Contributed by Kyle Schutter, a Partner at Grant & Co.

To go public, or not…

I attended the Ibuka accelerator, a program to help get private companies listed, kickoff event in October at the Nairobi Securities Exchange.

The Kenyan stock exchange, being the largest in the region, is worth a close look.

The requirements for listing in Nairobi are minimal and it is not nearly as hard to list as people make it out to be. A company needs only 1 year of track record, doesn’t need to be profitable, only needs to list 15% of its shares, only needs a capitalization of about $100,000, and only needs to have 25 shareholders within a few months of listing.

So why aren’t more companies doing it?

The Lagos, Johannesburg, Mauritius, and Nairobi stock exchanges are the most promising places to go public in Africa. We will focus on the Nairobi Securities Exchange as a case study to enable us to deep dive.

Note: nothing here should be construed as an insult to Africa, Kenya, or the Nairobi Securities Exchange. I love Kenya and hope to work together to find solutions that keep increasing investment in and wealth of Africa.

Brand Problem

Listing is only one part of the problem; you must have someone buy your shares. Is there a market that wants to buy shares in these particular companies?

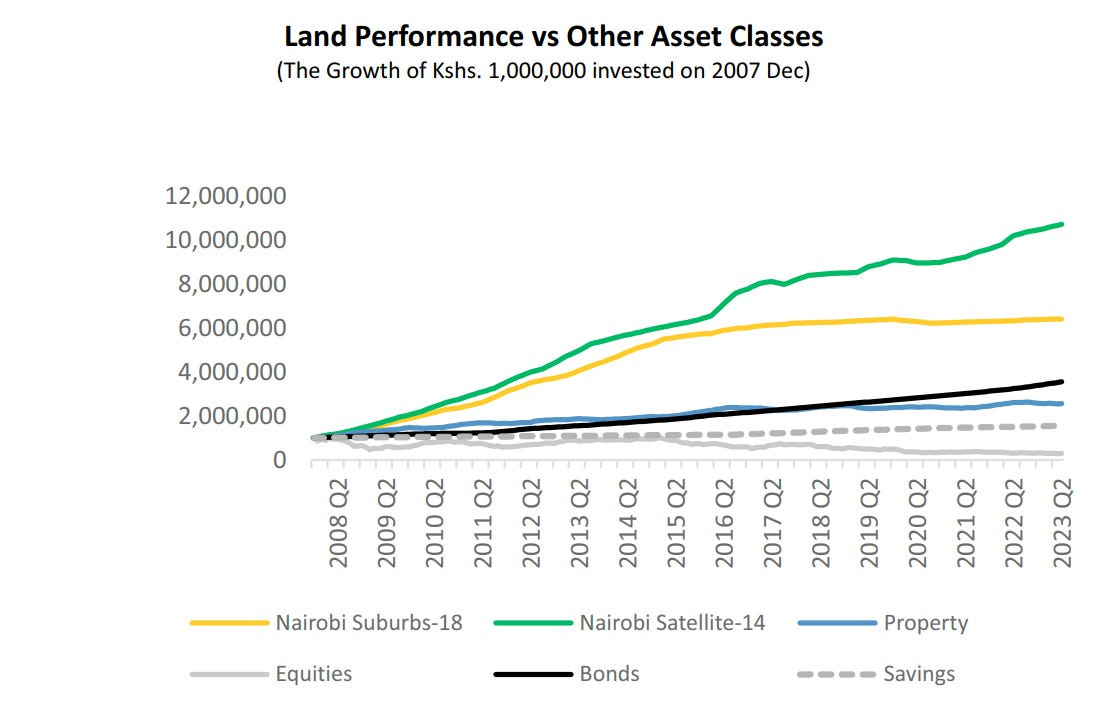

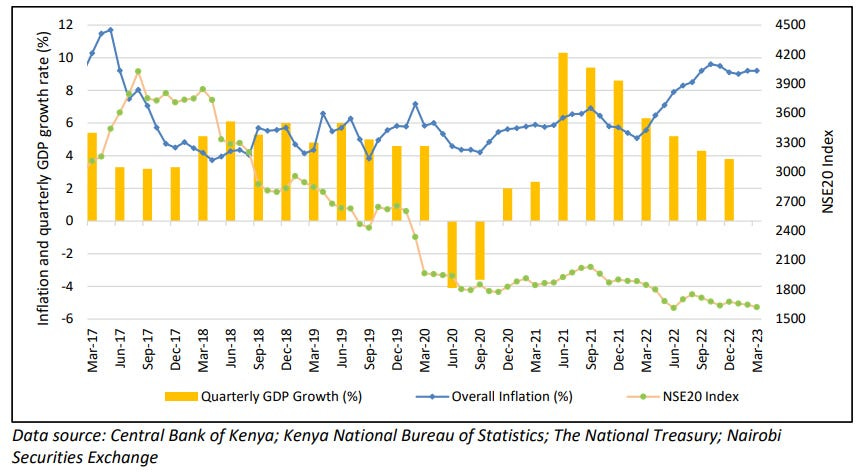

Kenyan equities (stocks) have not performed well, underperforming against bonds land, and even savings accounts. This isn’t a recent phenomenon, although the current economic downturn has worsened it. It has been going down for 8 years.

The NSE 20 index is down from 6,000 in 2015 to 1,400 in 2023.

Why take more risk with equities and get a lower return?

So, the brand name of Equities in Kenya and Africa is generally not good. What factors lead to this, and how can it be fixed?

Remember, Investing is a Keynesian Beauty Contest: the goal is not to pick the most beautiful investment but to pick the one that others think is the best. If Kenyan Equities have a bad brand and investors don’t think others will pick them, then no one will pick them, and they will go down.

Too hard to list… or too easy?

The requirements of the NSE (Nairobi Securities Exchange) are very entrepreneur-friendly, probably too friendly. There are two ways exchanges should maintain quality: ethics and financial performance. The NSE could improve on both accounts.

Ethics: the NSE has frozen the shares of Mumias and Kenya Airways, which prevents shareholders from liquidating their shares and props up the companies so they can keep operating rather than declare bankruptcy.

Financial Performance: Other stock exchanges delist companies if their share price or market capitalization falls too low. The electric scooter startup, Bird, once valued at $3.2b has now been delisted from NYSE because it failed to maintain the $15m market cap minimum threshold and has since gone bankrupt. Stocks that fall below $1.00 per share on the NYSE are also delisted. NSE could also set a minimum price to encourage management to improve performance or face the consequences of being delisted.

A leadership problem?

The Ibuka event had an enthusiastic vibe but maintained certain unfortunate* African stereotypes: the event started 1 hour late, and the presentation contained a major data inaccuracy. Timeliness and data integrity must be core to the culture of a stock exchange. *I likely maintained certain American stereotypes at the event: incessant, obnoxious questions. C’est le vie.

This suggests room for improvement in the NSE company culture and, consequently, for leadership improvement. According to publicly available information, the outgoing CEO of the NSE made Ksh31m (~$210,000), a 19% increase over the previous year, all while making only Ksh14m (~$100,000) for the exchange in profit, a drop of 90% from the previous year. This suggests a problem with his compensation package (and the compensation structuring at the NSE).

Overall, the NSE Equities market has been down since the NSE CEO was appointed 9 years ago, while the Kenyan economy has grown at ~5% a year. Having met him briefly, I had the impression the CEO of the NSE was more of a politician than a visionary who made things happen. Subsequent conversations with market players have not changed that impression.

A new CEO has been appointed as the current CEO has ended his two 4 year terms. Hopefully, new leadership will improve the company culture and results. But this 4-year term suggests more room for improvement: why not have the CEO’s tenure be based on performance? Stock exchanges like NYSE don’t have specific terms for their CEOs. But, perhaps the NSE is a quasi-parastatal. And with the “prestige” associated with running a public market there is a risk that new appointees will be based more on politics than competence and compensation will not be tied to results.

Furthermore, 8 years isn’t enough time to turn something around. A true visionary would want 15 good years to build something great. Imagine Steve Jobs had to leave Apple in 2005 before the iPhone came out. Or Elon had to leave before the Model S came out? The 2×4-year term could be disposed of.

The newly appointed CEO looks to be a strong choice. He is a lawyer/accountant and Partner from EY. We were hoping for an entrepreneur. Hopefully, he will be an entrepreneurial lawyer/accountant.

Capital flight?

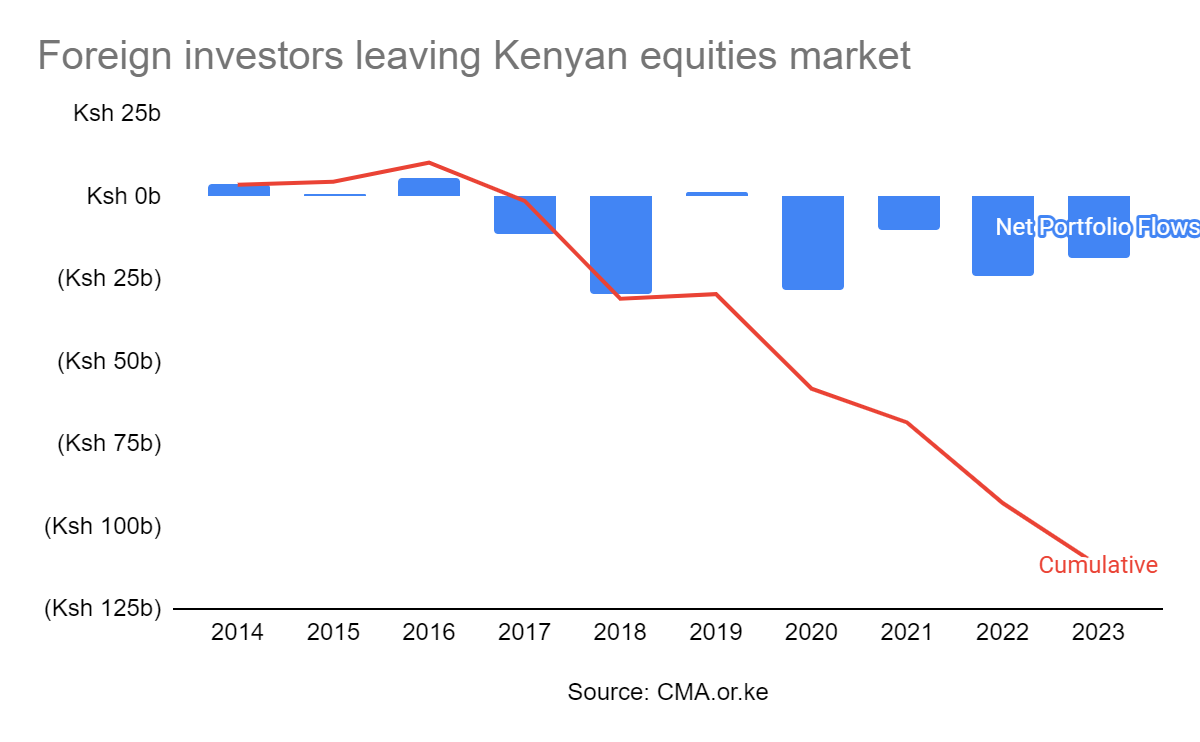

Another explanation for poor NSE performance is that foreign investors are leaving the African stock markets, especially the Kenyan stock market.

However, the Ksh 125b loss due to foreign investors leaving is only part of why the NSE has lost Ksh 1.5 trillion in value since 2021. Capital flight explains less than 10% of the story.

Anti-Free Market behavior

Here are two examples:

- The NSE has frozen the trading of Kenya Airlines and Mumias, both of which have substantial government ownership. Kenya Airlines shares have been frozen for 4 years, renewed annually each year with the explanation that Kenya Airways needed time to restructure. In 2022, Kenya Airways lost about $40m. In 2023, they lost about $150m. The more time they get to restructure, the worse it gets. Both companies should go bankrupt, and shareholders should be able to sell their shares. The exchange freezing shares makes investors nervous. By comparison, the NYSE only froze trading for 1 day, and that was when the World Trade Center buildings were attacked in 2001.

- That the CEO of the CMA has attempted to put price floors on stock prices is concerning. “Capital Markets Authority (CMA) chief executive Wycliff Shamia told the Star that the move has been necessitated by the fact some of the companies have very strong fundamentals but the valuation is quite low.” Yes, this is how free markets work. The market decides what something is worth, not the government. The latter would be communism.

Preference for other investments

Investors would rather speculate on land because Kenya has no property tax. GoK should fairly tax other parts of the economy, like creating a 0.1 to 1% annual Property Tax on land so that people can’t just sit on their land and speculate without contributing to the economy. All other developed and emerging economies have an annual Property Tax; it’s time Kenya did the same. Property tax is generally recognized as the least bad tax for economic growth and yet Kenya doesn’t have it and isn’t even considering it. See here how property tax could be implemented in Kenya and make all parties happy. With the devolved county governments, this could more easily be accomplished than in the past.

The effect of no property tax is clear in the numbers: Kenyan real estate is 75x bigger than equities ($678b vs $9b); meanwhile, by comparison, US real estate is only 2x bigger than US equities ($96T vs $46T). The US equities market sources capital from around the world because people trust Uncle Sam to treat equities fairly, but people don’t (yet) trust Uncle Kamau to do the same. I think the lack of Property Tax is the nail in the coffin of the NSE, and without this reform, there can be no vibrant equities market. (Note: the only meaningful property tax that exists is the capital gains tax when a property is sold, and even then, people can easily underreport the sale price, which is much harder to do on a public equities market. Some counties like Nairobi charge property tax at around $5-30 per year, which is a joke. There is also a tax on Rental payments, but this is not a tax on the property but a tax on a business being done on the property, making matters worse by disincentivizing property development.)

Because Treasury Bonds are over 15%, investors put their money there rather than risk equities. Hopefully, after the Eurobond payment in June 2024, Treasury yields will reduce and more money will flow back to the equities market.

The opportunity

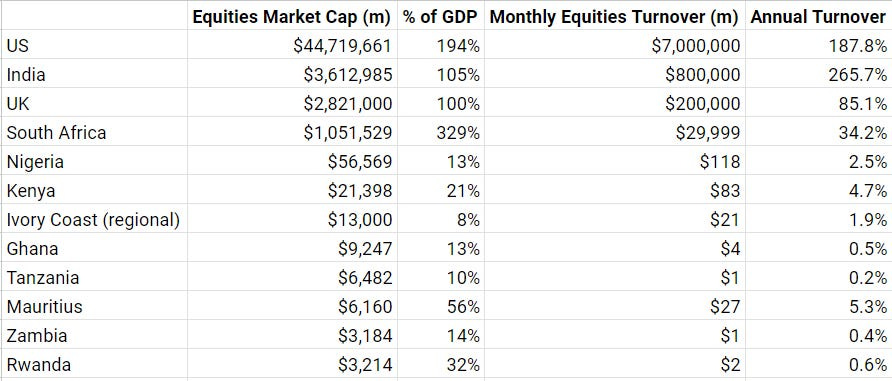

But there are reasons to be bullish on African stock markets. African markets, excluding South Africa, have a relatively small proportion of their GDP trading. There is room for the equities market to grow 10x to align with other markets like the US, South Africa, and India.

Further, Kenya is the region’s largest and most liquid market and could be a regional player—it is already one of the most liquid markets in Africa. By aggregating regional companies onto its exchange, NSE could grow another 10x. On top of that, GDP will compound to 63% growth over the next 10 years. This brings the total NSE market cap potential to ~630x growth over the next 10 years… if NSE can play its cards right. 630x growth would put the NSE in line with India, so it’s not impossible, as discussed below.

On top of that, Annual Turnover (trading of the shares) is relatively low compared to other markets at 4.7% on NSE, ~40x less trading than the US, adjusted for market cap.

There is room for more economic activity on African stock markets.

So where is this 630x growth going to come from?

- Increase valuation. The P/E (price to earnings) ratio is only 4.9 on NSE, a sign that investors have low growth expectations. This is half its historical level and 1/4th the ~20 P/E seen on US exchanges, a 4x growth potential for NSE stocks. This is due to uncertainty, low expectations, and discounting for inflation.

- More companies listing. About 1% of US companies are publicly listed compared to 0.001%ish (my guesstimate) of Kenyan companies. Realistically, 10x growth potential (as most Kenyan businesses are too small to go public).

- NSE quality. If the NSE can improve quality that will improve investor confidence and 2-10x growth.

- Virtuous Cycle. There are the compounding effects of a growing market, generating interest and crowding in more capital.

- Encourage international investors on local trading platforms. Currently, American, Canadian, Singaporean, and other foreign investors are discouraged from investing through existing brokerage channels and online trading platforms as the regulations in those countries are too costly to manage given the small public market. But as the market grows and trading platforms enable more foreign investors you can imagine that as returns are becoming more predictable with lower returns in the West, some intrepid investors will take an interest in Africa. 2x opportunity

- Distribution on international trading platforms. Like Robinhood, Charles Schwab, etc. 10x opportunity.

- Cross-listing from other countries in East, Central, and Southern Africa. Theoretically, a 10x opportunity, but in reality, maybe a 2x. Already, some of this is happening. Bank of Kigali (Rwanda) and Umeme (Uganda) are listed in their own countries but cross-listed on NSE. Crosslisting is relatively easy. Evidence suggests that cross-listing increases company valuation, so the cost of cross-listing more than pays for itself. (Source: Peristiani, Federal Reserve Bank of New York, 2010) Old Mutual, for example, is cross-listed on 5 exchanges. A Kenyan equities lawyer confirmed this would be a workable strategy.

- Behavioral nudges. There is no way for Kenyan trading apps to automatically reinvest dividends, while automatic reinvestment of dividends is possible in other markets like the US. This could boost share price by 5% per year. This would cut out stock brokers and their fees. My little research online suggests the CMA (Capital Markets Authority) currently prevents automatic dividend reinvestment due to pressure from stock brokers.

- Better trading UX. New trading apps that make it easy to buy shares can 2x capital yet again. I tried to sign up with 6 different trading apps and brokers. 3 didn’t allow Americans, Dutch, Singaporeans, or Canadians to trade. The others each had cumbersome documentation requirements: one required a scanned copy of a notarized copy of my passport. What’s the point of a copy of something notarized? The friction to buy shares as a foreigner or local is severe.

- Reduced trading fees. This is the big one. CDSC and other government entities can reduce the tax on trading, which is currently at 0.36%. If a stock is only expected to gain 10% a year, paying 0.36% per trade precludes an efficient market that quickly buys and sells. For comparison, the NYSE has a fee on trades of $0.001 (which comes to 0.003% for a typical $30/share stock, 1/100th the price of Kenyan fees). Broker fees are also extremely high in Kenya at 1-1.5%, 10x higher than in the US at 0-0.1%. Reducing fees would not directly increase market cap, but a 10x reduction in fees might increase liquidity 10x, bringing the NSE more in line with other exchanges, from 4.7% turnover to perhaps 50% turnover. Increasing liquidity would perhaps increase the market cap by 2-10x by increasing P/E and crowding in more companies.

- Improving taxation. Right now, US investors in Kenyan companies get taxed twice. Thus, going through Mauritius is advantageous.

Case study 1:

I tried to sign up for various trading apps (Exness, Sterling, AIB-AXYS, ABC). Finally, after a week I was able to sign up on EFG Hermes. I tried to trade using the Market Price but the Market Price was 2x the Limit Price. I was told by customer service to ignore the Market Price. Once I did make a trade it took two days for my trade to be reflected in the app. After many customer service requests, my trade was reflected but then the app showed I had a negative account balance. After another customer service call that has been fixed. Then my password stopped working.

I can see why there might not be a lot of retail investors in Kenyan securities as the buying experience does not inspire confidence. But it does show an opportunity for someone to build a better trading experience.

Why are companies resistant to going public?

Before we determine whether listing at all would benefit companies, let’s consider:

- does going public preclude a company from raising additional institutional capital?

- what are the tax implications?

- what are the compliance costs?

- with interest rates as they are, is now really the right time to list?

Treasuries are 15% in Kenya at the moment, so raising equity is a hard sell. But global interest rates are unlikely to stay high, so perhaps a reduction down to 10% in the coming years will be good for equities. Also, land prices, the other investment option, may run out of room to grow further as rural land prices in Kenya are already about the same as rural land prices in the US, channeling more investment to equities.

Compliance costs are Kenyan SMEs’ most commonly cited problem for not listing. However, the compliance costs in Kenya are typically only around $5,000 a month, which they should be doing even as a private company, like maintaining a board of directors and informing shareholders of material changes. Thus, this argument from SMEs doesn’t hold water.

In an IPO, a company would sell at least 15% of its shares to raise additional capital. Some companies might be concerned with how they can raise more capital after the IPO. Never fear! There are several options:

- Corporate Bond: this is just a loan with a maturity. Of note, there is no collateral required for this. Also, it has a bullet payment at the end, which gives the company some breathing room on repayment.

- Private placement: a select group of investors are invited to buy shares in the company. This can be done even before a public offering and provides more privacy for the company.

- Rights Issue: this is where shares are offered to existing shareholders only so they are not diluted. This funding method is fairly common in Kenya, though not as common in the US.

- Secondary Offering: just like a rights issue but open to anyone. This is common in the US. Tesla, for example, has had 8 Secondary Offerings since 2012.

- All-stock acquisition: not strictly raising capital, but a public company can issue new shares to buy another company without spending cash. For example, Facebook’s acquisitions of WhatsApp and Instagram were mostly paid for in shares. Berkshire Hathaway makes its acquisitions this way, or through retained earnings (reinvested profits) rather than through Secondary Offerings.

Kenya has many advantages over other markets:

- Recently, an app developed for retail investors called Dosikaa (I wrote the first review for it on the Play Store—it didn’t work for me) enables anyone to buy shares. Once Dosikaa works out the bugs, this greatly improves the share-buying UX, instead of going to a broker and signing a paper.

- Kenya doesn’t limit foreign ownership in most companies (aside from banks and telcos) thus, international capital could invest in NSE-listed companies, while other African countries often have more restrictions on foreign ownership.

- Increased liquidity and market capitalization compared to most other African exchanges.

There are also downsides:

- registering a company in Kenya doesn’t have the same tax advantages as Mauritius

- it doesn’t have nearly the same market depth as Johannesburg or other exchanges. Jumia, despite doing most of its business in Egypt, Kenya, and Nigeria, chose to list on the NYSE. JMIA once traded at $60/share but fell 20x. I bought some shares there at $2.5 last week. Let’s see if they can bounce back. Jumia raised more money on the NYSE than it could have on the NSE, but Jumia also might not have lost as much value if it had been listed in an African market. Local buyers in Kenya would have seen the value it creates by direct interaction on the ground. Thus, there are advantages to listing in Africa vs. New York.

One possible tax-efficient structure might be to register the holding company in Mauritius, list it in Mauritius, and then cross-list it to NSE (and other African exchanges) to increase liquidity.

Kenyan stocks have more government and founder ownership than the US; the US has more Retail, ESOP, and ETF (e.g. Index Fund) ownership than Kenya. (Source: CMA and TPC)

Case Study 2:

Flametree, listed on NSE GEMS (the growth board), has an equity value of around $10m, with sales growing about 25% a year. Flametree is a holding company that owns ~15 common spice, shampoo, and water tank brands in Kenya and other African countries. The CEO owns 84% of the company. The market cap is around $1.5m, the P/S is 0.05, P/B is 0.3–this would seem to be a very good buy. The CEO pays himself about $180,000 a year, which seems fair for a company of this size. But Flametree hasn’t paid dividends in years and the CEO has no incentive to. So the shares are kind of stuck in limbo, even as they are undervalued; since the CEO owns 84% there is no opportunity for a hostile takeover. The share price has declined about 90% since listing in 2014.

Case Study 3:

Equity Bank vs. KCB.

Equity Bank has a P/E of around 3.4 while KCB is around 1.8. Both seem undervalued. However, they have fairly different shareholdings. Largest investors:

Equity

– Arise BV (owned by Dutch and Norwegian Development finance institutions)

– James Mwangi (founder and CEO)

KCB

– Government of Kenya

– NSSF (social security)

Does ownership by a DFI and the founder help maintain the share price of Equity Bank?

I bought both Equity and KCB in December. Let’s see how they do.

Is a stock exchange ‘fit for purpose’ in Africa?

Just like mobile money in the US looks very different than mobile money in Africa (Venmo vs. Mpesa), perhaps funding large companies faces an analogous problem. Currently, African public markets are roughly a copy/paste of systems that work in the US. But the chances that a market with vastly less wealth, trust, and education would have the same optimal solution seems…small.

For example, NASDAQ was not even considered a stock market when Apple used it to sell its shares. It was considered an electronic over-the-counter (OTC) system typically reserved for the purgatory of penny stocks. But now it has risen to be the world’s second-largest exchange.

What would the African version of NASDAQ look like?

The EABX OTC system received regulatory approval on Feb 1, 2024. An OTC system for SACCO shares has also been created by Sacco Shares Exchange and SakoSoko.

MPesa was developed and funded by foreigners; Equity Bank, to this day, has a disproportionate amount of foreign shareholders.

What could a fit-for-purpose capital market look like? How can international Development Finance Institutions help?

Criticism of this article

Due to the nature of this article, many people have written comments to me directly rather than post them publicly. While the majority of comments were positive, I’ll focus on the critical ones here:

- You are biased and you promote American Exceptionalism [that is, that Americans are somehow better than others.] NSE and the US stock market are not comparable in any way.

- My goal is not to insult Kenya with this piece; I love Kenya and hope we can do better. I compared the NSE to the NYSE but could as easily have compared it to the Bombay Stock Exchange. NSE could serve all of Africa’s 1.4 billion people just like India’s stock exchanges serve 1.4 billion Indias. India is one country compared to 54 in Africa, but it is divided by religion, language, and culture just like Africa. BRSV exchange works across 7ish countries in West Africa so there’s no reason we can’t do the same in the east. The cross-listing seems like the low-hanging fruit where companies in Rwanda, Zambia, etc cross-list to NSE. We would see more of this if the NSE was more vivacious. So I’m not advocating that we should be like Americans but that there’s existing proof that it’s possible to be better.

- You cherry-picked your data.

- After asking for better data, none was shared.

- CMA is doing a great job of reforming the public markets for the better.

- When I requested examples, none were shared.

Macro trends

There is a trend globally for reduced public market listings. The number of IPOs in the US and UK has halved over the last 25 years.

This is reflected in Kenya where there have been no IPOs for a while, but in just the first half of 2023, there were 34 Private Equity deals worth $1.3b.

As the world becomes flatter, there is consolidation. Why list on the London Securities Exchange when you could list on Euronext or Nasdaq?

Therefore, there is a now or never, go big or go home for the NSE. If it doesn’t become a regional player it will be eclipsed by Mauritius, Johannesburg, Bombay, Euronext, or Nasdaq.

Go regional or become irrelevant.

Conclusion

Why don’t the public markets get fixed in Africa?

Fixing the capital markets starts with quality:

- Rebrand the NSE as the African Stock Exchange and implement the below changes to become a regional player.

- The most important and urgent problem is NSE leadership. The board is currently selecting a new CEO. A lot depends upon this choice. We need a visionary.

- NSE (Nairobi Securities Exchange) can delist companies trading below $1m market cap, below Ksh 10 per share, or have less than 25% freely floating shares.

- NSE can maintain a culture of timeliness and data quality.

- CMA (Capital Markets Authority) can revoke stock broker licenses for trading apps with less than 99% uptime.

- The government of Kenya can let the shilling float freely to eliminate the black market for currency and restore investor confidence.

- GoK can fairly tax land which will drive more investment to productive parts of the economy like equities.

- GoK can reduce interest rates on Treasury bonds. At 15% people would rather buy treasuries than take additional risk for the same (or even less) return on the stock exchange.

- Reduce trading fees. CDSC, NSE, brokers, and government entities can reduce fees that currently preclude an efficient market and high turnover.

- Let the free market do its job: Unfreeze listings like Mumias and Kenya Airways and the regulator, the CEO of CMA, could avoid saying things that sound communist.

- Sell off parastatals and partially government-owned companies. The government of Kenya can sell KenGen and Safaricom to pay off its debt and let companies operate more efficiently on the public markets and in private hands.

- Allow automatic dividend reinvestment: Public companies can create DRIPs (Dividend Reinvestment Programs) to increase demand for shares by automatically reinvesting dividends

- Develop a built-for-Africa solution. Innovators and entrepreneurs can consider what an African-native solution to public markets might be that looks very different from the public markets we have in the West.

Together, these actions would instill confidence in investors and companies, local and foreign.

Improving the public markets could be a win for everyone. A big win that could 10x the economy. A win for investors, companies, stock brokers, the NSE, international development organizations, and the Kenyan government revenue collection.