Cette collaboration vise à rendre les opportunités d’investissement en Afrique accessibles aux investisseurs accrédités des États-Unis grâce à la plateforme innovante de Fundr.

Miami et New York, États-Unis – Daba, le principal fournisseur d’infrastructures d’investissement multi-actifs en Afrique, a annoncé aujourd’hui un partenariat stratégique avec Fundr, une plateforme d’investissement en startups basée aux États-Unis. Cette collaboration a pour objectif de rendre les opportunités d’investissement en Afrique accessibles aux investisseurs accrédités des États-Unis grâce à la plateforme innovante de Fundr.

Daba propose une gamme complète de produits d’investissement, notamment une application d’investissement pour les investisseurs individuels, des services institutionnels, ainsi que des API pour les entreprises technologiques souhaitant intégrer des produits d’épargne et d’investissement.

La plateforme de Fundr utilise des données et de l’intelligence artificielle pour optimiser la prise de décision, éliminer les biais et augmenter l’efficacité dans l’investissement en phase d’amorçage. Elle collabore avec des investisseurs de toutes tailles pour analyser les opportunités d’investissement, optimiser leur processus d’investissement et fournir des informations approfondies en temps réel sur leurs portefeuilles.

« Ce partenariat avec Fundr s’aligne parfaitement avec notre mission de démocratiser l’investissement en Afrique », a déclaré Boum III Jr, PDG et co-fondateur de Daba. « En tirant parti du réseau d’investisseurs de Fundr, nous pouvons connecter davantage de capitaux mondiaux aux opportunités passionnantes qui émergent à travers le continent africain. »

Lauren Washington, PDG de Fundr, a commenté : « Nous sommes ravis de nous associer à Daba pour offrir des opportunités d’investissement de haute qualité en Afrique sur notre plateforme. Cette collaboration offre à nos investisseurs un accès unique à l’un des marchés à la croissance la plus rapide au monde, diversifiant ainsi davantage leurs portefeuilles. »

L’écosystème du capital-risque en Afrique a connu une croissance remarquable ces dernières années. Selon les données disponibles, le financement du capital-risque en Afrique a augmenté de 1 597 % entre 2015 et 2023, passant de 277 millions de dollars à 4,7 milliards de dollars. Cette montée en flèche de l’activité d’investissement reflète la scène florissante des startups technologiques sur le continent, stimulée par une population jeune et technophile ainsi que par une pénétration croissante des smartphones.

Le dividende démographique de l’Afrique et sa transformation numérique rapide présentent un cas d’investissement convaincant. Avec plus de 60 % de sa population âgée de moins de 25 ans et un nombre d’utilisateurs d’Internet mobile qui devrait atteindre 475 millions d’ici 2025, le continent est prêt pour une innovation continue et une croissance soutenue. Des secteurs tels que la fintech, le commerce électronique et les technologies propres sont particulièrement attractifs, offrant des solutions aux défis locaux et des opportunités de développement à travers les frontières.

Daba et Fundr s’engagent à assurer un processus d’intégration fluide et à fournir un support complet aux investisseurs intéressés par l’exploration de ces nouvelles opportunités. Au fur et à mesure que le partenariat se développe, les deux entreprises prévoient d’organiser des webinaires et des événements communs pour informer les investisseurs sur le marché africain et présenter des startups prometteuses de tout le continent.

À propos de Daba

Fondée en 2021, Daba est la principale plateforme d’investissement et de financement multi-actifs en Afrique. La société se consacre à libérer tout le potentiel d’investissement du continent en offrant une plateforme unifiée permettant aux particuliers et aux institutions d’accéder à des opportunités d’investissement de haute qualité sur les marchés africains.

À propos de Fundr

Fundr est une plateforme d’investissement en startups basée aux États-Unis qui simplifie le processus d’investissement dans les entreprises en phase de démarrage. Grâce à son algorithme intelligent et à ses processus rationalisés, Fundr offre aux investisseurs une diversification instantanée, un accès à des startups sélectionnées et des outils efficaces de gestion de portefeuille.

This collaboration aims to make African investment opportunities accessible to accredited US investors through Fundr’s innovative platform.

Miami and New York, USA – Daba, Africa’s premier multi-asset investment infrastructure provider, today announced a strategic partnership with Fundr, a leading US-based startup investment platform. This collaboration aims to make African investment opportunities accessible to accredited US investors through Fundr’s innovative platform.

Daba offers a comprehensive suite of investment products, including a real investing app for individual investors, institutional services, and APIs for tech companies to integrate savings and investing products.

Fundr’s platform uses data and AI to empower decision-making, remove bias, and increase efficiency in seed investing. It works with investors of all sizes to analyze investment opportunities, optimize their investment process, and provide real-time deep insights into their portfolios.

“This partnership with Fundr aligns perfectly with our mission to democratize investing in Africa,” said Boum III Jr, CEO & Co-founder of Daba. “By leveraging Fundr’s investor network, we can connect more global capital to the exciting opportunities emerging across the African continent.”

Lauren Washington, CEO of Fundr, commented, “We’re thrilled to partner with Daba to bring high-quality African investment opportunities to our platform. This collaboration offers our investors unique access to one of the world’s fastest-growing markets, further diversifying their portfolios.”

The African venture capital ecosystem has seen remarkable growth in recent years. According to available data, venture capital funding in Africa has seen a remarkable surge in recent years, growing by 1,597% from $277 million in 2015 to $4.7 billion in 2023. This surge in investment activity reflects the continent’s burgeoning tech startup scene, driven by a young, tech-savvy population and increasing smartphone penetration.

Africa’s demographic dividend and rapid digital transformation present a compelling investment case. With over 60% of its population under the age of 25 and mobile internet users expected to reach 475 million by 2025, the continent is poised for continued innovation and growth. Sectors such as fintech, e-commerce, and cleantech are particularly attractive, offering solutions to local challenges and opportunities for scaling across borders.

Daba and Fundr are committed to ensuring a smooth integration process and providing comprehensive support to investors interested in exploring these new opportunities. As the partnership develops, both companies plan to host joint webinars and events to educate investors about the African market and showcase promising startups from across the continent.

About Daba

Established in 2021, Daba is Africa’s leading multi-asset investment and financing platform. The company is dedicated to unlocking the continent’s full investment potential by providing a unified platform for individuals and institutions to access high-quality investment opportunities across African markets.

About Fundr

Fundr is a US-based startup investment platform that simplifies the process of investing in early-stage companies. Through its smart algorithm and streamlined processes, Fundr offers investors instant diversification, access to vetted startups, and efficient portfolio management tools.

I have long been a fan of DFS Lab, the “research-driven venture capital in Africa”.

It’s the only VC firm on the continent that consistently shares – publicly and transparently – nuanced, long-form reflections around its investment thesis.

By doing that, they gifted the ecosystem not just with high-quality articles, but new terms/concepts to describe & make sense of tech in Africa.

Kudos to them! 💥

In a world defined by information overload and sensationalism, mental clarity is one of the most underrated qualities we should consciously strive to cultivate.

How do you know what you know? What is the deep meaning of it? If you cut through the noise, what do you see?

Trying to answer these questions – peeling all the layers of opaqueness – most people would find themselves naked.

This is why, drawing inspiration from the Almanack of Naval Ravikant, I am happy to propose – for the first time – the Almanack of DFS Lab: 6 theoretical primitives to make sense of VC investing in Africa.

These are six concepts coined by the firm that I find extremely insightful/useful in my activities as a researcher/investor:

The Frontier Blindspot

Fortune at the middle of the pyramid

The B-side of African Tech

Cyborgs vs Androids

Invested infrastructure

African S-curves

The original articles are all available on the DFS Lab website and Medium page.

My contribution mainly consists of summarizing my understanding of them & complementing them with my own ideas.

Lessgò.

Subscribe

1) The Frontier Blindspot 👀

Premise: The world has developed “intuitions about how technology markets are structured and what successful technology companies look like”. Cool.

However: this learning process took place strictly in the context of Western economies.

Ergo: the same frameworks do not always apply to frontier markets (like Africa).

Thesis: the disconnect between how we think tech is supposed to work versus how it really works – in Africa & other frontier markets – is the Frontier Blindspot! 💥

It is a blindspot because we are partially clueless – how tech markets work or don’t work in Africa has yet to be demonstrated. As we cannot copy-paste, learning happens by trial and error, thorough research, and on-the-ground experience.

What type of bias did we borrow from the Global North when making our assumptions about tech in Africa?

we overestimated the pace of digitalization;

we underestimated the strength of informal markets;

we overlooked the state of infrastructure and consumer purchasing power

When you factor in low-paced digitalization, strong informal markets, and quirky infra, you’ll see that a lot of common startup wisdom about business models, distribution strategies, and growth projections, won’t apply to the continent.

However, local entrepreneurs are still finding unique ways to apply the “modern startup stack” to the specifics of the African environment.

This is where the real opportunities are, and the areas of excitement include:

Physical logistics

SME solution stack

Financial building blocks

Agent networks

Although these things may seem obvious today, I think they are still not obvious to many, and they certainly were not obvious in 2020 (when the article came out).

What I find particularly useful about this piece is stressing the differences in infrastructure and purchasing power. When looking at pitch decks, I try stress the following questions:

what needs to be there for your product to be made, consumed, or delivered? (read: infrastructure)

How many people can buy your product, regularly? How do you know it?

We are about to have a taste of it with the next concept ✨

Who is the African consumer & what is the real size of the African market for digital products?

Hashtag: debunking the (once) popular tag “Nigeria is a market of 200M people” with some rigorous thinking.

Why?

Because population size does not equal market size, we cannot boast “the youngest population in the world” without looking at income brackets too.

Let’s proceed in order.

“Most B2C tech startups are seeking to make money from people’s discretionary spending”

Discretionary spending is the spending power that remains once covered for necessities like food, clothing, and shelter.

The question asked is: among the 200M fellow Nigerians, how many have the discretionary spending for my type of product?

In the image below, we can look at income levels and their percentage of discretionary income (in Africa).

Source: Fortune at the middle of the pyramid

If you are a B2C startup, what is the juiciest segment?

As a fairly coherent group, the people earning between $5-$10 – while comprising only ~10% of the population – have one of the highest discretionary spending power combined.

This is the fortune at the middle of the pyramid: the segment having enough people, with enough discretionary spending power. To the left of the curve, there are a lot of people but with little money; to the right, they have a lot of money but they are too few.

Now, speaking of unit economics: how much does it cost to acquire these customers? Here things get trickier.

In Africa, higher incomes are usually digitally-fluent city dwellers. Their geographical concentration, professional status, and greater online life, make them perfect targets for digital acquisition strategies. The same doesn’t necessarily hold for lower-income prospects: acquiring them is harder and costs more (with traditional digital methods).

To this comes a paradox: if the cost of acquiring a new customer is way more than what you earn from them, you will soon move to serve higher-income consumers. However, if you only serve the +10$ income bracket, at some point, growth will stall and you’ll need to move cross-border (not easy).

What can we learn from all we just stayed?

purely consumer-focused apps that do not focus on necessities (read: targeting discretionary spending) face unique challenges with monetization in Africa. This is because

the largest economic opportunity sits within the 5-10$ bracket, but the cost of acquiring them is high due to lower digital presence.

Moving forward, I think two very important corollaries emerge about “how to be successful”:

build apps focused on necessities, or focused on the business equivalent of “necessities” (restocking, working capital, inventory etc..);

if you target consumers’ discretionary spending, invest in human agent networks, the physical point of entry to most digital experiences for middle-of-the-pyramid Africans.

Personally, whenever I look at the pitch deck of a B2C company:

if they target offline acquisition, it means they are serving the middle of the pyramid;

if they don’t mention offline acquisition, it means they are serving the top of the pyramid.

Hence, I’ll start to wonder. Given the risk and the complexities of moving cross-border, can they make money (read: positive operating profit) before moving cross-border?

Enjoying the article so far? Share it with bruvs and siss 💥

This article draws inspiration from Wang Huiwen, the co-founder of Meituan Dianping, the most successful Chinese food delivery company, turned super-app.

In an issue of the newsletter “The China Playbook”, Huiwen defines the internet industry as made of two sides:

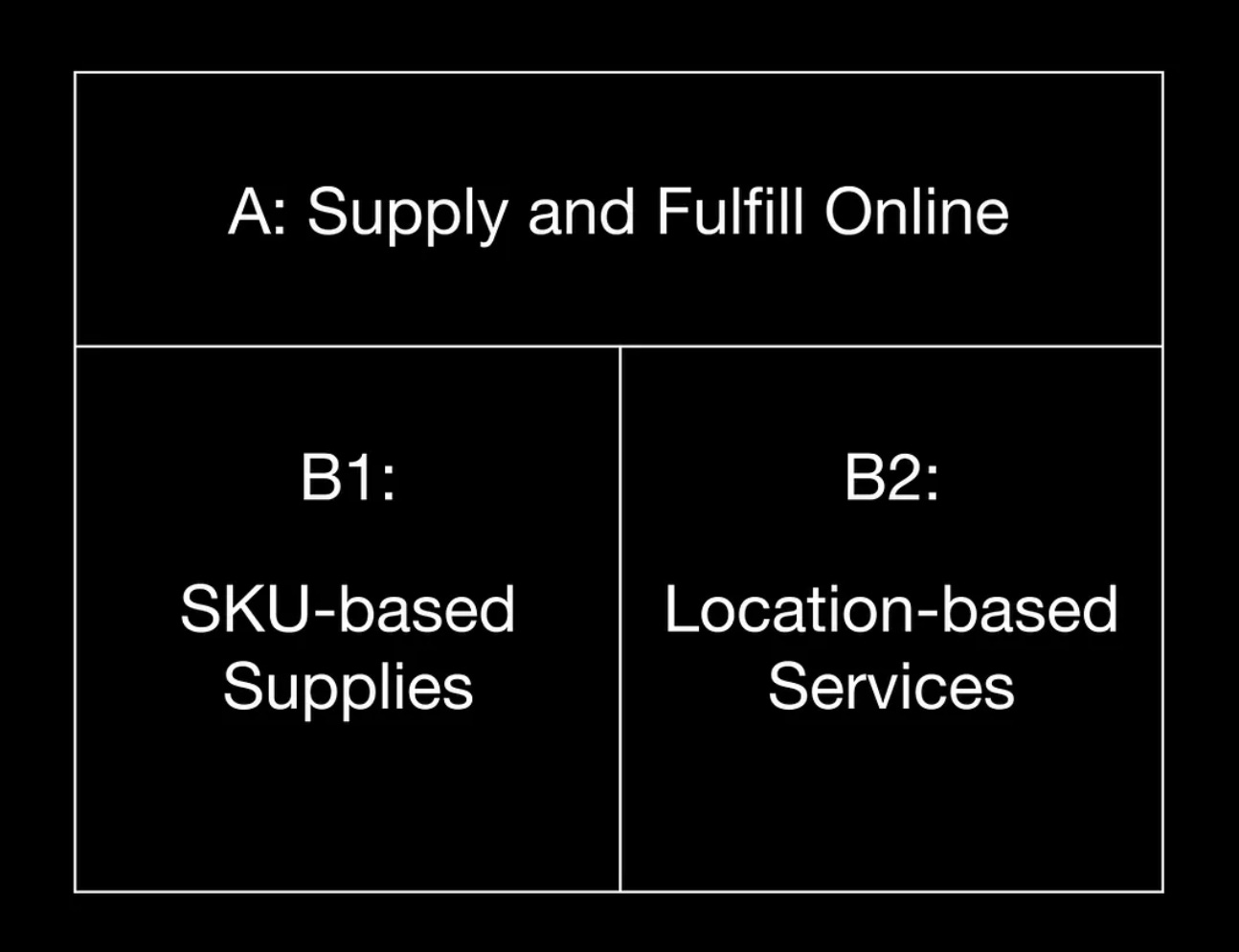

A-side: Supply and Fulfill Online

B-Side: Supply and Fulfill Offline

Side-A is products and services that are “pure internet”, as they can be delivered and consumed entirely online. SaaS (Salesforce), video-games (Voodoo), streaming (Spotify), etc…

Side-B is products and services that are delivered offline and consumed offline. Think of retail (Amazon), mobility (Uber), ticketing (Ticketmaster), etc…

If we have to apply this distinction to African economies, we would see that side-A (online utility) is smaller, compared to side B (offline utility).

The reason is that “fully digital experiences are either inaccessible, unaffordable or don’t cover the primary consumption needs for those in the bottom 95%.”

Ok cool. Let’s have a closer look at the B-side then. The B-side can be further divided into two sub-sections:

B1: SKU-based supplies

B2: location-based services

B1 is companies like Wasoko, Omniretail, and other traditional marketplaces. As digital businesses positioning in between the sourcing & delivery of physical products, their core competencies lie in ”understanding SKUs (stock keeping unit), understanding the supply chain, and understanding pricing”.

B2 is companies like Hubtel and Wahu Mobility. They are location-centric, as the physical location of customers & partners is a key element of their value proposition. For example, a ride-hailing company like Uber will need to recruit drivers in your city and ensure there are enough in your area as you order a ride – otherwise, you won’t be able to access their service. B2 businesses demand a larger offline team to manage operations closer to the customers.

What learnings do we have here?

B1 leverages technology to “improve the efficiency of existing value flows and reorganize pricing power”. On the contrary, “B2 is physical ubiquity”.

Let’s stop here.

In the article, Stephen Deng (DFS Lab MP) expands on the original concept expressed by Meituan Dianping founder.

When Wang Huiwen talks about B2 “location-based businesses”, he is primarily referring to ride-hailing, bike-sharing, and food-delivery, products made accessible by smartphone proliferation, which unlocked & democratized location data. These businesses are useful because you can see your location with your phone, and other people can see it too.

Deng however, twists its meaning for the African context, attaching to it the familiar notion of physical ubiquity: B2 businesses are interesting because of their physical proximity to the customers, mobilizing people and resources last-mile. Other than delivery, one can think of mobile money agents and social commerce as a form of B2 businesses. Their utility comes from their ability to integrate kiosks and people from your neighborhood in their business model. They are relatable, they are next door.

In short, they are more similar to Cyborgs, instead of Androids. What?

You read correctly. The concept of “B-Side of African Tech” is strictly intertwined with that of “Androids vs Cyborgs”, that we explore in the next section (before wrapping up with my two cents on this stuff).

Androids: solutions that replace informal markets with digital, formalized parts and processes

Cyborgs: solutions that enhance informal markets by arming them with digital, formalized parts and processes

Androids use tech to replace a set of existing actors.

Cyborgs use tech to improve the work of a set of existing actors.

Stephen Deng claims that we cannot brute force androids into existence if we are incapable of replacing informal players with significantly better solutions. And if we can’t replace them, we’d better empower them by building cyborgs.

It might seem like a B2C (Android) vs B2B (Cyborgs) play, but it’s more nuanced than that. Examples?

The ultimate Android example is Jumia and all Amazon-inspired B2C marketplaces: “replacing the local market with an online option that is meant to be more convenient, have more options, and is fully digitized”.

However, I think the same holds for many agri-tech platforms (like Complete Farmer or Winich Farms) that aggregate farmers’ produce and facilitate access to market & agro-inputs. In almost every pitch deck you will read about them “cutting out the middlemen”, the set of informal buyers and sellers who move crops to markets, whose commissions eat out farmers’ margins and drive inefficiencies (btw these platforms raised a lot of funds, but it’s not clear to me how much money they are making).

Cyborgs, on the contrary, look like tools that empower small businesses, applying a mix of online and offline. Instead of replacing existing relationships, they “supercharge them with digital optionality when the need arises”.

Both B2-side businesses and Cyborgs, tell the same story: existing structures can be valuable when they are empowered, instead of substituted.

Ok, but empowered how?

In my opinion, an online-offline Cyborg approach, can only be one of two things:

cost-effective offline distribution and/or marketing – agents knocking on doors or setting up shops;

tech-enabled intermediaries/retailers – empowered by a digital backend or specialized hardware.

That’s it!

Moniepoint is Africa’s fastest-growing fintech. Its distribution model? An army of human agents armed with PoS devices, knocking on merchants’ doors. The company revolutionized the capacity for Nigerian businesses to collect digital payments.

→ a Cyborg approach to digital payments.

Retailers’ bookkeeping apps like Oze and supply-chain management tools like Jetstream, both started as digital super-charger of African businesses: I give you tools to better manage invoices and logistics. Fast forward a couple of years, and they both ended up embedding credit and solving the pain of access to capital.

→ a Cyborg approach to digital lending.

I think Cyborg either means giving more “legs and arms” for asset-light digital businesses, or making “legs and arms” (SMBs) more competitive with digital tools.

Digital solution → leave a digital trace → data + learning models → better decision making

Digital solution → relational database & data integration → operational efficiencies

Digital solution → composable software stack → APIs & integrations → new products/services delivered on top of the main product

🪄🪄🪄

More in general, I think that both the “B-Side” and “Android vs Cyborg” arguments tend to over-emphasize the promises of the physical ubiquitous approach, without addressing the elephant in the room: we need more hardware.

A lot of things can be done with your phone, but not everything can be done with your phone, and sometimes, a phone is too much.

Limited storage/memory, weak bandwidth, and high data costs still represent hard limits to app utility for the average African business operator. A phone can do a lot, but not everything.

Safiri is a Tanzanian company equipping bus companies with thermal printers, and customers with digital ticket purchase options. They record transactions “digitally”, and print tickets “physically”. A good blend of digital and physical coming together. No need for Industry 4.0 here, just basic hardware tools.

And yet, I am not seeing enough investors stressing how specialized hardware – as well as consumer hardware – can play its role in the tech landscape.

We need more hardware. We can’t expect to revolutionize the continent simply with apps running on cheap smartphones.

I feel we’ll see major shifts when large-scale hardware manufacturing that truly responds to local business needs comes to fruition.

And yes, somehow, I am still convinced this can be a VC play.

Enjoying the article so far? Subscribe to Data Bites & have more of this 💩Subscribe

The concept is simple, yet powerful: the infrastructure built in the past has a lasting, indelible influence on our present & future.

Economists call it “path dependency”: society builds on top of what has been built, and this process makes us drift toward a trajectory of development and away from others.

In the United States, payment infrastructure has been built “for a time when phones were not as ubiquitous and hard-wired ethernet was increasingly common.”

The proliferation of PoS devices & phone cables (& later fiber cables), gradually made up the physical network on top of which credit cards’ adoption became widespread.

The alternative to cash travels on rails that took a long time to build, but once in place, it is hard to replace. It’s the hidden cost of path dependency: the more we build on top of invested infrastructure, the higher the switching costs to a different system.

“They have since gained ubiquity, and because mobile phone-based services can only offer marginal improvements, the system stays resilient — it is challenging to overcome the inertia of this invested infrastructure”

What is the invested infrastructure in Africa and how will it impact its future?

It is an important question to ask because – as we have seen – companies that leverage invested infrastructure can have a competitive edge, reducing costs and frictions to adoption; those that try to replace it might sink under the weight of high switching costs & behavioral change (although in some cases – boom jackpot 🎰).

If we think of financial infrastructure, in Africa the equivalent of the US card network is a combination of:

a human agent network

phones & SIM cards

tower cells

It hasn’t always been the case. The capillary presence established by telco companies in the continent from the 90s onward, brought along the way important infrastructural development that served as the launchpad to mobile money: financial infrastructure borrowed from the already existing communication infrastructure.

A human agent network could now be used to on-ramp/off-ramp physical cash.

Phones and SIM cards became wallets.

Tower cells relayed information – and now value – across long distances.

Innovation on top of invested infrastructure.

But it’s not over.

As the new payments infrastructure emerged, further developments “up the ladder” could see the light of day: “The combination of USSD-based mobile accounts that worked on every phone and cash-in/cash-out agents in nearly every neighborhood and village proved to be powerful infrastructure on which to build new product offerings”.

The first wave of successful tech businesses on the continent – real “market-creating” innovations – are the product of it.

Examples:

First generation: pay-as-you-go solar (like M-Kopa)

Second generation: digital lending

Access to energy & access to credit. Both are built on top of mobile money infrastructure, built on top of telco’s invested infrastructure.

What lessons can we take home from this chapter?

invested infrastructure matters

it looks different in Africa than in other places

opportunities exist for those who build on top of it + those who make it more efficient

Personally, I find myself asking the question” What’s the invested infrastructure here?”. And not just for payments, but for commerce, logistics, agriculture etc.. In short, it translates to: how things are done now, how much does it cost to switch and who has interest in doing it?

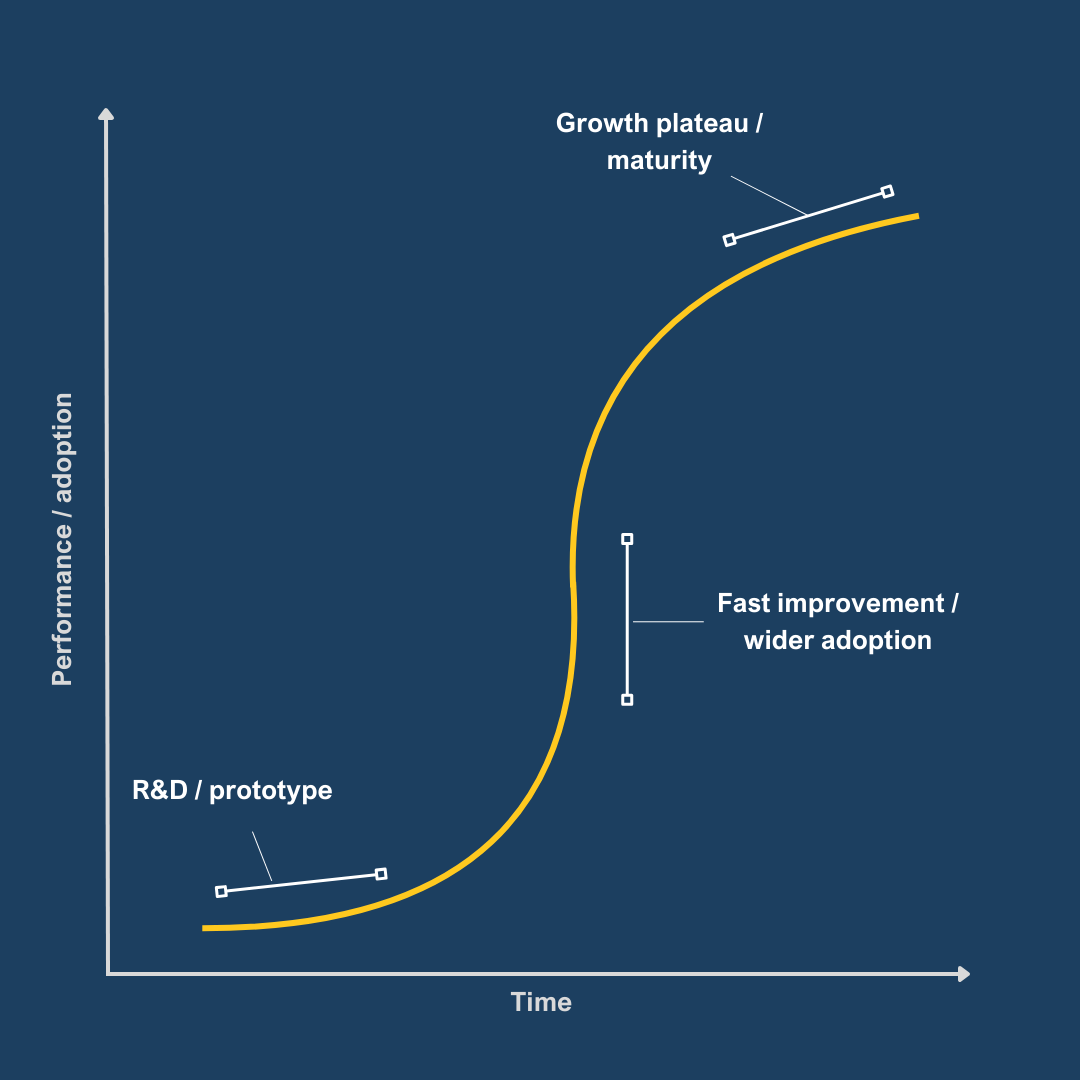

S-curves describe the performance of a new technology – or a technological toolset – over time.

In the beginning, during the R&D and prototyping phase, adoption is minimal and the potential of tech still needs to be validated. The curve is flat and growing slowly. Think of electric cars 15 years ago. It is the territory of university budgets, public finance, and research grants.

When the tech starts showing signs of improvement, it is followed by a steep acceleration in performance and increased adoption. Think of Generative AI one year ago. It is the land of VCs, profiting “by investing in emerging tech before it’s mainstream and exiting when growth plateaus”.

Finally, when a technology is mature, adoption widespread and there is little room for marginal improvements: the tail of the curve flattens. It is the PE and stock market game.

And then, onto the next technology, that will replace the incumbent with the next S-curve. Venture capital funding follows the S-curves cycle, the peak funding being when the curve is at its highest steep.

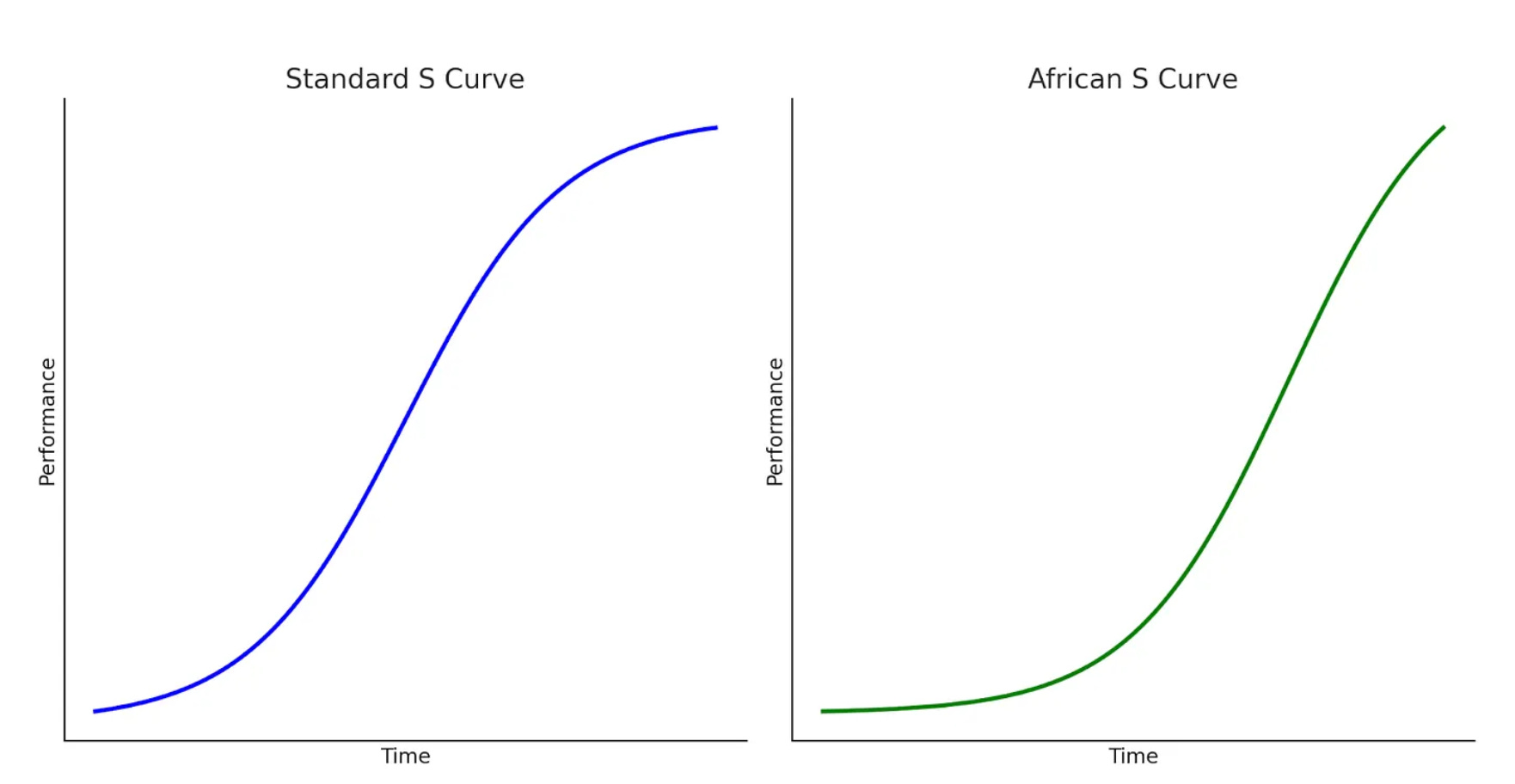

Now: in the wake of funding drought, startup bankruptcies, and crowding away of international investors, what can we say about the shape of the African S-curve?

One: African S curves have much longer tails.

This means that it takes more time for tech in Africa to see widespread adoption. Rather than a limit to technology performance, the problem lies in the lack of market readiness.

Read: “Customers don’t need new tech, or don’t trust new tech, or can’t afford new tech, or don’t have access to infrastructure for new tech, or don’t believe new tech provides enough value vs. old tech”

Two: African S curves have much steeper slopes

On the contrary, once adoption kicks in, the potential for improvements in technology can last for a very long time, going beyond what was once imagined.

The acceleration phase lasts a long time along with its benefits.

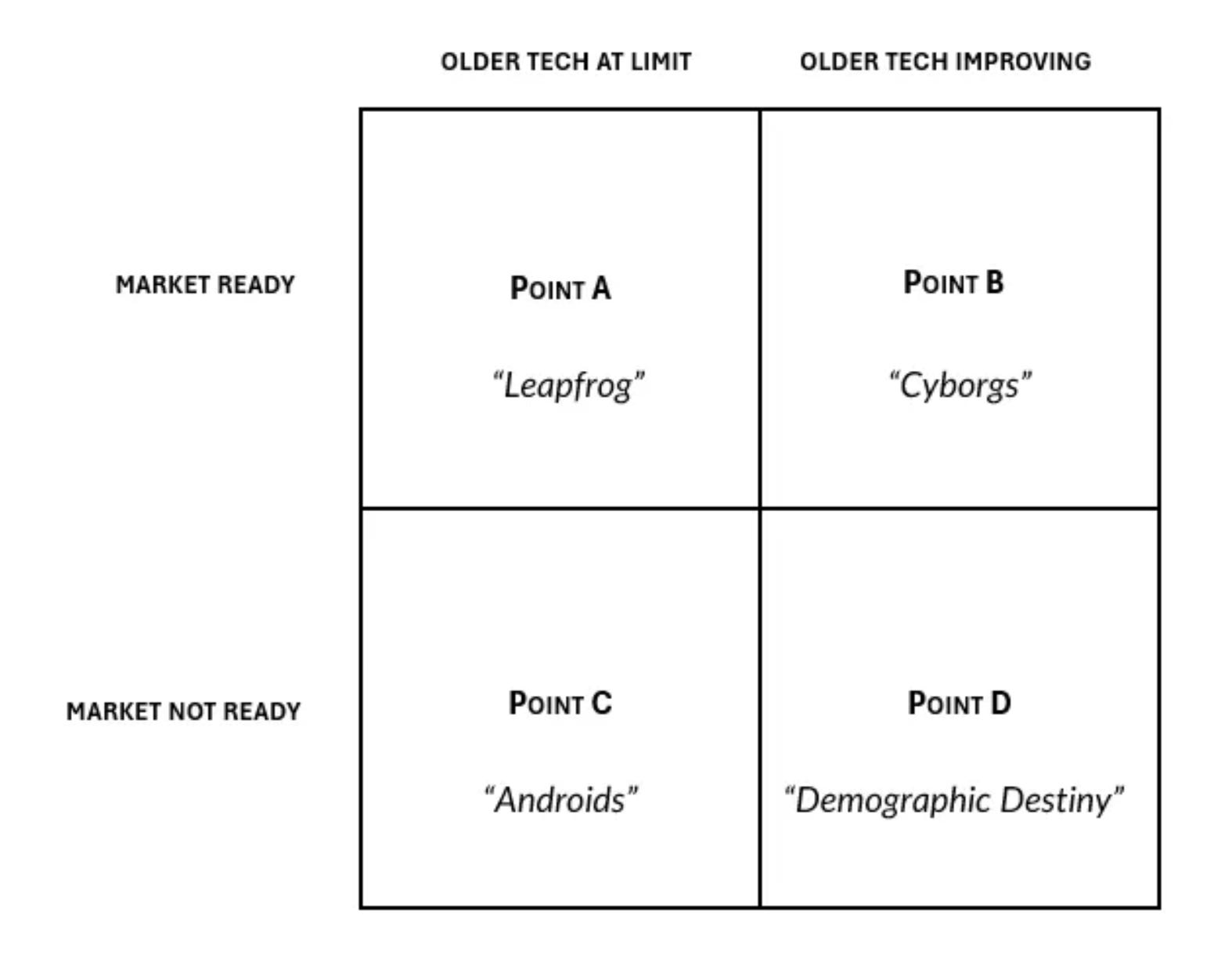

How do we change from one S-curve to the other? When will the new tech replace the old one?

There are 4 different scenarios.

If the old tech is not improving, and the market is ready for a novel solutions, then we’ll have a quick transition. This means heading towards Point A, and what people cheer as Africa’s technology leapfrog.

On the opposite side, if incumbents are delivering increasingly better utility to consumers, who are not ready to change for newcomers, then we’ll have a very gradual and slow transition. Ergo, heading towards Point D.

Many people either bought the point A narrative (technology leapfrog), or buys into point C one. They think old tech is crap, inefficient, and not making any progress. However, the market is not ready for new digital solutions yet. It’s a matter of time.

Stephen Deng, on the contrary, thinks we are heading towards point B. A situation where yes, the market is not ready, but the old tech – and the ecosystem around it – is still improving.

Think of mobile money. It is a fairly old technology ( and USSD codes), but it can still deliver innovation to its users. Telcos are blending digital offerings into their core model; traditional financial services are integrating with the mobile money ecosystem for seamless interactions; new products are developed on top of it every month.

If MoMo is the old tech, the new tech would be close to neo-banks like Djamo. How many customers does one have vs the other?

The shelf life of telecommunications technology has been pretty long. No surprise than that the true champions of tech in the continent are telcos. Companies like MTN, Airtel, Safaricom. This is in stark contrast with the Google, the Meta and the Microsoft of North America.

The main argument is the following: from now on, until we reach point B, a lot of incremental innovations will be built around the existing tech. We need to surf it 🏄🏽♂️

It is what Deng calls the “cybernetic commerce” area, yet another version of the Cyborg thesis.

The most interesting element of this article, to me, is the mental framework that comes with it: how many incremental innovations can still be built on top of the existing rails?

When you look at African markets overall, you’ll see that a lot of problems can be solved with existing technologies. There is no need for a breakthrough.

How to deliver the benefits of tech without losing money: this is the number one skill a founder must have.

This is the end, my friends. I hope you enjoyed the read. Writing this piece I’ve noticed that – as telcos in Africa – my essays have room for improvement. In particular, from now on I will try to deliver:

more real-life examples (what companies, what products etc…) → it helps with mental clarity when you have more than 1/2 examples

more exit simulations (revenues, potential returns) → VC exists where outsized returns exist, and we need to be more rigorous on that.

Les alternatives se présentent sous diverses formes et peuvent servir d’outils puissants pour atteindre la croissance, réduire la volatilité et améliorer la diversification du portefeuille.

Ces dernières années, il y a eu un virage croissant vers les investissements alternatifs dans le monde financier. Pourtant, malgré cette tendance, de nombreux investisseurs perçoivent encore les alternatives comme une catégorie d’investissement exclusive et étroite réservée à quelques-uns.

Cette perception est cependant loin d’être exacte. Les investissements alternatifs sont un domaine diversifié et expansif, offrant une vaste gamme d’actifs et de stratégies qui peuvent potentiellement bénéficier à un large éventail d’investisseurs.

Ces options d’investissement non traditionnelles se présentent sous diverses formes et peuvent servir d’outils puissants pour atteindre la croissance, réduire la volatilité et améliorer la diversification du portefeuille.

En nous plongeant dans le monde des investissements alternatifs, nous explorerons comment ces actifs sortent de leur statut de niche et deviennent de plus en plus accessibles à un public plus large d’investisseurs.

Les investissements alternatifs sont des actifs financiers qui ne relèvent pas des catégories d’investissement conventionnelles que sont les actions, les obligations et les liquidités. Ces investissements non traditionnels peuvent inclure le capital-investissement, le capital-risque, les fonds spéculatifs, l’immobilier, les matières premières, et même des actifs tangibles comme l’art ou les objets de collection.

Caractéristiques clés des investissements alternatifs :

Faible corrélation avec les marchés traditionnels : Les investissements alternatifs ne suivent souvent pas les mêmes tendances que les actions et les obligations, offrant ainsi des avantages de diversification.

Potentiel de rendements plus élevés : De nombreux investissements alternatifs offrent la possibilité de rendements supérieurs à la moyenne, bien que souvent avec un risque plus élevé.

Moins de liquidité : Les actifs alternatifs sont généralement plus difficiles à acheter et à vendre rapidement comparés aux actions ou obligations.

Réglementation limitée : De nombreux investissements alternatifs sont soumis à une surveillance réglementaire moindre que les titres traditionnels.

Frais plus élevés : Les investissements alternatifs sont souvent associés à des frais de gestion et de performance plus élevés.

Complexité : Ces investissements peuvent être plus complexes et peuvent nécessiter des connaissances spécialisées pour être compris et gérés efficacement.

Alternatives vs. Actifs Traditionnels

Les investissements traditionnels comme les actions et les obligations sont généralement très liquides, échangés sur des marchés publics, et ont une forte corrélation avec les mouvements du marché global. Ils sont également généralement plus transparents et soumis à des réglementations plus strictes.

En revanche, les investissements alternatifs peuvent être moins liquides, impliquent souvent des marchés publics et privés, et ont une corrélation plus faible avec les tendances générales du marché. Ils nécessitent fréquemment une gestion plus active et peuvent offrir le potentiel de rendements plus élevés, bien que potentiellement avec un risque plus élevé.

Types d’investissements alternatifs

Capital-Investissement (Private Equity) : Cela implique d’investir dans des entreprises privées ou des rachats d’entreprises publiques. En Afrique, le capital-investissement a joué un rôle crucial dans des secteurs comme les télécommunications, avec des entreprises comme Helios Investment Partners réalisant des investissements significatifs dans des sociétés comme Helios Towers.

Fonds Spéculatifs (Hedge Funds) : Ce sont des fonds gérés activement qui utilisent des stratégies d’investissement avancées. Bien que moins courants en Afrique, certains fonds spéculatifs se concentrent sur les marchés africains, comme Steyn Capital Management en Afrique du Sud.

Immobilier : Cela peut inclure des investissements directs dans des propriétés ou des fonds d’investissement immobilier (REITs). Le marché immobilier africain offre des opportunités significatives, avec une urbanisation rapide stimulant la demande dans des pays comme le Kenya et le Nigeria.

Matières Premières : Cela inclut des investissements dans des matières premières comme l’or, le pétrole ou les produits agricoles. L’Afrique est riche en ressources naturelles, rendant les investissements dans les matières premières particulièrement pertinents. Par exemple, investir dans des entreprises impliquées dans l’extraction d’or au Ghana ou la production de cacao en Côte d’Ivoire.

Infrastructure : Investissements dans des systèmes physiques comme les réseaux de transport, l’énergie ou les systèmes d’eau. L’Afrique présente un déficit important en infrastructures, offrant de nombreuses opportunités d’investissement, comme des projets d’énergie renouvelable dans des pays comme le Maroc ou le Kenya.

Capital-Risque (Venture Capital) : Cela implique d’investir dans des entreprises en phase de démarrage avec un fort potentiel de croissance. L’écosystème des startups technologiques en Afrique est en plein essor, avec des startups attirant des capitaux-risque significatifs. Les investisseurs peuvent participer à cet espace via des fonds de capital-risque, qui regroupent le capital de multiples investisseurs pour soutenir un portefeuille de startups. Par exemple, des fonds comme Future Africa investissent activement dans des entreprises technologiques africaines prometteuses.

Mythes sur les investissements alternatifs

Mythe : Les alternatives sont réservées aux ultra-riches.

Réalité : Bien que certains investissements alternatifs nécessitent des investissements minimums élevés, beaucoup sont désormais accessibles à un plus large éventail d’investisseurs via des fonds communs de placement et des ETFs.

Mythe : Les alternatives sont toujours à haut risque.

Réalité : Bien que certains investissements alternatifs comportent un risque élevé, d’autres peuvent en fait aider à réduire le risque global du portefeuille grâce à la diversification.

Mythe : Les alternatives surpassent toujours les investissements traditionnels.

Réalité : Les performances varient largement parmi les investissements alternatifs, et ils ne surpassent pas toujours les actions et les obligations.

Mythe : Les alternatives sont trop complexes pour les investisseurs moyens.

Réalité : Bien que certaines alternatives soient complexes, d’autres, comme l’immobilier ou les investissements dans les matières premières, peuvent être assez simples.

Mythe : Les alternatives sont complètement illiquides.

Réalité : La liquidité varie largement parmi les investissements alternatifs. Certains, comme certains fonds spéculatifs, offrent des opportunités de rachat régulières.

Avantages et inconvénients des investissements alternatifs

Avantages :

Diversification : Les alternatives peuvent aider à répartir le risque dans un portefeuille.

Potentiel de rendements plus élevés : Certaines alternatives offrent la possibilité de rendements supérieurs à la moyenne.

Couverture contre l’inflation : Certaines alternatives, comme l’immobilier et les matières premières, peuvent fournir une protection contre l’inflation.

Accès à des opportunités uniques : Les alternatives peuvent offrir une exposition à des investissements non disponibles sur les marchés publics.

Inconvénients :

Frais plus élevés : De nombreux investissements alternatifs sont associés à des frais de gestion et de performance significatifs.

Moins de liquidité : Il peut être plus difficile de vendre rapidement des investissements alternatifs.

Complexité : Certaines alternatives nécessitent des connaissances spécialisées pour être comprises et gérées efficacement.

Moins de transparence : De nombreux investissements alternatifs fournissent des rapports moins fréquents et détaillés que les investissements traditionnels.

Risque plus élevé : Certains investissements alternatifs comportent un risque de perte plus élevé.

Comment diversifier votre portefeuille avec des investissements alternatifs

Les investissements alternatifs peuvent être un outil puissant pour la diversification du portefeuille, offrant des avantages uniques qui complètent les actifs traditionnels comme les actions et les obligations. Voici comment vous pouvez utiliser les alternatives pour créer un portefeuille d’investissement plus robuste et diversifié :

Comprendre le concept de complémentarité : La clé d’une diversification efficace avec les alternatives réside dans le concept de complémentarité. Cela se réfère à la manière dont différents actifs évoluent les uns par rapport aux autres sous diverses conditions de marché. En sélectionnant des investissements qui ne se déplacent pas toujours dans la même direction, vous pouvez réduire le risque global du portefeuille. Par exemple, tandis que les actions peuvent lutter en période de ralentissement économique, certains investissements alternatifs comme l’or ou les fonds spéculatifs peuvent bien performer, équilibrant ainsi la performance de votre portefeuille.

Considérez différents horizons temporels et liquidités : Les investissements alternatifs ont souvent des horizons temporels plus longs et une liquidité plus faible comparés aux actifs traditionnels. Cela peut en fait être bénéfique pour la diversification du portefeuille. En incluant des investissements avec des horizons temporels variés, vous créez un portefeuille qui équilibre la flexibilité à court terme avec la stabilité à long terme.

Diversifiez à travers les marchés et les industries : Lors de l’intégration des alternatives, regardez au-delà des classes d’actifs. Diversifiez à travers différents marchés et industries. Par exemple, dans les investissements en capital-investissement ou en dette, choisissez des entreprises de secteurs complémentaires. Pour l’immobilier, répartissez les investissements à travers différents types de propriétés ou emplacements géographiques. Avec les matières premières, envisagez un mélange de différentes ressources comme les métaux, l’énergie et les produits agricoles. Cette approche aide à protéger votre portefeuille contre les baisses spécifiques à un secteur.

Équilibrez les niveaux de risque : Différents investissements alternatifs viennent avec des niveaux de risque variés. Considérez comment ces risques complètent le profil de risque existant de votre portefeuille. Par exemple, les investissements à plus long terme comme le capital-investissement peuvent offrir un risque de marché plus faible en raison de leurs horizons temporels prolongés. Les actifs physiques comme l’immobilier ou les objets de collection peuvent avoir un risque de marché plus faible mais un risque physique plus élevé (dommages, vol). L’objectif est de sélectionner des alternatives qui aident à équilibrer le risque global de votre portefeuille.

Utilisez des fonds d’investissement alternatifs : Pour de nombreux investisseurs, surtout ceux qui débutent avec les alternatives, l’utilisation de fonds d’investissement alternatifs peut être une bonne stratégie. Ces fonds, qui peuvent inclure des fonds spéculatifs, des fonds de capital-investissement ou des fonds d’investissement immobilier (REITs), offrent une gestion professionnelle et une diversification intégrée au sein de l’espace alternatif.

Envisagez des alternatives internationales : Regarder au-delà de votre marché domestique peut fournir des avantages supplémentaires de diversification. Les investissements alternatifs internationaux peuvent aider à se protéger contre les problèmes économiques spécifiques à un pays et fournir une exposition à différentes opportunités de croissance.

Commencez petit et augmentez progressivement l’exposition : Si vous êtes nouveau dans les investissements alternatifs, il est judicieux de commencer avec une petite allocation et d’augmenter progressivement votre exposition à mesure que vous vous familiarisez avec le comportement de ces actifs dans votre portefeuille.

Rebalancement régulier : Comme pour toute stratégie d’investissement, un rebalancement régulier est essentiel. Étant donné que les investissements alternatifs peuvent être moins liquides, il est important de revoir régulièrement votre portefeuille et d’effectuer des ajustements pour maintenir votre allocation d’actifs souhaitée.

En intégrant de manière réfléchie des investissements alternatifs dans votre portefeuille, vous pouvez potentiellement améliorer les rendements tout en réduisant le risque global. Cependant, il est important de se rappeler que les alternatives viennent avec leurs propres ensembles uniques de risques et de défis.

Comment investir dans les alternatives

Investissement direct : Pour ceux avec un capital significatif, investir directement dans des entreprises privées, l’immobilier ou les matières premières est une option.

Fonds : Les fonds communs de placement et les fonds négociés en bourse (ETFs) axés sur des actifs alternatifs offrent un point d’entrée plus accessible pour de nombreux investisseurs.

Plateformes d’investissement : Les plateformes numériques rendent les investissements alternatifs plus accessibles. Par exemple, Daba est une plateforme qui permet aux investisseurs d’accéder aux investissements dans les startups africaines et les fonds de capital-risque, un marché traditionnellement difficile d’accès pour les investisseurs individuels.

Fonds d’investissement immobilier (REITs) : Ceux-ci offrent un moyen d’investir dans l’immobilier sans posséder directement des propriétés.

Crowdfunding : Certaines plateformes permettent aux investisseurs de regrouper leur argent pour investir dans des alternatives comme l’immobilier ou les startups.

ETFs de matières premières : Ceux-ci fournissent une exposition aux matières premières sans avoir besoin de posséder directement l’actif physique.

Les plateformes d’investissement comme Daba sont particulièrement intéressantes pour ceux qui cherchent à investir dans des alternatives africaines. La plateforme permet aux investisseurs de soutenir des startups africaines prometteuses, offrant une exposition à l’écosystème technologique en pleine croissance du continent. Ce type de plateforme démocratise l’accès aux investissements en capital-risque, qui étaient traditionnellement disponibles uniquement pour les investisseurs institutionnels ou les individus à haute valeur nette.

Lors de la considération des investissements alternatifs, il est crucial de faire des recherches approfondies et de comprendre les risques impliqués. Bien que les alternatives puissent offrir des avantages significatifs, elles comportent également des défis uniques. Il est souvent judicieux de commencer petit et d’augmenter progressivement l’exposition à mesure que vous vous familiarisez avec ces types d’investissements.

Pour les investisseurs africains, ou ceux intéressés par les marchés africains, les alternatives présentent des opportunités uniques. La croissance économique rapide du continent, sa population jeune et ses marchés financiers en développement créent un terrain fertile pour les investissements alternatifs. Des startups technologiques à Lagos aux fermes solaires au Maroc, des projets d’infrastructure au Kenya aux investissements dans les matières premières à travers le continent, l’Afrique offre une gamme diversifiée d’options d’investissement alternatives.

Cependant, il est important de noter que l’investissement dans les alternatives africaines comporte également des risques uniques, notamment l’instabilité politique, la volatilité des devises et des cadres réglementaires moins développés dans certains pays. Comme pour tout investissement, une diligence raisonnable approfondie et une compréhension claire des risques et des récompenses potentielles sont essentielles.

En conclusion, bien que les investissements alternatifs aient été autrefois considérés comme une zone de niche pour les investisseurs sophistiqués, ils deviennent de plus en plus une considération courante pour la diversification du portefeuille.

Alors que le paysage de l’investissement évolue, en particulier dans des marchés dynamiques comme l’Afrique, les alternatives offrent des opportunités passionnantes pour ceux qui sont prêts à aller au-delà des actifs traditionnels. Que ce soit via des classes d’actifs alternatifs établies ou des plateformes innovantes comme Daba, les investisseurs ont désormais plus d’options que jamais pour diversifier leurs portefeuilles et accéder à des opportunités d’investissement uniques.

Alternatives come in various forms and can serve as powerful tools for achieving growth, reducing volatility, and enhancing portfolio diversification.

In recent years, there’s been a growing shift towards alternative investments in the financial world. Yet, despite this trend, many investors still perceive alternatives as an exclusive, narrowly defined investment category reserved for a select few.

This perception, however, is far from accurate. Alternative investments are a diverse and expansive field, offering a wide array of assets and strategies that can potentially benefit a broad range of investors.

These non-traditional investment options come in various forms and can serve as powerful tools for achieving growth, reducing volatility, and enhancing portfolio diversification.

As we delve into the world of alternative investments, we’ll explore how these assets are breaking out of their niche status and becoming increasingly accessible to a wider audience of investors.

Alternative investments are financial assets that fall outside the conventional investment categories of stocks, bonds, and cash. These non-traditional investments can include private equity, venture capital, hedge funds, real estate, commodities, and even tangible assets like art or collectibles.

Key Features of Alternative Investments:

Low correlation with traditional markets: Alternative investments often don’t move in tandem with stocks and bonds, providing diversification benefits.

Potential for higher returns: Many alternative investments offer the possibility of above-average returns, though often with higher risk.

Less liquidity: Alternative assets are typically harder to buy and sell quickly compared to stocks or bonds.

Limited regulation: Many alternative investments face less regulatory oversight than traditional securities.

Higher fees: Alternative investments often come with higher management and performance fees.

Complexity: These investments can be more complex and may require specialized knowledge to understand and manage effectively.

Alternatives vs. Traditional Assets

Traditional investments like stocks and bonds are typically highly liquid, traded on public markets, and have a high correlation to overall market movements. They’re also generally more transparent and subject to stricter regulations.

In contrast, alternative investments may be less liquid, often involve both public and private markets, and have a lower correlation to broad market trends. They frequently require more active management and can offer the potential for higher returns, albeit with potentially higher risk.

Types of Alternative Investments

Private Equity: This involves investing in private companies or buyouts of public companies. In Africa, private equity has played a crucial role in sectors like telecommunications, with firms like Helios Investment Partners making significant investments in companies like Helios Towers.

Hedge Funds: These are actively managed funds that use advanced investment strategies. While less common in Africa, some hedge funds focus on African markets, like Steyn Capital Management in South Africa.

Real Estate: This can include direct property investments or real estate investment trusts (REITs). The African real estate market offers significant opportunities, with rapid urbanization driving demand in countries like Kenya and Nigeria.

Commodities: These include investments in raw materials like gold, oil, or agricultural products. Africa is rich in natural resources, making commodity investments particularly relevant. For example, investing in companies involved in gold mining in Ghana or cocoa production in Côte d’Ivoire.

Infrastructure: Investments in physical systems like transportation networks, energy, or water systems. Africa has a significant infrastructure gap, presenting numerous investment opportunities, such as renewable energy projects in countries like Morocco or Kenya.

Venture Capital: This involves investing in early-stage companies with high growth potential. Africa’s tech startup ecosystem is booming, with startups attracting significant venture capital. Investors can participate in this space through venture funds, which pool capital from multiple investors to back a portfolio of startups. For example, funds like Future Africa are actively investing in promising African tech companies.

Myths About Alternative Investments

Myth: Alternatives are only for the ultra-wealthy. Reality: While some alternative investments have high minimum investments, many are now accessible to a broader range of investors through mutual funds and ETFs.

Myth: Alternatives are always high-risk. Reality: While some alternative investments carry high risk, others can actually help reduce overall portfolio risk through diversification.

Myth: Alternatives always outperform traditional investments. Reality: Performance varies widely among alternative investments, and they don’t always outperform stocks and bonds.

Myth: Alternatives are too complex for average investors. Reality: While some alternatives are complex, others, like real estate or commodity investments, can be quite straightforward.

Myth: Alternatives are completely illiquid. Reality: Liquidity varies widely among alternative investments. Some, like certain hedge funds, offer regular redemption opportunities.

Pros and Cons of Alternative Investments

Pros:

Diversification: Alternatives can help spread risk in a portfolio.

Potential for higher returns: Some alternatives offer the possibility of above-average returns.

Inflation hedge: Certain alternatives, like real estate and commodities, can provide protection against inflation.

Access to unique opportunities: Alternatives can provide exposure to investments not available in public markets.

Cons:

Higher fees: Many alternative investments come with significant management and performance fees.

Less liquidity: It can be harder to sell alternative investments quickly.

Complexity: Some alternatives require specialized knowledge to understand and manage effectively.

Less transparency: Many alternative investments provide less frequent and detailed reporting than traditional investments.

Higher risk: Some alternative investments carry a higher risk of loss.

How to Diversify Your Portfolio with Alternative Investments

As established, alternative investments can be a powerful tool for portfolio diversification, offering unique benefits that complement traditional assets like stocks and bonds. Here’s how you can use alternatives to create a more robust and diversified investment portfolio:

Understand the Concept of Complementarity: The key to effective diversification with alternatives lies in the concept of complementarity. This refers to how different assets move in relation to each other under various market conditions. By selecting investments that don’t always move in the same direction, you can reduce overall portfolio risk. For example, while stocks might struggle during an economic downturn, certain alternative investments like gold or hedge funds might perform well, balancing out your portfolio’s performance.

Consider Different Time Horizons and Liquidity: Alternative investments often have longer time horizons and lower liquidity compared to traditional assets. This can actually be beneficial for portfolio diversification. By including investments with varying time horizons, you create a portfolio that balances short-term flexibility with long-term stability.

Diversify Across Markets and Industries: When incorporating alternatives, look beyond just asset classes. Diversify across different markets and industries. For instance, in private equity or debt investments, choose companies from complementary industries. For real estate, spread investments across different types of properties or geographic locations. With commodities, consider a mix of different resources like metals, energy, and agricultural products. This approach helps protect your portfolio from sector-specific downturns.

Balance Risk Levels: Different alternative investments come with varying levels of risk. Consider how these risks complement the existing risk profile of your portfolio. For example, longer-term investments like private equity might offer lower market risk due to their extended time horizons. Physical assets like real estate or collectibles might have lower market risk but higher physical risk (damage, theft). The goal is to select alternatives that help balance out the overall risk of your portfolio.

Use Alternative Investment Funds: For many investors, especially those just starting with alternatives, using alternative investment funds can be a good strategy. These funds, which can include hedge funds, private equity funds, or real estate investment trusts (REITs), offer professional management and built-in diversification within the alternative space.

Consider International Alternatives: Looking beyond your home market can provide additional diversification benefits. International alternative investments can help protect against country-specific economic issues and provide exposure to different growth opportunities.

Start Small and Gradually Increase Exposure: If you’re new to alternative investments, it’s wise to start with a small allocation and gradually increase your exposure as you become more comfortable with how these assets behave in your portfolio.

Regular Rebalancing: As with any investment strategy, regular rebalancing is key. Because alternative investments can be less liquid, it’s important to regularly review your portfolio and make adjustments to maintain your desired asset allocation.

By thoughtfully incorporating alternative investments into your portfolio, you can potentially enhance returns while reducing overall risk. However, it’s important to remember that alternatives come with their own unique sets of risks and challenges.

How to Invest in Alternatives

Direct Investment: For those with significant capital, directly investing in private companies, real estate, or commodities is an option.

Funds: Mutual funds and exchange-traded funds (ETFs) focused on alternative assets provide a more accessible entry point for many investors.

Investment Platforms: Digital platforms are making alternative investments more accessible. For example, Daba is a platform that allows investors to access African startup and venture fund investments, traditionally a difficult market for individual investors to enter.

Real Estate Investment Trusts (REITs): These provide a way to invest in real estate without directly owning property.

Crowdfunding: Some platforms allow investors to pool money to invest in alternatives like real estate or startups.

Commodity ETFs: These provide exposure to commodities without the need to directly own the physical asset.

Investment platforms like Daba are particularly interesting for those looking to invest in African alternatives. The platform allows investors to back promising African startups, providing exposure to the continent’s rapidly growing tech ecosystem. This type of platform democratizes access to venture capital investments, which were traditionally only available to institutional investors or high-net-worth individuals.

When considering alternative investments, it’s crucial to do thorough research and understand the risks involved. While alternatives can offer significant benefits, they also come with unique challenges. It’s often wise to start small and gradually increase exposure as you become more comfortable with these investment types.

For African investors, or those interested in African markets, alternatives present unique opportunities. The continent’s rapid economic growth, young population, and developing financial markets create a fertile ground for alternative investments. From tech startups in Lagos to solar farms in Morocco, from infrastructure projects in Kenya to commodity investments across the continent, Africa offers a diverse range of alternative investment options.

However, it’s important to note that investing in African alternatives also comes with unique risks, including political instability, currency volatility, and less developed regulatory frameworks in some countries. As with any investment, thorough due diligence and a clear understanding of the risks and potential rewards are essential.

In conclusion, while alternative investments were once seen as a niche area for sophisticated investors, they are increasingly becoming a mainstream consideration for portfolio diversification.

As the investment landscape evolves, particularly in dynamic markets like Africa, alternatives offer exciting opportunities for those willing to venture beyond traditional assets. Whether through established alternative asset classes or innovative platforms like Daba, investors now have more options than ever to diversify their portfolios and tap into unique investment opportunities.

Contributed by Mathias Léopoldie, Co-Founder of Julaya via Realistic Optimist.

Optimizing for home runs

It is said that the first venture capital (VC) firm was founded in 1946, in the USA. The American Research & Development Corporation (ARDC) became famous for its $70,000 investment in Digital Equipment Corporation, a computer manufacturer, which went public in 1967 at a whopping $355M valuation. Investors taking risky bets on companies wasn’t new, but the computer era put venture capital’s singular “power law” on full display.

A baseball game is an apt analogy to conceptualize how venture capital works. The most exciting play, which also brings outsized returns, is when the ball skyrockets over the fence resulting in a home run.

VC is quite similar, as the power law nature implies that a few investments (<5%) will drive most of a fund’s returns. While the number of home runs in baseball might not guarantee winning the season, it does in VC.

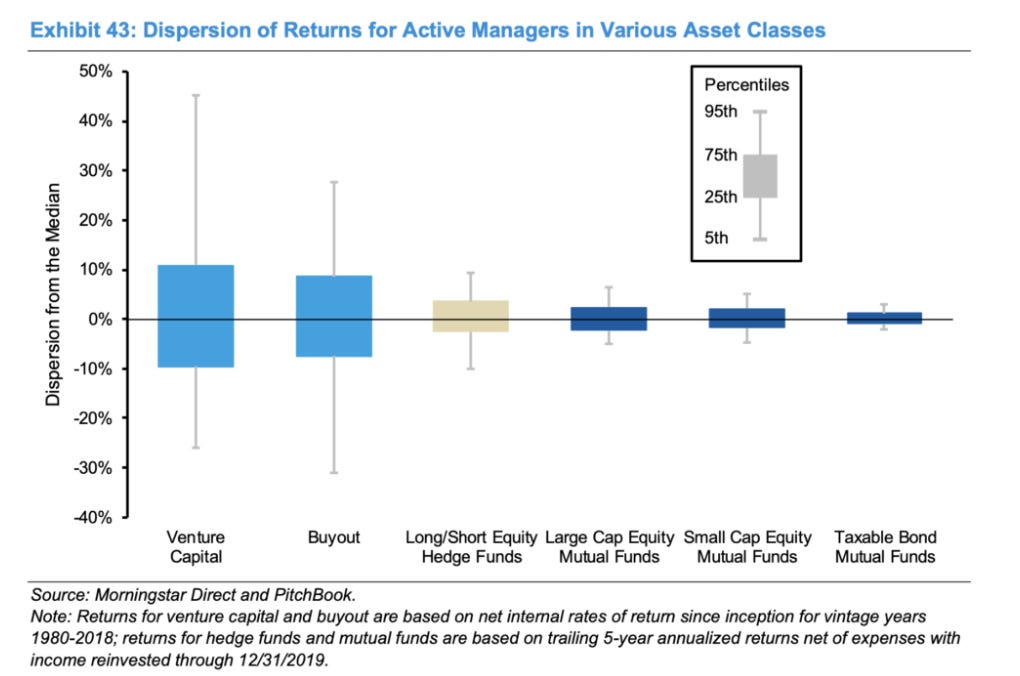

This is why VC is an exciting asset class: sharp skill and experience are necessary, but luck plays a non-negligible role. It is no surprise that, amongst asset classes, VC has the highest dispersion of returns. Participants can either win big or lose a lot.

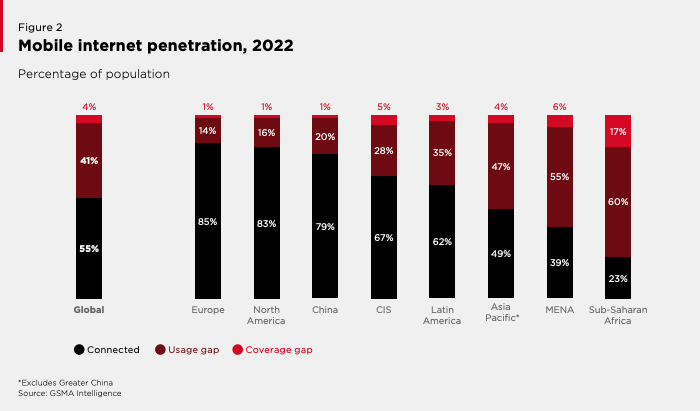

The African VC ecosystem is young, inching past its first decade of existence. The African internet revolution took a different shape than it did elsewhere: between 2005 and 2019, the share of African households possessing a computer went from 4% to 8%, while other developed economies witnessed a 55% to 80% jump over the same period.

One can’t expect a VC industry to suddenly flourish in an economy where microchip-equipped computer and smartphone ownership is so scarce. The heart of the VC industry is called “Silicon Valley” for a reason.

Another trend, however, calls our attention. Namely, the rise of mobile phones on the continent. Currently, over 80% of Africans own a mobile phone, a figure that reaches close to 100% in some countries. The 2000s-2010s feature phone mass production era is to thank. Transsion Holdings, a Chinese public company, tops the leaderboard in terms of mobile phones sold in Africa, through its portfolio of brands (Tecno, Itel, and Infinix).

This offline, ‘computerized’ revolution of sorts is significant for the continent, as a large part of Sub-Saharan Africa’s population still lacks internet access. This includes people who own a feature phone but no smartphone, or people for whom the cost of internet data is prohibitively expensive. Internet’s geographical reach in Africa also remains patchy, further complicating the equation.

Unsurprisingly, telecom operators have emerged as this mobile phone revolution’s winners. The mobile money industry is a striking example: a fertile mix of USSD technology and agent networks enabled telecom operators to become fintech companies as far back as 2007. Those same telcos now derive a significant amount of their business from the financial services they ushered in. M-Pesa, Kenya’s leading mobile money service provider, now accounts for more than 40% of Safaricom’s (its parent telecom operator) mobile service revenue.

In Sub-Saharan Africa, 55% of the population possesses a financial account, with mobile money’s rise boosting that number in recent years. That’s approximately double the amount of Africans with an internet connection.

Too early to call

In this context, many are the Cassandras lamenting venture capital’s failure in Africa. These conclusions seem premature, both because the industry itself is novel but also because the digital ecosystem it operates in is still nascent.

Even by removing Africa from the picture, venture capital is a long-term industry, and its illiquidity can lead to prolonged exit times. According to Dealroom, only 17% of portfolio startups globally exit within the investment period of 10 years. Initial, tangible VC investments in Africa debuted around 2012. We believe that the pessimists are neither right nor wrong: they’re just pontificating too early.

That being said, the past decade has drawn the contours of what can be improved and highlighted what has worked.

# years it takes for portfolio startups to exit, along with exit size (Dealroom)

The casino analogy

Casinos constitute another pertinent venture capital analogy. Addiction and money laundering aside, a casino is a fascinating business. In a casino, a few people win exuberant amounts, while the many ‘losers’ subsidize the entire operation. In return for setting up the infrastructure, applying rules, and mediating disputes, the casino pockets a handsome amount of the proceeds as profits.

Venture capital’s logic is similar to a casino’s. “Winners” are the top decile of skilled VC funds reaping outsized returns. “Losers” are the VC funds that don’t return the amount of money they promised their investors (LPs). The casino itself is the government, collecting tax revenue in return for organizing the game.

Without casinos’ power law gains distribution, no one would play. It is by design that ‘returns’ are extremely skewed, enabling the casino economy to work. VC is similar: it is by design that most of the returns come from the top decile funds and companies because winning in venture capital is hard. It wouldn’t be possible without the entire ecosystem structure, and failing companies still provide tremendous value to the other players.

Mixing profitability and venture scale

While far from a solely African problem, the confusion between these two terms may cause damage. In light of hostile, macroeconomic conditions, many Africa-focused VCs have started demanding that their startups reach “profitability” even if this means compromising on hyper-growth.

This is partly a mistake: if investors want to invest in profitable African businesses, they can invest in African banks for example, which exhibit fantastic ROIs. Or switch to private equity. But that isn’t the VC game.

VCs demanding that their portfolio companies, especially young ones (pre-seed and seed stages), become profitable quasi-eliminates any potential “home-run” companies. The latter can only emerge through market share dominance, a process facilitated by operating at a company-level loss when competitors can’t. Those home-run companies are the only way a VC can reach the outsized returns it promised its LPs.

Herein lies the confusion between profitability as a whole and positive unit economics at the marginal level. VCs should be encouraging their portfolio companies to reach “venture scale”. Venture scale is the ability to grow at a decreasing and very efficient marginal cost. This implies tinkering and getting unit economics to a point where the revenue generated from each unit sold is superior to what it costs to make it. This metric is referred to as the “contribution margin”.

A company with a positive contribution margin, which can be unprofitable as a whole because it has very high fixed costs (such as R&D), has a clear path to long-term profitability. This justifies pumping large amounts of money into it, enabling the company to reach the economies of scale it needs to win.

Companies continuing their fundraising route, and even going public, with iffy contribution margins either speed-run their death (Airlift) or make their lives significantly harder (SWVL). Those are the business models VCs should be wary of. However, a blind focus on company-level profitability for the sake of profitability doesn’t make much sense in the VC context. There are very useful data points that companies can follow to see if they are on the right path, such as the “burn multiple” or the “magic number”.

VCs investing in African startups should be cognizant of this difference as they hit the brakes during the current funding winter.

African VC: Expensive and risky, replete with singular challenges

The early innings of the African venture capital ecosystem have made two things clear: venture capital in Africa is expensive and risky.

It is expensive because lagging infrastructure might nudge startups to build out their own, which costs money, additional time, and expertise. If the infrastructure needed can’t be built in-house, such as public infrastructure (roads, etc…), the startup will have to contend with the higher prices resulting from the existing infrastructure’s inefficiencies. This is a salient problem for logistics startups, for example.

Funding high-growth businesses in Africa can thus turn out to be an expensive endeavor, generating infrastructure costs that wouldn’t be necessary in other, more developed markets.

It is riskier if funded by international funds in international currencies (USD, Euros, GB Pounds, etc…). Take Nigeria for example, one of the continent’s venture capital darlings. Earlier last year, the Central Bank of Nigeria floated the local currency (the naira) away from its traditional peg to the USD, in a bid to liberalize the economy. The move led to the naira’s sharp and sudden devaluation, revealing overarching uncertainty about its strength.

This was a disaster for Nigerian startups, especially those that reported their revenue numbers in dollars (a given if foreign investors are on the cap table). The devaluation meant that similar revenue in naira from one month to another could render just half the value in dollars.

If Nigerian startups had converted any USD from their funding rounds into naira, their buying power was also drastically slashed. From the investor’s point of view, the startup’s $USD valuation got trimmed almost overnight, due to factors outside the founders’ control. This also creates currency translation issues, making reporting of actual performance of ventures in local and USD currencies trickier and less reliable.

This is not an issue in developed markets with stronger currencies and free capital flows, such as the US or Europe. It can be reasonably assumed that this issue has contributed to Nigeria’s drop in startup investment.

To sum it all up: African venture capital is expensive because startups have to build out or deal with decrepit infrastructure hence requiring specific business models, and comparatively riskier since valuations are subject to currency-induced volatility.

The past year was also punctuated by the downfall of some well-funded African startups, failures attributed to a nebulous mix of founder wrongdoing, financial mismanagement, and outright fraud. As is often the case, very few people will uncover the full story behind these crashes.

Some observers were quick to generalize the trend, using these failures as proxies to gauge the integrity of all other African founders. Shady founders do and will always exist, regardless of the ecosystem’s maturity. There is an argument to be made that the safeguards against those founders are potentially lower in young ecosystems such as Africa, where governance standards have not yet been standardized and where investors are less aware of African markets’ specific features. That is a solvable problem.

These are normal ecosystem growing pains that need to be rationally addressed but are no cause for doomsday rhetoric.

What’s needed: liquidity

Venture capital’s equation is simple: can you invest in startups that will exit, and will those exits return (much) more money than your LPs put in while creating economic value for the clients, suppliers, and all stakeholders?

Exits, meaning a startup getting acquired or going public, are crucial to the venture capital ecosystem’s health. VCs are investing with the intention of outsized exits, but sometimes those turn out to be impossible. Adverse market conditions, a non-scalable business model, founder conflict… Exits can be jeopardized for various reasons.

When such a situation arises, invested VCs will sometimes face the choice of either settling down for a smaller exit or losing their money outright. We believe that the importance of these small exits, such as “acquihires” should not be underestimated as they remain important for VCs required to distribute to their LPs. Typically, they will also provide cash-outs for angel investors, employees, public institutions, and founders. These cash-outs will hopefully convince these stakeholders to pour money back into the ecosystem, launching a virtuous flywheel.

While the number of exits has been increasing on the continent, actual numbers of their combined value are hard to come through (many deals don’t disclose their terms). Briter Bridges also interestingly notes that the countries and sectors receiving the most amount of funding aren’t necessarily the ones with the most lucrative exit paths.

Liquidity events are essential to Africa’s VC market. So far, most of the attention has gone toward fundraising numbers, a relevant proxy for market sentiment but not market viability or growth. More attention should be paid to the African exit market, its intricacies, its possibilities, and its obstacles.

The future of African M&A

An overwhelming majority of exits for African startups today entail a merger/acquisition (M&A).

Two African M&A trends are likely to materialize over the next couple of years.

First is the consolidation of African startups operating in the same sector yet different geographies, and struggling to live up to the valuation they raised. The recent Wasoko-MaxAB merger announcement is an example of such.

Second is the potential rise of “south-south” startup acquisitions. The socio-demographic similarities between emerging markets make the solution built in one place potentially applicable to another, even thousands of miles away. This seems to be truer for lesser regulated sectors, such as edtech or e-commerce, but harder for more supervised ones, like fintech. The recent Orcas-Baims acquisition is an example of such a deal.

Players such as Brazil’s Ebanx, Estonia’s Bolt, and Russia’s Yango Delivery all operate in Africa and represent new competitors (and potential acquirers) for local African startups. This could stimulate the local M&A scene, but more importantly, entice other well-capitalized startups in emerging markets to expand to Africa.

Conclusion

Venture capital in Africa is a recent phenomenon, one whose success can’t yet be pronounced due to the sector’s long-term nature. These early years have highlighted the specificities of African venture capital, some of which aren’t relatable to more developed markets or even other emerging markets. This means copy-pasting Western frameworks in the African context is a faulty and lazy approach.

Foreign and local VCs investing in African startups should seek to deeply understand the continent’s intricacies, and develop fresh strategies to deal with them.

The ecosystem should give itself time. Adopting a longer-term view discounts short-term pessimism and allows one to rationally solve the challenges that arise. African venture capital can be a fantastic locomotive for African growth, but railroads don’t get built overnight.

As the Bambara saying puts it, munyu tè nimisa : one never regrets patience.

Mathias Léopoldie is the co-founder of Julaya, an Ivory Coast-based startup that offers digital payment and lending accounts for African companies of all sizes. Julaya serves over 1,500 companies, processes $400M of transactions, and has raised $10M in funding.

Julaya has offices in Benin, Senegal, France, and Ivory Coast.

Mathias would like to thank Mohamed Diabi (CEO at AFRKN Ventures) and Hannah Subayi Kamuanga (Partner at Launch Africa Ventures) for their thorough advice on this piece.

Un tableau de capitalisation bien entretenu aide les fondateurs, les investisseurs et les parties prenantes à suivre les parts de propriété, les tours d’investissement et la répartition des actions.

Gérer un tableau de capitalisation, communément appelé “cap table”, est un aspect crucial de la gestion d’une startup. Un tableau de capitalisation bien entretenu aide les fondateurs, les investisseurs et les parties prenantes à suivre les parts de propriété, les tours d’investissement et la répartition des actions.

Ce guide vous présentera les éléments essentiels pour gérer efficacement votre tableau de capitalisation, vous assurant d’avoir les outils et les connaissances nécessaires pour maintenir précision et transparence.

Comprendre le tableau de capitalisation

Un tableau de capitalisation est un tableau détaillé, une feuille de calcul ou un outil logiciel qui décrit les parts de propriété dans une entreprise. Il inclut généralement des informations sur :

Actions des fondateurs : Actions détenues par les fondateurs de l’entreprise.

Actions des investisseurs : Actions détenues par les investisseurs providentiels, les capital-risqueurs et autres investisseurs.

Options d’achat d’actions pour les employés : Actions attribuées aux employés dans le cadre de leur rémunération.

Notes convertibles : Dette pouvant être convertie en actions à un stade ultérieur.

Bons de souscription : Droits d’achat d’actions à un prix prédéterminé.

Un tableau de capitalisation complet fournit un instantané de la répartition des actions de l’entreprise, essentiel pour prendre des décisions éclairées sur les levées de fonds, la dilution des parts de propriété et la croissance future.