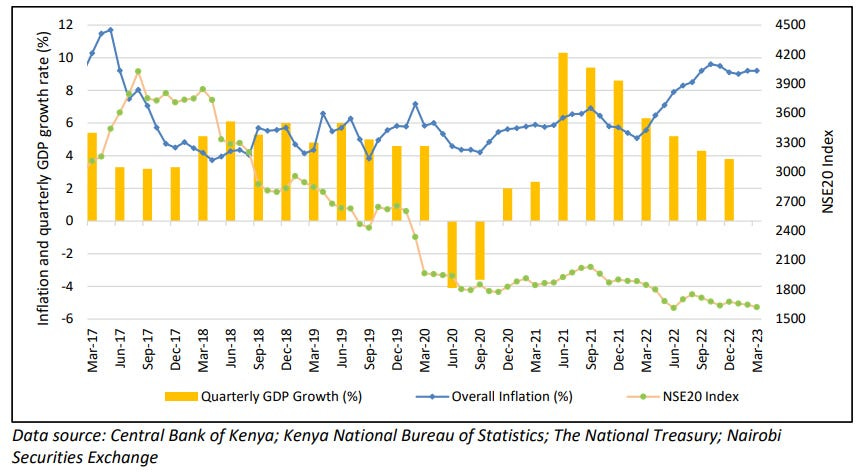

Kenyan equities (stocks) have not performed well, underperforming against bonds land, and even savings accounts. This isn’t a recent phenomenon, although the current economic downturn has worsened it. It has been going down for 8 years.

The NSE 20 index is down from 6,000 in 2015 to 1,400 in 2023.

Why take more risk with equities and get a lower return?

So, the brand name of Equities in Kenya and Africa is generally not good. What factors lead to this, and how can it be fixed?

Remember, Investing is a Keynesian Beauty Contest: the goal is not to pick the most beautiful investment but to pick the one that others think is the best. If Kenyan Equities have a bad brand and investors don’t think others will pick them, then no one will pick them, and they will go down.

Too hard to list… or too easy?

The requirements of the NSE (Nairobi Securities Exchange) are very entrepreneur-friendly, probably too friendly. There are two ways exchanges should maintain quality: ethics and financial performance. The NSE could improve on both accounts.

Ethics: the NSE has frozen the shares of Mumias and Kenya Airways, which prevents shareholders from liquidating their shares and props up the companies so they can keep operating rather than declare bankruptcy.

Financial Performance: Other stock exchanges delist companies if their share price or market capitalization falls too low. The electric scooter startup, Bird, once valued at $3.2b has now been delisted from NYSE because it failed to maintain the $15m market cap minimum threshold and has since gone bankrupt. Stocks that fall below $1.00 per share on the NYSE are also delisted. NSE could also set a minimum price to encourage management to improve performance or face the consequences of being delisted.

A leadership problem?

The Ibuka event had an enthusiastic vibe but maintained certain unfortunate* African stereotypes: the event started 1 hour late, and the presentation contained a major data inaccuracy. Timeliness and data integrity must be core to the culture of a stock exchange. *I likely maintained certain American stereotypes at the event: incessant, obnoxious questions. C’est le vie.

This suggests room for improvement in the NSE company culture and, consequently, for leadership improvement. According to publicly available information, the outgoing CEO of the NSE made Ksh31m (~$210,000), a 19% increase over the previous year, all while making only Ksh14m (~$100,000) for the exchange in profit, a drop of 90% from the previous year. This suggests a problem with his compensation package (and the compensation structuring at the NSE).

Overall, the NSE Equities market has been down since the NSE CEO was appointed 9 years ago, while the Kenyan economy has grown at ~5% a year. Having met him briefly, I had the impression the CEO of the NSE was more of a politician than a visionary who made things happen. Subsequent conversations with market players have not changed that impression.

A new CEO has been appointed as the current CEO has ended his two 4 year terms. Hopefully, new leadership will improve the company culture and results. But this 4-year term suggests more room for improvement: why not have the CEO’s tenure be based on performance? Stock exchanges like NYSE don’t have specific terms for their CEOs. But, perhaps the NSE is a quasi-parastatal. And with the “prestige” associated with running a public market there is a risk that new appointees will be based more on politics than competence and compensation will not be tied to results.

Furthermore, 8 years isn’t enough time to turn something around. A true visionary would want 15 good years to build something great. Imagine Steve Jobs had to leave Apple in 2005 before the iPhone came out. Or Elon had to leave before the Model S came out? The 2×4-year term could be disposed of.

The newly appointed CEO looks to be a strong choice. He is a lawyer/accountant and Partner from EY. We were hoping for an entrepreneur. Hopefully, he will be an entrepreneurial lawyer/accountant.

Capital flight?

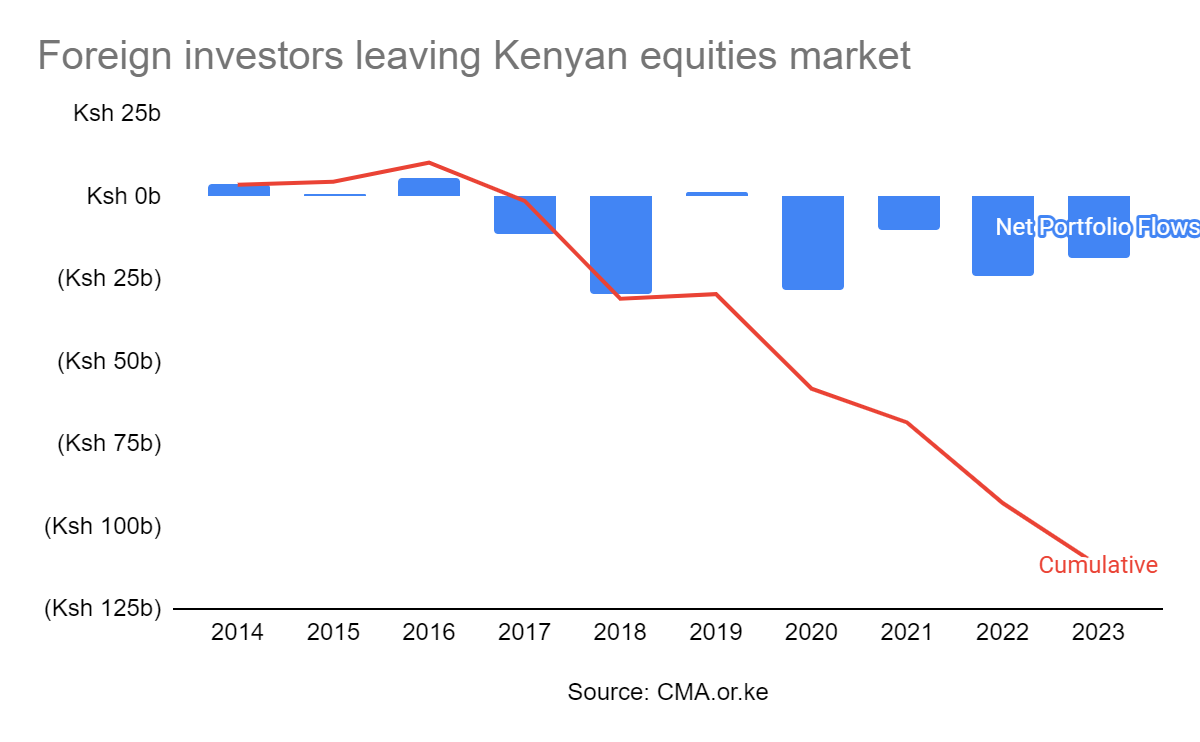

Another explanation for poor NSE performance is that foreign investors are leaving the African stock markets, especially the Kenyan stock market.

However, the Ksh 125b loss due to foreign investors leaving is only part of why the NSE has lost Ksh 1.5 trillion in value since 2021. Capital flight explains less than 10% of the story.

Anti-Free Market behavior

Here are two examples:

The NSE has frozen the trading of Kenya Airlines and Mumias, both of which have substantial government ownership. Kenya Airlines shares have been frozen for 4 years, renewed annually each year with the explanation that Kenya Airways needed time to restructure. In 2022, Kenya Airways lost about $40m. In 2023, they lost about $150m. The more time they get to restructure, the worse it gets. Both companies should go bankrupt, and shareholders should be able to sell their shares. The exchange freezing shares makes investors nervous. By comparison, the NYSE only froze trading for 1 day, and that was when the World Trade Center buildings were attacked in 2001.

That the CEO of the CMA has attempted to put price floors on stock prices is concerning. “Capital Markets Authority (CMA) chief executive Wycliff Shamia told the Star that the move has been necessitated by the fact some of the companies have very strong fundamentals but the valuation is quite low.” Yes, this is how free markets work. The market decides what something is worth, not the government. The latter would be communism.

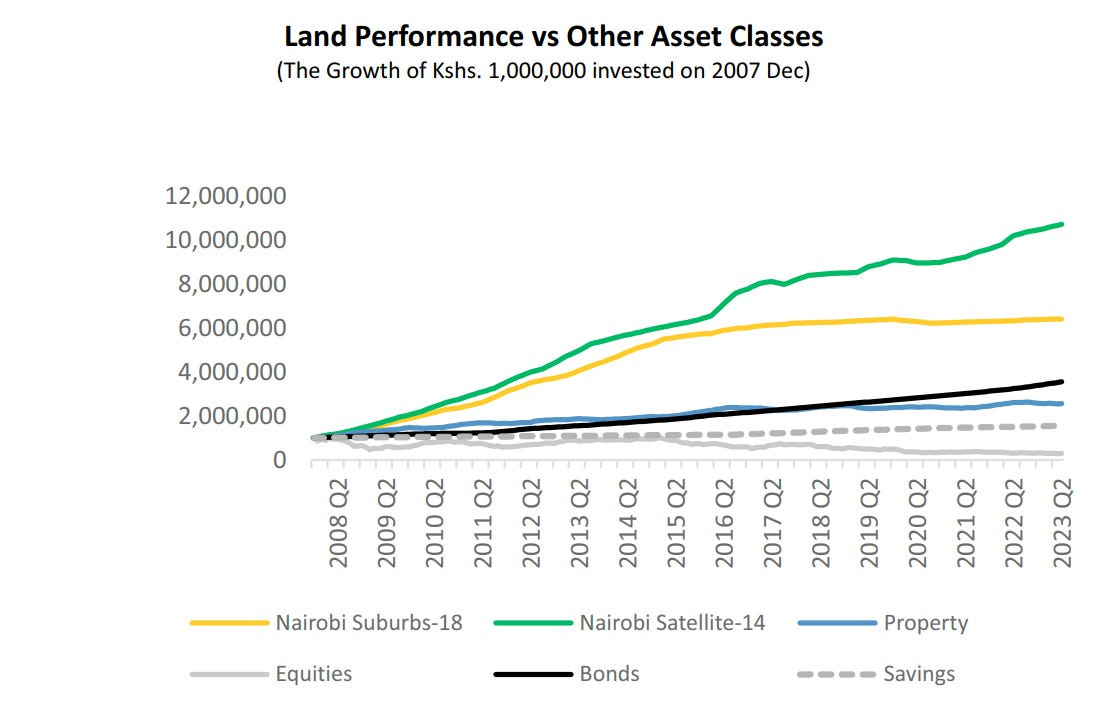

Preference for other investments

Investors would rather speculate on land because Kenya has no property tax. GoK should fairly tax other parts of the economy, like creating a 0.1 to 1% annual Property Tax on land so that people can’t just sit on their land and speculate without contributing to the economy. All other developed and emerging economies have an annual Property Tax; it’s time Kenya did the same. Property tax is generally recognized as the least bad tax for economic growth and yet Kenya doesn’t have it and isn’t even considering it. See here how property tax could be implemented in Kenya and make all parties happy. With the devolved county governments, this could more easily be accomplished than in the past.

The effect of no property tax is clear in the numbers: Kenyan real estate is 75x bigger than equities ($678b vs $9b); meanwhile, by comparison, US real estate is only 2x bigger than US equities ($96T vs $46T). The US equities market sources capital from around the world because people trust Uncle Sam to treat equities fairly, but people don’t (yet) trust Uncle Kamau to do the same. I think the lack of Property Tax is the nail in the coffin of the NSE, and without this reform, there can be no vibrant equities market. (Note: the only meaningful property tax that exists is the capital gains tax when a property is sold, and even then, people can easily underreport the sale price, which is much harder to do on a public equities market. Some counties like Nairobi charge property tax at around $5-30 per year, which is a joke. There is also a tax on Rental payments, but this is not a tax on the property but a tax on a business being done on the property, making matters worse by disincentivizing property development.)

Because Treasury Bonds are over 15%, investors put their money there rather than risk equities. Hopefully, after the Eurobond payment in June 2024, Treasury yields will reduce and more money will flow back to the equities market.

The opportunity

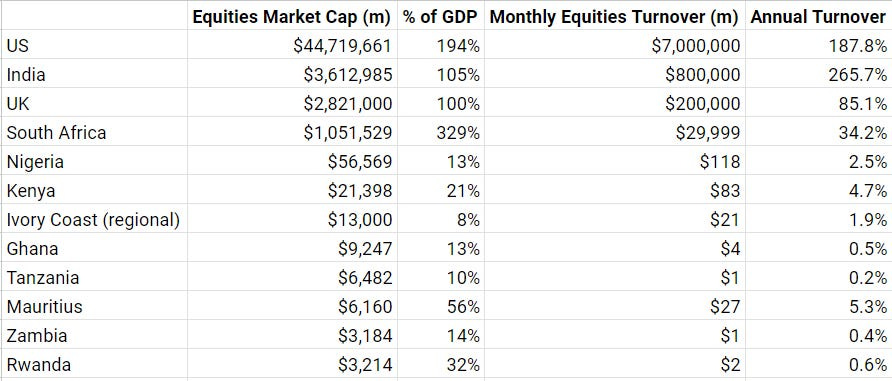

But there are reasons to be bullish on African stock markets. African markets, excluding South Africa, have a relatively small proportion of their GDP trading. There is room for the equities market to grow 10x to align with other markets like the US, South Africa, and India.

Further, Kenya is the region’s largest and most liquid market and could be a regional player—it is already one of the most liquid markets in Africa. By aggregating regional companies onto its exchange, NSE could grow another 10x. On top of that, GDP will compound to 63% growth over the next 10 years. This brings the total NSE market cap potential to ~630x growth over the next 10 years… if NSE can play its cards right. 630x growth would put the NSE in line with India, so it’s not impossible, as discussed below.

On top of that, Annual Turnover (trading of the shares) is relatively low compared to other markets at 4.7% on NSE, ~40x less trading than the US, adjusted for market cap.

There is room for more economic activity on African stock markets.

So where is this 630x growth going to come from?

Increase valuation. The P/E (price to earnings) ratio is only 4.9 on NSE, a sign that investors have low growth expectations. This is half its historical level and 1/4th the ~20 P/E seen on US exchanges, a 4x growth potential for NSE stocks. This is due to uncertainty, low expectations, and discounting for inflation.

More companies listing. About 1% of US companies are publicly listed compared to 0.001%ish (my guesstimate) of Kenyan companies. Realistically, 10x growth potential (as most Kenyan businesses are too small to go public).

NSE quality. If the NSE can improve quality that will improve investor confidence and 2-10x growth.

Virtuous Cycle. There are the compounding effects of a growing market, generating interest and crowding in more capital.

Encourage international investors on local trading platforms. Currently, American, Canadian, Singaporean, and other foreign investors are discouraged from investing through existing brokerage channels and online trading platforms as the regulations in those countries are too costly to manage given the small public market. But as the market grows and trading platforms enable more foreign investors you can imagine that as returns are becoming more predictable with lower returns in the West, some intrepid investors will take an interest in Africa. 2x opportunity

Distribution on international trading platforms. Like Robinhood, Charles Schwab, etc. 10x opportunity.

Cross-listing from other countries in East, Central, and Southern Africa. Theoretically, a 10x opportunity, but in reality, maybe a 2x. Already, some of this is happening. Bank of Kigali (Rwanda) and Umeme (Uganda) are listed in their own countries but cross-listed on NSE. Crosslisting is relatively easy. Evidence suggests that cross-listing increases company valuation, so the cost of cross-listing more than pays for itself. (Source: Peristiani, Federal Reserve Bank of New York, 2010) Old Mutual, for example, is cross-listed on 5 exchanges. A Kenyan equities lawyer confirmed this would be a workable strategy.

Behavioral nudges. There is no way for Kenyan trading apps to automatically reinvest dividends, while automatic reinvestment of dividends is possible in other markets like the US. This could boost share price by 5% per year. This would cut out stock brokers and their fees. My little research online suggests the CMA (Capital Markets Authority) currently prevents automatic dividend reinvestment due to pressure from stock brokers.

Better trading UX. New trading apps that make it easy to buy shares can 2x capital yet again. I tried to sign up with 6 different trading apps and brokers. 3 didn’t allow Americans, Dutch, Singaporeans, or Canadians to trade. The others each had cumbersome documentation requirements: one required a scanned copy of a notarized copy of my passport. What’s the point of a copy of something notarized? The friction to buy shares as a foreigner or local is severe.

Reduced trading fees. This is the big one. CDSC and other government entities can reduce the tax on trading, which is currently at 0.36%. If a stock is only expected to gain 10% a year, paying 0.36% per trade precludes an efficient market that quickly buys and sells. For comparison, the NYSE has a fee on trades of $0.001 (which comes to 0.003% for a typical $30/share stock, 1/100th the price of Kenyan fees). Broker fees are also extremely high in Kenya at 1-1.5%, 10x higher than in the US at 0-0.1%. Reducing fees would not directly increase market cap, but a 10x reduction in fees might increase liquidity 10x, bringing the NSE more in line with other exchanges, from 4.7% turnover to perhaps 50% turnover. Increasing liquidity would perhaps increase the market cap by 2-10x by increasing P/E and crowding in more companies.

Improving taxation. Right now, US investors in Kenyan companies get taxed twice. Thus, going through Mauritius is advantageous.

Case study 1:

I tried to sign up for various trading apps (Exness, Sterling, AIB-AXYS, ABC). Finally, after a week I was able to sign up on EFG Hermes. I tried to trade using the Market Price but the Market Price was 2x the Limit Price. I was told by customer service to ignore the Market Price. Once I did make a trade it took two days for my trade to be reflected in the app. After many customer service requests, my trade was reflected but then the app showed I had a negative account balance. After another customer service call that has been fixed. Then my password stopped working.

I can see why there might not be a lot of retail investors in Kenyan securities as the buying experience does not inspire confidence. But it does show an opportunity for someone to build a better trading experience.

Why are companies resistant to going public?

Before we determine whether listing at all would benefit companies, let’s consider:

does going public preclude a company from raising additional institutional capital?

what are the tax implications?

what are the compliance costs?

with interest rates as they are, is now really the right time to list?