Les investisseurs institutionnels et individuels ont pu soutenir la mission de BuuPass consistant à numériser le secteur de la mobilité en Afrique via la plateforme d’investissement unifiée de Daba.

BuuPass, une plateforme de billetterie de voyage numérique basée au Kenya, a récemment reçu un investissement de Tim Draper, un capital-risqueur renommé.

BuuPass a obtenu l’investissement de Draper en participant à l’émission de télé-réalité Meet the Drapers. Le montant levé n’a pas été divulgué. Jusqu’à présent, la startup avait levé 2,5 millions de dollars depuis sa fondation.

Qui est Tim Draper ?

Tim Draper est le fondateur de Draper Associates, DFJ et du Draper Venture Network. Il a financé une remarquable série de sociétés à succès, dont Coinbase, Baidu, Tesla, Skype, SpaceX, Twitch et Hotmail, entre autres.

Un défenseur éminent de Bitcoin et de la décentralisation, Draper a été une figure clé dans l’espace des crypto-monnaies, avec des investissements dans plus de 50 sociétés de crypto.

Ses réalisations incluent le titre d’”Entrepreneur du Monde” décerné par le World Entrepreneurship Forum et sa présence parmi les 100 personnes les plus puissantes de la finance selon Worth Magazine.

Ce que cela signifie pour les investisseurs de BuuPass

L’investissement marque la troisième incursion de Draper en Afrique, témoignant de sa confiance dans le potentiel de l’entreprise à révolutionner le paysage des transports en Afrique.

Le financement marque également un bond majeur vers la vision de BuuPass de devenir une licorne dans le secteur des transports. Il alimentera sa mission de numériser le marché du transport longue distance de 100 milliards de dollars en Afrique.

De plus, l’expertise et le réseau mondial de Draper offriront à BuuPass des opportunités de croissance et d’innovation inégalées.

Numérisation du secteur de la mobilité en Afrique

BuuPass est une place de marché B2B2C à pile complète qui connecte les compagnies de transport avec des plateformes de billetterie en ligne.

Traction impressionnante : BuuPass a déjà réalisé d’importants progrès, vendant plus de 16 millions de billets de voyage et générant plus de 100 millions de dollars de GMV, avec une présence en Afrique de l’Est et australe et des itinéraires dans plus de 15 pays.

La start-up prévoit d’utiliser l’investissement pour redoubler d’efforts dans sa mission de numériser le marché africain du transport longue distance en connectant les compagnies de transport avec des plateformes de billetterie en ligne.

“Promesse incroyable”

“BuuPass a montré une promesse incroyable dans la transformation de l’industrie des transports en Afrique”, a déclaré Tim Draper à propos de la start-up. “Je suis ravi de faire partie de ce voyage et j’ai hâte de voir BuuPass stimuler l’innovation et la connectivité à travers le continent.”

Sonia Kabra, co-fondatrice de BuuPass, a exprimé son enthousiasme quant à l’investissement : “Obtenir un investissement de Tim Draper est une étape monumentale pour BuuPass. Sa croyance en notre vision et notre potentiel est un énorme vote de confiance.

“Ce partenariat nous rapproche de notre objectif de mouvement fluide des personnes et des biens à travers l’Afrique, et c’est une étape significative vers la réalisation de notre rêve de devenir une licorne dans le secteur des transports.”

Daba Finance est fier d’avoir permis la participation des investisseurs au parcours de BuuPass et nous sommes impatients de suivre sa croissance et son succès. Pour en savoir plus sur la manière dont Daba permet d’investir dans les opportunités africaines pour les investisseurs individuels et institutionnels, visitez notre site web ou téléchargez notre application mobile.

Through Daba’s unified investment platform, institutional and retail investors supported BuuPass’ mission of digitizing the mobility sector in Africa.

BuuPass, a digital travel ticketing platform based in Kenya, has received an investment from Tim Draper, a renowned venture capitalist.

This comes one year after the company raised $1.3 million in pre-seed funding, which saw the participation of Founders Factory Africa, Renew Capital, Ajim Capital, Google Black Founders Fund, and several individual and corporate investors who participated through Daba Finance.

BuuPass secured the investment from Draper by participating in the Meet the Drapers reality TV show. The amount raised has not been disclosed. Before now, the startup had raised $2.5 million since it was founded.

Who is Tim Draper?

Tim Draper is the founder of Draper Associates, DFJ, and the Draper Venture Network. He has funded a remarkable array of successful companies including Coinbase, Baidu, Tesla, Skype, SpaceX, Twitch, and Hotmail, among others.

A prominent advocate for Bitcoin and decentralization, Draper has been a pivotal figure in the cryptocurrency space, with investments in over 50 crypto companies.

His accolades include being named “Entrepreneur of the World” by the World Entrepreneurship Forum and ranking among the top 100 most powerful people in finance by Worth Magazine.

What this means for investors in BuuPass

The investment marks Draper’s third venture in Africa, reflecting his confidence in the company’s potential to revolutionize Africa’s transportation landscape.

The funding also signifies a major leap toward BuuPass’s vision of becoming a unicorn in the transportation sector. It will fuel its mission to digitize the $100 billion long-distance transport market in Africa.

In addition, Draper’s expertise and global network will provide BuuPass with unparalleled opportunities for growth and innovation.

Digitizing Africa’s mobility sector

BuuPass is a B2B2C full-stack marketplace that connects transport companies with online ticketing platforms.

BuuPass has already made significant strides, selling over 16 million travel tickets and generating over $100 million in GMV, with a presence in East and Southern Africa with routes across more than 15 countries.

The startup plans to use the investment to double down on its mission to digitize the African long-distance transport market by connecting transport companies with online ticketing platforms.

“Incredible Promise”

“BuuPass has shown incredible promise in transforming the transportation industry in Africa,” Tim Draper said on the startup. “I am excited to be part of this journey and look forward to seeing BuuPass drive innovation and connectivity across the continent.”

Sonia Kabra, co-founder of BuuPass, expressed her excitement about the investment: “Securing investment from Tim Draper is a monumental milestone for BuuPass. His belief in our vision and potential is a huge vote of confidence.

“This partnership brings us closer to our goal of seamless movement of people and goods across Africa, and it’s a significant step towards achieving our dream of becoming a unicorn in the transportation sector.”

Daba Finance is proud to have enabled investor participation in BuuPass’ journey and we look forward to following its growth and success. To find more about how Daba enables investing in Africa opportunities for individual and institutional investors, visit our webpage or get our mobile app.

Ces dernières présentent de forts effets multiplicateurs en vue de réduire la pauvreté et de favoriser la prospérité partagée sur le continent.

L’alimentation et les boissons, l’infrastructure, les soins de santé, l’éducation et les énergies renouvelables sont apparus comme les cinq principaux secteurs pour les opportunités d’investissement dans le rapport.

Ensemble, ils représentent plus de 60 % des opportunités identifiées couvrant l’Afrique de l’Est, de l’Ouest et australe.

L’équipe d’intelligence de Daba explore en outre cinq autres secteurs. Lisez la suite pour découvrir où se trouvent les opportunités d’investissement les plus attractives en Afrique.

Où investir en Afrique : Voici les 10 secteurs les plus prometteurs

1. Alimentation et Agriculture

Le secteur de l’alimentation et de l’agriculture joue un rôle économique intégral à travers l’Afrique.

Malgré la croissance de sa classe moyenne et une réduction de sa dépendance à l’agriculture, l’Afrique continue de connaître une population croissante et une demande croissante en matière d’alimentation.

Par conséquent, le continent offre des perspectives d’investissement substantielles dans les secteurs de l’agriculture et de l’agroalimentaire. Ces opportunités englobent des investissements dans divers aspects de la chaîne de valeur agricole, notamment les terres agricoles, les intrants agricoles, la transformation et les innovations agritech.

L’Afrique subsaharienne, en particulier, est confrontée à des besoins agricoles importants qui vont au-delà des éléments fondamentaux tels que les engrais, les semences et l’irrigation pour inclure des améliorations essentielles de l’infrastructure.

Les entreprises impliquées dans l’amélioration des routes, des installations de stockage, des ports et des réseaux électriques dans la région peuvent également prospérer en soutenant et facilitant la croissance des opérations agricoles florissantes de l’Afrique subsaharienne.

Ces investissements offrent non seulement des rendements financiers potentiels, mais contribuent également à relever les défis de sécurité alimentaire auxquels la région est confrontée.

L’Afrique continue de connaître une population croissante et une demande croissante en alimentation.

2. Infrastructure

Les besoins en infrastructure restent critiques pour faire avancer les résultats socio-économiques. Les exigences continuent de croître au milieu de l’urbanisation rapide et de l’industrialisation.

Bien que la pénurie d’infrastructures en Afrique soit indéniable, elle offre de nombreuses opportunités d’investissement, notamment pour des secteurs tels que la construction, les télécommunications, l’énergie et les transports, entre autres.

La BAD estime que le continent aura besoin jusqu’à 170 milliards de dollars par an d’ici 2025 pour rénover ses infrastructures, les deux tiers de ce montant étant nécessaires pour des infrastructures entièrement nouvelles et le tiers restant pour la maintenance.

Par conséquent, les routes, le logement, l’électricité, la gestion des déchets et d’autres projets à long terme signalent un fort potentiel de partenariat public-privé.

3. Soins de Santé

Les secteurs des soins de santé et des médicaments sur ordonnance sont estimés à une valeur combinée de 3 milliards de dollars, les médicaments innovants/brevetés contribuant approximativement à hauteur de 1,7 milliard de dollars à cette valeur. Les médicaments en vente libre détiennent actuellement une valeur de 378 millions de dollars.

Étant donné la montée en puissance des sociétés pharmaceutiques produisant des médicaments génériques, il est fort probable qu’il y ait une augmentation des investissements dans le secteur de la santé du pays.

Cela est particulièrement significatif compte tenu du fait que 85 % de la population africaine dépend des services de santé publics.

Il est raisonnable de prévoir que le public accueillerait favorablement le Plan national d’assurance maladie, cherchant ainsi à accéder à des médicaments et à des installations de traitement plus abordables.

Ne manquez pas les opportunités d’investissement exclusives en Afrique ! Téléchargez l’application Daba dès aujourd’hui et débloquez un monde de rendements potentiels tout en ayant un impact positif.

4. Éducation

Investir dans l’éducation en Afrique représente une opportunité de soutenir la croissance du continent tout en générant des rendements.

La population africaine devrait doubler d’ici 2050, ce qui entraînera une demande croissante en matière d’éducation de qualité.

Des opportunités d’investissement existent dans la construction et la gestion d’écoles, la technologie éducative, les bourses d’études et les programmes de formation.

Les écoles privées et l’enseignement supérieur sont particulièrement prometteurs compte tenu de la demande croissante en éducation de qualité et abordable.

La technologie éducative offre également une opportunité à grande échelle. Avec l’augmentation de l’accès aux mobiles et à Internet, les plateformes en ligne et les applications peuvent fournir une éducation abordable dans des régions éloignées et mal desservies.

Investir dans l’éducation en Afrique offre une opportunité de soutenir la croissance du continent tout en générant des rendements.

Fournir des bourses d’études et des formations aux étudiants et aux professionnels africains est un autre investissement important. Les partenariats avec des organisations déjà actives dans cet espace offrent des canaux d’investissement idéaux.

L’expansion de la population jeune de l’Afrique et la demande d’éducation de qualité créent une opportunité de stimuler le développement grâce à l’investissement et de générer des rendements financiers.

5. Énergies Renouvelables

L’Afrique dispose de ressources énergétiques renouvelables abondantes qui présentent d’importantes opportunités d’investissement alors que le continent passe aux sources d’énergie durables.

L’énergie solaire et éolienne devrait connaître une croissance massive, avec une capacité installée augmentant de 100 fois pour le solaire et de 35 fois pour l’éolien d’ici 2050. Cela nécessitera des milliards d’investissements au cours des prochaines décennies.

Le Maroc, l’Afrique du Sud et les pays d’Afrique du Nord seront des marchés clés pour les projets solaires et éoliens en raison de l’irradiation solaire forte et des ressources éoliennes, selon le Forum économique mondial.

L’énergie hydroélectrique offre également un potentiel substantiel, avec une capacité attendue quadruplée d’ici 2050. Les pays d’Afrique subsaharienne disposent des plus grandes ressources hydroélectriques restantes à exploiter. La production d’hydrogène vert est un autre domaine prêt pour une croissance et des exportations majeures, avec des projets déjà en cours au Maroc, en Namibie et en Afrique du Sud.

Cumulativement, près de 3 000 milliards de dollars de dépenses en capital sur les énergies renouvelables et les infrastructures de soutien seront nécessaires en Afrique d’ici 2050. Investir tôt permet aux institutions financières de conduire la transition et de capitaliser sur les opportunités à long terme.

Le paysage des technologies propres en Afrique connaît un essor sans précédent, alimenté par une combinaison de ressources renouvelables abondantes.

6. Marchés des matières premières

De nombreux pays africains dépendent largement du commerce des matières premières. Certains d’entre eux naviguent à travers les cycles des matières premières, comme le montrent les principaux pays exportateurs de pétrole comme l’Angola et le Nigeria, ainsi que les pays producteurs de cuivre tels que la République démocratique du Congo et la Zambie.

Selon les estimations de l’ONU, l’Afrique détient plus de 30 % des réserves minérales mondiales, y compris plus de la moitié des réserves mondiales d’or, de chrome et de platine, une proportion importante des réserves mondiales de diamants, et 5 % des réserves naturelles de minerai de lithium.

Le continent abrite également les principaux exportateurs mondiaux de produits agricoles tels que le cacao (Côte d’Ivoire et Ghana), le café (Éthiopie et Ouganda), le thé (Kenya) et le coton (Bénin, Burkina Faso, Égypte, Soudan et Mali).

Vous recherchez une chance de faire une différence tout en obtenant des rendements. Rendez-vous sur notre application pour commencer à investir dans la croissance de l’Afrique dès aujourd’hui !

7. Commerce de détail et commerce électronique

L’expansion de la classe moyenne africaine, qui est passée de 313 millions de personnes au cours des 30 dernières années, présente des perspectives d’investissement attrayantes dans des secteurs axés sur le commerce de détail.

Pour donner un contexte, les entreprises de télécommunications en Afrique ont ajouté plus de 400 millions d’abonnés, soit plus que l’ensemble de la population américaine, depuis 2000.

La croissance de la classe moyenne africaine peut être attribuée principalement à une expansion économique robuste, à un passage vers l’emploi salarié et à un éloignement de l’agriculture. Le rythme général peut avoir été plus lent que prévu, mais la composition démographique du continent reste attrayante.

Pour répondre à ce marché, une industrie du commerce électronique en pleine croissance émerge rapidement, aidée par un nombre croissant d’utilisateurs d’Internet. D’ici 2025, l’Afrique devrait avoir plus d’un demi-milliard d’acheteurs en ligne, avec une pénétration de 40 % et un taux de croissance annuel composé de 17 %.

8. Immobilier et logement

L’urbanisation et la croissance démographique dans de nombreux pays africains ont alimenté une demande croissante en matière de logements résidentiels et commerciaux.

Ce paysage dynamique offre des opportunités attrayantes dans les projets de développement immobilier, permettant aux investisseurs de capitaliser sur l’élan de croissance du continent pour potentiellement tirer profit de la valorisation des biens immobiliers.

De nombreuses techniques d’investissement éprouvées qui ont réussi dans le monde occidental, telles que les locations à long terme, les fiducies de placement immobilier (FPI), les locations de vacances et les options de bail, peuvent générer des rendements comparables sur le marché africain.

Les investisseurs qui préfèrent une approche prudente peuvent envisager des options telles que les FPI et autres fonds immobiliers. Ces véhicules d’investissement peuvent offrir une exposition au marché immobilier tout en diversifiant les risques et en offrant potentiellement des rendements plus stables.

9. Services Financiers et Fintech

Le paysage des services financiers en Afrique a évolué au cours des deux dernières décennies et jouera un rôle crucial dans la sécurisation de l’avenir du continent.

Sans financement durable et crédit commercial, le développement de projets dans des domaines clés tels que l’infrastructure, les soins de santé et les projets énergétiques reste conceptuel plutôt que réalité.

Les réformes réglementaires, l’émergence d’une classe moyenne urbaine et les avancées technologiques permettent aux institutions financières d’accéder à des mécanismes de financement pour atténuer les risques et maximiser les rendements.

Les revenus dans le secteur des services financiers dans son ensemble pourraient croître à environ 10 % par an pour atteindre 230 milliards de dollars d’ici 2025.

L’émergence de solutions basées sur la technologie financière détient particulièrement une grande promesse pour ce secteur. Le potentiel fintech de l’Afrique était d’environ 150 milliards de dollars en 2020, selon un rapport de McKinsey, alimenté par l’assurance, le commerce de détail et les prêts aux PME.

À l’avenir, le marché devrait croître de 10 % par an pour atteindre environ 230 milliards de dollars d’ici 2025, avec le secteur de la blockchain, des paiements et des portefeuilles prévu pour croître le plus rapidement.

Vous voulez franchir la prochaine étape pour exploiter le potentiel d’investissement de l’Afrique ? Rendez-vous sur notre site Web ou téléchargez dès maintenant l’application Daba pour commencer votre voyage.

10. Technologie et Innovation

Le secteur technologique de l’Afrique connaît une croissance rapide, avec de nombreuses entreprises innovantes émergentes pour relever les défis du monde réel et répondre aux demandes des consommateurs.

Ces startups africaines bénéficient de plusieurs avantages, notamment le fait d’être les premiers à se lancer sur le marché et de s’aligner sur des tendances démographiques favorables.

Malgré le ralentissement économique mondial de 2022, les startups africaines ont réussi à obtenir des niveaux record de financement de la part de capitaux-risqueurs aux États-Unis, en Europe et dans d’autres régions.

Notamment, le continent a même donné naissance à sept licornes – startups valorisées à plus de

1 milliard de dollars – soulignant ainsi davantage le potentiel naissant et le succès de l’industrie technologique en Afrique.

Impacts et Rendements

La plupart des opportunités sont projetées pour générer un nouvel impact positif pour les groupes sous-desservis. Cela indique qu’elles peuvent contribuer de manière significative à surmonter les défis urgents de développement durable.

Elles offrent également des rendements attractifs. Environ la moitié prévoit des taux de rendement internes dépassant 20 %, accompagnés de marges bénéficiaires brutes élevées.

Cependant, des horizons d’investissement à long terme sont courants, en particulier dans des secteurs à forte intensité de capital tels que le transport et l’infrastructure, où la patience est essentielle.

Financement et Mise en Œuvre

Bien que certaines opportunités répondent aux conditions de financement à taux de marché, la plupart nécessitent des approches publiques-privées mixtes.

Ces partenariats peuvent aborder les risques liés à la réglementation, à l’accessibilité, aux lacunes en compétences et aux contraintes de l’environnement propice.

Les collaborations à travers des organismes régionaux tels que la Zone de Libre-Échange Continentale Africaine permettent également aux entreprises d’accéder à des marchés plus vastes, de diversifier les portefeuilles et de partager des expériences. De plus, ils permettent aux pays de se concentrer sur des interventions autour de leurs avantages comparatifs.

La Voie à Suivre: Saisissez les Opportunités d’Investissement en Afrique dès Aujourd’hui

L’Afrique offre de nombreuses perspectives d’investissement pour fournir simultanément un impact positif et des gains financiers à moyen et long terme.

Les investisseurs institutionnels et les partenaires au développement doivent continuer à travailler ensemble pour transformer les opportunités en réalité dans des domaines tels que l’agriculture, l’infrastructure, les soins de santé, l’éducation et les énergies renouvelables.

Pour plus de contenu et d’analyses sur les tendances économiques et les opportunités d’investissement en Afrique, téléchargez dès aujourd’hui l’application Daba ! Et si vous êtes un investisseur institutionnel prêt à explorer des opportunités adaptées à vos intérêts et objectifs, remplissez ce formulaire d’intérêt sur le site Web de Daba !

These present strong multiplier effects towards poverty reduction and shared prosperity on the continent.

Food and beverages, infrastructure, healthcare, education, and renewable energy emerged as the top five sectors for investment opportunities in the report.

Together, they accounted for over 60% of identified prospects spanning Eastern, Western, and Southern Africa.

The Daba Intelligence team further explores five more sectors. Read on to discover where Africa’s hottest investment opportunities lie.

Where To Invest In Africa: Here Are The Top 10 Most Promising Sectors

1. Food and Agriculture

The food and agriculture sector plays an integral economic role across Africa.

Despite the growth of its middle class and a reduced reliance on agriculture, Africa continues to experience a rising population and an increasing demand for food.

As a result, the continent offers substantial investment prospects in the agriculture and agribusiness sectors. These opportunities encompass investments in various aspects of the agricultural value chain, including farmland, agricultural inputs, processing, and agritech innovations.

Sub-Saharan Africa, in particular, faces significant agricultural needs that extend beyond fundamental elements like fertilizer, seeds, and irrigation to include essential infrastructure improvements.

Companies involved in enhancing roads, storage facilities, ports, and power grids in the region can also thrive as they support and facilitate the growth of Sub-Saharan Africa’s thriving agricultural operations.

These investments not only offer potential financial returns but also contribute to addressing the food security challenges that the region faces.

Africa continues to experience a rising population and an increasing demand for food.

2. Infrastructure

Infrastructure needs remain critical for advancing socioeconomic outcomes. Requirements continue rising amidst rapid urbanization and industrialization.

While Africa’s infrastructure shortage is undeniable, it provides abundant investment opportunities – particularly for sectors like construction, telecommunications, energy, and transportation, to name a few.

The AfDB estimates that the continent needs up to $170 billion per year by 2025 to overhaul its infrastructure, with two-thirds of that being needed for entirely new infrastructure and the remaining one-third for maintenance.

Consequently, roads, housing, electricity, waste management, and other long-term projects signal strong public-private partnership potential.

3. Healthcare

The healthcare and prescription medicines sectors are estimated to have a combined worth of $3 billion, with innovator/patented medications contributing around $1.7 billion to this value. Over-the-counter medicines currently hold a value of $378 million.

Given the rise in pharmaceutical companies producing generic medicines, there’s a strong likelihood of increased investment in the nation’s healthcare sector.

This is particularly significant considering that 85% of Africa’s population depends on public health services.

It’s reasonable to anticipate that the public would readily embrace the National Health Insurance Plan, seeking access to more affordable medicines and treatment facilities.

Don’t miss out on exclusive investment opportunities in Africa! Download the Daba app today and unlock a world of potential returns while making a positive impact.

4. Education

Investing in education in Africa presents an opportunity to support the continent’s growth while yielding returns. Africa’s population is expected to double by 2050, driving demand for quality education.

Investment opportunities exist in building and running schools, educational technology, scholarships, and training programs. Private schools and higher education are particularly promising given the increasing demand for affordable, quality education.

Educational technology also provides a large-scale opportunity. With growing mobile and internet access, online platforms and apps can deliver affordable education in remote, underserved areas.

Investing in education in Africa presents an opportunity to support the continent’s growth while yielding returns.

Providing African students and professionals with scholarships and training is another impactful investment. Partnerships with organizations already active in this space provide ideal investment channels.

Africa’s expanding youth population and demand for quality education create an opportunity to spur development through investment and generate financial returns.

5. Renewable energy

Africa has abundant renewable energy resources that present major investment opportunities as the continent transitions to sustainable energy sources.

Solar and wind power are projected to see massive growth, with installed capacity increasing 100x for solar and 35x for wind by 2050. This will require billions in investment over the coming decades.

Morocco, South Africa, and North African countries will be key markets for solar and wind projects due to strong solar irradiation and wind resources, according to the World Economic Forum.

Hydroelectric power also offers substantial potential, with capacity expected to quadruple by 2050. Sub-Saharan African countries have the greatest remaining hydro resources to tap. Green hydrogen production is another area primed for major growth and exports, with projects already underway in Morocco, Namibia, and South Africa.

Cumulatively, nearly $3 trillion in capital expenditure on renewables and supporting infrastructure will be needed in Africa by 2050. Investing early can allow financial institutions to drive the transition and capitalize on long-term opportunities.

Africa’s CleanTech landscape is experiencing an unprecedented boom, fueled by a combination of abundant renewable resources.

6. Commodity markets

Many African nations rely extensively on the trade of commodities. Some of them navigate the ups and downs of commodity cycles, exemplified by major oil-exporting countries like Angola and Nigeria, as well as copper-producing nations such as the Democratic Republic of Congo and Zambia.

According to UN estimates, Africa holds over 30% of global mineral reserves, including more than half the world’s reserves of gold, chrome, and platinum, a significant proportion of global diamond reserves, and 5% of naturally occurring lithium ore reserves.

The continent is also home to leading global exporters of agricultural commodities like cocoa (Cote d’Ivoire and Ghana), coffee (Ethiopia and Uganda), tea (Kenya), and cotton (Benin, Burkina Faso, Egypt, Sudan, and Mali).

Looking for a chance to make a difference while earning returns. Head over to our app to start investing in Africa’s growth today!

7. Retail and e-commerce

Africa’s expanding middle class, which has surged from 313 million people over the past 30 years, presents enticing investment prospects in retail-focused sectors.

For context, telecom companies in Africa have added over 400 million subscribers—more than the entire US population—since 2000.

The growth of Africa’s middle class can be attributed mainly to robust economic expansion, a shift towards salaried employment, and a move away from agriculture. The general pace may have been slower than expected but the continent’s demographic makeup remains attractive.

Catering to this market is a rapidly growing e-commerce industry, helped by an increasing number of Internet users. By 2025, Africa is forecast to have over half a billion online shoppers, with a 40% penetration, and a 17% compound annual growth rate (CAGR).

8. Real estate and housing

Urbanization and population growth in numerous African countries have fueled a rising demand for both residential and commercial real estate.

This dynamic landscape offers compelling opportunities in real estate development projects, allowing investors to capitalize on the continent’s growth momentum to potentially profit from the appreciating property values.

Many of the proven investment techniques that have succeeded in the Western world, such as long-term rentals, real estate investment trusts (REITs), vacation rentals, and lease options, can yield comparable returns in the African market.

Investors who prefer a cautious approach can consider options like REITs and other real estate funds. These investment vehicles can provide exposure to the real estate market while diversifying risk and potentially offering more stable returns.

9. Financial services and fintech

Africa’s financial services landscape has evolved over the last two decades and will play a critical role in securing the continent’s future.

Without sustainable funding and commercial credit, project development in key areas such as infrastructure, healthcare, and energy projects remain concepts rather than reality.

Regulatory reforms, the emergence of an urban middle class, and technological advancements allow financial institutions access to funding mechanisms to mitigate risk and maximize returns.

Want to take the next step in tapping Africa’s investment potential? Head over to our website or download the Daba app now to start your journey.

Revenues in the financial services sector at large could grow at about 10% per annum to $230 billion by 2025.

The emergence of fintech-driven solutions particularly holds great promise for this sector. Africa’s fintech potential was around $150 billion in 2020, per a report by McKinsey, fueled by insurance, retail, and SME lending.

Going forward, the market is projected to grow by 10% per year to reach around $230 billion by 2025, with the blockchain, payments, and wallets sectors expected to grow fastest.

10. Technology and Innovation

Africa’s technology sector is experiencing rapid growth, with numerous innovative companies emerging to address real-world challenges and cater to consumer demands.

These African startups enjoy several advantages, including being early movers in the market and aligning with favorable demographic trends.

Despite the global economic slowdown experienced in 2022, African startups managed to secure record levels of funding from venture capitalists in the United States, Europe, and other regions.

Notably, the continent has even given rise to seven unicorns – startups valued at over $1 billion – further underlining the burgeoning potential and success of Africa’s tech industry.

Impact and Returns

Most opportunities are projected to generate a new positive outcome for underserved groups. This indicates they can meaningfully contribute to overcoming pressing sustainable development challenges.

They also offer attractive returns. About half forecast internal rates of return exceeding 20%, alongside high gross profit margins.

However, long investment horizons are common, especially in capital-intensive sectors like transportation and infrastructure where patience is key.

Financing and Implementation

Although some opportunities meet conditions for market-rate financing, most require blended public-private approaches.

These partnerships can address risks related to regulation, affordability, skills gaps, and enabling environment constraints.

Collaborations through regional bodies like the African Continental Free Trade Area also allow businesses to access larger markets, diversify portfolios, and share experiences. Additionally, they enable countries to focus interventions around their comparative advantages.

The Way Forward: Seize Africa’s Investment Opportunities Today

Africa provides abundant investment prospects to simultaneously deliver positive impact and financial gains over the medium to long term.

Institutional investors and development partners should continue working together to turn opportunities into reality in areas including agriculture, infrastructure, healthcare, education, and renewable energy.

And for retail investors, the good news is that the proliferation of investment platforms like Daba makes participating in investment opportunities in Africa’s emerging markets easier than ever.

For more content and analysis on economic trends and investment opportunities in Africa, get the Daba application today! And if you’re an institutional investor ready to explore opportunities tailored to your interests and objectives, fill out this interest form on the Daba website!

L’une des principales questions que se posent souvent les investisseurs souhaitant diversifier leur portefeuille est : “Où investir en Afrique ?” Les actions africaines offrent certaines des opportunités les plus prometteuses pour les investisseurs particuliers et institutionnels.

Dans ce blog, nous explorons certaines des tendances marquantes sur la bourse l’année dernière et pourquoi les investisseurs intéressés par l’Afrique devraient se tourner vers la Bourse Régionale des Valeurs Mobilières (BRVM), la bourse régionale desservant huit pays d’Afrique de l’Ouest francophones.

Qu’est-ce que la BRVM ?

La Bourse Régionale des Valeurs Mobilières (BRVM) sert de bourse régionale pour les États membres de l’Union Économique et Monétaire Ouest-Africaine (UEMOA).

Il s’agit notamment du Bénin, du Burkina Faso, de la Côte d’Ivoire, de la Guinée-Bissau, du Mali, du Niger, du Sénégal et du Togo.

Malgré des défis tels que l’inflation et les tensions politiques, la BRVM a fait preuve de résilience en 2023, avec son indice composite affichant une croissance constante.

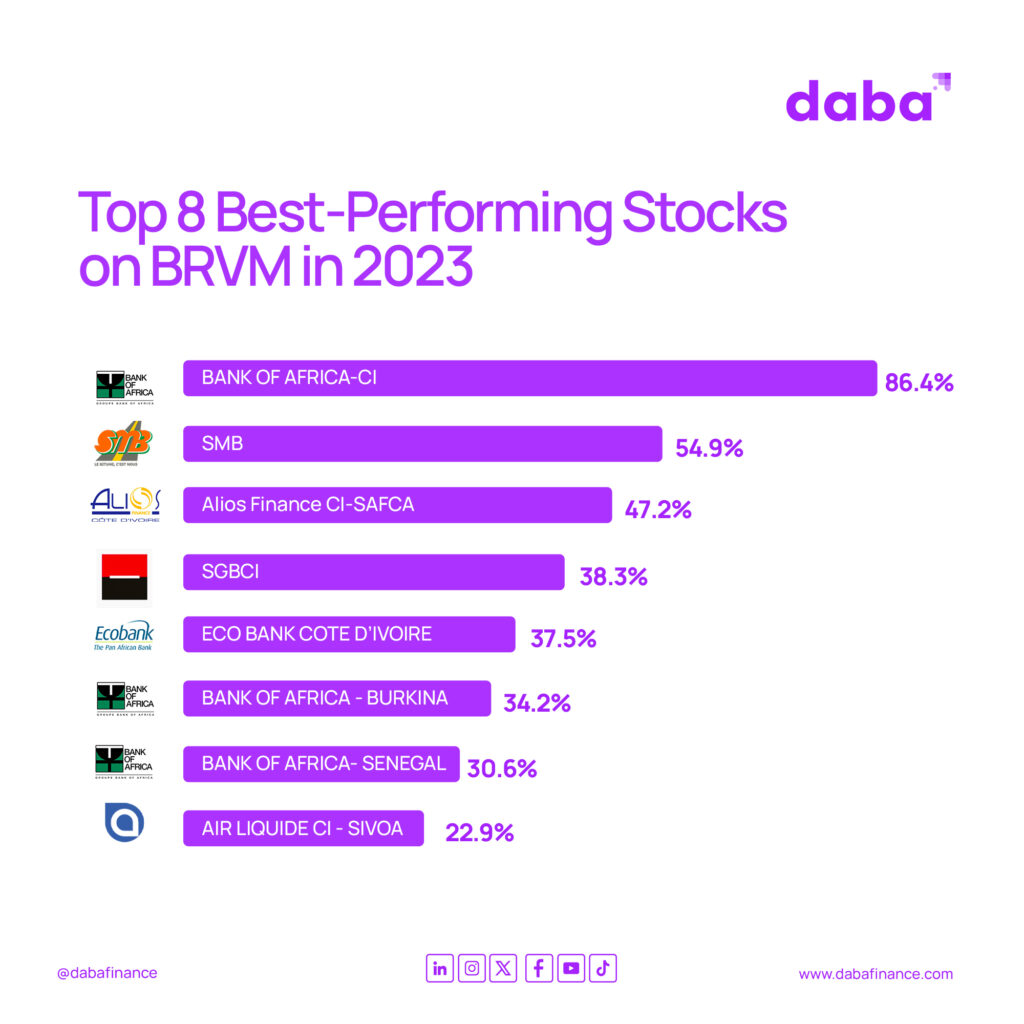

1. BOA, Sonatel, Orange en tête

L’année dernière, 21 actions ont connu des périodes prospères, enregistrant des gains en capital notables, tandis que 23 actions ont connu un déclin, avec 2 maintenant la stabilité.

Les secteurs de la finance et des services publics ont notamment contribué à l’orientation positive du marché boursier de la BRVM, enregistrant des gains de 14,45 % et 8,64 % respectivement.

Notamment, des actions au sein de ces secteurs, telles que Sonatel et Orange Côte d’Ivoire, ont joué un rôle crucial dans cette performance. BOA CI s’est révélé être le meilleur performer, affichant un gain impressionnant de 86,35 %, alimenté par les opportunités dans le secteur bancaire ivoirien.

L’indice composite de la BRVM, l’indicateur de performance global, a connu une croissance initiale modeste à 203,22 points (+0,46 %). Cependant, il a conclu l’année avec une augmentation notable de 5,38 %, atteignant 214,15 points, marquant ainsi sa troisième année consécutive de croissance.

Vous voulez diversifier votre portefeuille ? Les actions phares de la BRVM offrent des opportunités prometteuses pour les investisseurs. Consultez l’application Daba pour y accéder.

2. Augmentation de la distribution de dividendes

Malgré les défis de 2022 et les directives prudentes de la BCEAO concernant la distribution de dividendes des banques, les sociétés cotées à la BRVM ont considérablement augmenté la rémunération des actionnaires en 2023. Les dividendes distribués aux investisseurs ont augmenté de 25,82%, totalisant 647,8 milliards de FCFA.

Des entreprises telles que Sonatel, Orange CI, Société Générale CI, Ecobank CI et Société Ivoirienne de Banque se sont démarquées en distribuant des sommes substantielles à leurs actionnaires.

3. Brandon McCain acquiert des actions dans BICICI

Brandon McCain Capital, dirigé par Ahmed Cissé, a acquis une participation de 19,11% dans BICICI auprès du groupe SUNU bancassurance. Cette transaction, évaluée à 22,12 milliards de FCFA, marque un changement significatif dans la structure de l’actionnariat de BICICI.

4. Vista Group négocie le rachat d’actions d’Oragroup

Le Vista Group a engagé des discussions pour le rachat des actions d’Oragroup détenues par ECP. Cet accord, avec un consortium dirigé par Emerging Capital Partners, vise à faire de Vista le principal actionnaire d’Oragroup, détenant plus de 61% des actions.

Cependant, des divergences de valorisation entre ECP et le groupe de Simon Tiemtoré posent des défis à l’achèvement de l’accord.

5. La BRVM dépasse la barre des 8 000 milliards de FCFA

Un jalon important atteint par la BRVM en 2023 a été son franchissement historique de la barre des 8 000 milliards de FCFA en capitalisation boursière. Cette occasion mémorable a eu lieu le 12 septembre 2023, propulsée par des sommets notables dans les actions de Société Générale CI et Orange CI, au milieu d’augmentations généralisées.

Par la suite, le 20 septembre 2023, la BRVM est devenue le cinquième marché le plus important en Afrique, avec une capitalisation boursière de 12,861 milliards de dollars, dépassant celle de la bourse de Nairobi de 9,77 milliards de dollars.

La cotation d’Orange Côte d’Ivoire à la fin de 2022 a largement contribué à cette réalisation, représentant environ 20% de la capitalisation boursière totale.

Malgré une baisse du volume global des transactions de 45,8% par rapport à 2022, la valeur des transactions a augmenté de 41,2%, atteignant 246 milliards de FCFA en 2023, reflétant une évolution positive du marché.

À la recherche d’un moyen simple de tirer parti de l’histoire de croissance de la BRVM ? Daba offre une expérience transparente pour les investisseurs. Rejoignez-nous dès aujourd’hui et commencez votre parcours !

6. Acquisition du groupe Crédit d’Afrique par Alios Finance

Le 12 décembre, Tunisie Leasing et Factoring a annoncé son accord avec le groupe Crédit d’Afrique, dirigé par l’entrepreneur à succès Serge BILE, pour l’acquisition de ses filiales.

Cette acquisition comprend des participations majoritaires dans les filiales d’Alios Finance en Côte d’Ivoire, au Cameroun et au Gabon. Alors que la filiale ivoirienne était confrontée à des défis financiers, cette vente pourrait potentiellement découler des performances financières des filiales.

Safca, contrôlée à 52,02% par Alios Finance, a connu une augmentation significative de 47,16% de sa valeur boursière à la BRVM à la fin de l’année.

7. Records historiques pour Ecobank CI, Société Générale CI et SIB

En 2023, certaines actions ont atteint leurs prix les plus élevés depuis leur introduction à la BRVM. Notamment, Ecobank CI, Nestlé CI, Orange CI, Société Générale CI et SIB ont atteint des jalons significatifs dans leur évolution de prix.

Ces développements, tout en reflétant un sentiment de marché positif, peuvent avoir un impact sur les bénéfices, les dividendes et les actifs nets. Les attentes élevées des investisseurs pourraient entraîner une augmentation des ratios cours/bénéfices et une baisse de la rentabilité moyenne, affectant l’attrait des actions en fonction du rendement des dividendes.

8. Meilleurs rendements offerts lors des publications

Avec la publication des états financiers pour 2022 au cours de 2023, plusieurs entreprises se sont distinguées par le niveau de rémunération des actionnaires qu’elles ont offert. BOA BF a mené le classement avec un rendement de dividende notable de 11,09%, suivi par Palmci à 11,05%.

Nestlé CI, BOA CI et SOGB ont complété le top 5 avec des rendements respectifs de 10,79%, 10,40% et 10,30%. Cet indicateur, avec un rendement moyen en dividendes de plus de 10%, a contribué à renforcer la confiance des investisseurs dans le marché boursier.

Prêt à profiter de généreux dividendes des actions de la BRVM ? Avec la plateforme intuitive de Daba, investir n’a jamais été aussi facile. Téléchargez l’application dès maintenant pour commencer.

9. Les concessions de Sonatel

Malgré sa domination de longue date, Sonatel s’est retrouvé déplacé en tant que géant de la capitalisation boursière à la BRVM, cédant la première place à son homologue ivoirien, Orange CI.

L’introduction en bourse réussie d’Orange Côte d’Ivoire, la plus importante jamais réalisée sur le marché de la BRVM, a suscité l’excitation du marché, propulsant sa valeur boursière de près de 15% en seulement deux séances.

Cependant, la consolidation post-introduction en bourse a permis à Sonatel de récupérer sa position, partageant désormais la domination du marché avec Orange CI, commandant collectivement plus de 42% de la capitalisation boursière globale.

Investir dans des actions africaines, en particulier via des plateformes comme la BRVM, offre aux investisseurs une porte d’entrée vers des opportunités diverses et prometteuses.

En comprenant les tendances du marché, les développements stratégiques et la performance sectorielle, les investisseurs peuvent prendre des décisions éclairées sur où et comment investir dans les marchés boursiers dynamiques de l’Afrique, débloquant ainsi le potentiel de croissance du continent et contribuant au succès des investissements à long terme.

La plateforme d’investissement de pointe de Daba offre aux investisseurs un moyen transparent et efficace de découvrir, de négocier et de surveiller les investissements sur la BRVM. Téléchargez dès maintenant l’application Daba pour commencer à constituer votre portefeuille BRVM dès aujourd’hui.

Un séisme politique a frappé l’Afrique de l’Ouest le mois dernier, alors que trois nations dirigées par des juntas militaires annonçaient leur retrait de la Communauté économique des États de l’Afrique de l’Ouest (CEDEAO), le bloc régional.

Le Niger, le Mali et le Burkina Faso ont accusé la CEDEAO de ne pas les avoir soutenus contre la violence djihadiste et l’influence étrangère excessive, avant de quitter l’organisation fin janvier.

Le départ abrupt a suscité des comparaisons avec le “Brexit” (le retrait du Royaume-Uni de l’Union européenne), marquant une rupture historique après des décennies de construction de liens économiques et politiques entre les 15 États membres.

Alors que les répliques se font sentir dans toute la région, voici tout ce que vous devez savoir sur cette crise et ses implications profondes pour le commerce, la sécurité et la vie de millions de personnes en Afrique de l’Ouest.

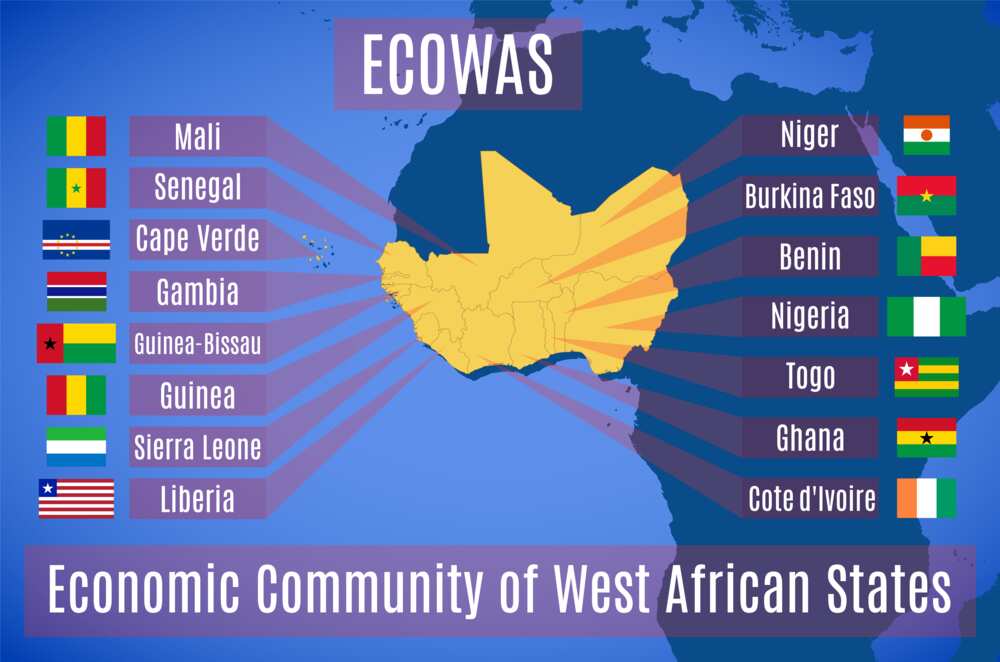

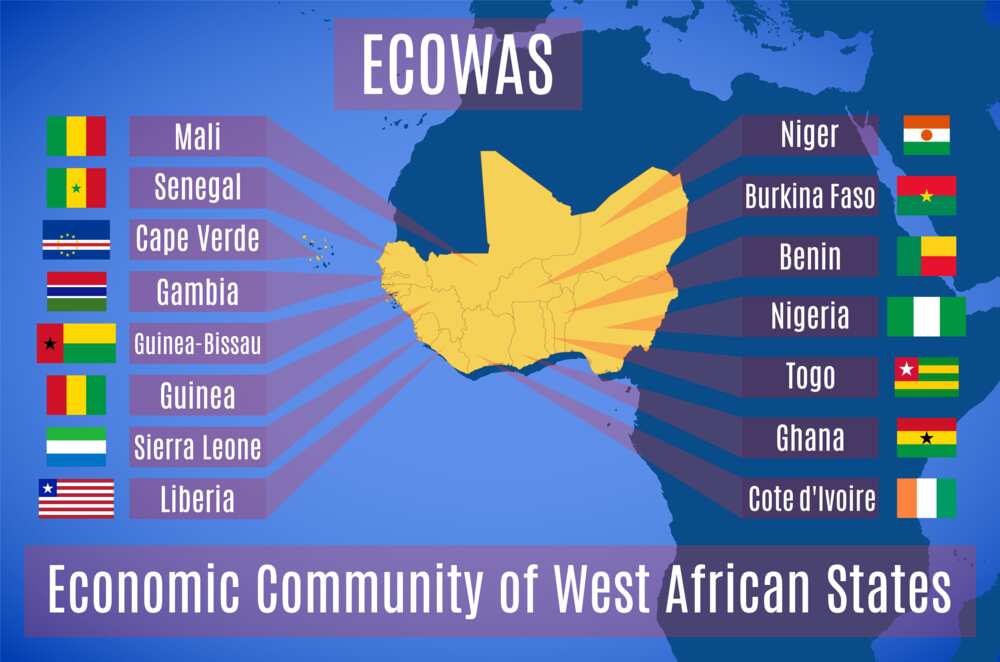

Qu’est-ce que la CEDEAO ?

Fondée en 1975, la Communauté économique des États de l’Afrique de l’Ouest (CEDEAO) comprend 15 nations de la région.

La CEDEAO vise à promouvoir la coopération régionale et le commerce, facilitant les déplacements sans visa pour améliorer les conditions de vie de sa population et assurer la stabilité économique.

Elle joue également un rôle crucial dans les efforts de maintien de la paix dans une partie volatile du continent et est un allié sécuritaire important pour l’Occident, y compris les États-Unis.

La présidence du bloc est tournante parmi ses États membres, le Nigeria, la puissance économique de la région, étant actuellement en charge.

États membres de la CEDEAO

Pourquoi le Burkina Faso, le Mali et le Niger ont-ils quitté la CEDEAO ?

Ces dernières années, le Burkina Faso, le Mali et le Niger ont été submergés par des insurrections djihadistes et une instabilité politique, subissant plusieurs coups d’État.

Le Mali a connu deux coups, un en 2020 et un autre en 2021. Le Burkina Faso a fait face à deux coups en moins d’un an en 2022. Enfin, le Niger a connu un coup d’État l’été dernier.

La CEDEAO a réagi en suspendant les pays et en imposant des sanctions sévères. Cela a entraîné un ressentiment croissant et un défi de la part des juntas militaires qui dirigent désormais ces nations.

Ils accusent la CEDEAO de ne pas avoir fourni de soutien contre le terrorisme et d’être influencée par des “puissances étrangères” comme la France.

Ne manquez pas de profiter des changements dynamiques en Afrique de l’Ouest. Obtenez dès maintenant l’application Daba pour des alertes opportunes et des recommandations personnalisées afin d’optimiser votre portefeuille d’investissement.

Le Niger, le Mali et le Burkina Faso accusent la CEDEAO de ne pas les avoir soutenus contre la violence djihadiste et l’influence étrangère excessive.

Comment la région a-t-elle réagi à cette décision ?

La CEDEAO a exprimé sa tristesse face à cette décision. Le Nigeria, actuel président de la CEDEAO, a déclaré que les dirigeants de junte “non élus” déçoivent leur peuple mais restent ouverts au dialogue.

Les analystes avertissent que les sanctions ont eu un effet contre-productif, alimentant le sentiment anti-français et resserrant les liens avec la Russie.

La menace d’une intervention militaire contre le Niger a mobilisé les citoyens pour soutenir le coup d’État.

Cette position ferme a sapé la crédibilité de la CEDEAO, mais souligne également l’instabilité alors que les armées prennent le pouvoir dans toute la région.

Le président du Nigeria et président en exercice de la CEDEAO, Bola Ahmed Tinubu.

Quels seront les impacts du départ de la CEDEAO sur les pays ?

La décision pourrait nuire gravement aux nations pauvres et enclavées du Sahel qui dépendent fortement du commerce transfrontalier.

Le Niger partage 1 500 km de frontière avec le Nigeria et 80 % de son commerce se fait avec son voisin plus riche.

La fermeture de la frontière par le Nigeria à la suite du coup d’État militaire qui a renversé le président Mohammed Bazoum met en péril des échanges d’une valeur d’environ 226 millions de dollars et des vies, selon plusieurs rapports.

Pour tous les pays dirigés par des juntas, perdre l’accès au marché de la CEDEAO, évalué à 702 milliards de dollars, pourrait entraîner des pénuries, des hausses de prix, des tarifs douaniers accrus et des restrictions financières.

À mesure que les citoyens seront confrontés à plus de difficultés économiques, la pression pourrait s’accentuer sur les régimes de junte fragiles luttant pour contenir la violence.

Comment le “moment Brexit” affectera-t-il la région ?

Les experts ont comparé la séparation imminente au Brexit, avertissant qu’elle pourrait prendre des années à être mise en œuvre mais qu’elle déferlerait des décennies d’intégration.

Les flux commerciaux et de services de la région, d’une valeur de près de 150 milliards de dollars par an, seront perturbés.

Cela soulève également des incertitudes autour des importantes populations de la diaspora du Burkina Faso, du Mali et du Niger vivant dans toute l’Afrique de l’Ouest.

Par exemple, la Côte d’Ivoire accueille plus de 5 millions de migrants de ces nations.

Dans le pire des cas, l’effondrement du bloc pourrait déclencher un exode massif.

La CEDEAO a été critiquée pour avoir rapidement sanctionné les juntas militaires après des années d’inaction contre les dirigeants civils qui ont prolongé leur règne grâce à des élections ou référendums douteux dans des pays comme la Côte d’Ivoire et la Guinée.

Cette double norme a réduit la crédibilité de la CEDEAO. De plus, bien que la CEDEAO ait menacé d’intervenir militairement, son incapacité à concrétiser ces menaces a encore affaibli sa position.

Intéressé par la navigation dans le Brexit de l’Afrique de l’Ouest et la maximisation de vos opportunités d’investissement ? Explorez notre plateforme pour prospérer dans ce paysage de marché en évolution.

Le Niger partage 1 500 km de frontière avec le Nigeria et 80 % de son commerce se fait avec son voisin plus riche.

Depuis longtemps, les experts en sécurité exhortent les pays régionaux à renforcer la coopération et le partage du renseignement pour faire face aux insurrections alimentées par la pauvreté, la négligence, les abus et l’idéologie.

Cependant, la crise actuelle au sein de la CEDEAO met en évidence le fossé cro

issant entre les gouvernements démocratiquement élus alliés à l’Occident et les États dirigés par des militaires de plus en plus dépendants de la Russie et de la Chine pour leur soutien.

Cette scission entrave une réponse régionale coordonnée à l’insécurité croissante et aux insurrections.

À l’avenir, la CEDEAO doit combler ce fossé et renforcer la collaboration entre ses États membres pour relever les défis communs.

Comment les investisseurs peuvent-ils commercer avec le Brexit de l’Afrique de l’Ouest ?

En tant qu’investisseur cherchant à négocier le Brexit de l’Afrique de l’Ouest via la BRVM, plusieurs stratégies peuvent être adoptées.

Une façon est d’analyser la performance boursière des entreprises cotées à la BRVM qui ont une exposition significative au Niger, au Burkina Faso et au Mali (telles que la Banque de l’Afrique et Onatel), en particulier celles opérant dans des secteurs susceptibles d’être affectés par les changements géopolitiques, tels que l’agriculture, l’exploitation minière et les infrastructures.

Les investisseurs peuvent également surveiller les fluctuations des devises, car le retrait de la CEDEAO pourrait avoir un impact sur les taux de change et influencer par conséquent les prix des actions.

De plus, rester informé des développements politiques et des changements de politique dans la région est crucial pour prendre des décisions d’investissement éclairées.

Enfin, les investisseurs peuvent diversifier leurs portefeuilles en envisageant des actifs autres que les actions, tels que des obligations ou des fonds négociés en bourse (ETF), qui peuvent offrir des opportunités alternatives pour tirer parti des mouvements de marché résultant du Brexit de l’Afrique de l’Ouest.

Restez en avance sur la courbe avec nos ressources et outils complets conçus pour aider les investisseurs à capitaliser sur les opportunités émergentes au milieu des changements géopolitiques en Afrique de l’Ouest. Visitez notre site web ou téléchargez l’application dès maintenant !

A political quake struck West Africa last month, as three nations ruled by military juntas announced their withdrawal from the Economic Community of West African States (ECOWAS) regional bloc.

Niger, Mali, and Burkina Faso accused ECOWAS of failing to support them against jihadist violence and excessive foreign influence, before quitting the organization late January.

The abrupt departure has prompted comparisons to “Brexit” (the withdrawal of the United Kingdom (UK) from the European Union), marking a historic rupture after decades of building economic and political ties between the 15 member states.

As the aftershocks reverberate across the region, here is everything you need to know about this crisis and its far-reaching implications for trade, security, and the lives of millions in West Africa.

What is ECOWAS?

Founded in 1975, the Economic Community of West African States (ECOWAS) comprises 15 nations in the region.

ECOWAS aims to foster regional cooperation and trade, facilitating visa-free travel to uplift the living standards of its people and ensure economic stability.

It also plays a crucial role in peacekeeping efforts in a volatile part of the continent and is a significant security ally to the West, including the United States.

The leadership of the bloc rotates among its member countries, with Nigeria, the economic powerhouse of the region, currently in charge.

ECOWAS Member States

Why did Burkina Faso, Mali and Niger quit ECOWAS?

In recent years, Burkina Faso, Mali, and Niger have been overwhelmed by jihadist insurgencies and political instability, undergoing multiple coups.

Mali endured two coups, one in 2020 and another in 2021. Burkina Faso faced two coups within a year in 2022. Lastly, Niger experienced a coup last summer.

ECOWAS responded by suspending the countries and imposing tough sanctions. This led to growing resentment and defiance from the military juntas now ruling these nations.

They accuse ECOWAS of failing to provide support against terrorism and of being influenced by “foreign powers” like France.

Don’t miss out on capitalizing on the changing dynamics in West Africa. Get the Daba app now for timely alerts and personalized recommendations to optimize your investment portfolio.

Niger, Mali, and Burkina Faso accuse ECOWAS of failing to support them against jihadist violence and excessive foreign influence.

How has the region responded to the decision?

ECOWAS has expressed sadness at the decision. Nigeria, the current ECOWAS chair, said the “unelected” junta leaders are letting their people down but remain open to engagement.

Analysts warn that sanctions have backfired, fueling anti-French sentiment and closer ties with Russia. Threatening military intervention against Niger rallied citizens to support the coup.

The tough stance has undermined ECOWAS’s credibility but also underscores instability as armies seize power across the region.

Nigeria President and Chairperson of ECOWAS, Bola Ahmed Tinubu.

How will leaving ECOWAS affect the countries?

The decision could severely harm the poor, landlocked Sahel nations who heavily rely on cross-border trade.

Niger shares 1,500 km of border with Nigeria and 80% of its trade is done with its richer neighbor.

The border closure by Nigeria following the military takeover that overthrew President Mohammed Bazoum puts trade worth about $226 million and lives at risk, per multiple reports.

For all the junta-led countries, losing access to the $702 billion ECOWAS market could lead to shortages, higher prices, increased tariffs, and financial restrictions.

As citizens face more economic hardship, pressure may mount on fragile junta regimes struggling to contain violence.

The region’s trade and services flows, worth nearly $150 billion a year, will be disrupted.

It also raises uncertainty around the large diaspora populations from Burkina Faso, Mali, and Niger living across West Africa. Ghana, Togo, and Benin also have a big diaspora from Niger.

For example, Ivory Coast hosts over 5 million migrants from these nations.

In a worst-case scenario, the bloc’s collapse could trigger a mass exodus.

ECOWAS has faced criticism for swiftly sanctioning the military juntas after years of inaction against civilian leaders who prolonged their rule through questionable elections or referendums in nations like Ivory Coast and Guinea.

This double standard has reduced ECOWAS’s credibility. Additionally, though ECOWAS has threatened military intervention, its failure to follow through on those threats has further weakened its standing.

Interested in navigating the West Africa Brexit and maximizing your investment opportunities? Explore our platform to thrive in this evolving market landscape.

Niger shares 1,500 km of border with Nigeria and 80% of its trade is done with its richer neighbor.

For a long time, security experts have urged regional countries to enhance cooperation and intelligence-sharing to address the spreading insurgencies fueled by poverty, neglect, abuse, and ideology.

However, the current crisis at ECOWAS highlights the growing divide between democratically elected governments allied with the West and military-ruled states increasingly reliant on Russia and China for support. This schism thwarts a coordinated regional response to rising insecurity and insurgencies.

Moving forward, ECOWAS must bridge this divide and boost collaboration between member states to tackle shared challenges.

How can investors trade the West Africa Brexit?

As an investor looking to trade the West African Brexit via the BRVM, there are several strategies you can adopt.

One way is to analyze the stock performance of companies listed on the BRVM that have significant exposure to Niger, Burkina Faso, and Mali (such as Bank of Africa and Onatel), particularly those operating in sectors likely to be affected by geopolitical changes, such as agriculture, mining, and infrastructure.

Investors can also monitor currency fluctuations, as the withdrawal from ECOWAS could impact exchange rates and consequently influence stock prices. Additionally, staying abreast of political developments and policy changes within the region is crucial for making informed investment decisions.

Finally, investors can diversify their portfolios by considering assets beyond equities, such as bonds or exchange-traded funds (ETFs), which may provide alternative opportunities to capitalize on market movements resulting from the West Africa Brexit.

Stay ahead of the curve with our comprehensive resources and tools designed to help investors capitalize on emerging opportunities amidst geopolitical shifts in West Africa. Visit our website or download the app now!

Despite contributing only 3.8% of global greenhouse gas emissions, Africa faces the brunt of climate change’s wrath. Emerging VC-backed innovators aim to change the continent’s fortunes.

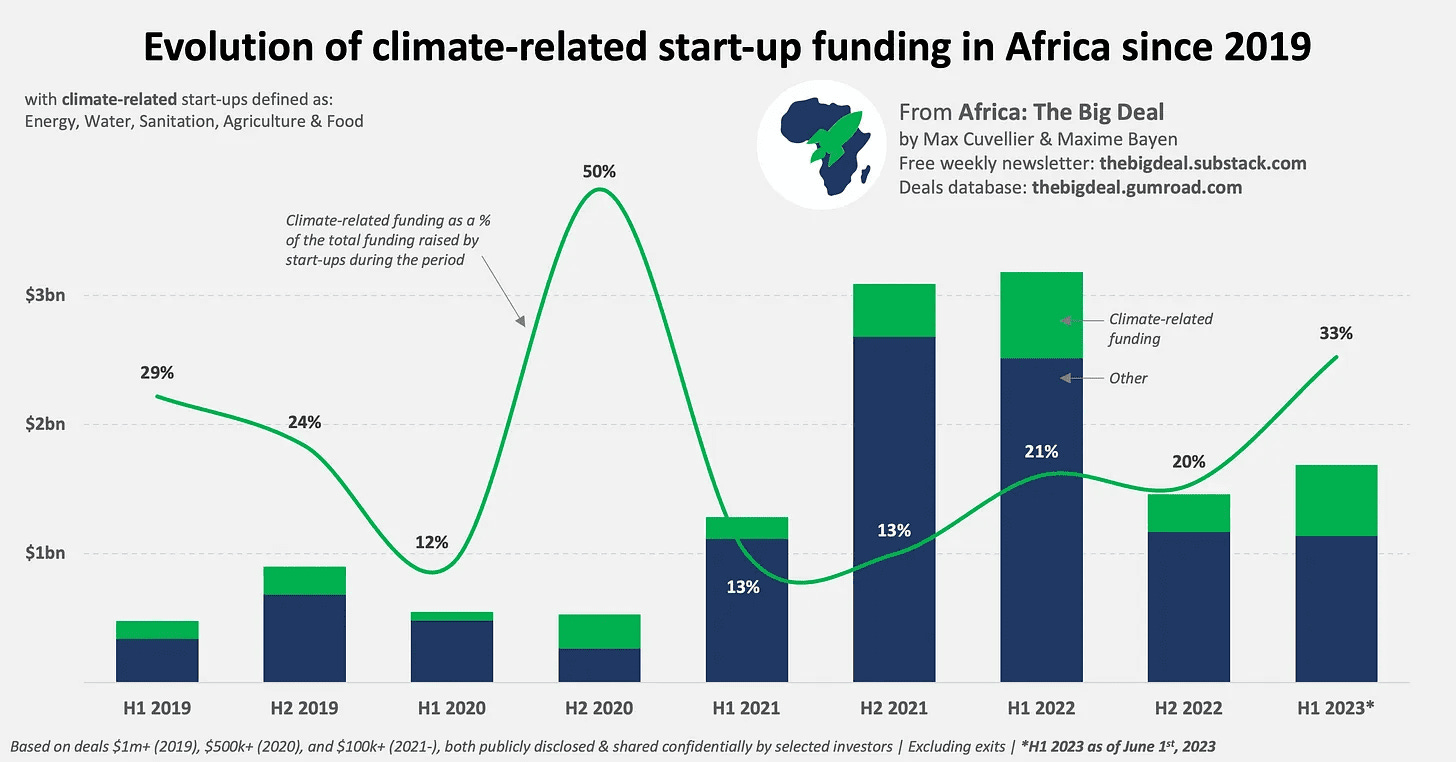

In 2022, climate-tech funding in Africa grew 3.5x to over $860m, making climate Africa’s most funded sector after fintech.

The funding was largely driven by clean energy technologies.

Broadly, the cleantech sector attracted the most foreign direct investment (FDI) flows into Africa, per the Africa Attractiveness Report by global consulting giant EY. (You can read our summary of the report here)

The timing of this surge in climate funding couldn’t be better.

Climate change comes to Africa

The scorching heat waves, drying water sources, and erratic weather patterns are no longer distant nightmares for Africa.

Climate change is here, and its impact is undeniable.

Despite contributing only 3.8% of global greenhouse gas emissions, Africa faces the brunt of climate change’s wrath.

For comparison, China, the United States, and the European Union account for 23%, 19%, and 13% respectively.

Yet in 2019, five of the ten countries most affected were African nations, bearing the consequences of devastating weather disasters.

Mozambique, Zimbabwe, Malawi, South Sudan, and Niger faced devastating weather disasters like Cyclone Idai, fueled by scorching temperatures that heated the Indian Ocean and led to heavy rainfall and flooding.

At least five countries in Africa were devastated by Cyclone Idai, one of the continent’s worst natural disasters on record.

In East Africa though, rising temperatures have disrupted the traditional rain patterns that make Ethiopia, Northern Kenya, and Somalia green.

The year 2022 marked a record fifth rainless season in a row, leading to severe drought and hunger for millions in the Horn of Africa, where the United Nations estimates that around 13m people are dealing with severe hunger.

By 2050, the continent’s iconic glaciers on Mount Kilimanjaro, Mount Kenya, and the Ruwenzori Mountains will vanish, a stark reminder of the warming planet.

But Africa isn’t sitting idly by.

The continent hosted its first-ever Africa Climate Change Summit in September, culminating in the historic “Nairobi Declaration.”

This declaration saw African leaders commit to combat climate change through increased investments, a carbon tax, and sustainable development goals.

However, the fight requires more than just declarations.

This is where climate-focused tech startups take center stage.

Africa’s first-ever Climate Change summit in Nairobi saw leaders commit to combating climate change through increased investments, a carbon tax, and SDGs.

African innovators to the rescue

Over 500 startups have emerged across Africa in the last 15 years, offering innovative solutions in agriculture, clean energy, sustainable materials, e-mobility, and nature-based solutions, per a 2022 report by Briter Bridges.

In Ethiopia, for instance, a booming urban population and single-use plastic have seen waste generation skyrocket from 9,700 tonnes/day in 2015 to 12,200 tonnes/day in 2020.

This trend is fueling environmental and health woes and projections warn this figure could double by 2030.

This is because of how building materials are produced, what materials are used, and the properties’ energy efficiency once they’re up and running.

Kubik’s mission is to build clean and affordable living for all, solving Africa’s housing and waste crises simultaneously.

Its solution boasts several advantages:

Cost-effective: Significantly cheaper than conventional materials

Time-saving: Constructions are twice as fast as traditional methods

Eco-friendly: Over 5 times less polluting than cement

In a recent oversubscribed seed round, Kubik secured $3.34 million to fuel its growth and expand its reach.

This investment affirms the potential of Kubik’s solution to tackle waste, improve housing, and protect the environment.

Buildings account for 40% of total global carbon emissions. Kubik’s mission is to build clean and affordable living for all.

A look at the types of solutions that populate the climate sector reveals that agriculture and energy—specifically pay-as-you-go solar scale-ups—dominate.

However, the space is getting broader with startups addressing a range of issues.

Here are some other startups leading the charge:

Coliba: Specializing in the collection and recycling of plastic waste, which is converted into granules and then resold to various industries.

Amini: Bridging the environmental data gap with AI-powered sensors that monitor air quality and water resources.

Figorr: Tackling food waste through its AI-powered platform that connects farmers with buyers for unsold produce.

Powerstove: Providing clean and efficient cookstoves that reduce reliance on firewood and improve health.

Daystar Solar: Bringing affordable solar power to off-grid communities, empowering households and businesses.

PEG Africa: Offering pay-as-you-go solar home systems, reaching over 1m customers across Ghana, Senegal, Mali, and Ivory Coast.

M-Kopa: Another Kenyan champion, providing clean energy solutions to off-grid communities through its pay-as-you-go model.

Solar Freeze: Empowering smallholder farmers with off-grid solar-powered refrigeration to preserve their produce.

BasiGo: An electric bus company leasing vehicles to bus owners on a pay-as-you-drive model, facilitating the transition to clean mobility without high upfront costs.

The rise of these startups is fueled by a surge in investor backing.

Out of the 500 identified climate-tech startups on the continent, 147 have secured funding since 2015.

More so, at least 230 deals over $1m have been signed in the climate-tech space since 2019, just over 20% of all the deals signed in Africa.

Around 73% of this funding went to energy startups.

Image credit: The Big Deal

This trend is set to be further bolstered by the launch of new climate-tech funds over the past year—despite the global VC funding cooldown.

Some of these include…

Pan-African venture firm Novastar’s $200m Africa People + Planet fund for startups developing agriculture and climate solutions.

VC firm Equator’s $40m fundraising to back seed and Series A startups in energy, agriculture, and mobility.

Catalyst Fund’s new climate-focused $30m fund, now investing in its first cohort of startups.

Satgana, a new climate tech firm launched in late 2022, with plans to allocate up to 40% of its funds to “planet-positive” startups in Africa.

There’s the $250m AfricaGoGreen Fund (AAGF), which closed the second tranche of its fundraising in February and counts pay-as-you-go solar providers BBOXX and Solarise as part of its portfolio.

Also, the Energy Entrepreneurs Growth Fund (EEGF), backed by Shell and Canadian investor FinDev, raised $110m for startups that increase access to clean and reliable energy for African households and businesses.

E3 Capital (formerly Energy Access Ventures)’s Low Carbon Economy Fund for Africa (E3LCEF), hit its first close in May at $48m.

Oxfam Novib and Goodwell also recently launched a new $22m Pepea fund to provide venture debt to startups in this space.

Climate venture builder, Persistent Energy, recently closed a $10m Series C funding round to strengthen its team and scale climate activities in Africa.

Also, the Climate Investment Funds (CIF), implemented by the AfDB, has supported the development of 39 investment plans across 27 African countries to unlock climate action.

PEG Africa offers pay-as-you-go solar home systems, reaching over 1m customers across Ghana, Senegal, Mali, and Ivory Coast.

These dedicated funds show a sustained commitment to supporting climate-tech innovation in Africa.

While the funding landscape is promising, challenges remain.

Additionally, the low number of exits (10, all in energy) indicates a long road ahead for commercial capital to enter at scale.

M-Kopa provides clean energy solutions to off-grid communities through a pay-as-you-go model.

Still, the momentum is undeniable.

Climate-related startups in Africa have raised $3.4bn between 2019-2023, nearly 60% of the total funding volume invested in the much more mature fintech sector.

That, coupled with the emergence of innovative solutions and government-backed initiatives, demonstrates a commitment to tackling climate challenges.

Africa is not just facing the brunt of climate change; it is also becoming a breeding ground for innovative solutions that can inspire the world.

Le Sénégal s’apprête à émettre une obligation du Trésor de 200 milliards de francs CFA (330 millions de dollars) en trois tranches ce mois-ci, suscitant un intérêt significatif des investisseurs.

Avec le pays d’Afrique de l’Ouest affichant l’une des économies à croissance rapide du continent africain, les investisseurs ont de bonnes raisons d’être enthousiastes.

Le Sénégal s’est établi comme un modèle de stabilité politique en Afrique de l’Ouest. Le pays a connu des transitions pacifiques du pouvoir depuis son indépendance en 1960.

Récemment, le président Macky Sall a annoncé qu’il ne chercherait pas un troisième mandat aux élections de 2024, apaisant les tensions politiques antérieures.

Le pays s’est également affirmé comme un participant fréquent et fiable sur le marché financier de l’Union économique et monétaire ouest-africaine (UEMOA). En 2023 seul, le gouvernement sénégalais a réalisé 44 émissions d’obligations sur cette plateforme.

Dakar, Senegal

Les agences mondiales de notation de crédit Standard & Poor’s et Moody’s ont classé le Sénégal respectivement aux niveaux d’investissement B+ et Ba3, soulignant l’amélioration de la solvabilité du pays.

Le FMI prévoit également que le Sénégal, déjà deuxième économie de l’UEMOA, enregistrera le deuxième taux de croissance économique le plus élevé en Afrique cette année et le cinquième au monde.

2. Flux de revenus réguliers

Comme la plupart des obligations gouvernementales, l’offre du Sénégal fournira aux investisseurs des paiements d’intérêts réguliers tout au long de la durée de vie de l’obligation, assurant un flux de revenus régulier.

La tranche de 5 ans offre un coupon de 6,25 %, la tranche de 7 ans offre 6,45 %, et la tranche de 10 ans offre 6,65 %, offrant aux investisseurs un flux de revenus semi-annuel robuste et stable, assurant des rendements attrayants surtout compte tenu des tendances actuelles des taux mondiaux.

3. Faible risque de défaut

Soutenues par un gouvernement souverain, les obligations souveraines comme celles du Sénégal présentent un risque de défaut extrêmement faible par rapport aux titres d’entreprises.

Alors que les obligations d’entreprises offrent des rendements attractifs, elles dépendent uniquement de la santé financière de l’entreprise émettrice. Le Sénégal n’a jamais fait défaut sur ses obligations.

Les investisseurs peuvent compter sur le gouvernement pour respecter ses paiements d’intérêts promis et le remboursement du principal.

President Macky Sall

4. Avantages fiscaux

Les investisseurs résidents bénéficieront d’une exonération d’impôts sur les paiements d’intérêts et le remboursement du principal. Cette combinaison de rendements attrayants sans imposition rend les obligations sénégalaises attrayantes en tant que proposition de revenus fixes.

Pour les investisseurs étrangers, les revenus sont soumis aux régimes fiscaux nationaux applicables.

5. Liquidité et accessibilité

Les obligations souveraines ont tendance à être plus activement négociées en raison de volumes d’émission plus importants, assurant une liquidité saine pour les investisseurs.

Les obligations peuvent être achetées directement auprès du gouvernement ou via des plateformes d’investissement en ligne telles que Daba.

Elles seront négociées sur la Bourse Régionale des Valeurs Mobilières (BRVM) de l’Afrique de l’Ouest francophone, assurant une liquidité pour les investisseurs.

Le gouvernement se réserve le droit de racheter des obligations sur le marché ouvert, permettant aux investisseurs de vendre facilement leurs avoirs.

L’obligation sénégalaise sera négociée sur la BRVM, fournissant une liquidité pour les investisseurs.

Les investisseurs peuvent également acheter facilement des obligations sénégalaises par le biais de courtiers ou de fonds communs de placement sans participer directement aux enchères. La possibilité de retirer relativement facilement des investissements avant l’échéance offre une flexibilité supplémentaire.

Avec les perspectives de croissance économique solides du Sénégal et son profil de crédit, combinés à la fiabilité et aux avantages d’une obligation souveraine, les investisseurs peuvent s’exposer à l’une des économies phares de l’Afrique tout en obtenant un rendement attractif et sans risque sur leur capital.

Pour plus de contenu sur les tendances et opportunités d’investissement, consultez l’application Daba dès aujourd’hui !

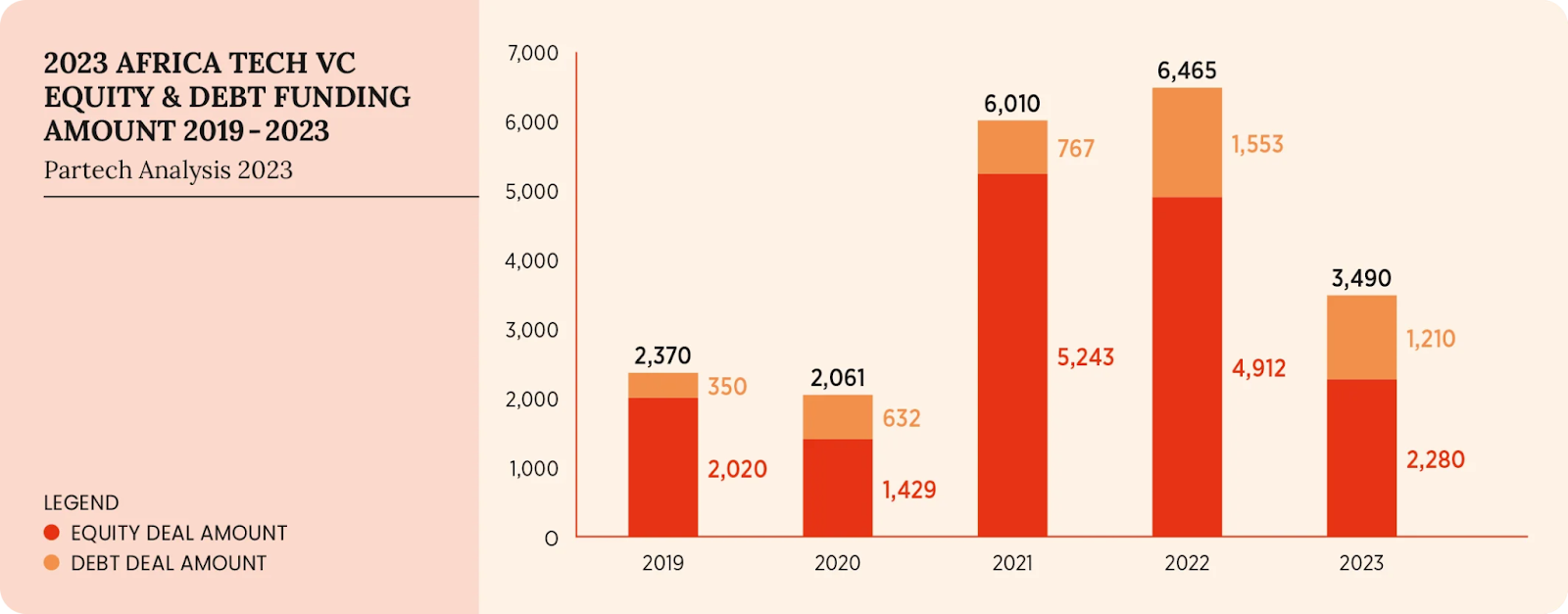

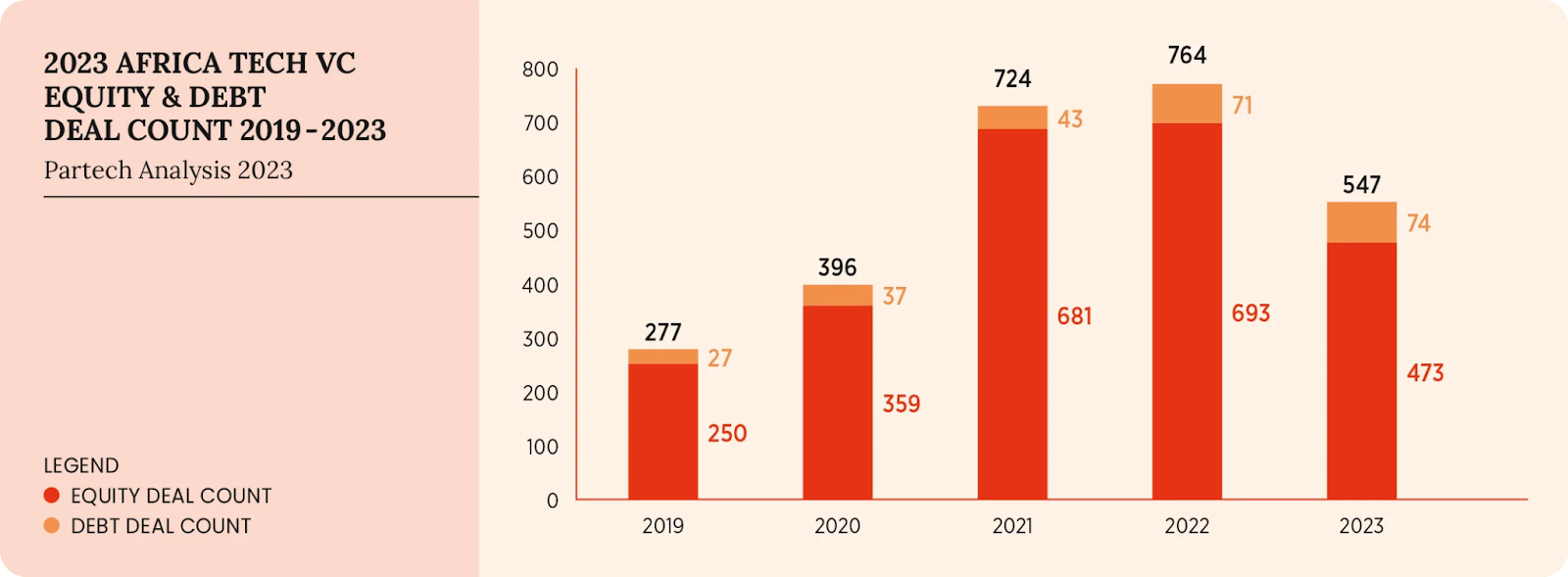

Le rapport annuel de Partech sur le capital-risque technologique en Afrique offre des perspectives précieuses sur l’évolution de l’écosystème technologique africain.

L’édition 2023 révèle un ralentissement significatif du financement, en accord avec les tendances mondiales du capital-risque, mais met en lumière des zones de résilience.

Voici les principales conclusions.

Diminution de moitié du financement reflète la conjoncture mondiale

En 2023, les start-ups africaines ont levé 3,5 milliards de dollars, soit une baisse annuelle de 46 %, répartie sur 547 transactions (-28 %). Les fonds propres ont spécifiquement enregistré une diminution de financement de 50 %.

Cela reflète la crise mondiale du financement du capital-risque alors que les investisseurs devenaient plus prudents. Cependant, l’Afrique a toujours attiré plus de 500 investisseurs, démontrant un intérêt continu et fort.

Baisse observée à tous les stades de financement

Le rapport montre des baisses à tous les stades de financement, la plus importante étant dans les tours de croissance (-31 % en moyenne). Les tours d’amorçage et de série A ont diminué modérément (8 à 16 %), tandis que la série B est restée stable.

Cela indique que les investisseurs se sont concentrés sur le soutien aux entreprises existantes de leur portefeuille plutôt que sur de nouveaux investissements.

Les 4 principaux marchés restent en tête, avec des changements

Les quatre principaux marchés africains – l’Afrique du Sud, le Nigeria, l’Égypte et le Kenya – dominent toujours, sécurisant 79 % des transactions. Cependant, leur part de transactions a légèrement diminué (passant de 77 %), signalant une activité croissante sur tout le continent.

L’Afrique du Sud a pris la première place en termes de fonds propres levés avec 548 millions de dollars. Cependant, le Kenya a capturé la première place pour le financement global avec 719 millions de dollars grâce à un financement important par la dette. Ainsi, ces deux nations sont actuellement en tête du financement technologique en Afrique.

Le Nigeria est resté en première position en termes de nombre de transactions, malgré une division par deux de son financement en fonds propres. Pendant ce temps, l’Égypte a subi le plus gros impact parmi les quatre premiers, avec une chute de 58 % des transactions en fonds propres.

Montée du francophone

Encourageant, 52 % des pays africains ont bénéficié d’investissements technologiques, contre 46 % en 2022. L’Afrique francophone a connu une croissance substantielle, représentant 15 % des fonds propres (contre 11 %) dans 20 % des transactions. Cela indique une attention renforcée du capital-risque au-delà des quatre principaux hubs technologiques.

La Fintech conserve la couronne du financement

Comme les années précédentes, la fintech s’est classée première tant en nombre de transactions (113) qu’en financement total des fonds propres (852 millions de dollars).

Le commerce électronique et les technologies propres se sont classés à égalité en deuxième position avec des parts de 13 % chacun. La domination de la fintech montre le besoin immense de l’Afrique en matière d’inclusion financière et de solutions de paiement.

La croissance du financement pour les fondatrices

Les start-ups fondées par des femmes ont levé 25 % des transactions en fonds propres, soit une augmentation de 3 points de pourcentage par rapport à 2022. Elles ont également obtenu 392 millions de dollars en fonds propres, représentant 17 % du total des fonds propres, contre 13 % l’année précédente. Bien que cela reste faible par rapport à la population, le soutien du capital-risque aux femmes leaders technologiques a gagné du terrain de manière significative.

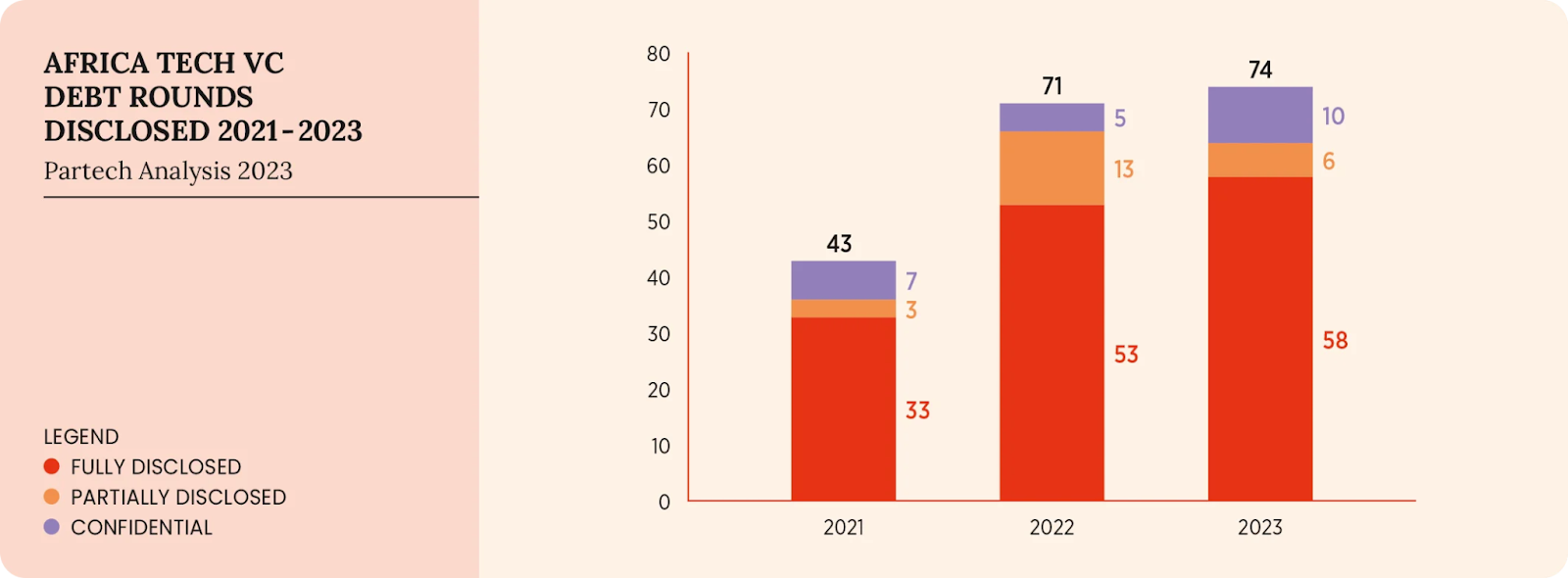

La dette émerge comme un complément aux fonds propres

Le rapport met en avant la pertinence croissante de la dette, représentant 35 % du financement total contre seulement 24 % en 2022. Le Kenya a été en tête du financement par la dette avec une part de 32 %, axée principalement sur les entreprises de technologies propres et de fintech.

Alors que les fonds propres se resserrent, la dette offre une alternative de capital viable pour les start-ups africaines en maturation.

En résumé, bien que l’environnement de financement technologique en Afrique soit devenu nettement plus difficile en 2023, le secteur semble résister à la tempête.

Les acteurs clés ont maintenu des niveaux de financement respectables compte tenu du contexte, les investisseurs ont continué à soutenir un éventail de marchés et de fondateurs, et la dette a contribué à atténuer le ralentissement des fonds propres.

Le rapport de Partech suggère un optimisme prudent quant au retour de la croissance technologique en Afrique après la crise. Des métriques clés telles que le nombre de transactions et le financement des femmes soulignent l’élan sous-jacent de l’industrie.

Vous souhaitez en savoir plus sur les tendances en matière d’investissement et accéder aux opportunités en Afrique ? Téléchargez l’application Daba depuis vos magasins d’applications dès aujourd’hui !