Understanding investment terminology is crucial for making informed decisions and building a solid investment strategy. Here are 21 key investment terms you need to know to kickstart or continue your investment journey.

1. Asset

An asset is anything of economic value that can be owned or controlled to produce value. Assets can be physical, like real estate, or financial, like stocks and bonds. Assets are essential because they can generate income or be sold for a profit.

Assets might include shares in companies listed on the Johannesburg Stock Exchange or real estate investments in burgeoning cities like Nairobi. For instance, investing in a commercial property in Lagos, Nigeria, which generates rental income.

2. Bond

Bonds are fixed-income securities issued by governments, municipalities, or corporations to raise capital. When you buy a bond, you are essentially lending money to the issuer in exchange for periodic interest payments and the return of the bond’s face value when it matures.

Bonds are considered safer than stocks, though they typically offer lower returns. In Africa, bonds are often used to finance large infrastructure projects. You could purchase a Kenyan government bond to support national infrastructure development.

3. Stock

A stock represents ownership in a company and a claim on part of the company’s assets and earnings. Stocks are a primary means for companies to raise capital and for investors to gain equity in potentially high-growth businesses.

Stocks are known for their potential for high returns but also come with higher risk compared to bonds. Example: Buying stocks in a promising Senegal-based telecom giant Sonatel (SNTS) on the BRVM stock exchange.

ETFs are investment funds traded on stock exchanges, much like stocks. They hold a diversified portfolio of assets such as stocks, bonds, or commodities and aim to track the performance of a specific index.

ETFs offer the benefits of diversification, liquidity, and lower fees compared to mutual funds. They are an efficient way to invest in a broad market segment or specific sector. As an investor, you could put money in an ETF that tracks the performance of the top 50 companies in Africa.

A capital gain is the profit realized from the sale of an investment when the sale price exceeds the purchase price. Capital gains can occur with any investment, including stocks, bonds, real estate, and more.

This profit is subject to capital gains tax, which varies by country. Capital gains are an essential measure of an investment’s profitability.

Suppose you purchase 100 shares of an African tech startup at $10 per share, totaling $1,000. After two years, the company’s value has increased, and you sell your shares at $15 per share, totaling $1,500. The capital gain in this scenario is $500 ($1,500 – $1,000).

6. Asset Allocation

Asset allocation is the process of deciding how to distribute your investments among different asset classes, such as stocks, bonds, real estate, and cash.

The goal of asset allocation is to balance risk and reward by apportioning assets according to an individual’s risk tolerance, goals, and investment time frame.

A well-diversified portfolio can help protect against market volatility. For example, allocating 60% of your portfolio to stocks, 30% to bonds, and 10% to real estate in various African countries.

7. Diversification

Closely related to allocating assets, diversification is an investment strategy that involves spreading your investments across various asset classes, industries, and geographic regions to reduce risk.

By not putting all your eggs in one basket, you can mitigate potential losses from any single investment. Diversification aims to maximize returns by investing in different areas that would each react differently to the same event. For instance, Investing in agricultural startups in Kenya, mining companies in Ghana, and fintech firms in Nigeria.

Compound interest is the interest on a loan or deposit calculated based on both the initial principal and the accumulated interest from previous periods. This means that interest earns interest over time, leading to exponential growth of the invested amount. Compounding can significantly increase the value of your investments, making it a powerful tool for building wealth.

Suppose you invest $1,000 in an African stock fund that earns an annual interest rate of 8%. At the end of the first year, you would earn $80 in interest, making your total investment $1,080. In the second year, you earn interest not just on your original $1,000 but also on the $80 interest from the first year.

This means you earn $86.40 in the second year, bringing your total to $1,166.40. Over time, this compounding effect accelerates, significantly increasing your investment’s growth.

9. Financial Advisor

A financial advisor is a professional who helps individuals manage their finances by providing advice on investments, taxes, estate planning, retirement, and more. Financial advisors can offer personalized strategies tailored to your financial goals and risk tolerance. They can help create and manage a comprehensive financial plan to ensure long-term financial health.

10. Dividend

A dividend is a portion of a company’s earnings distributed to shareholders, usually in the form of cash or additional shares. Dividends provide a steady income stream and are often paid by established profitable companies. Dividend-paying stocks are attractive to investors seeking regular income in addition to potential capital gains.

11. Index Fund

An index fund is a type of mutual fund or ETF designed to replicate the performance of a specific index, such as the S&P 500, the FTSE/JSE All Share Index, the BRVM Composite, BRVM 30, or BRVM Prestige index.

Index funds offer broad market exposure, low operating expenses, and low portfolio turnover. They are a popular choice for investors seeking to achieve long-term growth with minimal active management.

Interest is the cost of borrowing money, typically expressed as a percentage of the principal amount. It can also refer to the earnings from interest-bearing investments like savings accounts, bonds, and certificates of deposit (CDs). Understanding interest rates is crucial for both borrowers and investors, as they affect loan costs and investment returns.

Suppose you deposit $1,000 into a savings account in a Ghanaian bank that offers an annual interest rate of 5%. After one year, you would earn $50 in interest, making your total balance $1,050.

If you leave the interest in the account, the following year, you’ll earn interest on $1,050, resulting in $52.50 in interest, demonstrating the power of compound interest.

13. Mutual Fund

A mutual fund pools money from many investors to purchase a diversified portfolio of stocks, bonds, or other securities. Managed by professional fund managers, mutual funds offer investors the benefits of diversification, professional management, and liquidity. They are suitable for investors seeking exposure to a broad range of assets without having to manage them individually.

14. Portfolio

A portfolio is a collection of investments owned by an individual or institution. It includes a variety of asset classes such as stocks, bonds, real estate, and cash.

A well-balanced portfolio reflects the investor’s risk tolerance, time horizon, and financial goals. Regular portfolio reviews and rebalancing are essential to maintaining the desired asset allocation.

You could create a portfolio with investments in African tech startups, government bonds, and real estate.

15. Real Estate

Real estate involves the purchase, ownership, management, rental, or sale of land and any structures on it. Real estate is a popular investment for diversification and income generation.

Investors can participate directly by buying properties or indirectly through Real Estate Investment Trusts (REITs).

16. Return

Return is the gain or loss on an investment over a specified period, typically expressed as a percentage of the investment’s cost. Returns can come from capital gains, dividends, interest, and other forms of income. Analyzing historical returns helps investors assess the potential profitability and risk of an investment.

Suppose you invest $1,000 in shares of an Ethiopian telecommunications company. After one year, the value of your shares has increased to $1,150. During this period, you also received $50 in dividends. The total return on your investment will be calculated as follows:

Total Return = (Ending Value – Initial Investment + Dividends) / Initial Investment

Total Return = ($1,150 – $1,000 + $50) / $1,000 = $200 / $1,000 = 0.20 or 20%

So, your total return on the investment is 20%.

17. Retirement Account

A retirement account is a financial account specifically designed to save for retirement, offering tax advantages to encourage long-term savings. Common types include Individual Retirement Accounts (IRAs) and 401(k) plans. These accounts provide tax-deferred or tax-free growth, helping individuals build a substantial retirement fund.

18. Risk Tolerance

Risk tolerance is the degree of variability in investment returns that an individual is willing to withstand. It depends on factors like financial goals, investment horizon, and personality.

Understanding your risk tolerance is essential for creating an investment strategy that aligns with your comfort level and long-term objectives. Assessing your risk tolerance, for instance, would help to decide between high-growth tech stocks in Kenya and stable government bonds in Botswana.

18. Security

A security is a financial instrument that represents an ownership position in a company (stock), a creditor relationship with a government or corporation (bond), or ownership rights (option). Securities are essential components of investment portfolios and are regulated to ensure transparency and fairness.

20. Stock Market

The stock market is a collection of markets where stocks (equities) are bought and sold. It includes stock exchanges like the Nigerian Exchange and the BRVM, where traders and investors interact to trade shares.

The stock market plays a crucial role in the economy by providing companies with access to capital and investors with growth opportunities.

Cash refers to currency in the form of paper bills, coins, and funds held in checking, savings, and money market accounts. It is considered a liquid asset because it can be easily accessed and used for transactions.

Maintaining a portion of your portfolio in cash or cash equivalents provides flexibility to quickly take advantage of investment opportunities or cover unexpected expenses. In the context of investing in Africa, holding cash can be particularly useful for navigating periods of volatility or capitalizing on short-term opportunities.

Keeping a portion of your investment in a high-yield savings account in a stable African currency like the CFA Franc can be crucial to ensure liquidity and quick access to funds when needed.

Becoming a Savvy Investor

Understanding these key investment terms can significantly enhance your ability to navigate the world of investing.

Whether you are new to investing or looking to deepen your knowledge, Daba provides the tools and resources you need to succeed.

From real-time analytics to expert advice through Daba Pro, you can confidently manage and grow your investments in Africa’s dynamic markets. Visit our platform today to start your investment journey.

Le monde de l’investissement en actions a son propre langage. Comprendre ces termes clés est crucial pour prendre des décisions d’investissement éclairées.

Investir dans des actions peut être un excellent moyen de construire de la richesse, surtout dans les marchés émergents comme ceux desservis par la BRVM (Bourse Régionale des Valeurs Mobilières).

Cependant, le monde de l’investissement en actions a son propre langage. Comprendre ces termes clés est crucial pour prendre des décisions d’investissement éclairées.

Dans cet article, nous allons explorer 15 termes essentiels du marché boursier, avec des exemples pratiques de la BRVM pour vous aider à naviguer en toute confiance sur le marché boursier ouest-africain.

1. Action

Une action représente une part de propriété dans une entreprise. Lorsque vous achetez des actions de la Société Générale Côte d’Ivoire (SGBC) à la BRVM, vous achetez une petite part de cette grande banque opérant en Afrique de l’Ouest.

2. Dividende

Une partie des bénéfices d’une entreprise versée aux actionnaires. Sonatel, une entreprise de télécommunications de premier plan cotée à la BRVM, a une histoire de paiement de dividendes réguliers à ses actionnaires, leur fournissant un flux de revenu stable.

3. Capitalisation boursière

La valeur totale des actions en circulation d’une entreprise. Elle se calcule en multipliant le prix de marché d’une action par le nombre d’actions en circulation. Actuellement, Sonatel Sénégal (SNTS) a l’une des plus grandes capitalisations boursières à la BRVM, reflétant sa présence significative dans le secteur des télécommunications ouest-africain.

4. Marché haussier (Bull Market)

Une période de hausse des prix des actions et d’optimisme sur le marché. La BRVM a connu un marché haussier en 2015 lorsque l’indice composite de la BRVM a augmenté de plus de 17 %, porté par les fortes performances des secteurs des télécommunications et bancaire.

5. Marché baissier (Bear Market)

Une période de baisse des prix des actions et de pessimisme sur le marché. La BRVM a connu un marché baissier en 2016 lorsque l’indice composite de la BRVM a chuté d’environ 3,87 %, affecté par les incertitudes économiques mondiales.

Le degré de variation du prix de négociation au fil du temps. Les actions de Tractafric Motors CI (PRSC), une entreprise automobile cotée à la BRVM, ont montré une plus grande volatilité par rapport aux actions plus stables comme Sonatel, offrant à la fois des risques et des opportunités pour les investisseurs.

7. Ratio Cours/Bénéfice (P/E Ratio)

Un ratio d’évaluation comparant le prix d’une action aux bénéfices par action de l’entreprise. Le ratio P/E est l’un des indicateurs d’évaluation les plus populaires des actions. Il donne une indication de savoir si une action à son prix de marché actuel est chère ou bon marché.

Typiquement, le ratio P/E moyen est autour de 20 à 25. Tout ce qui est en dessous serait considéré comme un bon ratio cours/bénéfice, tandis que tout ce qui est au-dessus serait un pire ratio P/E.

Par exemple, une action avec un ratio P/E d’environ 8 suggère qu’elle pourrait être sous-évaluée par rapport à certaines actions bancaires mondiales avec des ratios P/E plus élevés.

8. Liquidité

La facilité avec laquelle un actif peut être acheté ou vendu sans affecter son prix. Sonatel et Orange CI (ORAC) sont parmi les actions les plus liquides à la BRVM, ce qui les rend plus faciles à négocier par rapport à des entreprises plus petites et moins fréquemment négociées.

9. Diversification

Répartir les investissements sur divers actifs pour réduire le risque. Un investisseur à la BRVM pourrait diversifier en détenant des actions dans différents secteurs, tels que Sonatel SNTS (télécommunications), SGBC (banques) et Solibra (boissons).

Le processus d’offre d’actions d’une entreprise privée au public pour la première fois. En 2022, la BRVM a accueilli l’IPO d’Orange Côte d’Ivoire (la plus grande jamais réalisée sur la bourse), marquant un ajout significatif à la représentation du secteur des télécommunications régional sur la bourse.

11. Ordre au marché

Un ordre d’acheter ou de vendre une action immédiatement au meilleur prix disponible. Si vous passez un ordre au marché pour des actions Sonatel, il sera exécuté au prix de marché actuel, ce qui pourrait être avantageux dans un marché en mouvement rapide.

12. Ordre à cours limité

Un ordre d’acheter ou de vendre une action à un prix spécifique ou mieux. Vous pourriez placer un ordre à cours limité pour acheter des actions SGCI à 11 000 XOF ou moins, vous assurant de ne pas payer plus que le prix désiré.

13. Rendement du dividende

Le dividende annuel par action divisé par le prix actuel de l’action, exprimé en pourcentage. Si le prix de l’action de Sonatel est de 13 000 XOF et qu’elle verse un dividende annuel de 1 300 XOF par action, son rendement du dividende serait de 10 %.

14. Actions de premier ordre (Blue Chip Stocks)

Actions de grandes entreprises bien établies avec une histoire de bénéfices stables. Sonatel, Orange et SGBC sont souvent considérées comme des actions de premier ordre à la BRVM en raison de leur taille, de leur stabilité et de leur performance constante.

Une mesure de la valeur d’une section du marché boursier. L’indice composite de la BRVM et l’indice BRVM 30 sont des indicateurs clés de la performance globale du marché dans la région UEMOA.

Comprendre ces 15 termes clés est crucial pour quiconque souhaite investir en actions. Alors que vous commencez votre parcours d’investissement, rappelez-vous que la connaissance est le pouvoir. Ces termes vous aideront à analyser les investissements potentiels, à comprendre les mouvements du marché et à prendre des décisions éclairées.

Chez Daba, nous nous engageons à donner aux investisseurs les connaissances et les outils dont ils ont besoin pour réussir sur les marchés africains et émergents. Notre plateforme offre un accès aux actions de la BRVM et à d’autres opportunités d’investissement à travers l’Afrique, soutenue par des informations fiables et des insights d’experts.

Que vous soyez intéressé par des actions de premier ordre comme Sonatel et SGBC, ou que vous cherchiez à diversifier votre portefeuille dans différents secteurs et marchés, Daba Pro peut vous aider à naviguer dans le monde passionnant des investissements africains en toute confiance.

Commencez votre parcours d’investissement avec nous dès aujourd’hui et mettez en pratique vos nouvelles connaissances pour construire un portefeuille solide et diversifié. N’oubliez pas, bien que comprendre ces termes soit important, il est toujours sage de mener des recherches approfondies et d’envisager de consulter des professionnels avant de prendre des décisions d’investissement.

The world of stock investing comes with its own language. Understanding these key terms is crucial for making informed investment decisions.

Investing in stocks can be an excellent way to build wealth, especially in emerging markets like those served by the BRVM (Bourse Régionale des Valeurs Mobilières).

However, the world of stock investing comes with its own language. Understanding these key terms is crucial for making informed investment decisions.

In this article, we’ll explore 15 essential stock market terms, with practical examples from the BRVM to help you navigate the West African stock market with confidence.

1. Stock

A stock represents partial ownership in a company. When you buy shares of Société Générale Côte d’Ivoire (SGBC) on the BRVM, you’re purchasing a small piece of this major bank operating in West Africa.

2. Dividend

A portion of a company’s profits paid out to shareholders. Sonatel, a leading telecommunications company listed on the BRVM, has a history of paying regular dividends to its shareholders, providing them with a steady income stream.

3. Market Capitalization

The total value of a company’s outstanding shares. It is calculated by multiplying the market price of a single share by the outstanding shares. Currently, Sonatel Senegal (SNTS) has one of the largest market capitalizations on the BRVM, reflecting its significant presence in the West African telecom sector.

4. Bull Market

A period of rising stock prices and optimism in the market. The BRVM experienced a bull market in 2015 when the BRVM Composite Index rose by over 17%, driven by strong performances in sectors like telecommunications and banking.

5. Bear Market

A period of falling stock prices and pessimism in the market. The BRVM faced a bear market in 2016 when the BRVM Composite Index fell by about 3.87%, affected by global economic uncertainties.

The degree of variation in trading price over time. Shares of Tractafric Motors CI (PRSC), an automotive company listed on the BRVM, have shown higher volatility compared to more stable stocks like Sonatel, presenting both risks and opportunities for investors.

7. Price-to-Earnings (P/E) Ratio

A valuation ratio comparing a company’s stock price to its earnings per share. The PE ratio is one of the most popular valuation metrics of stocks. It provides an indication of whether a stock at its current market price is expensive or cheap.

Typically, the average P/E ratio is around 20 to 25. Anything below that would be considered a good price-to-earnings ratio, whereas anything above that would be a worse P/E ratio.

For instance, a stock with a P/E ratio of around 8 suggests it may be undervalued compared to some global banking stocks with higher P/E ratios.

8. Liquidity

The ease with which an asset can be bought or sold without affecting its price. Sonatel and Orange CI (ORAC) are among the most liquid stocks on the BRVM, making them easier to trade compared to smaller, less frequently traded companies.

9. Diversification

Spreading investments across various assets to reduce risk. An investor on the BRVM might diversify by holding stocks in different sectors, such as Sonatel SNTS (telecom), SGBC (banking), and Solibra (beverages).

The process of offering shares of a private company to the public for the first time. In 2022, the BRVM welcomed Orange Cote d’Ivoire’s IPO (the largest ever on the bourse), marking a significant addition to the regional telecom sector representation on the exchange.

11. Market Order

An order to buy or sell a stock immediately at the best available price. If you place a market order for Sonatel shares, it will be executed at the current market price, which could be beneficial in a fast-moving market.

12. Limit Order

An order to buy or sell a stock at a specific price or better. You might set a limit order to buy SGCI shares at 11,000 XOF or lower, ensuring you don’t pay more than your desired price.

13. Dividend Yield

The annual dividend per share divided by the stock’s current price, expressed as a percentage. If Sonatel’s stock price is 13,000 XOF and it pays an annual dividend of 1,300 XOF per share, its dividend yield would be 10%.

14. Blue Chip Stocks

Shares of large, well-established companies with a history of stable earnings. Sonatel, Orange, and SGBC are often considered blue-chip stocks on the BRVM due to their size, stability, and consistent performance.

A measurement of the value of a section of the stock market. The BRVM Composite Index and the BRVM 30 Index are key indicators of overall market performance in the WAEMU/UEMOA region.

Understanding these 15 key terms is crucial for anyone looking to invest in stocks. As you begin your investment journey, remember that knowledge is power. These terms will help you analyze potential investments, understand market movements, and make informed decisions.

At Daba, we’re committed to empowering investors with the knowledge and tools they need to succeed in African and emerging markets. Our platform offers access to BRVM stocks and other investment opportunities across Africa, backed by reliable information and expert insights.

Whether you’re interested in blue chip stocks like Sonatel and SGBC, or you’re looking to diversify your portfolio across different sectors and markets, Daba Pro can help you navigate the exciting world of African investments with confidence.

Start your investment journey with us today and put your new knowledge to work in building a strong, diversified portfolio. Remember, while understanding these terms is important, it’s always wise to conduct thorough research and consider seeking professional advice before making investment decisions.

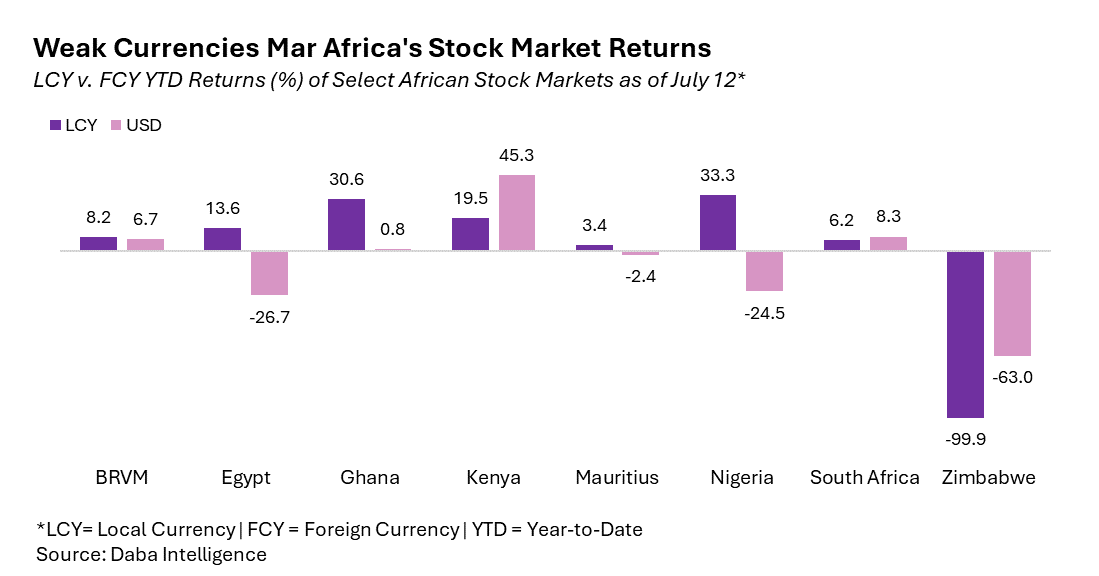

Les devises africaines faibles érodent les rendements des actions pour les investisseurs en dollars, diminuant l’attrait du continent en tant que destination de marché de frontière. La BRVM offre une alternative convaincante.

Presque partout en Afrique, les marchés boursiers sont en plein essor, certains atteignant des niveaux sans précédent. Les actions égyptiennes, mesurées par l’indice EGX 30, ont encore grimpé de 0,45 % la semaine se terminant le 10 juillet. L’indice de référence a bondi de plus de 13 % depuis le début de l’année en termes de monnaie locale – un rallye impressionnant à tous égards. Mais pour les investisseurs internationaux évaluant leurs rendements en dollars américains, le tableau est bien moins réjouissant.

La forte baisse de la livre égyptienne par rapport au dollar a transformé ces gains à deux chiffres en une perte douloureuse de -26 %. Cela reflète le paradoxe auquel sont confrontés de nombreux marchés boursiers africains en 2024. Alors que les indices boursiers locaux affichent des gains enviables, les devises faibles sur des marchés comme l’Égypte, le Nigeria, le Zimbabwe et d’autres érodent les rendements pour les investisseurs internationaux et ceux mesurant la performance en dollars américains ou en euros, diminuant ainsi l’attrait du continent en tant que destination de marché de frontière.

Le mois dernier, l’un des plus grands gestionnaires d’actifs du monde, BlackRock, a annoncé la liquidation de son ETF iShares de 400 millions de dollars qui investissait dans des pays comme le Nigeria et le Kenya, citant des conditions économiques difficiles et des problèmes de devises. La liquidation met en évidence des défis systémiques plus larges dans ces marchés : la volatilité des devises a rendu de plus en plus difficile pour les investisseurs étrangers de maintenir des rendements stables, aux côtés des défis de liquidité du marché et des restrictions sur le rapatriement des bénéfices.

Ce développement pourrait inciter à une réévaluation des profils de risque-rendement des actions africaines parmi les investisseurs mondiaux, ce qui pourrait potentiellement entraîner une réduction des flux de capitaux étrangers vers ces marchés à court terme.

Les réformes coûteuses de l’Égypte

L’histoire de l’Égypte est particulièrement frappante. La divergence spectaculaire entre les rendements des actions en termes de monnaie locale et étrangère découle de la récente crise monétaire de l’Égypte.

En mars 2024, le pays a mis en œuvre des réformes économiques, y compris une forte dévaluation de la livre égyptienne. La banque centrale a augmenté les taux d’intérêt de 600 points de base et a permis à la valeur de la livre de plonger par rapport au dollar américain.

Ces mesures faisaient partie d’un plan de sauvetage de 8 milliards de dollars avec le Fonds monétaire international (FMI), élargi à partir d’un précédent accord de 3 milliards de dollars. Les réformes visent à résoudre la pénurie chronique de devises étrangères du pays nord-africain et l’inflation galopante, qui a vu les prix du pain non subventionné presque doubler en un an seulement.

Bien que la dévaluation puisse aider à rendre les exportations égyptiennes plus compétitives et améliorer le déficit commercial du pays, elle a considérablement diminué le pouvoir d’achat des Égyptiens, dont près de 30 % vivent déjà dans la pauvreté. Pour les investisseurs internationaux, la baisse de la devise a plus que compensé les gains du marché boursier.

Les problèmes du naira nigérian éclipsent le rallye du marché

Le Nigeria présente un tableau similaire. L’indice NGX All Share a grimpé de 33,3 % en termes de naira depuis le début de 2024. Pourtant, lorsqu’ils sont mesurés en dollars américains, les investisseurs enregistrent une perte de -24,46 %.

Le coupable ? La piètre performance du naira nigérian. Bloomberg a rapporté que le naira a terminé le premier semestre de 2024 en tant que monnaie la moins performante au monde, s’affaiblissant de 40 % depuis le début de l’année. Cette série de pertes est la plus longue depuis juillet 2017 pour l’une des plus grandes économies d’Afrique.

Le Nigeria a lutté pendant des années avec une pénurie aiguë de devises étrangères et une instabilité, principalement en raison d’une production de pétrole brut plus faible et d’un manque de diversification économique. Depuis juin 2023, lorsque le gouvernement du président Bola Tinubu a introduit des changements de politique pour attirer les flux de capitaux et relancer l’économie, la monnaie locale a perdu environ 70 % de sa valeur par rapport au dollar.

Le gouverneur de la banque centrale, Olayemi Cardoso, s’est montré optimiste quant à la possibilité de stabiliser la volatilité de la devise. Depuis son entrée en fonction en septembre, il a augmenté les taux d’intérêt de 750 points de base pour atteindre 26,25 %, a éliminé un arriéré de devises étrangères et a négocié des entrées de dollars multilatéraux pour aider à stabiliser la monnaie.

Cependant, la performance du naira au premier semestre de 2024 suggère que des défis importants subsistent.

La volatilité extrême des devises au Zimbabwe

La situation au Zimbabwe est peut-être la plus extrême. L’indice All Share de la Bourse du Zimbabwe (ZSE) a chuté de 99,92 % en termes de monnaie locale depuis le début de l’année. Lorsqu’il est converti en dollars américains, cela se traduit par une perte de 62,95 %.

Cette baisse survient alors que le Zimbabwe a récemment annoncé la conversion de ses soldes en dollars locaux en une nouvelle monnaie appelée Zimbabwe Gold, ou ZiG. Ce geste représente une nouvelle tentative de stabiliser la situation monétaire volatile du pays, qui a connu de multiples redénominations et périodes d’hyperinflation au cours des deux dernières décennies.

La nouvelle monnaie ZiG est supposément adossée à des réserves d’or, le gouverneur de la banque centrale affirmant avoir 1,1 tonne d’or dans ses coffres et des réserves supplémentaires à l’étranger. Cependant, les économistes et les citoyens restent sceptiques, compte tenu de l’histoire du pays en matière de réformes monétaires ratées.

Malgré l’introduction du ZiG, environ 85 % de toutes les transactions au Zimbabwe sont encore réalisées en dollars américains, soulignant le manque de confiance persistant dans la monnaie locale. Cette dollarisation persistante rend difficile le fonctionnement efficace du marché boursier en termes de monnaie locale.

L’avantage de la BRVM

Contrairement aux pertes dues aux devises observées sur certains marchés africains, la BRVM, une bourse régionale desservant huit pays d’Afrique de l’Ouest, offre des rendements solides en termes de monnaie locale et étrangère.

L’indice composite de la BRVM, qui couvre les actions cotées à la Bourse Régionale des Valeurs Mobilières, dont le siège est à Abidjan, en Côte d’Ivoire, a augmenté de 8,18 % en termes de monnaie locale au 12 juillet. Plus important encore pour les investisseurs internationaux, ces gains se traduisent par un rendement de 6,74 % en dollars américains et de 7,97 % en euros.

La capacité de préserver les rendements pour les investisseurs étrangers découle de la devise utilisée dans ses pays membres. La bourse opère avec le franc CFA, qui est indexé sur l’euro à un taux fixe. Cette parité offre un niveau de stabilité et de prévisibilité qui fait cruellement défaut à de nombreuses autres devises africaines.

Les huit pays desservis par la BRVM – Bénin, Burkina Faso, Côte d’Ivoire, Guinée-Bissau, Mali, Niger, Sénégal et Togo – sont tous membres de l’Union Économique et Monétaire Ouest Africaine (UEMOA). Ce bloc économique utilise le franc CFA d’Afrique de l’Ouest, qui maintient sa parité avec l’euro depuis 1999.

Alors que les rendements sont plus modestes que sur certains autres marchés africains, l’écart minimal entre les rendements en monnaie locale et étrangère démontre la valeur de la stabilité monétaire. La légère différence est due aux fluctuations du taux de change euro-dollar plutôt qu’à une faiblesse du franc CFA lui-même. Les mouvements de l’euro ont également été beaucoup moins dramatiques que les dévaluations observées dans des pays comme l’Égypte et le Nigeria.

Cette stabilité rend la BRVM attrayante pour les investisseurs averses au risque souhaitant obtenir une exposition aux actions africaines sans prendre de risques significatifs liés aux devises. Elle permet aux investisseurs de se concentrer davantage sur les fondamentaux des entreprises et les facteurs économiques plutôt que sur les risques de change et offre également un environnement plus prévisible pour les entreprises cotées.

Cependant, la parité du franc CFA n’est pas sans controverse. Les critiques soutiennent qu’elle limite la flexibilité de la politique monétaire et maintient les pays membres trop dépendants de la France. Néanmoins, pour les investisseurs recherchant un juste milieu entre les marchés à forte croissance et à haut risque et la stabilité des économies développées, la BRVM offre une alternative convaincante.

Le tableau d’ensemble

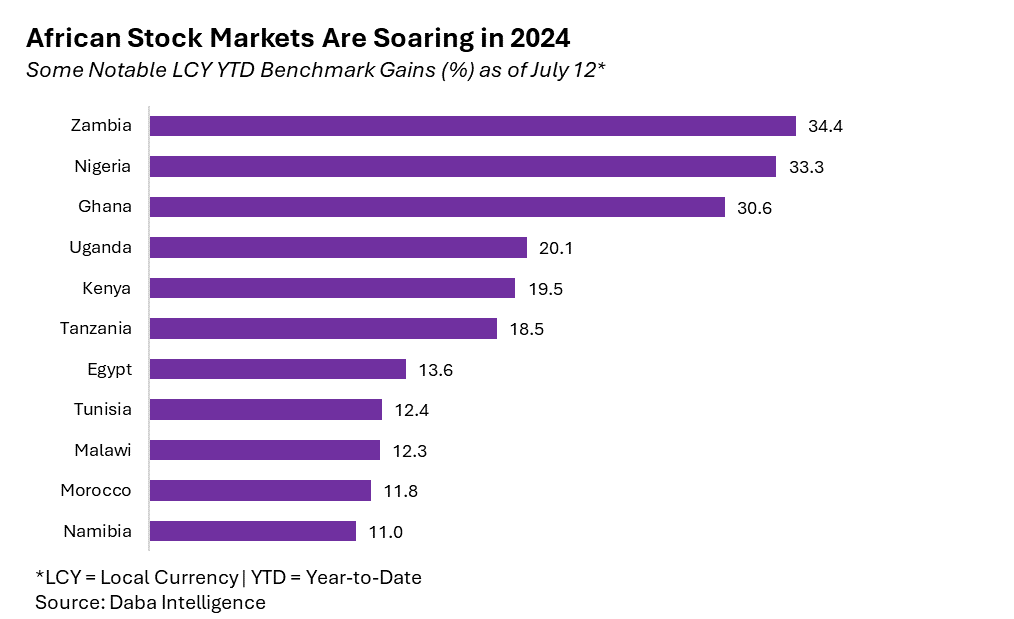

Malgré les défis liés aux devises, de nombreux marchés boursiers africains ont affiché des performances impressionnantes en termes de monnaie locale en 2024.

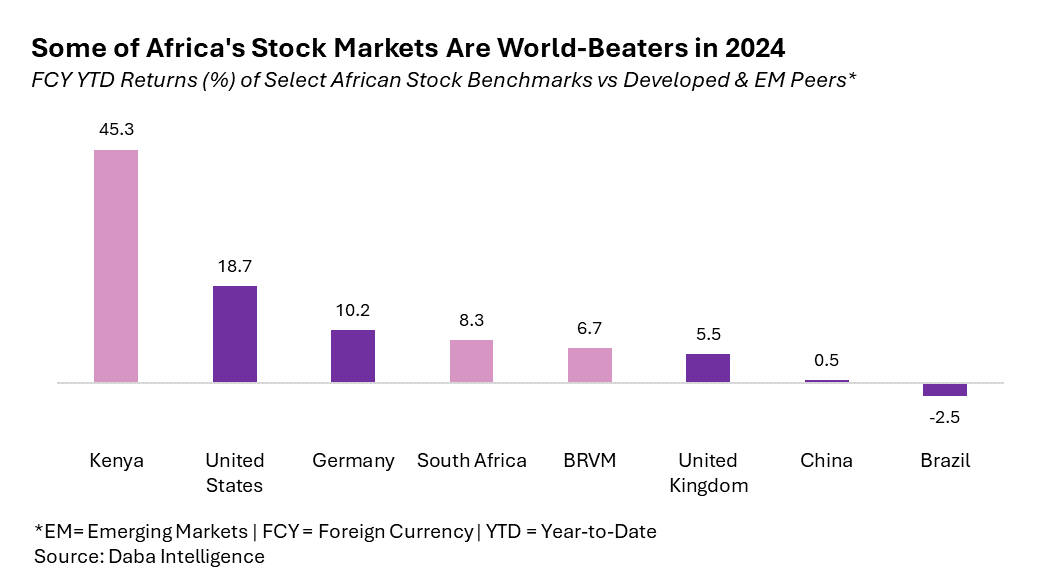

À noter également le Kenya, dont l’indice de référence boursier a rebondi de son creux précédent pour devenir l’un des meilleurs performeurs mondiaux. L’indice All-Share de la Bourse des Valeurs de Nairobi a enregistré un rendement de plus de 45 % pour les investisseurs en dollars cette année, après une perte de plus de 40 % en 2023.

Ces chiffres soulignent le potentiel des marchés boursiers africains, notamment pour les investisseurs locaux ou ceux capables de couvrir le risque de change efficacement.

Cependant, la différence marquée entre les rendements en monnaie locale et en dollars américains sur de nombreux marchés met en évidence le rôle crucial que joue la stabilité monétaire dans l’attraction et la rétention des investissements internationaux.

Équilibrer croissance et stabilité

Les fortunes divergentes des marchés boursiers africains en 2024 soulignent les défis complexes auxquels sont confrontées les économies du continent. Alors que de nombreux pays connaissent une croissance économique robuste et des marchés boursiers locaux en plein essor, l’instabilité monétaire menace de saper ces gains aux yeux des investisseurs internationaux.

Pour des pays comme l’Égypte et le Nigeria, la voie à suivre consiste à équilibrer soigneusement la nécessité de taux de change compétitifs avec le désir de stabilité monétaire. Les deux nations travaillent avec des partenaires internationaux comme le FMI pour mettre en œuvre des réformes, mais le processus sera probablement progressif et potentiellement volatile.

La situation du Zimbabwe reste particulièrement difficile, compte tenu de son histoire d’hyperinflation et de multiples crises monétaires. L’introduction de la monnaie ZiG représente une nouvelle tentative de stabiliser le système monétaire, mais il reste à voir si cet effort réussira là où d’autres ont échoué.

Le succès relatif de la BRVM et de la zone franc CFA offre un modèle intrigant pour d’autres régions africaines à considérer. Bien que les unions monétaires complètes puissent ne pas être réalisables ou souhaitables pour tous les pays, explorer des moyens d’améliorer la coopération monétaire et de réduire la volatilité des taux de change pourrait aider à préserver les gains des marchés boursiers pour les investisseurs locaux et internationaux.

Pour les investisseurs, la principale conclusion est l’importance croissante de regarder au-delà des rendements boursiers bruts lors de l’évaluation des opportunités d’investissement en Afrique. Les tendances des devises, les réformes économiques et la stabilité politique sont des facteurs cruciaux à considérer en plus de la performance des actions. Bien que le potentiel de rendements élevés existe, comme en témoigne la forte performance en monnaie locale de nombreux marchés, la gestion de l’exposition aux devises est essentielle pour réaliser des gains réels.

Alors que l’Afrique continue de se développer et que ses marchés financiers mûrissent, la stabilité monétaire sera la clé pour débloquer le plein potentiel des marchés boursiers du continent. En attendant, les investisseurs devront naviguer prudemment, en équilibrant les opportunités passionnantes présentées par l’histoire de croissance de l’Afrique avec les risques très réels posés par la volatilité des devises.

Weak African currencies erode equity returns for dollar investors, dimming the continent’s appeal as a frontier market destination. The BRVM offers a compelling alternative.

Almost everywhere you look in Africa, stock markets are soaring with some hitting unprecedented levels. Egyptian equities, as measured by the EGX 30 index, climbed another 0.45% in the week ending July 10. The benchmark index had surged over 13% since the start of the year in local currency terms – an impressive rally by any measure. But for international investors eyeing their returns in US dollars, the picture is far less rosy.

The Egyptian pound’s steep decline against the greenback had turned those double-digit gains into a painful -26% loss. This mirrors the paradox facing many African equity markets in 2024. While local stock indices post enviable gains, weak currencies in markets like Egypt, Nigeria, Zimbabwe and others are eroding returns for international investors and those measuring performance in US dollars or euros, dimming the continent’s appeal as a frontier market destination.

Last month, one of the world’s largest asset managers BlackRock said it was liquidating its $400 million iShares ETF which had investments in countries like Nigeria and Kenya, citing tough economic conditions and currency issues. The liquidation points to broader systemic challenges in these markets: currency volatility has made it increasingly difficult for foreign investors to maintain stable returns, alongside market liquidity challenges and restrictions on the repatriation of profits.

This development may prompt a reassessment of risk-reward profiles for African equities among global investors, potentially leading to a reduced inflow of foreign capital into these markets in the near term.

Egypt’s Costly Reforms

Egypt’s story is particularly striking. The dramatic divergence between equity returns in local and foreign currency terms stems from Egypt’s recent currency crisis.

In March 2024, the country implemented economic reforms, including a sharp devaluation of the Egyptian pound. The central bank hiked interest rates by 600 basis points and allowed the pound’s value to plummet against the US dollar.

In March 2024, the country implemented economic reforms, including a sharp devaluation of the Egyptian pound.

These measures were part of an $8 billion rescue package deal with the International Monetary Fund (IMF), expanded from a previous $3 billion agreement. The reforms aim to address the North African nation’s chronic foreign currency shortage and rampant inflation, which saw unsubsidized bread prices nearly double in just one year.

While the devaluation may help make Egyptian exports more competitive and improve the country’s trade deficit, it has significantly diminished the purchasing power of Egyptians, nearly 30% of whom already live in poverty. For international investors, the currency’s decline has more than offset any stock market gains.

Nigeria’s Naira Woes Overshadow Market Rally

Nigeria presents a similar picture. The NGX All Share Index has soared 33.3% in naira terms since the start of 2024. Yet, when measured in US dollars, investors are looking at a -24.46% loss.

The culprit? The Nigerian naira’s dismal performance. Bloomberg reported that the naira ended the first half of 2024 as the world’s worst-performing currency, weakening by 40% since the start of the year. This losing streak is the longest since July 2017 for one of Africa’s largest economies.

FILE PHOTO: A man counts Nigerian naira notes in a marketplace in Yola, Nigeria, February 22, 2023. REUTERS/Esa Alexander/File Photo

Nigeria has grappled with acute foreign exchange scarcity and instability for years, primarily due to lower crude oil production and a lack of economic diversification. Since June 2023, when President Bola Tinubu’s government introduced policy changes to attract inflows and revive the economy, the local currency has lost about 70% of its value against the dollar.

Central Bank Governor Olayemi Cardoso has expressed optimism that the currency’s volatility may be subsiding. Since taking office in September, he has increased interest rates by 750 basis points to 26.25%, cleared a foreign exchange backlog, and negotiated multilateral dollar inflows to help stabilize the currency.

However, the naira’s performance in the first half of 2024 suggests that significant challenges remain.

Extreme Currency Volatility in Zimbabwe

Zimbabwe’s situation is perhaps the most extreme. The Zimbabwe Stock Exchange (ZSE) All Share Index has plummeted 99.92% in local currency terms year-to-date. When converted to US dollars, this translates to a 62.95% loss.

This decline comes as Zimbabwe recently announced the conversion of its domestic dollar balances into a new currency called Zimbabwe Gold, or ZiG. This move represents yet another attempt to stabilize the country’s volatile currency situation, which has seen multiple redenominations and periods of hyperinflation over the past two decades.

The new ZiG currency is supposedly backed by gold reserves, with the central bank governor claiming 1.1 tons of gold in its vaults and additional reserves abroad. However, economists and citizens remain skeptical, given the country’s history of failed currency reforms.

Despite the introduction of ZiG, around 85% of all transactions in Zimbabwe are still conducted in US dollars, highlighting the ongoing lack of confidence in the domestic currency. This persistent dollarization makes it challenging for the stock market to function effectively in local currency terms.

ZiG represents yet another attempt to stabilize Zimbabwe’s volatile currency situation, which has lasted for two decades.

The BRVM Advantage

In stark contrast to the currency-driven losses seen in some African markets, the BRVM, a regional stock exchange serving eight West African countries, is delivering solid returns in both local and foreign currency terms.

The BRVM Composite index, which covers stocks listed on the Bourse Régionale des Valeurs Mobilières headquartered in Abidjan, Côte d’Ivoire, has risen 8.18% in local currency terms through July 12th. More importantly for international investors, those gains translate to a 6.74% return in US dollars and a 7.97% return in euros.

An ability to preserve returns for foreign investors stems from the currency used in its member countries. The exchange operates using the CFA franc, which is pegged to the euro at a fixed rate. This peg provides a level of stability and predictability that’s sorely lacking in many other African currencies.

The eight countries served by the BRVM – Benin, Burkina Faso, Côte d’Ivoire, Guinea-Bissau, Mali, Niger, Senegal, and Togo – are all members of the West African Economic and Monetary Union (WAEMU). This economic bloc uses the West African CFA franc, which has maintained its peg to the euro since 1999.

While the returns are more modest than in some other African markets, the minimal gap between local and foreign currency returns demonstrates the value of currency stability. The slight difference is due to fluctuations in the euro-dollar exchange rate rather than weakness in the CFA franc itself. The euro’s movements have also been far less dramatic than the devaluations seen in countries like Egypt and Nigeria.

This stability makes the BRVM an attractive option for risk-averse investors looking to gain exposure to African equities without taking on significant currency risk. It allows investors to focus more on company fundamentals and economic factors rather than currency risk and also provides a more predictable environment for the listed companies.

However, the CFA franc peg is not without controversy. Critics argue it limits monetary policy flexibility and keeps the member countries too dependent on France. Nonetheless, for investors seeking a middle ground between high-growth, high-risk markets and the stability of developed economies, the BRVM offers a compelling alternative.

The Bigger Picture

Despite the currency challenges, many African stock markets have shown impressive performance in local currency terms in 2024.

Of noteworthy mention is Kenya‘s stock benchmark, which swung from rock bottom earlier in the year to being one of the world’s best performers. The Nairobi Securities Exchange All-Share Index has returned over 45% for dollar investors this year, following a loss of more than 40% in 2023.

These figures underscore the potential of African equity markets, particularly for local investors or those able to hedge currency risk effectively.

However, the stark difference between local currency returns and US dollar returns in many markets highlights the critical role that currency stability plays in attracting and retaining international investment.

Balancing Growth and Stability

The divergent fortunes of African stock markets in 2024 underscore the complex challenges facing the continent’s economies. While many countries are seeing robust economic growth and booming local stock markets, currency instability threatens to undermine these gains in the eyes of international investors.

For countries like Egypt and Nigeria, the path forward involves carefully balancing the need for competitive exchange rates with the desire for currency stability. Both nations are working with international partners like the IMF to implement reforms, but the process is likely to be gradual and potentially volatile.

Zimbabwe’s situation remains particularly challenging, given its history of hyperinflation and multiple currency crises. The introduction of the ZiG currency represents yet another attempt to stabilize the monetary system, but it remains to be seen whether this effort will succeed where others have failed.

The relative success of the BRVM and the CFA franc zone offers an intriguing model for other African regions to consider. While full currency unions may not be feasible or desirable for all countries, exploring ways to enhance monetary cooperation and reduce exchange rate volatility could help preserve stock market gains for both local and international investors.

For investors, the key takeaway is the increasing importance of looking beyond headline stock market returns when evaluating African investment opportunities. Currency trends, economic reforms, and political stability are crucial factors to consider alongside equity performance. While the potential for high returns exists, as evidenced by the strong local currency performance of many markets, managing currency exposure is crucial to realizing gains in real terms.

As Africa continues to develop and its financial markets mature, addressing currency stability will be key to unlocking the full potential of the continent’s stock markets. Until then, investors will need to navigate carefully, balancing the exciting opportunities presented by Africa’s growth story with the very real risks posed by currency volatility.

Les marchés boursiers africains ont connu une croissance robuste, offrant des opportunités lucratives aux investisseurs. Découvrez les dix plus grandes bourses du continent par capitalisation boursière en mai 2024.

Les marchés boursiers africains ont connu une croissance robuste, offrant des opportunités lucratives aux investisseurs. Avec 29 bourses opérationnelles et une capitalisation boursière combinée d’environ 1,3 trillion de dollars, les bourses africaines contribuent à plus de 2 % du marché mondial.

Aujourd’hui, les cinq plus grands marchés boursiers par capitalisation boursière sont la JSE d’Afrique du Sud, la bourse de Casablanca, la Bourse du Botswana, la Nigerian Exchange (NGX) et l’EGX. Aux côtés de ces géants, des bourses importantes se trouvent également dans des pays comme le Kenya et la Bourse Régionale des Valeurs Mobilières (BRVM), qui dessert huit pays francophones de l’Union Économique et Monétaire Ouest Africaine (UEMOA).

En explorant les dix plus grandes bourses par capitalisation boursière, découvrez comment Daba peut renforcer votre parcours d’investissement à travers les marchés dynamiques de l’Afrique. Basé sur les dernières données du 31 mai 2024, fournies par Daba Intelligence, voici les dix plus grandes bourses d’Afrique classées par capitalisation boursière en dollars américains :

La Bourse de Johannesburg, fondée en 1887, est la plus grande d’Afrique avec une capitalisation boursière de 1,07 trillion de dollars. Il y a environ 354 entreprises cotées, les plus importantes étant Naspers Limited, FirstRand Limited et Standard Bank Group.

La Bourse de Casablanca au Maroc, fondée en 1929, est la deuxième plus grande bourse d’Afrique avec une capitalisation boursière de 69,8 milliards de dollars. Les principales entreprises cotées incluent Attijariwafa Bank, Banque Centrale Populaire et Bank of Africa.

3. Bourse du Botswana (BSE) – 52 461 754 292,20 $

Avec une capitalisation boursière de 52,5 milliards de dollars, la Bourse du Botswana est la troisième plus grande d’Afrique. Les principales entreprises cotées incluent Anglo American Plc, First National Bank Botswana et Botswana Insurance Holdings.

Que vous soyez un investisseur institutionnel recherchant une exécution commerciale fiable ou un investisseur de détail cherchant à élargir vos horizons d’investissement, la plateforme conviviale de Daba garantit transparence et facilité d’utilisation. Téléchargez notre application maintenant pour commencer.

Dividendes élevés sur les Bourses Africaines : La clé pour optimiser votre portefeuille

4. Nigerian Exchange (NGX) – 41 029 161 524,02 $

La NGX du Nigeria a une capitalisation boursière de 41 milliards de dollars, ce qui en fait la quatrième plus grande bourse d’Afrique. Les principales entreprises cotées incluent Airtel Africa Plc, MTN Nigeria Communications, Dangote Cement et BUA Cement.

5. Bourse égyptienne (EGX) – 40 278 844 587,20 $

La Bourse égyptienne, formée par la fusion des bourses d’Alexandrie et du Caire, a une capitalisation boursière de 40,3 milliards de dollars. Les principales entreprises cotées incluent Abu Qir Fertilizers, Alexandria Containers and Goods et Commercial International Bank.

La BRVM, bourse régionale desservant huit nations ouest-africaines, a une capitalisation boursière de 13,8 milliards de dollars. Environ 56 entreprises sont cotées et les principales cotations incluent Sonatel, Orange Côte d’Ivoire et Ecobank Transnational Incorporated.

7. Bourse des valeurs mobilières de Nairobi (NSE) – 13 639 305 859,51 $

La Bourse des valeurs mobilières de Nairobi au Kenya a une capitalisation boursière de 13,6 milliards de dollars. Safaricom, Equity Group Holdings et East African Breweries Limited sont ses plus grandes entreprises cotées. Fondée en 1954, la NSE est la plus grande bourse d’Afrique de l’Est avec 65 entreprises cotées.

Investir sur les marchés dynamiques de l’Afrique n’a jamais été aussi facile. Les services d’investissement de Daba offrent des stratégies personnalisées pour vous aider à maximiser les rendements et à gérer les risques efficacement. Téléchargez notre application maintenant pour commencer.

8. Bourse de Maurice (SEM) – 7 429 084 934,02 $

La SEM a une capitalisation boursière de 7,4 milliards de dollars, avec les principales cotations incluant MCB Group, Ireland Blyth et SBM Holdings. Fondée en 1989, la Bourse de Maurice (SEM) couvre Maurice et est basée à Port Louis. 56 entreprises sont cotées sur le marché officiel de la SEM, tandis que 42 autres sont cotées sur le marché du développement et des entreprises (DEM).

9. Bourse de Dar es Salaam – 6 657 926 433,80 $

La Bourse de Dar es Salaam en Tanzanie a une capitalisation boursière de 6,7 milliards de dollars. Située à Dar es Salaam, la capitale commerciale et plus grande ville de Tanzanie, elle a été incorporée en septembre 1996 et les échanges ont commencé en avril 1998.

10. Bourse du Ghana (GSE) – 5 709 315 520,89 $

En dernière position des dix premières, on trouve la Bourse du Ghana avec une capitalisation boursière de 5,7 milliards de dollars. Ses principales entreprises cotées incluent Ecobank Transnational, AngloGold Ashanti Plc et Access Bank Ghana.

La croissance dynamique des bourses africaines souligne l’importance croissante du continent dans la finance mondiale. Daba s’engage à fournir des informations fiables, des services transparents et des expériences d’investissement fluides sur ces marchés.

Que vous cherchiez à diversifier votre portefeuille ou à explorer des opportunités émergentes, Daba se positionne comme votre partenaire de confiance pour naviguer dans le paysage dynamique des investissements en Afrique.

African stock markets have experienced robust growth, presenting lucrative opportunities for investors. Discover the ten largest stock exchanges on the continent by market cap as of May 2024.

African stock markets have experienced robust growth, presenting lucrative opportunities for investors. With 29 operational exchanges and a combined market capitalization of around $1.3 trillion, African bourses contribute over 2% to the global market.

Some of the oldest and most established exchanges in Africa include the Egyptian Exchange (EGX), founded in 1883, the Casablanca Stock Exchange of Morocco, tracing its roots back to 1929, the Johannesburg Stock Exchange (JSE) established in 1887, and the Nairobi Securities Exchange in Kenya, which dates back to 1954.

Today, the top five largest stock markets by market capitalization are South Africa’s JSE, the Casablanca bourse, the Botswana Stock Exchange, the Nigerian Exchange (NGX), and EGX. Alongside these titans, sizable exchanges can also be found in countries like Kenya and the West African Economic and Monetary Union (WAEMU) regional exchange serving eight French-speaking nations.

As we explore the ten largest stock exchanges by market capitalization, discover how Daba can empower your investment journey across Africa’s dynamic markets. Based on the latest data as of May 31, 2024, sourced by Daba Intelligence, here are the ten largest stock exchanges in Africa ranked by market capitalization in US dollars:

The Johannesburg Stock Exchange, founded in 1887, is the largest in Africa with a market capitalization of $1.07 trillion. There are around 354 listed companies, with the largest being Naspers Limited, FirstRand Limited, and Standard Bank Group.

The Casablanca Stock Exchange in Morocco, founded in 1929, is the second-largest stock market in Africa with a market cap of $69.8 billion. The top listed companies include Attijariwafa Bank, Banque Centrale Populaire, and Bank of Africa.

With a market capitalization of $52.5 billion, the Botswana Stock Exchange is the third-largest in Africa. Major listed companies include Anglo American Plc, First National Bank Botswana, and Botswana Insurance Holdings.

Whether you’re an institutional investor seeking reliable trade execution or a retail investor looking to expand your investment horizons, Daba’s user-friendly platform ensures transparency and ease of use. Download our app now to get started.

Tap to Read: How to optimize your investments in Africa with dividend yields

4. Nigerian Exchange (NGX) – $41,029,161,524.02

Nigeria’s NGX has a market cap of $41 billion, making it the fourth-largest stock exchange in Africa. Major listed companies include Airtel Africa Plc, MTN Nigeria Communications, Dangote Cement, and BUA Cement.

5. Egyptian Exchange (EGX) – $40,278,844,587.20

The Egyptian Exchange, formed by the merger of Alexandria and Cairo stock exchanges, has a market cap of $40.3 billion. Top listed firms include Abu Qir Fertilizers, Alexandria Containers and Goods, and Commercial International Bank.

Kenya’s Nairobi Securities Exchange has a market capitalization of $13.6 billion. Safaricom, Equity Group Holdings, and East African Breweries Limited are its biggest listed companies. Founded in 1954, the NSE is the largest stock market in East Africa with 65 listed companies.

Investing in Africa’s vibrant markets has never been easier. Daba’s investment services offer personalized strategies to help you maximize returns and manage risk effectively. Download our app now to get started.

8. Stock Exchange of Mauritius (SEM) – $7,429,084,934.02

The SEM has a market cap of $7.4 billion, with top listings including MCB Group, Ireland Blyth, and SBM Holdings. Founded in 1989, the Stock Exchange of Mauritius (SEM) covers Mauritius and is based in Port Louis. 56 companies are quoted on the SEM’s official market, while another 42 are quoted on the Development and Enterprise Market (DEM).

9. Dar es Salaam Stock Exchange – $6,657,926,433.80

Tanzania’s Dar es Salaam Stock Exchange has a market capitalization of $6.7 billion. Located in Dar es Salaam, the commercial capital and largest city in Tanzania, it was incorporated in September 1996 and trading started in April 1998.

Rounding out the top 10 is the Ghana Stock Exchange with a market cap of $5.7 billion. Its major listed companies include Ecobank Transnational, AngloGold Ashanti Plc, and Access Bank Ghana.

The dynamic growth of African stock exchanges underscores the continent’s increasing significance in global finance. Daba is committed to providing reliable information, transparent services, and seamless investment experiences across these markets.

Whether you are looking to diversify your portfolio or explore emerging opportunities, Daba stands as your trusted partner in navigating Africa’s vibrant investment landscape.

Invest with Daba to leverage the potential of Africa’s leading stock markets and drive your financial growth. Download the app to get started today!

High Dividend Yields on African Stock Exchanges: The Key to Optimizing Your Investment Portfolio in Africa

Investors are always looking for ways to optimize their portfolios and maximize their returns. One of the most effective techniques is to leverage dividend yields, especially on African stock exchanges. In this article, we will explore this portfolio optimization strategy, examining its advantages, potential risks, and how the Daba investment platform can help you implement this technique. Let’s dive into how to optimize your investments in Africa with dividend yields

What is Portfolio Optimization through Dividends?

Portfolio optimization through dividends involves investing in stocks of companies that regularly pay high dividends. The dividend yield is the ratio of the annual dividend per share to the stock price. The higher the yield, the more passive income the investor receives.

Benefits of this Strategy

Generation of Passive Income: Dividends provide a regular cash flow, allowing investors to benefit from passive income in addition to potential capital gains.

Stability: Companies that regularly pay dividends are often well-established and financially stable, offering some security to investors.

Protection Against Market Volatility: High-dividend stocks can help mitigate the effects of market volatility, with dividend income offsetting potential stock price declines.

Potential Risks

Dividend Reduction or Suspension: Companies may decide to reduce or suspend their dividend payments based on their financial performance or strategy.

Lack of Growth: Companies paying high dividends may have fewer resources to devote to growth, limiting their potential for stock price appreciation.

High Stock Prices: Companies that regularly pay high dividends may see their stock prices increase rapidly, which can alter the yield for investors who buy these stocks at higher prices.

Example on the BRVM

Let’s take the example of BOA Benin, listed on the Regional Stock Exchange (BRVM). In May 2024, BOA Benin is expected to pay a dividend of 706 FCFA per share, representing a dividend yield of 10.17%. By investing in this stock before the ex-dividend date (23/05/2024), you can benefit from this attractive yield and optimize your portfolio.

How Daba Can Help You

The Daba investment platform simplifies access to investment opportunities on African stock exchanges, including the BRVM. With Daba, you can easily research and invest in high-dividend stocks while benefiting from tools and resources to make informed decisions.

To learn more about investing in the stock market on Daba, visit the Daba platform at https://daba.finance/app.

We invite you to consult our comprehensive guide on investing in the stock market on Daba, available here.

Conclusion

Portfolio optimization through dividends is a powerful strategy for investors seeking to generate passive income and potentially mitigate risks on African stock exchanges. By using the Daba platform, you can take advantage of this technique and access attractive investment opportunities. Start optimizing your portfolio now and build a stronger financial future on the African continent.

Contributed by Kyle Schutter, a Partner at Grant & Co.

To go public, or not…

I attended the Ibuka accelerator, a program to help get private companies listed, kickoff event in October at the Nairobi Securities Exchange.

The Kenyan stock exchange, being the largest in the region, is worth a close look.

The requirements for listing in Nairobi are minimal and it is not nearly as hard to list as people make it out to be. A company needs only 1 year of track record, doesn’t need to be profitable, only needs to list 15% of its shares, only needs a capitalization of about $100,000, and only needs to have 25 shareholders within a few months of listing.

So why aren’t more companies doing it?

The Lagos, Johannesburg, Mauritius, and Nairobi stock exchanges are the most promising places to go public in Africa. We will focus on the Nairobi Securities Exchange as a case study to enable us to deep dive.

Note: nothing here should be construed as an insult to Africa, Kenya, or the Nairobi Securities Exchange. I love Kenya and hope to work together to find solutions that keep increasing investment in and wealth of Africa.

Brand Problem

Listing is only one part of the problem; you must have someone buy your shares. Is there a market that wants to buy shares in these particular companies?

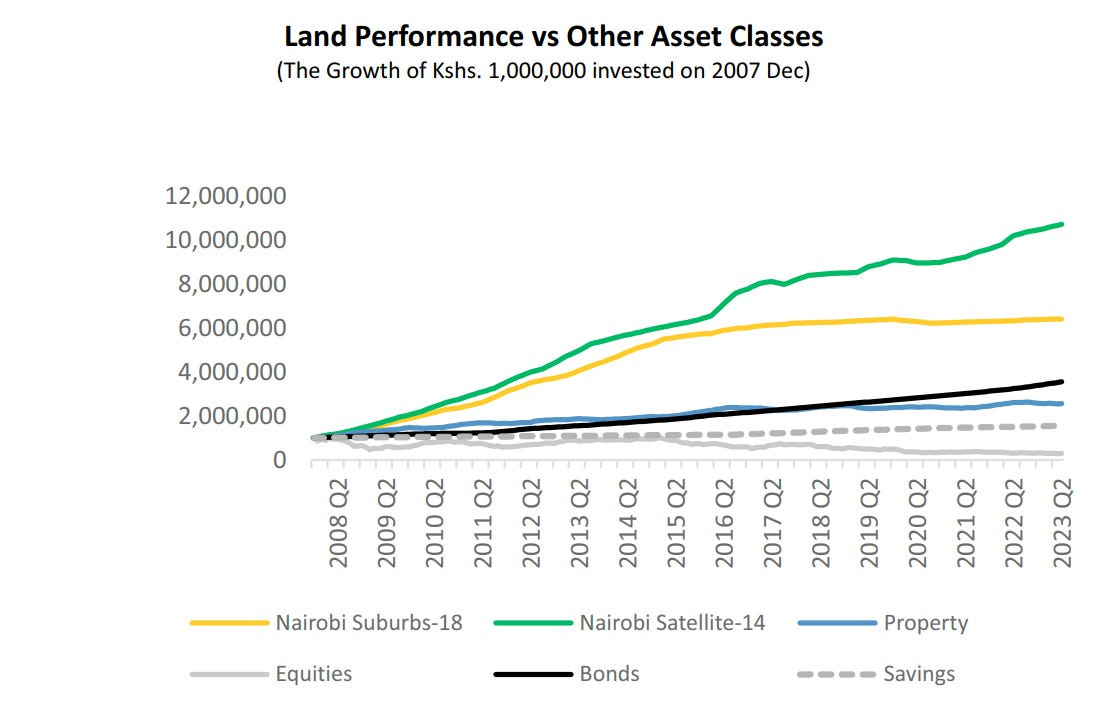

Kenyan equities (stocks) have not performed well, underperforming against bonds land, and even savings accounts. This isn’t a recent phenomenon, although the current economic downturn has worsened it. It has been going down for 8 years.

The NSE 20 index is down from 6,000 in 2015 to 1,400 in 2023.

Why take more risk with equities and get a lower return?

So, the brand name of Equities in Kenya and Africa is generally not good. What factors lead to this, and how can it be fixed?

Remember, Investing is a Keynesian Beauty Contest: the goal is not to pick the most beautiful investment but to pick the one that others think is the best. If Kenyan Equities have a bad brand and investors don’t think others will pick them, then no one will pick them, and they will go down.

Too hard to list… or too easy?

The requirements of the NSE (Nairobi Securities Exchange) are very entrepreneur-friendly, probably too friendly. There are two ways exchanges should maintain quality: ethics and financial performance. The NSE could improve on both accounts.

Ethics: the NSE has frozen the shares of Mumias and Kenya Airways, which prevents shareholders from liquidating their shares and props up the companies so they can keep operating rather than declare bankruptcy.

Financial Performance: Other stock exchanges delist companies if their share price or market capitalization falls too low. The electric scooter startup, Bird, once valued at $3.2b has now been delisted from NYSE because it failed to maintain the $15m market cap minimum threshold and has since gone bankrupt. Stocks that fall below $1.00 per share on the NYSE are also delisted. NSE could also set a minimum price to encourage management to improve performance or face the consequences of being delisted.

A leadership problem?

The Ibuka event had an enthusiastic vibe but maintained certain unfortunate* African stereotypes: the event started 1 hour late, and the presentation contained a major data inaccuracy. Timeliness and data integrity must be core to the culture of a stock exchange. *I likely maintained certain American stereotypes at the event: incessant, obnoxious questions. C’est le vie.

This suggests room for improvement in the NSE company culture and, consequently, for leadership improvement. According to publicly available information, the outgoing CEO of the NSE made Ksh31m (~$210,000), a 19% increase over the previous year, all while making only Ksh14m (~$100,000) for the exchange in profit, a drop of 90% from the previous year. This suggests a problem with his compensation package (and the compensation structuring at the NSE).

Overall, the NSE Equities market has been down since the NSE CEO was appointed 9 years ago, while the Kenyan economy has grown at ~5% a year. Having met him briefly, I had the impression the CEO of the NSE was more of a politician than a visionary who made things happen. Subsequent conversations with market players have not changed that impression.

A new CEO has been appointed as the current CEO has ended his two 4 year terms. Hopefully, new leadership will improve the company culture and results. But this 4-year term suggests more room for improvement: why not have the CEO’s tenure be based on performance? Stock exchanges like NYSE don’t have specific terms for their CEOs. But, perhaps the NSE is a quasi-parastatal. And with the “prestige” associated with running a public market there is a risk that new appointees will be based more on politics than competence and compensation will not be tied to results.

Furthermore, 8 years isn’t enough time to turn something around. A true visionary would want 15 good years to build something great. Imagine Steve Jobs had to leave Apple in 2005 before the iPhone came out. Or Elon had to leave before the Model S came out? The 2×4-year term could be disposed of.

The newly appointed CEO looks to be a strong choice. He is a lawyer/accountant and Partner from EY. We were hoping for an entrepreneur. Hopefully, he will be an entrepreneurial lawyer/accountant.

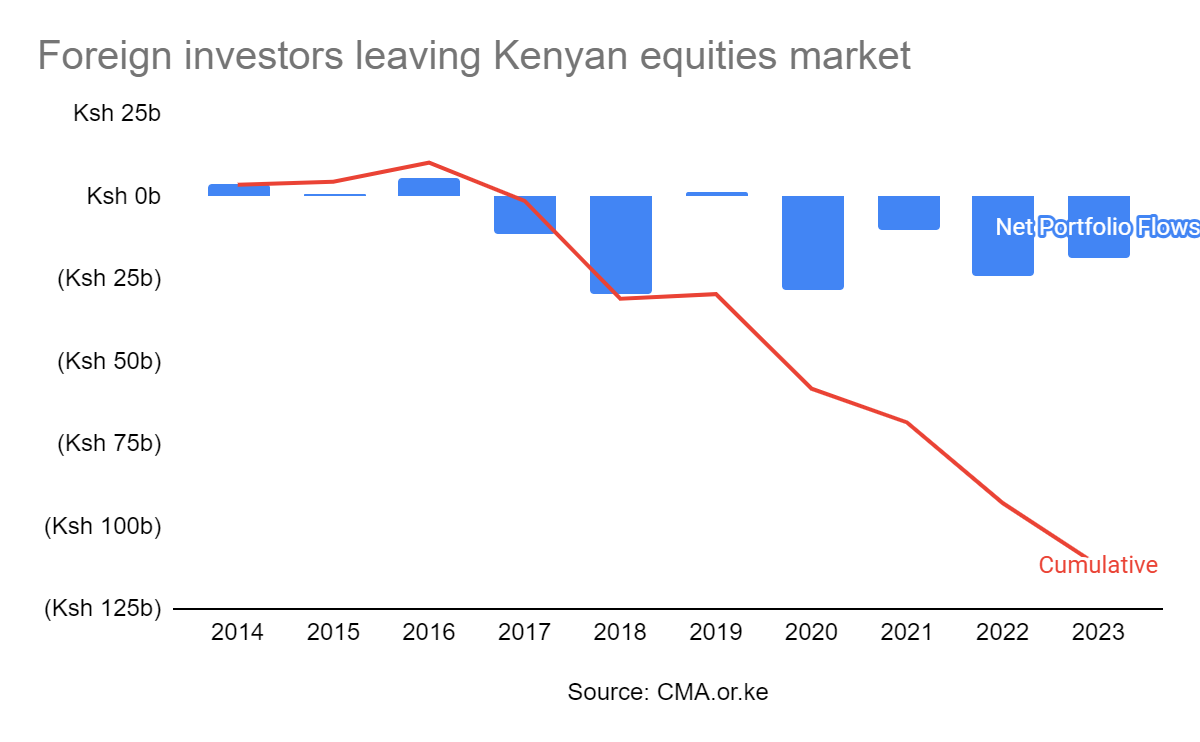

Capital flight?

Another explanation for poor NSE performance is that foreign investors are leaving the African stock markets, especially the Kenyan stock market.

However, the Ksh 125b loss due to foreign investors leaving is only part of why the NSE has lost Ksh 1.5 trillion in value since 2021. Capital flight explains less than 10% of the story.

Anti-Free Market behavior

Here are two examples:

The NSE has frozen the trading of Kenya Airlines and Mumias, both of which have substantial government ownership. Kenya Airlines shares have been frozen for 4 years, renewed annually each year with the explanation that Kenya Airways needed time to restructure. In 2022, Kenya Airways lost about $40m. In 2023, they lost about $150m. The more time they get to restructure, the worse it gets. Both companies should go bankrupt, and shareholders should be able to sell their shares. The exchange freezing shares makes investors nervous. By comparison, the NYSE only froze trading for 1 day, and that was when the World Trade Center buildings were attacked in 2001.

That the CEO of the CMA has attempted to put price floors on stock prices is concerning. “Capital Markets Authority (CMA) chief executive Wycliff Shamia told the Star that the move has been necessitated by the fact some of the companies have very strong fundamentals but the valuation is quite low.” Yes, this is how free markets work. The market decides what something is worth, not the government. The latter would be communism.

Preference for other investments

Investors would rather speculate on land because Kenya has no property tax. GoK should fairly tax other parts of the economy, like creating a 0.1 to 1% annual Property Tax on land so that people can’t just sit on their land and speculate without contributing to the economy. All other developed and emerging economies have an annual Property Tax; it’s time Kenya did the same. Property tax is generally recognized as the least bad tax for economic growth and yet Kenya doesn’t have it and isn’t even considering it. See here how property tax could be implemented in Kenya and make all parties happy. With the devolved county governments, this could more easily be accomplished than in the past.

The effect of no property tax is clear in the numbers: Kenyan real estate is 75x bigger than equities ($678b vs $9b); meanwhile, by comparison, US real estate is only 2x bigger than US equities ($96T vs $46T). The US equities market sources capital from around the world because people trust Uncle Sam to treat equities fairly, but people don’t (yet) trust Uncle Kamau to do the same. I think the lack of Property Tax is the nail in the coffin of the NSE, and without this reform, there can be no vibrant equities market. (Note: the only meaningful property tax that exists is the capital gains tax when a property is sold, and even then, people can easily underreport the sale price, which is much harder to do on a public equities market. Some counties like Nairobi charge property tax at around $5-30 per year, which is a joke. There is also a tax on Rental payments, but this is not a tax on the property but a tax on a business being done on the property, making matters worse by disincentivizing property development.)

Because Treasury Bonds are over 15%, investors put their money there rather than risk equities. Hopefully, after the Eurobond payment in June 2024, Treasury yields will reduce and more money will flow back to the equities market.

The opportunity

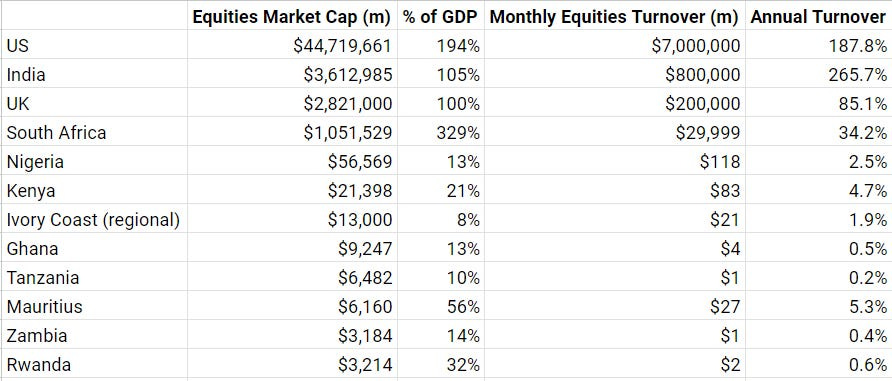

But there are reasons to be bullish on African stock markets. African markets, excluding South Africa, have a relatively small proportion of their GDP trading. There is room for the equities market to grow 10x to align with other markets like the US, South Africa, and India.

Further, Kenya is the region’s largest and most liquid market and could be a regional player—it is already one of the most liquid markets in Africa. By aggregating regional companies onto its exchange, NSE could grow another 10x. On top of that, GDP will compound to 63% growth over the next 10 years. This brings the total NSE market cap potential to ~630x growth over the next 10 years… if NSE can play its cards right. 630x growth would put the NSE in line with India, so it’s not impossible, as discussed below.

On top of that, Annual Turnover (trading of the shares) is relatively low compared to other markets at 4.7% on NSE, ~40x less trading than the US, adjusted for market cap.

There is room for more economic activity on African stock markets.

So where is this 630x growth going to come from?

Increase valuation. The P/E (price to earnings) ratio is only 4.9 on NSE, a sign that investors have low growth expectations. This is half its historical level and 1/4th the ~20 P/E seen on US exchanges, a 4x growth potential for NSE stocks. This is due to uncertainty, low expectations, and discounting for inflation.

More companies listing. About 1% of US companies are publicly listed compared to 0.001%ish (my guesstimate) of Kenyan companies. Realistically, 10x growth potential (as most Kenyan businesses are too small to go public).

NSE quality. If the NSE can improve quality that will improve investor confidence and 2-10x growth.

Virtuous Cycle. There are the compounding effects of a growing market, generating interest and crowding in more capital.

Encourage international investors on local trading platforms. Currently, American, Canadian, Singaporean, and other foreign investors are discouraged from investing through existing brokerage channels and online trading platforms as the regulations in those countries are too costly to manage given the small public market. But as the market grows and trading platforms enable more foreign investors you can imagine that as returns are becoming more predictable with lower returns in the West, some intrepid investors will take an interest in Africa. 2x opportunity

Distribution on international trading platforms. Like Robinhood, Charles Schwab, etc. 10x opportunity.

Cross-listing from other countries in East, Central, and Southern Africa. Theoretically, a 10x opportunity, but in reality, maybe a 2x. Already, some of this is happening. Bank of Kigali (Rwanda) and Umeme (Uganda) are listed in their own countries but cross-listed on NSE. Crosslisting is relatively easy. Evidence suggests that cross-listing increases company valuation, so the cost of cross-listing more than pays for itself. (Source: Peristiani, Federal Reserve Bank of New York, 2010) Old Mutual, for example, is cross-listed on 5 exchanges. A Kenyan equities lawyer confirmed this would be a workable strategy.

Behavioral nudges. There is no way for Kenyan trading apps to automatically reinvest dividends, while automatic reinvestment of dividends is possible in other markets like the US. This could boost share price by 5% per year. This would cut out stock brokers and their fees. My little research online suggests the CMA (Capital Markets Authority) currently prevents automatic dividend reinvestment due to pressure from stock brokers.

Better trading UX. New trading apps that make it easy to buy shares can 2x capital yet again. I tried to sign up with 6 different trading apps and brokers. 3 didn’t allow Americans, Dutch, Singaporeans, or Canadians to trade. The others each had cumbersome documentation requirements: one required a scanned copy of a notarized copy of my passport. What’s the point of a copy of something notarized? The friction to buy shares as a foreigner or local is severe.

Reduced trading fees. This is the big one. CDSC and other government entities can reduce the tax on trading, which is currently at 0.36%. If a stock is only expected to gain 10% a year, paying 0.36% per trade precludes an efficient market that quickly buys and sells. For comparison, the NYSE has a fee on trades of $0.001 (which comes to 0.003% for a typical $30/share stock, 1/100th the price of Kenyan fees). Broker fees are also extremely high in Kenya at 1-1.5%, 10x higher than in the US at 0-0.1%. Reducing fees would not directly increase market cap, but a 10x reduction in fees might increase liquidity 10x, bringing the NSE more in line with other exchanges, from 4.7% turnover to perhaps 50% turnover. Increasing liquidity would perhaps increase the market cap by 2-10x by increasing P/E and crowding in more companies.

Improving taxation. Right now, US investors in Kenyan companies get taxed twice. Thus, going through Mauritius is advantageous.

Case study 1:

I tried to sign up for various trading apps (Exness, Sterling, AIB-AXYS, ABC). Finally, after a week I was able to sign up on EFG Hermes. I tried to trade using the Market Price but the Market Price was 2x the Limit Price. I was told by customer service to ignore the Market Price. Once I did make a trade it took two days for my trade to be reflected in the app. After many customer service requests, my trade was reflected but then the app showed I had a negative account balance. After another customer service call that has been fixed. Then my password stopped working.

I can see why there might not be a lot of retail investors in Kenyan securities as the buying experience does not inspire confidence. But it does show an opportunity for someone to build a better trading experience.

Why are companies resistant to going public?

Before we determine whether listing at all would benefit companies, let’s consider:

does going public preclude a company from raising additional institutional capital?

what are the tax implications?

what are the compliance costs?

with interest rates as they are, is now really the right time to list?

Treasuries are 15% in Kenya at the moment, so raising equity is a hard sell. But global interest rates are unlikely to stay high, so perhaps a reduction down to 10% in the coming years will be good for equities. Also, land prices, the other investment option, may run out of room to grow further as rural land prices in Kenya are already about the same as rural land prices in the US, channeling more investment to equities.

Compliance costs are Kenyan SMEs’ most commonly cited problem for not listing. However, the compliance costs in Kenya are typically only around $5,000 a month, which they should be doing even as a private company, like maintaining a board of directors and informing shareholders of material changes. Thus, this argument from SMEs doesn’t hold water.

In an IPO, a company would sell at least 15% of its shares to raise additional capital. Some companies might be concerned with how they can raise more capital after the IPO. Never fear! There are several options:

Corporate Bond: this is just a loan with a maturity. Of note, there is no collateral required for this. Also, it has a bullet payment at the end, which gives the company some breathing room on repayment.

Private placement: a select group of investors are invited to buy shares in the company. This can be done even before a public offering and provides more privacy for the company.

Rights Issue: this is where shares are offered to existing shareholders only so they are not diluted. This funding method is fairly common in Kenya, though not as common in the US.

Secondary Offering: just like a rights issue but open to anyone. This is common in the US. Tesla, for example, has had 8 Secondary Offerings since 2012.