The world’s largest producer of cocoa, an annual GDP growth of +6.8% over the past decade, a stable currency pegged to the euro and increasing oil output.

Ivory Coast, a pillar of the West African Economic and Monetary Union (WAEMU), embodies a model of resilience and economic progress.

Despite past political challenges, including a civil war in early 2010, the country has strengthened its stability and democratic processes, creating a conducive environment for economic growth.

With a population of over 27 million, the nation has transformed its economy, showing a steady annual growth of 6.8% and an expanding stock market that has garnered global attention from investors.

Overcoming Economic Challenges

As the world’s leading producer of cocoa, Ivory Coast has maintained impressive economic growth with an annual GDP growth rate of 6.8% over the past decade. Even during the global slowdown caused by the COVID-19 pandemic, the country recorded a growth of 2% in 2020, outperforming many African nations.

The latest report from the African Development Bank describes it as one of the best-performing economies in the region, with a projected growth of 6.5% in 2024 (according to the IMF).

The Bourse Régionale des Valeurs Mobilières (BRVM), a regional stock exchange shared with other WAEMU countries (Senegal, Burkina Faso, Niger, Togo, Benin, Mali, Guinea Bissau), has seen its market capitalization increase by 40% over the last five years, with significant participation from Ivorian companies.

In 2022, the BRVM reached a trading volume of over $2 billion, demonstrating the growing interest in the country’s capital market.

Currency Stability, Energy Discoveries, and Positive Economic Projections Attract Investors

The CFA franc pegged to the euro, offers exchange rate stability, countering the volatility affecting other African currencies, such as the Nigerian naira, which lost nearly 70% of its value against the dollar in a year.

This stability, combined with recent oil and gas discoveries, spurred by a significant find by the Italian company Eni, has intensified investor interest, projecting a future of growing oil production.

The visit of Italian President Sergio Mattarella underscores the strategic importance of Italian-Ivorian relations, with projections envisioning oil production increasing to 200,000 barrels per day by 2026.

With a forecasted growth of 6.8% between 2024 and 2025, driven by hydrocarbon production and infrastructure investments, a reduction of the fiscal deficit to 3.5% by 2025 is expected, compared to 5.6% of GDP in 2022.

This consolidation is supported by effective government commitment recognized by international financial institutions.

Growing Demand for Financial Products

The economic expansion of Ivory Coast is stimulating demand for innovative financial products, leading to the emergence of platforms like Daba Finance.

“The lack of investment platforms focused on the Francophone West African region and the need to efficiently channel over $5 billion annually sent by the African diaspora to be invested in the continent, have led to the creation of Daba Finance,” says Anthony Miclet, Italian co-founder of Daba Finance.

Recently launched in the American and African markets, Daba Finance is a platform designed to meet the needs of investors seeking exposure to this dynamic market, offering investment opportunities in stocks, bonds, and African startups.

“The outdated and fragmented infrastructure of African capital markets makes it difficult for anyone to access high-quality investment opportunities on the continent. Daba aims to bridge this gap by providing a unified and user-friendly platform for investors interested in Africa,” adds Anthony Miclet.

With its focus on Francophone West Africa, particularly Ivory Coast, Daba Finance positions itself as a key entry point for investors looking to capitalize on the region’s economic growth prospects, stability offered by the CFA franc, and attractive dividends, ranging from 8% to 10%, offered by large companies listed on the BRVM such as Orange and Sonatel.

Thanks to sustained economic growth, a rising stock market, currency stability, and significant oil discoveries, Ivory Coast remains an excellent investment opportunity in Africa, maintaining its trajectory as a regional economic powerhouse.

L’inclusion dans la liste de Jeune Afrique témoigne du potentiel que Daba voit dans les secteurs dynamiques.

Lengo.ai, une startup qui utilise l’intelligence artificielle pour aider les détaillants informels à gérer leurs stocks, a été nommée l’une des 20 entreprises africaines en démarrage les plus prometteuses par le magazine Jeune Afrique.

Cette reconnaissance met en évidence la manière dont les entreprises technologiques africaines peuvent avoir un impact réel en résolvant les problèmes de manière innovante.

Le système d’assistance vocale de Lengo.ai comble le fossé entre les grands producteurs alimentaires et les petits détaillants en rationalisant la distribution. Cela démontre le potentiel de la technologie à transformer les industries et à améliorer les moyens de subsistance à travers le continent.

Chez Daba, notre engagement à favoriser la croissance économique et l’innovation en Afrique se manifeste par notre partenariat avec des startups comme Lengo.ai.

En tant que partie intégrante de notre portefeuille d’investissement, Lengo.ai représente un atout stratégique et met en avant notre rôle dans le soutien aux entreprises innovantes prêtes à diriger la révolution technologique en Afrique.

Grâce à notre plateforme, Daba offre aux investisseurs particuliers et institutionnels une exposition à une gamme d’opportunités, y compris des entreprises technologiques et commerciales pionnières comme Lengo.ai.

L’inclusion de la startup dans la liste de Jeune Afrique témoigne du potentiel que nous voyons dans ces secteurs dynamiques et souligne les types d’entreprises à fort impact que Daba cherche à soutenir.

On s’attend à ce que l’Afrique représente jusqu’à 40 % de la population humaine d’ici la fin du 21e siècle, le marché des produits de grande consommation étant positionné pour devenir son premier secteur industriel d’importance mondiale.

Pour plus de détails sur la manière dont Lengo.ai utilise l’IA pour transformer le commerce informel, et le rôle de Daba, vous pouvez lire l’étude de cas disponible en français et en anglais. Elle offre un aperçu du parcours de Lengo.ai et de l’approche de Daba pour identifier les startups prometteuses.

Investissez avec Daba aujourd’hui et faites partie du paysage technologique en plein essor de l’Afrique. Stimulez la croissance et l’innovation avec nous, en exploitant le riche potentiel et l’esprit entrepreneurial vibrant du continent.

Pour plus d’informations sur la manière d’investir avec Daba et pour découvrir d’autres histoires de réussite comme Lengo.ai, visitez notre site web.

Le potentiel économique florissant de l’Afrique offre d’immenses opportunités, mais attirer davantage d’investissements étrangers nécessite une position stratégique des entreprises à travers le continent.

En adoptant les bonnes stratégies, les entreprises africaines peuvent accroître leur attrait pour les investisseurs étrangers et débloquer un flot de capitaux pour alimenter l’innovation, la croissance et la résilience.

Stratégies pour les entreprises africaines afin d’attirer plus d’investissements étrangers

1. Préparer l’Investissement

La base de l’attraction des investissements directs étrangers réside dans le fait de s’assurer que vos opérations, vos finances et votre gouvernance sont conformes aux meilleures pratiques internationales. Les investisseurs recherchent des entreprises ayant des fondamentaux solides, des normes mondiales et un engagement envers la transparence.

Les entreprises africaines doivent prioriser la professionnalisation de leurs opérations avant de se lancer dans des démarches de collecte de fonds. Cela inclut la mise en œuvre de rapports financiers solides, le renforcement de la gouvernance d’entreprise et le respect des exigences de conformité spécifiques à l’industrie.

2. Exploiter les Plateformes d’Accès aux Investissements

Rejoindre des plateformes de collecte de fonds panafricaines peut considérablement accroître la visibilité et fournir des canaux de transactions vérifiés que les investisseurs étrangers font confiance.

Ces plateformes rationalisent le flux de transactions à grande échelle, connectant les entreprises africaines à un réseau mondial d’investisseurs recherchant activement des opportunités sur le continent. En exploitant ces plateformes, les entreprises africaines peuvent efficacement présenter leur potentiel à un public ciblé de parties intéressées.

Êtes-vous une startup ou une entreprise en phase de démarrage cherchant à stimuler votre expansion ? Daba se spécialise dans la fourniture de solutions complètes de collecte de fonds conçues pour propulser votre entreprise vers de nouveaux sommets. Consultez dès maintenant cette page sur notre site web et découvrez comment nous pouvons vous aider à accéder aux ressources dont vous avez besoin pour prospérer.

3. Mettre en Avant les Secteurs à Fort Potentiel

Pour captiver l’attention des investisseurs étrangers, il est crucial de mettre en avant les industries à fort potentiel du continent au-delà des récits traditionnels de matières premières et d’extraction. L’Afrique compte de nombreux secteurs prometteurs, notamment la technologie financière, l’agroalimentaire, les énergies renouvelables, les infrastructures et les technologies de l’information.

En mettant en avant les perspectives de croissance et les opportunités inexploitées dans ces secteurs, les entreprises africaines peuvent communiquer efficacement le paysage économique diversifié du continent et attirer des investissements alignés sur les tendances mondiales.

4. Promouvoir les Success Stories et la Preuve Sociale

Lorsque les entreprises africaines démontrent des rendements solides aux premiers investisseurs étrangers, la promotion de ces success stories peut inspirer confiance et attirer davantage d’investissements.

Le succès engendre le succès, et en mettant en avant des cas exemplaires de projets rentables, les entreprises africaines peuvent tirer parti de la preuve sociale pour convertir les sceptiques et débloquer des flux de capitaux supplémentaires. Ces success stories servent de puissants témoignages du potentiel d’investissement en Afrique.

5. Mettre l’Accent sur l’Impact Économique Inclusif

À une époque où les investisseurs accordent de plus en plus d’importance aux normes environnementales, sociales et de gouvernance (ESG), les entreprises africaines doivent souligner comment leurs activités contribuent à la création d’emplois durables, au développement des compétences, à l’autonomisation des femmes et à la résilience climatique.

En s’alignant sur ces priorités mondiales, les entreprises africaines peuvent se positionner comme des catalyseurs de la croissance économique inclusive, en résonance avec les valeurs et les objectifs des investisseurs socialement responsables.

Déverrouillez les portes de la croissance pour votre entreprise en phase de démarrage. Daba propose des solutions de collecte de fonds sur mesure pour aider les startups à obtenir les financements dont elles ont besoin. Visitez dès aujourd’hui la page dédiée aux startups de notre site web pour découvrir nos services et franchir la première étape vers la réalisation de vos rêves entrepreneuriaux.

Avec une approche stratégique et un engagement envers l’excellence, les entreprises africaines peuvent surmonter les obstacles historiques et débloquer le vaste potentiel que les investissements directs étrangers représentent pour la transformation économique du continent.

En adoptant ces stratégies, l’Afrique peut ouvrir la voie à un avenir de prospérité, d’innovation et de croissance durable, alimenté par l’afflux de capitaux mondiaux.

La collecte de fonds peut être un défi intimidant pour les startups et les entreprises en phase de démarrage. Daba est là pour simplifier le processus avec nos solutions expertes de collecte de fonds. Visitez notre site web dès aujourd’hui pour découvrir comment nos services peuvent vous aider à naviguer dans le paysage de la collecte de fonds et à sécuriser les investissements qui stimulent votre croissance.

Africa’s booming economic potential holds immense opportunities, but attracting increased foreign investment requires strategic positioning by companies across the continent.

By adopting the right strategies, African enterprises can boost their appeal to overseas investors and unlock a torrent of capital to fuel innovation, growth, and resilience.

Strategies for African companies to get more foreign investments

1. Build Investment Readiness

The foundation of attracting FDI lies in ensuring that your operations, financials, and governance adhere to international best practices. Investors seek companies with sound fundamentals, global standards, and a commitment to transparency.

African enterprises must prioritize professionalizing their operations before embarking on fundraising endeavors. This includes implementing robust financial reporting, strengthening corporate governance, and adhering to industry-specific compliance requirements.

2. Leverage Investment Access Platforms

Joining pan-African fundraising platforms like Daba can significantly expand visibility and provide vetted deal channels that overseas investors trust. These platforms streamline deal flow at scale, connecting African companies with a global network of investors actively seeking opportunities on the continent.

By leveraging these platforms, African enterprises can effectively showcase their potential to a targeted audience of interested parties.

Are you a startup or early-stage company seeking to fuel your expansion? Daba provides comprehensive capital-raising solutions to propel your business. Check out this page on our website now and discover how we can help you access the resources you need to thrive.

3. Highlight High-Potential Sectors

To captivate the attention of foreign investors, it is crucial to highlight the continent’s high-potential industries beyond traditional narratives of commodities and extraction. Africa boasts numerous promising sectors, including fintech, agribusiness, renewable energy, infrastructure, and information technology.

By showcasing the growth prospects and untapped opportunities within these sectors, African companies can effectively communicate the continent’s diverse economic landscape and attract investment aligned with global trends.

4. Promote Success Stories and Social Proof

When African ventures demonstrate strong returns to early overseas backers, promoting these success stories can inspire confidence and attract further investment.

Success breeds success, and by highlighting exemplary cases of profitable ventures, African companies can leverage social proof to convert skeptics and unlock additional capital inflows. These success stories serve as powerful testaments to the potential of investing in Africa.

5. Emphasize Inclusive Economic Impact

In an era where investors increasingly prioritize environmental, social, and governance (ESG) standards, African companies must emphasize how their enterprises drive sustainable job creation, skills development, women’s empowerment, and climate resilience.

By aligning with these global priorities, African businesses can position themselves as catalysts for inclusive economic growth, resonating with the values and objectives of socially responsible investors.

Unlock the doors to growth for your early-stage venture. Daba offers tailored capital-raising solutions to help startups secure the funding they need. Visit the startups page of our website today to explore our services.

With a strategic approach and a commitment to excellence, African companies can overcome historical barriers and unlock the vast potential that foreign direct investment holds for the continent’s economic transformation.

By adopting these strategies, Africa can pave the way for a future of prosperity, innovation, and sustainable growth, fueled by the influx of global capital.

Raising capital can be a daunting challenge for startups and early-stage companies. Daba is here to simplify the process with our expert capital-raising solutions. Reach out to us today to learn how our services can help you navigate the fundraising landscape and secure the investments that drive your growth.

La part relative du stock d’IDE de l’Afrique en provenance d’Europe a diminué au cours de la dernière décennie, tandis que celle de l’Asie a augmenté.

L’investissement direct étranger (IDE) se produit lorsqu’une personne ou une entreprise d’un pays investit dans une entreprise d’un autre pays et en prend le contrôle significatif, généralement en possédant 10 % ou plus de son pouvoir de vote.

L’IDE est crucial pour relier les économies à l’échelle mondiale, car il établit des liens durables entre elles. C’est un moyen vital pour que la technologie circule entre les pays, stimule le commerce international en offrant un accès à de nouveaux marchés, et joue un rôle majeur dans la croissance économique.

Ainsi, nous discutons des principaux pays qui représentent la plus grande part des flux d’IDE vers les marchés africains. Mais d’abord, pourquoi l’IDE est-il important pour l’Afrique, et quelles sont les dernières tendances en matière d’investissement direct étranger sur le continent ?

Pourquoi l’Investissement Étranger est-il Important pour l’Afrique ?

Pour l’Afrique, l’IDE est crucial pour plusieurs raisons. Premièrement, il apporte un capital indispensable pour le développement des infrastructures, la création d’emplois et le transfert de technologie, qui sont essentiels à la croissance économique.

L’IDE facilite également la diversification des économies en introduisant de nouvelles industries et en améliorant celles qui existent déjà. De plus, il favorise le commerce et renforce l’intégration économique mondiale en connectant les marchés africains aux réseaux internationaux.

En outre, l’IDE s’accompagne souvent d’expertise, de compétences en gestion et d’un accès aux marchés mondiaux, ce qui peut aider les entreprises locales à s’étendre et à devenir plus compétitives.

En outre, il favorise l’innovation et les améliorations de productivité grâce aux transferts de connaissances et à la diffusion de la technologie. Enfin, l’IDE contribue à la stabilité des économies africaines en fournissant une source stable de financement externe et en réduisant la dépendance à l’égard de sources volatiles telles que l’aide étrangère ou les exportations de produits de base.

Ne manquez pas les opportunités d’investissement exclusives en Afrique ! Téléchargez dès aujourd’hui l’application Daba et débloquez un monde de retours potentiels tout en ayant un impact positif.

Dernières Tendances des Flux d’IDE vers l’Afrique

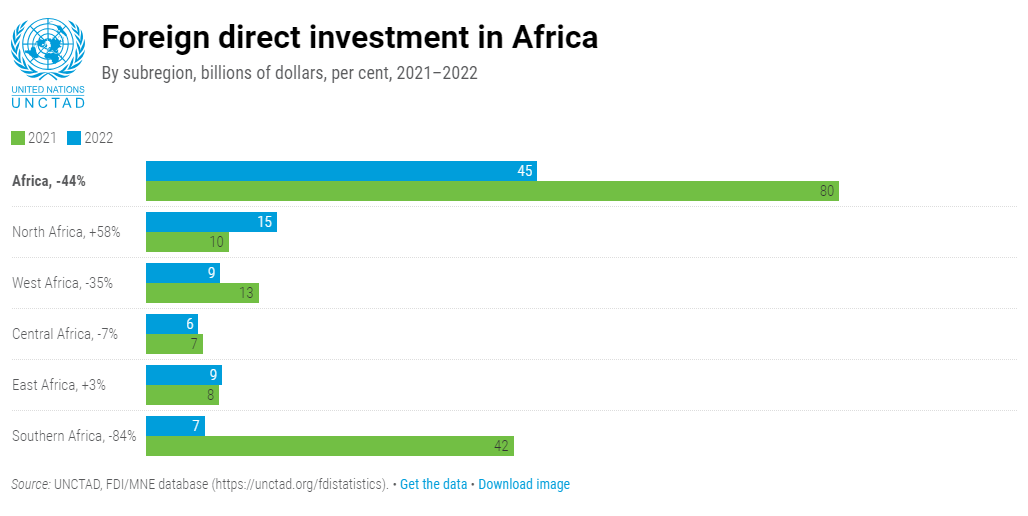

Le Rapport sur l’Investissement Mondial de la CNUCED pour l’année 2023 révèle que les investissements étrangers en provenance de l’étranger vers l’Afrique sont passés à 45 milliards de dollars en 2022, contre un record de 80 milliards de dollars en 2021. Cela représentait 3,5 % de l’investissement mondial total.

En Afrique du Nord, l’Égypte a vu un gros bond des investissements étrangers à 11 milliards de dollars en raison de plus d’entreprises achetant et fusionnant. Le nombre de nouveaux projets annoncés a plus que doublé pour atteindre 161. Les accords pour des projets internationaux ont également augmenté des deux tiers pour atteindre 24 milliards de dollars. Cependant, l’investissement au Maroc a légèrement baissé de 6 % pour atteindre 2,1 milliards de dollars.

En Afrique de l’Ouest, le Nigeria a enregistré un investissement étranger négatif de -187 millions de dollars car certains investisseurs se sont retirés. Mais le nombre de nouveaux projets a augmenté de 24 % pour atteindre 2 milliards de dollars. L’investissement au Sénégal est resté le même à 2,6 milliards de dollars, tandis que le Ghana a vu une diminution de 39 % pour atteindre 1,5 milliard de dollars.

En Afrique de l’Est, l’investissement en Éthiopie a chuté de 14 % pour atteindre 3,7 milliards de dollars, mais il a quand même reçu le deuxième investissement étranger le plus important sur le continent. L’investissement en Ouganda a augmenté de 39 % pour atteindre 1,5 milliard de dollars en raison d’investissements dans l’extraction de ressources. La Tanzanie a enregistré une augmentation de 8 % pour atteindre 1,1 milliard de dollars.

En Afrique Centrale, l’investissement en République Démocratique du Congo est resté le même à 1,8 milliard de dollars, principalement grâce aux investissements dans les champs pétrolifères et l’exploitation minière.

En Afrique Australe, l’investissement étranger en Afrique du Sud s’est élevé à 9 milliards de dollars, moins qu’en 2021 mais le double de la moyenne des dix dernières années. En Zambie, après deux années de pertes, l’investissement étranger a augmenté pour atteindre 116 millions de dollars.

Vous recherchez une chance de faire la différence tout en obtenant des retours. Rendez-vous sur notre application pour commencer à investir dans la croissance de l’Afrique dès aujourd’hui !

Au cours des cinq dernières années, l’investissement étranger a augmenté dans quatre des groupes économiques en Afrique.

L’investissement dans le Marché Commun de l’Afrique Orientale et Australe a augmenté de 14 % pour atteindre 22 milliards de dollars. Il a également augmenté dans la Communauté de Développement de l’Afrique Australe (multiplié par quatre pour atteindre 10 milliards de dollars), l’Union Économique et Monétaire Ouest Africaine (doublant pour atteindre 5,2 milliards de dollars), et la Communauté d’Afrique de l’Est (en hausse de 9 % pour atteindre 3,8 milliards de dollars).

De manière générale, les destinations de l’IDE en Afrique ont évolué au cours de la dernière décennie, avec l’Afrique du Nord et l’Afrique Australe – qui représentaient la majorité de l’IDE à mi-2000 – perdant des parts d’IDE au profit de l’Afrique de l’Est.

Sources des Flux d’IDE vers l’Afrique

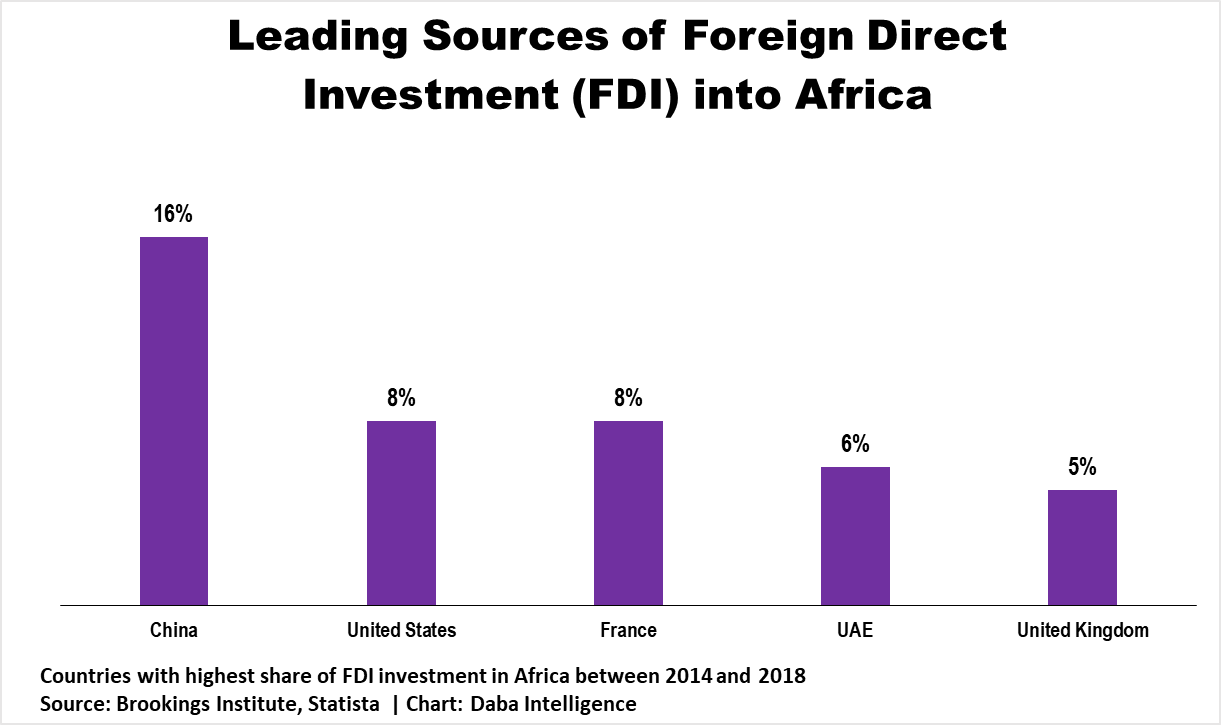

Les investisseurs européens restent la source la plus importante de stock d’IDE en Afrique, avec en tête le Royaume-Uni (60 milliards de dollars), la France (54 milliards de dollars), et les Pays-Bas (54 milliards de dollars) au cours des cinq dernières années.

Mais la part relative du stock d’IDE de l’Afrique provenant de l’Europe a diminué au cours de la dernière décennie, tandis que la part de l’Asie a augmenté – la Chine étant actuellement en tête.

Nous explorons les principales sources des flux d’IDE vers l’Afrique, sur la base des données de la recherche de l’Institut Brookings de l’année 2014 à 2018.

Chine

La Chine est le plus grand investisseur mondial en Afrique en termes de capital total. Elle a investi plus de 72 milliards de dollars sur le continent de 2014 à 2018. Cet investissement a créé plus de 137 000 emplois à travers 259 projets.

France

La France a investi 34 milliards de dollars en Afrique sur la même période, créant 58 000 emplois dans 329 projets. Les investissements de la France sont cruciaux pour ses anciennes colonies en Afrique, telles que le Nigeria, le Maroc, l’Algérie et la Côte d’Ivoire.

États-Unis

L’investissement direct américain en Afrique s’est élevé à près de 31 milliards de dollars de 2014 à 2018. Les États-Unis étaient responsables de 463 projets sur le continent, soit le plus grand nombre par rapport à tout autre pays. Ces projets ont créé 62 000 emplois. Les entreprises américaines continuent de rechercher des opportunités d’investissement en Afrique.

Vous voulez franchir la prochaine étape pour exploiter le potentiel d’investissement de l’Afrique ? Rendez-vous sur notre site Web ou téléchargez dès maintenant l’application Daba pour commencer votre voyage.

Émirats Arabes Unis

Les Émirats Arabes Unis (EAU) ont versé plus de 25 milliards de dollars en Afrique au cours de quatre années. Cela est logique étant donné la proximité des Émirats Arabes Unis avec l’Afrique de l’Est, car ils se trouvent à l’extrémité orientale de la péninsule arabique.

Les investissements en capital des Émirats Arabes Unis en Afrique devraient augmenter fortement dans les années à venir : Le gouvernement en 2020 a annoncé une initiative de 500 millions de dollars pour aider la jeunesse africaine et numériser les ressources.

Fin 2019, les Émirats Arabes Unis ont déclaré finaliser un accord de libre-échange avec un consortium de pays africains, et le mois dernier, ils ont signé un accord de 35 milliards de dollars avec l’Égypte pour développer un tronçon stratégique de la côte méditerranéenne du pays nord-africain.

Royaume-Uni

Le Royaume-Uni a investi près de 18 milliards de dollars en Afrique de 2014 à 2018, couvrant 286 projets et créant 41 000 emplois. Le Royaume-Uni, comme la France, entretient toujours des liens forts avec ses anciennes colonies en Afrique, telles que Sierra Leone, le Kenya, le Zimbabwe, l’Ouganda, la Zambie, la Tanzanie et l’Égypte.

Entre 2014 et 2018, l’investissement direct chinois sur le continent africain représentait la principale source d’IDE.

Pourquoi Plus de Pays Investissent en Afrique

L’Afrique représente un marché significatif et inexploité pour l’investissement étranger. Ses 54 pays abritent 1,3 milliard de personnes, dont beaucoup sont jeunes et auront besoin de bons emplois dans les années à venir, ainsi qu’une abondance de ressources naturelles, du pétrole à l’or en passant par les diamants et le lithium.

De plus, la Zone de Libre-Échange Continentale Africaine (ZLECAF), qui relie 1,3 milliard de personnes de 55 pays, offre une grande chance pour l’économie africaine de croître et entraînera très probablement plus d’investissements étrangers en Afrique en réduisant les règles et en facilitant l’accès aux nouveaux marchés.

Comment les investisseurs peuvent-ils se positionner au mieux pour saisir les opportunités découlant de ces développements rapides dans le paysage d’investissement en Afrique ?

Contactez-nous chez Daba pour vous guider dans le voyage de l’investissement en Afrique, que vous soyez un investisseur individuel ou institutionnel. Téléchargez notre application, remplissez ce formulaire sur notre site Web ou discutez avec notre équipe sur WhatsApp pour commencer.

The relative share of Africa’s FDI stock originating from Europe declined in the last decade, while Asia’s share increased—with China currently leading the pack.

Foreign direct investment (FDI) is when a person or business from one country invests in and gains significant control over a company in another country, typically by owning 10% or more of its voting power.

FDI is crucial for connecting economies globally, as it establishes lasting ties between them. It’s a vital way for technology to move between countries, boosts international trade by providing access to new markets, and plays a big role in driving economic growth.

As such, we discuss the top countries that account for the largest share of FDI flows into African markets. But first, why is FDI important to Africa, and what are the latest foreign direct investment trends on the continent?

Why Is Foreign Investment Important To Africa?

For Africa, FDI is crucial for several reasons. Firstly, it brings in much-needed capital for infrastructure development, job creation, and technology transfer, which are essential for economic growth.

FDI also facilitates the diversification of economies by introducing new industries and enhancing existing ones. Moreover, it promotes trade and strengthens global economic integration by connecting African markets with international networks.

In addition, FDI often comes with expertise, managerial skills, and access to global markets, which can help local businesses expand and become more competitive.

Furthermore, it fosters innovation and productivity enhancements through knowledge spillovers and technology diffusion. Lastly, FDI contributes to the stability of African economies by providing a stable source of external financing and reducing reliance on volatile sources like foreign aid or commodity exports.

Don’t miss out on exclusive investment opportunities in Africa! Download the Daba app today and unlock a world of potential returns while making a positive impact.

Latest Trends in FDI Flows to Africa

UNCTAD’s World Investment Report 2023 reveals that money invested from abroad into Africa dropped to $45 billion in 2022 from a record high of $80 billion in 2021. This made up 3.5% of the total global investment.

In North Africa, Egypt saw a big jump in foreign investment to $11 billion due to more companies buying and merging. The number of new projects announced more than doubled to 161. Deals for international projects also went up by two-thirds to $24 billion. However, investment in Morocco went down a bit by 6% to $2.1 billion.

In West Africa, Nigeria experienced negative foreign investment of -$187 million because some investors pulled out. But new projects increased by 24% to $2 billion. Investment in Senegal stayed the same at $2.6 billion, while Ghana saw a decrease of 39% to $1.5 billion.

In East Africa, investment in Ethiopia dropped by 14% to $3.7 billion, but it still received the second most foreign investment on the continent. Uganda’s investment went up by 39% to $1.5 billion due to investments in extracting resources. Tanzania saw an increase of 8% to $1.1 billion.

In Central Africa, investment in the Democratic Republic of the Congo stayed the same at $1.8 billion, mainly from investments in oil fields and mining.

In Southern Africa, foreign investment in South Africa was $9 billion, less than in 2021 but double the average of the last ten years. In Zambia, after two years of losses, foreign investment increased to $116 million.

Looking for a chance to make a difference while earning returns. Head over to our app to start investing in Africa’s growth today!

Over the past five years, foreign investment has increased in four of the economic groups in Africa.

Investment in the Common Market for Eastern and Southern Africa went up by 14% to $22 billion. It also increased in the Southern African Development Community (rising four times to $10 billion), the West African Economic and Monetary Union (doubling to $5.2 billion), and the East African Community (up by 9% to $3.8 billion).

Generally, the destinations of FDI in Africa have shifted over the last decade, with Northern and Southern Africa—which made up the majority of FDI stock in the mid-2000s—losing FDI share to Eastern Africa.

Sources of FDI Flows to Africa

European investors remain the most important source of FDI stock in Africa, led by the United Kingdom ($60 billion), France ($54 billion), and the Netherlands ($54 billion) over the past five years.

But the relative share of Africa’s FDI stock originating from Europe declined in the last decade, while Asia’s share increased—with China currently leading the pack.

We explore the leading sources of FDI flows to Africa, based on data from the Brookings Institute research from the year 2014 to 2018.

China

China is the world’s largest investor in Africa in terms of total capital. They invested more than $72 billion in the continent from 2014 to 2018. That investment created more than 137,000 jobs across 259 projects.

France

France invested $34 billion in Africa over the same period, creating 58,000 jobs in 329 projects. France’s investments are crucial to its former colonies in Africa, such as Nigeria, Morocco, Algeria, and the Ivory Coast.

The United States

American direct investment in Africa was nearly $31 billion from 2014 to 2018. The United States was responsible for a total of 463 projects on the continent, the most of any other country. These projects created 62,000 jobs. American companies continue to seek investment opportunities in Africa.

Want to take the next step in tapping Africa’s investment potential? Head over to our website or download the Daba app now to start your journey.

United Arab Emirates

The United Arab Emirates (UAE) poured more than $25 billion into Africa over four years. This makes sense given the UAE’s proximity to eastern Africa as it sits on the eastern edge of the Arabian peninsula.

The UAE’s capital investments in Africa are expected to rise sharply in the coming years: The government 2020 announced a $500 million initiative to help Africa’s youth and digitize resources.

In late 2019, the UAE said it was finalizing a free trade agreement with a consortium of African countries, and last month, it signed a $35 billion deal with Egypt to develop a prime stretch of the North African country’s Mediterranean coast.

United Kingdom

The United Kingdom invested nearly $18 billion in Africa from 2014 to 2018, covering 286 projects and creating 41,000 jobs. Britain, like France, still has strong ties to its former colonies in Africa, such as Sierra Leone, Kenya, Zimbabwe, Uganda, Zambia, Tanzania, and Egypt.

Between 2014 and 2018, Chinese direct investment in the African continent represented the main source of FDI.

Why More Countries Are Investing in Africa

Africa represents a significant untapped market for foreign investment. Its 54 countries are home to 1.3 billion people, many of whom are young and will need good jobs in the coming years, and an abundance of natural resources from oil and gold to diamonds and lithium.

In addition, the African Continental Free Trade Area (AfCFTA), which links 1.3 billion people from 55 countries, offers a big chance for Africa’s economy to grow and is poised to draw more foreign investment into its markets by cutting down rules and making it easier to reach new markets.

How can investors best position themselves to capture opportunities arising from these rapid developments in Africa’s investment landscape?

Reach out to us at Daba to guide you on the journey of investing in Africa, whether you’re an individual or institutional investor. Download our app, fill out this form on our website, or chat with our team on WhatsApp to get started.

Contributed by Kyle Schutter, a Partner at Grant & Co.

To go public, or not…

I attended the Ibuka accelerator, a program to help get private companies listed, kickoff event in October at the Nairobi Securities Exchange.

The Kenyan stock exchange, being the largest in the region, is worth a close look.

The requirements for listing in Nairobi are minimal and it is not nearly as hard to list as people make it out to be. A company needs only 1 year of track record, doesn’t need to be profitable, only needs to list 15% of its shares, only needs a capitalization of about $100,000, and only needs to have 25 shareholders within a few months of listing.

So why aren’t more companies doing it?

The Lagos, Johannesburg, Mauritius, and Nairobi stock exchanges are the most promising places to go public in Africa. We will focus on the Nairobi Securities Exchange as a case study to enable us to deep dive.

Note: nothing here should be construed as an insult to Africa, Kenya, or the Nairobi Securities Exchange. I love Kenya and hope to work together to find solutions that keep increasing investment in and wealth of Africa.

Brand Problem

Listing is only one part of the problem; you must have someone buy your shares. Is there a market that wants to buy shares in these particular companies?

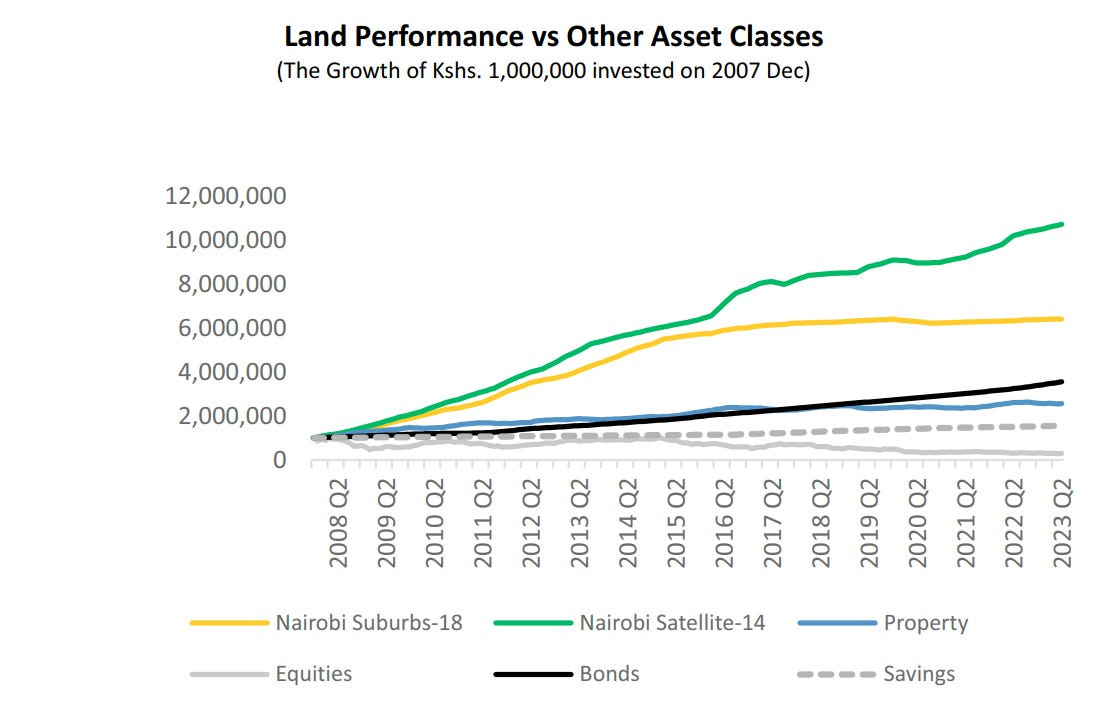

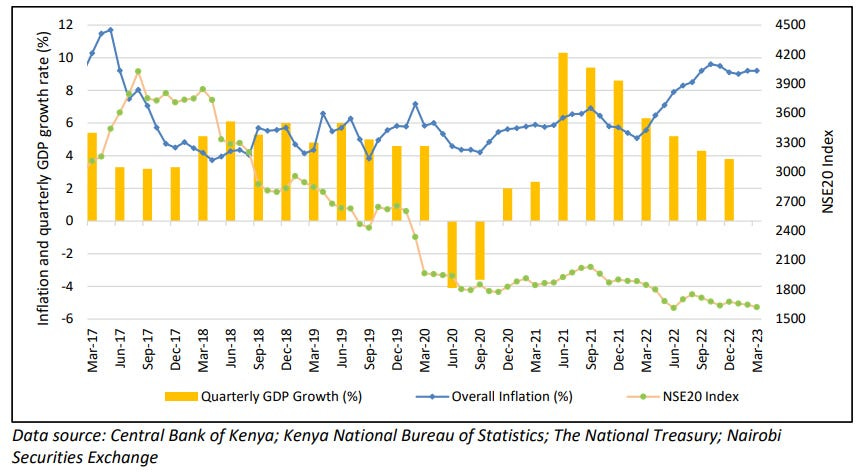

Kenyan equities (stocks) have not performed well, underperforming against bonds land, and even savings accounts. This isn’t a recent phenomenon, although the current economic downturn has worsened it. It has been going down for 8 years.

The NSE 20 index is down from 6,000 in 2015 to 1,400 in 2023.

Why take more risk with equities and get a lower return?

So, the brand name of Equities in Kenya and Africa is generally not good. What factors lead to this, and how can it be fixed?

Remember, Investing is a Keynesian Beauty Contest: the goal is not to pick the most beautiful investment but to pick the one that others think is the best. If Kenyan Equities have a bad brand and investors don’t think others will pick them, then no one will pick them, and they will go down.

Too hard to list… or too easy?

The requirements of the NSE (Nairobi Securities Exchange) are very entrepreneur-friendly, probably too friendly. There are two ways exchanges should maintain quality: ethics and financial performance. The NSE could improve on both accounts.

Ethics: the NSE has frozen the shares of Mumias and Kenya Airways, which prevents shareholders from liquidating their shares and props up the companies so they can keep operating rather than declare bankruptcy.

Financial Performance: Other stock exchanges delist companies if their share price or market capitalization falls too low. The electric scooter startup, Bird, once valued at $3.2b has now been delisted from NYSE because it failed to maintain the $15m market cap minimum threshold and has since gone bankrupt. Stocks that fall below $1.00 per share on the NYSE are also delisted. NSE could also set a minimum price to encourage management to improve performance or face the consequences of being delisted.

A leadership problem?

The Ibuka event had an enthusiastic vibe but maintained certain unfortunate* African stereotypes: the event started 1 hour late, and the presentation contained a major data inaccuracy. Timeliness and data integrity must be core to the culture of a stock exchange. *I likely maintained certain American stereotypes at the event: incessant, obnoxious questions. C’est le vie.

This suggests room for improvement in the NSE company culture and, consequently, for leadership improvement. According to publicly available information, the outgoing CEO of the NSE made Ksh31m (~$210,000), a 19% increase over the previous year, all while making only Ksh14m (~$100,000) for the exchange in profit, a drop of 90% from the previous year. This suggests a problem with his compensation package (and the compensation structuring at the NSE).

Overall, the NSE Equities market has been down since the NSE CEO was appointed 9 years ago, while the Kenyan economy has grown at ~5% a year. Having met him briefly, I had the impression the CEO of the NSE was more of a politician than a visionary who made things happen. Subsequent conversations with market players have not changed that impression.

A new CEO has been appointed as the current CEO has ended his two 4 year terms. Hopefully, new leadership will improve the company culture and results. But this 4-year term suggests more room for improvement: why not have the CEO’s tenure be based on performance? Stock exchanges like NYSE don’t have specific terms for their CEOs. But, perhaps the NSE is a quasi-parastatal. And with the “prestige” associated with running a public market there is a risk that new appointees will be based more on politics than competence and compensation will not be tied to results.

Furthermore, 8 years isn’t enough time to turn something around. A true visionary would want 15 good years to build something great. Imagine Steve Jobs had to leave Apple in 2005 before the iPhone came out. Or Elon had to leave before the Model S came out? The 2×4-year term could be disposed of.

The newly appointed CEO looks to be a strong choice. He is a lawyer/accountant and Partner from EY. We were hoping for an entrepreneur. Hopefully, he will be an entrepreneurial lawyer/accountant.

Capital flight?

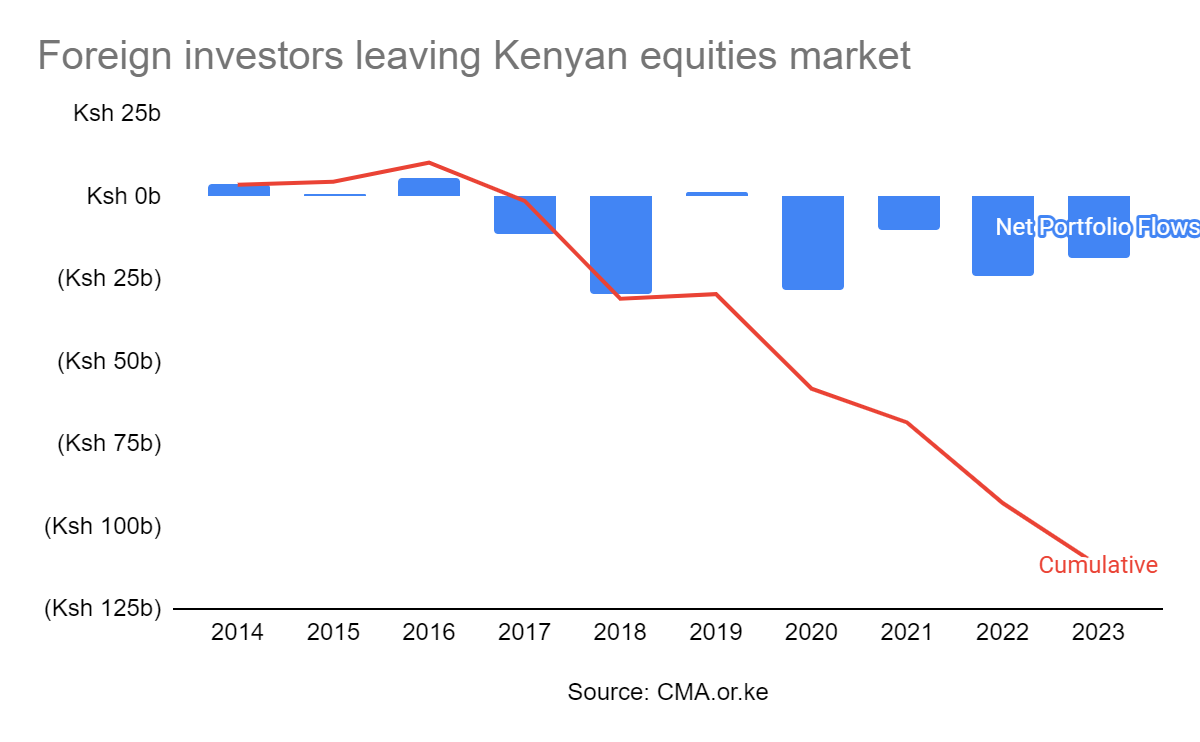

Another explanation for poor NSE performance is that foreign investors are leaving the African stock markets, especially the Kenyan stock market.

However, the Ksh 125b loss due to foreign investors leaving is only part of why the NSE has lost Ksh 1.5 trillion in value since 2021. Capital flight explains less than 10% of the story.

Anti-Free Market behavior

Here are two examples:

The NSE has frozen the trading of Kenya Airlines and Mumias, both of which have substantial government ownership. Kenya Airlines shares have been frozen for 4 years, renewed annually each year with the explanation that Kenya Airways needed time to restructure. In 2022, Kenya Airways lost about $40m. In 2023, they lost about $150m. The more time they get to restructure, the worse it gets. Both companies should go bankrupt, and shareholders should be able to sell their shares. The exchange freezing shares makes investors nervous. By comparison, the NYSE only froze trading for 1 day, and that was when the World Trade Center buildings were attacked in 2001.

That the CEO of the CMA has attempted to put price floors on stock prices is concerning. “Capital Markets Authority (CMA) chief executive Wycliff Shamia told the Star that the move has been necessitated by the fact some of the companies have very strong fundamentals but the valuation is quite low.” Yes, this is how free markets work. The market decides what something is worth, not the government. The latter would be communism.

Preference for other investments

Investors would rather speculate on land because Kenya has no property tax. GoK should fairly tax other parts of the economy, like creating a 0.1 to 1% annual Property Tax on land so that people can’t just sit on their land and speculate without contributing to the economy. All other developed and emerging economies have an annual Property Tax; it’s time Kenya did the same. Property tax is generally recognized as the least bad tax for economic growth and yet Kenya doesn’t have it and isn’t even considering it. See here how property tax could be implemented in Kenya and make all parties happy. With the devolved county governments, this could more easily be accomplished than in the past.

The effect of no property tax is clear in the numbers: Kenyan real estate is 75x bigger than equities ($678b vs $9b); meanwhile, by comparison, US real estate is only 2x bigger than US equities ($96T vs $46T). The US equities market sources capital from around the world because people trust Uncle Sam to treat equities fairly, but people don’t (yet) trust Uncle Kamau to do the same. I think the lack of Property Tax is the nail in the coffin of the NSE, and without this reform, there can be no vibrant equities market. (Note: the only meaningful property tax that exists is the capital gains tax when a property is sold, and even then, people can easily underreport the sale price, which is much harder to do on a public equities market. Some counties like Nairobi charge property tax at around $5-30 per year, which is a joke. There is also a tax on Rental payments, but this is not a tax on the property but a tax on a business being done on the property, making matters worse by disincentivizing property development.)

Because Treasury Bonds are over 15%, investors put their money there rather than risk equities. Hopefully, after the Eurobond payment in June 2024, Treasury yields will reduce and more money will flow back to the equities market.

The opportunity

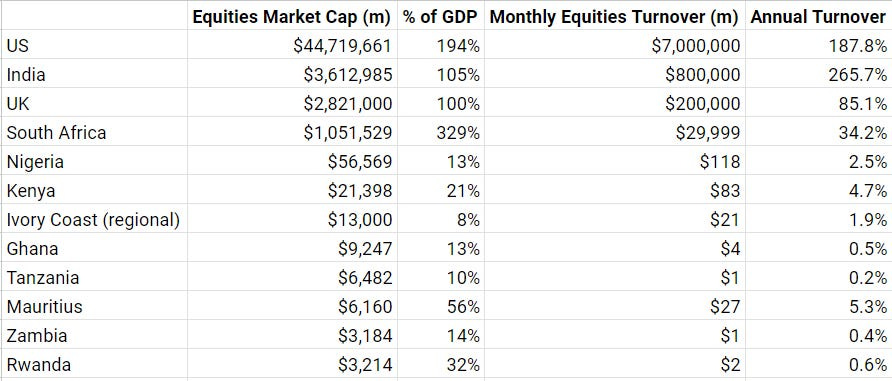

But there are reasons to be bullish on African stock markets. African markets, excluding South Africa, have a relatively small proportion of their GDP trading. There is room for the equities market to grow 10x to align with other markets like the US, South Africa, and India.

Further, Kenya is the region’s largest and most liquid market and could be a regional player—it is already one of the most liquid markets in Africa. By aggregating regional companies onto its exchange, NSE could grow another 10x. On top of that, GDP will compound to 63% growth over the next 10 years. This brings the total NSE market cap potential to ~630x growth over the next 10 years… if NSE can play its cards right. 630x growth would put the NSE in line with India, so it’s not impossible, as discussed below.

On top of that, Annual Turnover (trading of the shares) is relatively low compared to other markets at 4.7% on NSE, ~40x less trading than the US, adjusted for market cap.

There is room for more economic activity on African stock markets.

So where is this 630x growth going to come from?

Increase valuation. The P/E (price to earnings) ratio is only 4.9 on NSE, a sign that investors have low growth expectations. This is half its historical level and 1/4th the ~20 P/E seen on US exchanges, a 4x growth potential for NSE stocks. This is due to uncertainty, low expectations, and discounting for inflation.

More companies listing. About 1% of US companies are publicly listed compared to 0.001%ish (my guesstimate) of Kenyan companies. Realistically, 10x growth potential (as most Kenyan businesses are too small to go public).

NSE quality. If the NSE can improve quality that will improve investor confidence and 2-10x growth.

Virtuous Cycle. There are the compounding effects of a growing market, generating interest and crowding in more capital.

Encourage international investors on local trading platforms. Currently, American, Canadian, Singaporean, and other foreign investors are discouraged from investing through existing brokerage channels and online trading platforms as the regulations in those countries are too costly to manage given the small public market. But as the market grows and trading platforms enable more foreign investors you can imagine that as returns are becoming more predictable with lower returns in the West, some intrepid investors will take an interest in Africa. 2x opportunity

Distribution on international trading platforms. Like Robinhood, Charles Schwab, etc. 10x opportunity.

Cross-listing from other countries in East, Central, and Southern Africa. Theoretically, a 10x opportunity, but in reality, maybe a 2x. Already, some of this is happening. Bank of Kigali (Rwanda) and Umeme (Uganda) are listed in their own countries but cross-listed on NSE. Crosslisting is relatively easy. Evidence suggests that cross-listing increases company valuation, so the cost of cross-listing more than pays for itself. (Source: Peristiani, Federal Reserve Bank of New York, 2010) Old Mutual, for example, is cross-listed on 5 exchanges. A Kenyan equities lawyer confirmed this would be a workable strategy.

Behavioral nudges. There is no way for Kenyan trading apps to automatically reinvest dividends, while automatic reinvestment of dividends is possible in other markets like the US. This could boost share price by 5% per year. This would cut out stock brokers and their fees. My little research online suggests the CMA (Capital Markets Authority) currently prevents automatic dividend reinvestment due to pressure from stock brokers.

Better trading UX. New trading apps that make it easy to buy shares can 2x capital yet again. I tried to sign up with 6 different trading apps and brokers. 3 didn’t allow Americans, Dutch, Singaporeans, or Canadians to trade. The others each had cumbersome documentation requirements: one required a scanned copy of a notarized copy of my passport. What’s the point of a copy of something notarized? The friction to buy shares as a foreigner or local is severe.

Reduced trading fees. This is the big one. CDSC and other government entities can reduce the tax on trading, which is currently at 0.36%. If a stock is only expected to gain 10% a year, paying 0.36% per trade precludes an efficient market that quickly buys and sells. For comparison, the NYSE has a fee on trades of $0.001 (which comes to 0.003% for a typical $30/share stock, 1/100th the price of Kenyan fees). Broker fees are also extremely high in Kenya at 1-1.5%, 10x higher than in the US at 0-0.1%. Reducing fees would not directly increase market cap, but a 10x reduction in fees might increase liquidity 10x, bringing the NSE more in line with other exchanges, from 4.7% turnover to perhaps 50% turnover. Increasing liquidity would perhaps increase the market cap by 2-10x by increasing P/E and crowding in more companies.

Improving taxation. Right now, US investors in Kenyan companies get taxed twice. Thus, going through Mauritius is advantageous.

Case study 1:

I tried to sign up for various trading apps (Exness, Sterling, AIB-AXYS, ABC). Finally, after a week I was able to sign up on EFG Hermes. I tried to trade using the Market Price but the Market Price was 2x the Limit Price. I was told by customer service to ignore the Market Price. Once I did make a trade it took two days for my trade to be reflected in the app. After many customer service requests, my trade was reflected but then the app showed I had a negative account balance. After another customer service call that has been fixed. Then my password stopped working.

I can see why there might not be a lot of retail investors in Kenyan securities as the buying experience does not inspire confidence. But it does show an opportunity for someone to build a better trading experience.

Why are companies resistant to going public?

Before we determine whether listing at all would benefit companies, let’s consider:

does going public preclude a company from raising additional institutional capital?

what are the tax implications?

what are the compliance costs?

with interest rates as they are, is now really the right time to list?

Treasuries are 15% in Kenya at the moment, so raising equity is a hard sell. But global interest rates are unlikely to stay high, so perhaps a reduction down to 10% in the coming years will be good for equities. Also, land prices, the other investment option, may run out of room to grow further as rural land prices in Kenya are already about the same as rural land prices in the US, channeling more investment to equities.

Compliance costs are Kenyan SMEs’ most commonly cited problem for not listing. However, the compliance costs in Kenya are typically only around $5,000 a month, which they should be doing even as a private company, like maintaining a board of directors and informing shareholders of material changes. Thus, this argument from SMEs doesn’t hold water.

In an IPO, a company would sell at least 15% of its shares to raise additional capital. Some companies might be concerned with how they can raise more capital after the IPO. Never fear! There are several options:

Corporate Bond: this is just a loan with a maturity. Of note, there is no collateral required for this. Also, it has a bullet payment at the end, which gives the company some breathing room on repayment.

Private placement: a select group of investors are invited to buy shares in the company. This can be done even before a public offering and provides more privacy for the company.

Rights Issue: this is where shares are offered to existing shareholders only so they are not diluted. This funding method is fairly common in Kenya, though not as common in the US.

Secondary Offering: just like a rights issue but open to anyone. This is common in the US. Tesla, for example, has had 8 Secondary Offerings since 2012.

All-stock acquisition: not strictly raising capital, but a public company can issue new shares to buy another company without spending cash. For example, Facebook’s acquisitions of WhatsApp and Instagram were mostly paid for in shares. Berkshire Hathaway makes its acquisitions this way, or through retained earnings (reinvested profits) rather than through Secondary Offerings.

Kenya has many advantages over other markets:

Recently, an app developed for retail investors called Dosikaa (I wrote the first review for it on the Play Store—it didn’t work for me) enables anyone to buy shares. Once Dosikaa works out the bugs, this greatly improves the share-buying UX, instead of going to a broker and signing a paper.

Kenya doesn’t limit foreign ownership in most companies (aside from banks and telcos) thus, international capital could invest in NSE-listed companies, while other African countries often have more restrictions on foreign ownership.

Increased liquidity and market capitalization compared to most other African exchanges.

There are also downsides:

registering a company in Kenya doesn’t have the same tax advantages as Mauritius

it doesn’t have nearly the same market depth as Johannesburg or other exchanges. Jumia, despite doing most of its business in Egypt, Kenya, and Nigeria, chose to list on the NYSE. JMIA once traded at $60/share but fell 20x. I bought some shares there at $2.5 last week. Let’s see if they can bounce back. Jumia raised more money on the NYSE than it could have on the NSE, but Jumia also might not have lost as much value if it had been listed in an African market. Local buyers in Kenya would have seen the value it creates by direct interaction on the ground. Thus, there are advantages to listing in Africa vs. New York.

One possible tax-efficient structure might be to register the holding company in Mauritius, list it in Mauritius, and then cross-list it to NSE (and other African exchanges) to increase liquidity.

Kenyan stocks have more government and founder ownership than the US; the US has more Retail, ESOP, and ETF (e.g. Index Fund) ownership than Kenya. (Source: CMA and TPC)

Case Study 2:

Flametree, listed on NSE GEMS (the growth board), has an equity value of around $10m, with sales growing about 25% a year. Flametree is a holding company that owns ~15 common spice, shampoo, and water tank brands in Kenya and other African countries. The CEO owns 84% of the company. The market cap is around $1.5m, the P/S is 0.05, P/B is 0.3–this would seem to be a very good buy. The CEO pays himself about $180,000 a year, which seems fair for a company of this size. But Flametree hasn’t paid dividends in years and the CEO has no incentive to. So the shares are kind of stuck in limbo, even as they are undervalued; since the CEO owns 84% there is no opportunity for a hostile takeover. The share price has declined about 90% since listing in 2014.

Case Study 3:

Equity Bank vs. KCB.

Equity Bank has a P/E of around 3.4 while KCB is around 1.8. Both seem undervalued. However, they have fairly different shareholdings. Largest investors:

Equity

– Arise BV (owned by Dutch and Norwegian Development finance institutions)

– James Mwangi (founder and CEO)

KCB

– Government of Kenya

– NSSF (social security)

Does ownership by a DFI and the founder help maintain the share price of Equity Bank?

I bought both Equity and KCB in December. Let’s see how they do.

Is a stock exchange ‘fit for purpose’ in Africa?

Just like mobile money in the US looks very different than mobile money in Africa (Venmo vs. Mpesa), perhaps funding large companies faces an analogous problem. Currently, African public markets are roughly a copy/paste of systems that work in the US. But the chances that a market with vastly less wealth, trust, and education would have the same optimal solution seems…small.

For example, NASDAQ was not even considered a stock market when Apple used it to sell its shares. It was considered an electronic over-the-counter (OTC) system typically reserved for the purgatory of penny stocks. But now it has risen to be the world’s second-largest exchange.

What would the African version of NASDAQ look like?

The EABX OTC system received regulatory approval on Feb 1, 2024. An OTC system for SACCO shares has also been created by Sacco Shares Exchange and SakoSoko.

MPesa was developed and funded by foreigners; Equity Bank, to this day, has a disproportionate amount of foreign shareholders.

What could a fit-for-purpose capital market look like? How can international Development Finance Institutions help?

Criticism of this article

Due to the nature of this article, many people have written comments to me directly rather than post them publicly. While the majority of comments were positive, I’ll focus on the critical ones here:

You are biased and you promote American Exceptionalism [that is, that Americans are somehow better than others.] NSE and the US stock market are not comparable in any way.

My goal is not to insult Kenya with this piece; I love Kenya and hope we can do better. I compared the NSE to the NYSE but could as easily have compared it to the Bombay Stock Exchange. NSE could serve all of Africa’s 1.4 billion people just like India’s stock exchanges serve 1.4 billion Indias. India is one country compared to 54 in Africa, but it is divided by religion, language, and culture just like Africa. BRSV exchange works across 7ish countries in West Africa so there’s no reason we can’t do the same in the east. The cross-listing seems like the low-hanging fruit where companies in Rwanda, Zambia, etc cross-list to NSE. We would see more of this if the NSE was more vivacious. So I’m not advocating that we should be like Americans but that there’s existing proof that it’s possible to be better.

You cherry-picked your data.

After asking for better data, none was shared.

CMA is doing a great job of reforming the public markets for the better.

When I requested examples, none were shared.

Macro trends

There is a trend globally for reduced public market listings. The number of IPOs in the US and UK has halved over the last 25 years.

This is reflected in Kenya where there have been no IPOs for a while, but in just the first half of 2023, there were 34 Private Equity deals worth $1.3b.

As the world becomes flatter, there is consolidation. Why list on the London Securities Exchange when you could list on Euronext or Nasdaq?

Therefore, there is a now or never, go big or go home for the NSE. If it doesn’t become a regional player it will be eclipsed by Mauritius, Johannesburg, Bombay, Euronext, or Nasdaq.

Go regional or become irrelevant.

Conclusion

Why don’t the public markets get fixed in Africa?

Fixing the capital markets starts with quality:

Rebrand the NSE as the African Stock Exchange and implement the below changes to become a regional player.

The most important and urgent problem is NSE leadership. The board is currently selecting a new CEO. A lot depends upon this choice. We need a visionary.

NSE (Nairobi Securities Exchange) can delist companies trading below $1m market cap, below Ksh 10 per share, or have less than 25% freely floating shares.

NSE can maintain a culture of timeliness and data quality.

CMA (Capital Markets Authority) can revoke stock broker licenses for trading apps with less than 99% uptime.

The government of Kenya can let the shilling float freely to eliminate the black market for currency and restore investor confidence.

GoK can fairly tax land which will drive more investment to productive parts of the economy like equities.

GoK can reduce interest rates on Treasury bonds. At 15% people would rather buy treasuries than take additional risk for the same (or even less) return on the stock exchange.

Reduce trading fees. CDSC, NSE, brokers, and government entities can reduce fees that currently preclude an efficient market and high turnover.

Let the free market do its job: Unfreeze listings like Mumias and Kenya Airways and the regulator, the CEO of CMA, could avoid saying things that sound communist.

Sell off parastatals and partially government-owned companies. The government of Kenya can sell KenGen and Safaricom to pay off its debt and let companies operate more efficiently on the public markets and in private hands.

Allow automatic dividend reinvestment: Public companies can create DRIPs (Dividend Reinvestment Programs) to increase demand for shares by automatically reinvesting dividends

Develop a built-for-Africa solution. Innovators and entrepreneurs can consider what an African-native solution to public markets might be that looks very different from the public markets we have in the West.

Together, these actions would instill confidence in investors and companies, local and foreign.

Improving the public markets could be a win for everyone. A big win that could 10x the economy. A win for investors, companies, stock brokers, the NSE, international development organizations, and the Kenyan government revenue collection.

L’écosystème commercial de l’Afrique recèle un immense potentiel mais continue de faire face à des lacunes en capital. Combler ce fossé grâce à l’investissement de la diaspora peut accélérer la croissance tout en offrant des opportunités d’impact social convaincantes.

L’écosystème des start-ups et des petites entreprises (PME) africaines offre un potentiel de croissance immense mais rencontre encore des défis pour accéder au capital patient nécessaire pour prospérer.

Avec une population jeune et technophile, une classe moyenne en pleine croissance et une multitude de défis sociaux et environnementaux à résoudre – les opportunités d’impact et de rendements sont nombreuses. Cependant, des lacunes critiques en matière de financement persistent.

Combler le fossé en capital de la diaspora

Avec plus de 100 milliards de dollars de transferts de fonds envoyés annuellement depuis la diaspora africaine répartie dans le monde entier vers le continent, il existe un immense potentiel pour canaliser ces fonds vers des entreprises en phase de démarrage prometteuses.

Cependant, des problèmes tels que le manque de sensibilisation, la confiance, les perceptions négatives et l’accès à des accords de qualité ont entravé cela.

Le financement de capital-risque en Afrique reste fortement orienté vers les stades ultérieurs, tandis que les start-ups en phase de démarrage luttent pour obtenir des financements pré-seed et seed pour peaufiner leurs produits et gagner une première traction.

Comme l’ont discuté les panelistes experts Jennifer Frimpong de Ma Adjaho & Co et le PDG d’ARED Henri Nyakarundi lors de la première partie de notre série de webinaires axée sur l’investissement de la diaspora, le biais de familiarité culturelle joue également un rôle.

Les investisseurs de la diaspora ont souvent tendance à privilégier les opportunités dans leurs pays d’origine en raison de liens personnels et de familiarité. Mais cela limite le champ des investissements potentiels.

Établir la confiance et la sensibilisation pour des plateformes telles que Daba qui mènent une diligence raisonnable rigoureuse et offrent un accès ouvert à des accords soigneusement examinés et transparents à travers l’Afrique est essentiel pour surmonter ce biais.

Autonomiser les start-ups et les investisseurs

Frimpong a expliqué que les start-ups ont besoin de plus de soutien pour “professionnaliser” et devenir “prêtes à l’investissement” afin d’attirer le capital de la diaspora.

De l’affinage de leurs propositions de valeur, à la modélisation financière et à la création de pitchs convaincants – les start-ups ont besoin d’un accompagnement pratique.

Avec l’accélération appropriée des ventures à fort potentiel, des secteurs de l’agroalimentaire à la technologie financière, en passant par le commerce électronique, et au-delà peuvent offrir aux diasporans des opportunités convaincantes avec un impact social.

Saisir l’élan

La scène des start-ups en Afrique est sur le point de prospérer au cours de la prochaine décennie, en particulier avec la puissance de la diaspora et des plateformes comme Daba élargissant l’accès au financement en phase de démarrage.

Mais réaliser ce potentiel immense nécessite une action collective à travers les sphères publique, privée et non gouvernementale pour favoriser le talent entrepreneurial et injecter du capital de croissance dans l’écosystème.

Nous encourageons tous ceux qui souhaitent soutenir les entreprises africaines – que ce soit par l’investissement, la réforme des politiques, l’incubation, ou d’autres moyens – à en savior plus, à s’impliquer et à entrer en contact.

Le moment est venu de canaliser le capital de la diaspora vers les ventures les plus brillantes du continent. Avec des efforts coordonnés, l’écosystème des start-ups en Afrique peut transformer les économies et élever des millions de personnes.

Si vous n’avez pas pu assister au webinaire ou si vous souhaitez le revoir, vous pouvez visionner l’enregistrement sur notre chaîne YouTube. Et pour en savoir plus sur la façon dont Daba permet d’investir dans les opportunités en Afrique pour les investisseurs individuels et institutionnels, visitez notre page web ou téléchargez notre application mobile.

Africa’s business ecosystem holds immense potential but still faces capital gaps. Bridging this through diaspora investment can accelerate growth while providing compelling social impact opportunities.

The African startup and small business (SME) ecosystem holds immense growth potential but still faces challenges in accessing the patient capital needed to thrive.

With a young, tech-savvy population, rapidly growing middle class, and abundance of social and environmental challenges to solve – the opportunities for impact and returns are plentiful. However, critical funding gaps persist.

Bridging the Diaspora Capital Gap

With over $100 billion in remittances sent annually from the widespread African diaspora back to the continent, there is vast potential to channel these funds into promising early-stage ventures.

However, issues like lack of awareness, trust, negative perceptions, and quality deal access have hampered this.

Venture funding in Africa remains heavily skewed towards later stages, while early-stage startups struggle to raise pre-seed and seed funding to refine products and gain initial traction.

An in-session snapshot of our webinar this week. Catch the full conversation on YouTube.

As discussed by expert panelists Jennifer Frimpong of Ma Adjaho & Co and ARED CEO Henri Nyakarundi during Part 1 of our Diaspora investment-focused webinar series, cultural familiarity bias also plays a role.

Diaspora investors often gravitate towards opportunities in their countries of origin due to personal ties and familiarity. But this limits the scope of potential investments.

Building trust and awareness for platforms like Daba that conduct rigorous due diligence and open access to thoroughly vetted, transparent deals across Africa is critical to overcoming this bias.

Empowering Startups and Investors in Africa

Frimpong explained that Startups need more support “professionalizing” to “investment readiness” to attract diaspora capital.

From sharpening their value propositions to refining financial modeling and crafting compelling pitches – startups need hands-on nurturing.

With the right acceleration of high-potential ventures, sectors from agribusiness to fintech, e-commerce, and beyond can offer diasporans compelling opportunities with social impact.

Seizing Africa’s Growth Momentum

Africa’s startup scene is set to thrive over the next decade, especially with the power of the diaspora and platforms like Daba expanding early-stage funding access.

But realizing this immense potential requires collective action across public, private, and non-profit spheres to foster entrepreneurial talent and inject growth capital into the ecosystem.

We encourage all those looking to support African enterprises – whether through investment, policy reform, incubation, or other means – to learn more and get involved and in touch.

The time is now to funnel diaspora capital into the continent’s brightest ventures. With coordinated efforts, Africa’s startup ecosystem can transform economies and uplift millions.

If you could not join the webinar or would like to watch it again, you can catch the recording on our YouTube channel. And to find more about how Daba enables investing in Africa opportunities for individual and institutional investors, visit our webpage or get our mobile app.

Ces dernières présentent de forts effets multiplicateurs en vue de réduire la pauvreté et de favoriser la prospérité partagée sur le continent.

L’alimentation et les boissons, l’infrastructure, les soins de santé, l’éducation et les énergies renouvelables sont apparus comme les cinq principaux secteurs pour les opportunités d’investissement dans le rapport.

Ensemble, ils représentent plus de 60 % des opportunités identifiées couvrant l’Afrique de l’Est, de l’Ouest et australe.

L’équipe d’intelligence de Daba explore en outre cinq autres secteurs. Lisez la suite pour découvrir où se trouvent les opportunités d’investissement les plus attractives en Afrique.

Où investir en Afrique : Voici les 10 secteurs les plus prometteurs

1. Alimentation et Agriculture

Le secteur de l’alimentation et de l’agriculture joue un rôle économique intégral à travers l’Afrique.

Malgré la croissance de sa classe moyenne et une réduction de sa dépendance à l’agriculture, l’Afrique continue de connaître une population croissante et une demande croissante en matière d’alimentation.

Par conséquent, le continent offre des perspectives d’investissement substantielles dans les secteurs de l’agriculture et de l’agroalimentaire. Ces opportunités englobent des investissements dans divers aspects de la chaîne de valeur agricole, notamment les terres agricoles, les intrants agricoles, la transformation et les innovations agritech.

L’Afrique subsaharienne, en particulier, est confrontée à des besoins agricoles importants qui vont au-delà des éléments fondamentaux tels que les engrais, les semences et l’irrigation pour inclure des améliorations essentielles de l’infrastructure.

Les entreprises impliquées dans l’amélioration des routes, des installations de stockage, des ports et des réseaux électriques dans la région peuvent également prospérer en soutenant et facilitant la croissance des opérations agricoles florissantes de l’Afrique subsaharienne.

Ces investissements offrent non seulement des rendements financiers potentiels, mais contribuent également à relever les défis de sécurité alimentaire auxquels la région est confrontée.

L’Afrique continue de connaître une population croissante et une demande croissante en alimentation.

2. Infrastructure

Les besoins en infrastructure restent critiques pour faire avancer les résultats socio-économiques. Les exigences continuent de croître au milieu de l’urbanisation rapide et de l’industrialisation.

Bien que la pénurie d’infrastructures en Afrique soit indéniable, elle offre de nombreuses opportunités d’investissement, notamment pour des secteurs tels que la construction, les télécommunications, l’énergie et les transports, entre autres.

La BAD estime que le continent aura besoin jusqu’à 170 milliards de dollars par an d’ici 2025 pour rénover ses infrastructures, les deux tiers de ce montant étant nécessaires pour des infrastructures entièrement nouvelles et le tiers restant pour la maintenance.

Par conséquent, les routes, le logement, l’électricité, la gestion des déchets et d’autres projets à long terme signalent un fort potentiel de partenariat public-privé.

3. Soins de Santé

Les secteurs des soins de santé et des médicaments sur ordonnance sont estimés à une valeur combinée de 3 milliards de dollars, les médicaments innovants/brevetés contribuant approximativement à hauteur de 1,7 milliard de dollars à cette valeur. Les médicaments en vente libre détiennent actuellement une valeur de 378 millions de dollars.

Étant donné la montée en puissance des sociétés pharmaceutiques produisant des médicaments génériques, il est fort probable qu’il y ait une augmentation des investissements dans le secteur de la santé du pays.

Cela est particulièrement significatif compte tenu du fait que 85 % de la population africaine dépend des services de santé publics.

Il est raisonnable de prévoir que le public accueillerait favorablement le Plan national d’assurance maladie, cherchant ainsi à accéder à des médicaments et à des installations de traitement plus abordables.

Ne manquez pas les opportunités d’investissement exclusives en Afrique ! Téléchargez l’application Daba dès aujourd’hui et débloquez un monde de rendements potentiels tout en ayant un impact positif.

4. Éducation

Investir dans l’éducation en Afrique représente une opportunité de soutenir la croissance du continent tout en générant des rendements.

La population africaine devrait doubler d’ici 2050, ce qui entraînera une demande croissante en matière d’éducation de qualité.

Des opportunités d’investissement existent dans la construction et la gestion d’écoles, la technologie éducative, les bourses d’études et les programmes de formation.

Les écoles privées et l’enseignement supérieur sont particulièrement prometteurs compte tenu de la demande croissante en éducation de qualité et abordable.

La technologie éducative offre également une opportunité à grande échelle. Avec l’augmentation de l’accès aux mobiles et à Internet, les plateformes en ligne et les applications peuvent fournir une éducation abordable dans des régions éloignées et mal desservies.

Investir dans l’éducation en Afrique offre une opportunité de soutenir la croissance du continent tout en générant des rendements.

Fournir des bourses d’études et des formations aux étudiants et aux professionnels africains est un autre investissement important. Les partenariats avec des organisations déjà actives dans cet espace offrent des canaux d’investissement idéaux.

L’expansion de la population jeune de l’Afrique et la demande d’éducation de qualité créent une opportunité de stimuler le développement grâce à l’investissement et de générer des rendements financiers.

5. Énergies Renouvelables

L’Afrique dispose de ressources énergétiques renouvelables abondantes qui présentent d’importantes opportunités d’investissement alors que le continent passe aux sources d’énergie durables.

L’énergie solaire et éolienne devrait connaître une croissance massive, avec une capacité installée augmentant de 100 fois pour le solaire et de 35 fois pour l’éolien d’ici 2050. Cela nécessitera des milliards d’investissements au cours des prochaines décennies.

Le Maroc, l’Afrique du Sud et les pays d’Afrique du Nord seront des marchés clés pour les projets solaires et éoliens en raison de l’irradiation solaire forte et des ressources éoliennes, selon le Forum économique mondial.

L’énergie hydroélectrique offre également un potentiel substantiel, avec une capacité attendue quadruplée d’ici 2050. Les pays d’Afrique subsaharienne disposent des plus grandes ressources hydroélectriques restantes à exploiter. La production d’hydrogène vert est un autre domaine prêt pour une croissance et des exportations majeures, avec des projets déjà en cours au Maroc, en Namibie et en Afrique du Sud.

Cumulativement, près de 3 000 milliards de dollars de dépenses en capital sur les énergies renouvelables et les infrastructures de soutien seront nécessaires en Afrique d’ici 2050. Investir tôt permet aux institutions financières de conduire la transition et de capitaliser sur les opportunités à long terme.

Le paysage des technologies propres en Afrique connaît un essor sans précédent, alimenté par une combinaison de ressources renouvelables abondantes.

6. Marchés des matières premières

De nombreux pays africains dépendent largement du commerce des matières premières. Certains d’entre eux naviguent à travers les cycles des matières premières, comme le montrent les principaux pays exportateurs de pétrole comme l’Angola et le Nigeria, ainsi que les pays producteurs de cuivre tels que la République démocratique du Congo et la Zambie.

Selon les estimations de l’ONU, l’Afrique détient plus de 30 % des réserves minérales mondiales, y compris plus de la moitié des réserves mondiales d’or, de chrome et de platine, une proportion importante des réserves mondiales de diamants, et 5 % des réserves naturelles de minerai de lithium.

Le continent abrite également les principaux exportateurs mondiaux de produits agricoles tels que le cacao (Côte d’Ivoire et Ghana), le café (Éthiopie et Ouganda), le thé (Kenya) et le coton (Bénin, Burkina Faso, Égypte, Soudan et Mali).

Vous recherchez une chance de faire une différence tout en obtenant des rendements. Rendez-vous sur notre application pour commencer à investir dans la croissance de l’Afrique dès aujourd’hui !

7. Commerce de détail et commerce électronique

L’expansion de la classe moyenne africaine, qui est passée de 313 millions de personnes au cours des 30 dernières années, présente des perspectives d’investissement attrayantes dans des secteurs axés sur le commerce de détail.

Pour donner un contexte, les entreprises de télécommunications en Afrique ont ajouté plus de 400 millions d’abonnés, soit plus que l’ensemble de la population américaine, depuis 2000.

La croissance de la classe moyenne africaine peut être attribuée principalement à une expansion économique robuste, à un passage vers l’emploi salarié et à un éloignement de l’agriculture. Le rythme général peut avoir été plus lent que prévu, mais la composition démographique du continent reste attrayante.

Pour répondre à ce marché, une industrie du commerce électronique en pleine croissance émerge rapidement, aidée par un nombre croissant d’utilisateurs d’Internet. D’ici 2025, l’Afrique devrait avoir plus d’un demi-milliard d’acheteurs en ligne, avec une pénétration de 40 % et un taux de croissance annuel composé de 17 %.

8. Immobilier et logement

L’urbanisation et la croissance démographique dans de nombreux pays africains ont alimenté une demande croissante en matière de logements résidentiels et commerciaux.

Ce paysage dynamique offre des opportunités attrayantes dans les projets de développement immobilier, permettant aux investisseurs de capitaliser sur l’élan de croissance du continent pour potentiellement tirer profit de la valorisation des biens immobiliers.

De nombreuses techniques d’investissement éprouvées qui ont réussi dans le monde occidental, telles que les locations à long terme, les fiducies de placement immobilier (FPI), les locations de vacances et les options de bail, peuvent générer des rendements comparables sur le marché africain.