La Coupe d’Afrique des Nations (CAN) 2023 débute ce samedi avec la Côte d’Ivoire en tant que pays hôte face à la Guinée-Bissau.

Malgré le fait que le tournoi soit officiellement désigné comme les finales de 2023, il se déroule en 2024.

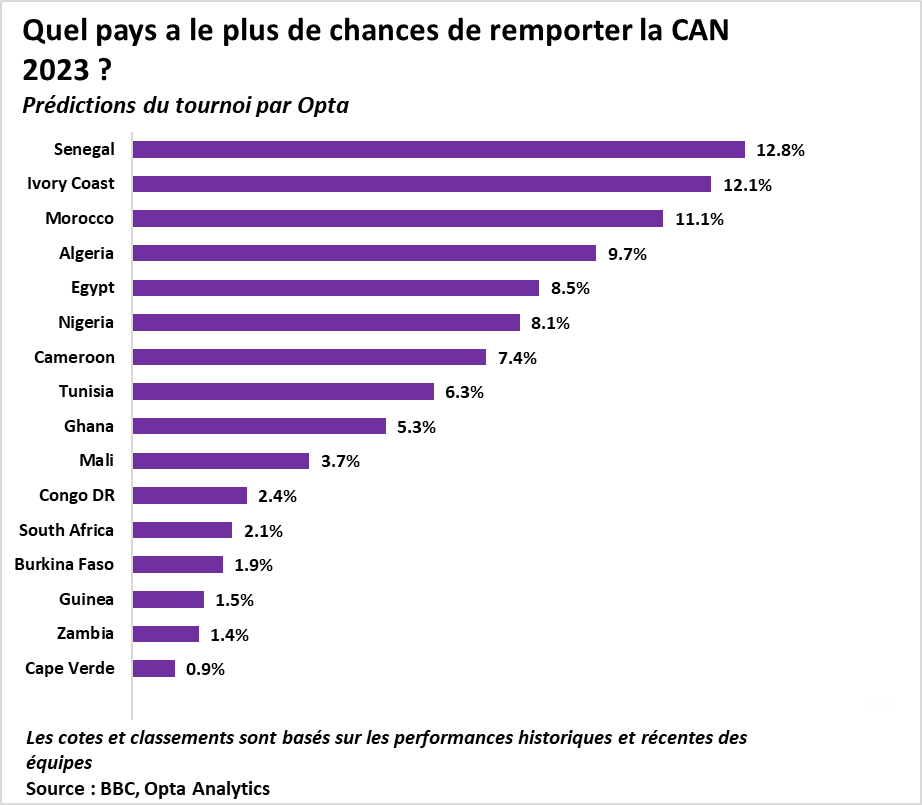

Les champions en titre, le Sénégal, entrent dans la compétition en tant que favoris, cherchant à devenir la quatrième équipe à remporter consécutivement la CAN, un exploit réalisé pour la dernière fois par l’Égypte de 2006 à 2010.

Pour analyser les potentiels vainqueurs, BBC Sport et Opta utilisent un modèle de prédiction basé sur l’intelligence artificielle.

Sadio Mané tient le trophée de la CAN après que le Sénégal soit sorti victorieux lors de la dernière édition du tournoi. Crédit image : Eurosport

Ce modèle examine la probabilité des résultats des matchs – victoire, match nul ou défaite – en incorporant les cotes du marché des paris et les classements des équipes d’Opta, basés sur les performances historiques et récentes.

Il prend également en compte la force de l’adversaire et la difficulté du parcours jusqu’à la finale, en tenant compte de la composition des groupes et des éventuels affrontements en phase éliminatoire.

Selon le modèle de prédiction, le Sénégal émerge en tant que favori avec une probabilité de 12,8 % de remporter le trophée.

La Côte d’Ivoire suit de près avec une probabilité de 12,1 %, cherchant à remporter leur troisième titre de la CAN après leurs victoires en 1992 et 2015.

L’Égypte, pays hôte en 2006, reste le dernier pays hôte à avoir remporté le tournoi.

Le Maroc, cherchant son deuxième titre de la CAN depuis 1976, et l’Algérie complètent le top cinq avec des probabilités de 11,1 % et 9,7 %, respectivement.

L’Égypte, sept fois championne de la CAN, vise la rédemption après leur défaite déchirante face au Sénégal en finale en 2021.

Mohamed Salah, qui a connu la défaite en finale en 2017, est impatient de remporter son premier titre de la Coupe d’Afrique des Nations.

Le modèle de prédiction donne à l’Égypte une probabilité de 16 % d’atteindre une autre finale cette année, marquant un éventuel retour depuis leur dernier triomphe en 2010.

Les sept meilleures équipes selon le modèle de prédiction comprennent également le Nigeria et le Cameroun, tous deux des poids lourds du football africain.

Le Nigeria, trois fois champion de la CAN (1980, 1994 et 2013), a une probabilité de 8,1 % de remporter le trophée, avec Victor Osimhen, le Joueur de l’Année africain 2023, se démarquant comme un buteur redoutable.

Le Cameroun, cinq fois champion (1984, 1988, 2000, 2002 et 2017), a une probabilité de réussite de 7,5 %.

La performance impressionnante d’Osimhen lors des qualifications, où il a marqué 10 buts pour le Nigeria, met en avant la puissance de marquage des Super Eagles, avec 22 buts au total, soit sept de plus que toute autre équipe.

L’équilibre entre les réalisations historiques, les performances récentes des équipes et les contributions individuelles des joueurs façonne les prédictions, faisant de la CAN 2023 une perspective passionnante pour les fans et les passionnés de football.

En conclusion, alors que la Coupe d’Afrique des Nations 2023 se déroule en 2024, la compétition est sur le point de livrer des moments palpitants.

Le modèle de prédiction basé sur l’intelligence artificielle suggère que le Sénégal, la Côte d’Ivoire et l’Égypte sont les principaux prétendants, tandis que le Nigeria et le Cameroun, avec leur riche histoire du football, ajoutent une couche supplémentaire d’excitation au tournoi.

Le terrain est prêt pour une bataille intense alors que ces équipes luttent pour le titre prestigieux du football africain.

Divulgation : Ce blog a été sourcé à partir de Opta Analyst et régénéré à l’aide de l’IA.

The 2023 Africa Cup of Nations (Afcon) kicks off this Saturday with Ivory Coast hosting Guinea-Bissau.

Despite the tournament being officially labeled as the 2023 finals, they are taking place in 2024.

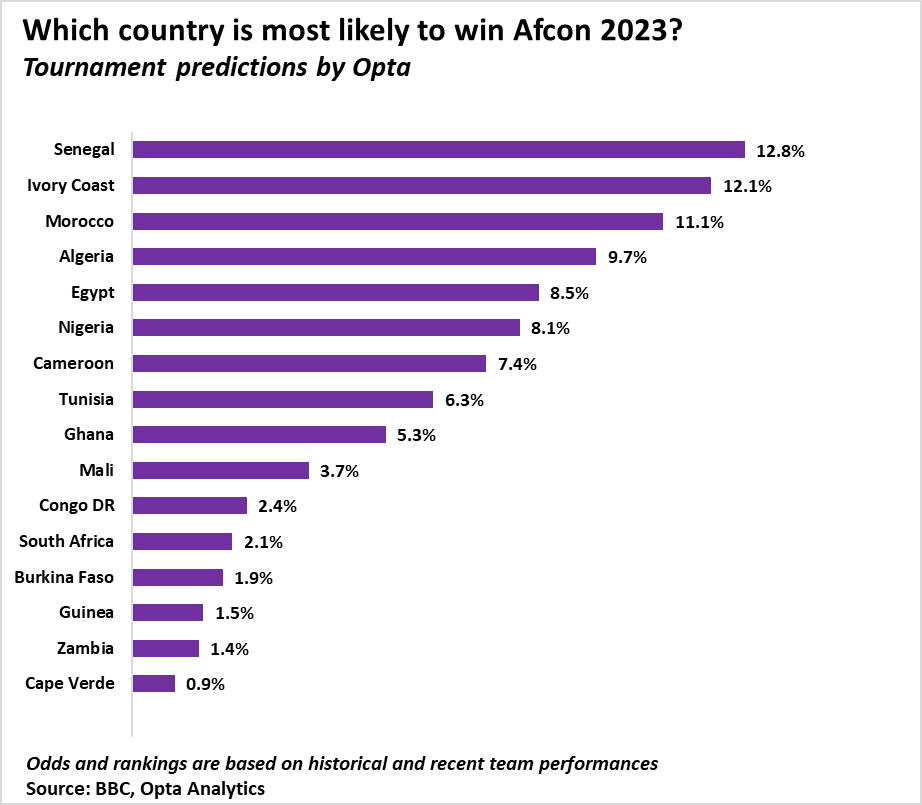

The reigning champions, Senegal, enter the competition as favorites, seeking to become the fourth team to win consecutive Afcons, a feat last achieved by Egypt from 2006 to 2010.

BBC Sport and Opta utilize an artificial intelligence prediction model to analyze the potential winners.

Sadio Mane holds the AFCON trophy after Senegal emerged victorious in the last edition of the tournament. Image credit: Eurosport

This model examines the probability of match outcomes—win, draw, or loss—by incorporating betting market odds and Opta’s team rankings, which are based on historical and recent performances.

It also considers opponent strength and the difficulty of the path to the final, factoring in group compositions and potential knockout stage match-ups.

Senegal emerges as the front-runner with a 12.8% chance of lifting the trophy.

Ivory Coast closely follows with a 12.1% probability, aiming for their third Afcon title after victories in 1992 and 2015.

Egypt, the host nation in 2006, remains the last host to win the tournament.

Morocco, seeking their second Afcon title since 1976, and Algeria round off the top five contenders with 11.1% and 9.7% chances, respectively.

Egypt, a seven-time Afcon champion, eyes redemption after their heartbreaking loss to Senegal in the 2021 final.

Mohamed Salah, who experienced defeat in the 2017 final, is eager to secure his first Africa Cup of Nations title.

The prediction model gives Egypt a 16% chance of reaching another final this year, marking a potential comeback since their last triumph in 2010.

The top seven teams in the predictor model include Nigeria and Cameroon, both heavyweights in African football.

Nigeria, three-time Afcon winners (1980, 1994, and 2013), have an 8.1% chance of lifting the trophy, with Victor Osimhen, the 2023 African Footballer of the Year, standing out as a potent goalscorer.

Cameroon, five-time champions (1984, 1988, 2000, 2002, and 2017), hold a 7.5% chance of success.

Osimhen’s impressive performance in the qualifiers, where he scored 10 goals for Nigeria, emphasizes the Super Eagles’ goal-scoring prowess, with 22 overall goals, seven more than any other side.

The balance between historical achievements, recent team performances, and individual player contributions shapes the predictions, making the 2023 Afcon an exciting prospect for fans and football enthusiasts alike.

In conclusion, as the 2023 Africa Cup of Nations unfolds in 2024, the competition is poised to deliver thrilling moments.

The AI prediction model suggests Senegal, Ivory Coast, and Egypt as the primary contenders. Nigeria and Cameroon, with their rich footballing history, add an extra layer of excitement to the tournament.

The stage is set for an intense battle as these teams vie for the prestigious title in African football.

Disclosure: This blog was sourced from Opta Analyst and re-generated using AI.

There are not many places to look but up in the new year for African tech stakeholders after what turned out to be a tough 2023 for startups globally.

This year, budgets and valuations were cut, business models revised, layoffs were frequent, and some startups shuttered as the harsh realities of a funding downturn, mismanagement, and fraud took their toll on African tech.

It’s time to take stock of the last 12 months in what’s been a rollercoaster year. Read on to discover the major themes in Africa’s tech ecosystem.

The venture funding market shrinks

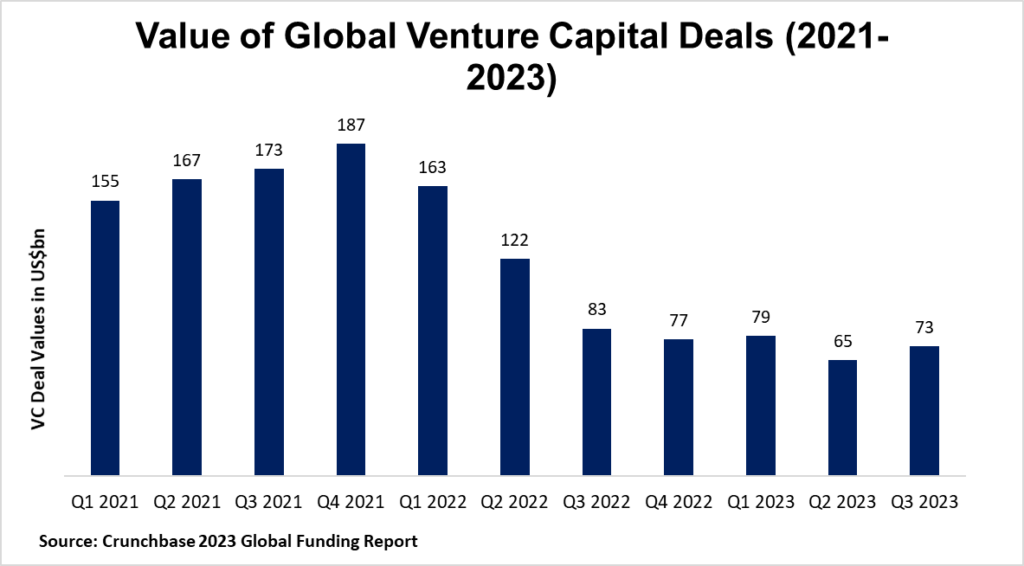

The exuberance of 2022’s VC landscape gave way to a stark reality in 2023, with funding plummeting by around half globally in the first half of the year.

This dramatic shift coincided with hikes in interest rates, which had a chilling effect on fundraising. For every 1% hike in interest rates, there was an alarming 3.2% decline in VC capital.

This tightening environment not only reduced the pool of VC money available to startups but also made debt financing, a potential alternative, a less viable option due to higher borrowing costs.

After a bullish 2022 in which Africa was the only continent to record growth in venture funding values, there was no escaping the downturn this year.

The funding winter reached the continent in the H1 2023. Startup funding plunged to just over $1bn, a stark drop from $3.5bn the year before, per AVCA data.

Investors completed 263 deals – a 40% reduction in both deal volume and funding compared to the previous year.

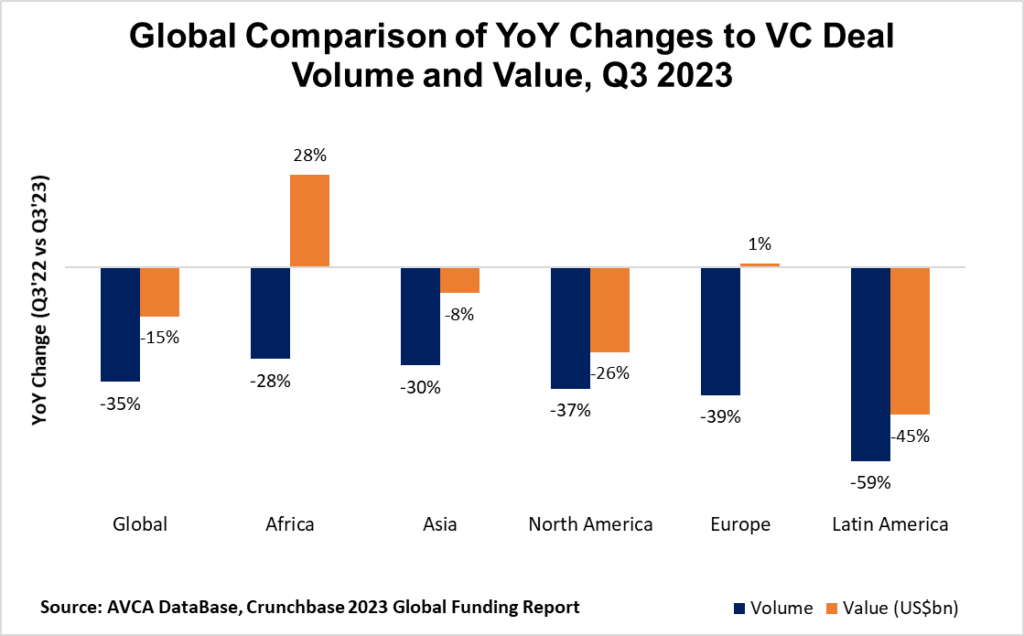

Although African startups staged an impressive comeback in Q3 2023, with funding jumping by 28% compared to the year before.

The general slowdown prompted a reshuffle, with investor focus shifting towards nurturing young startups in their early stages or mature players nearing unicorn status.

Most likely Africa’s VC funding figures fell far from 2022 levels. The final tally as of Q3 2023 to date, per AVCA, stood at $2.95bn – down from the $4.3bn that was raised by the same point last year.

That means Africa’s venture capital industry managed to attract two-thirds (69%) of the capital it accrued by September 2022, and a more disappointing 56% of the total funding last year.

While VC funding is harder to come by, Development Finance Institutions (DFIs)—such as the IFC, BII, US DFC, and Proparco—are becoming more active in the tech startup landscape.

Venture debt & hybrid rounds become more frequent

2023’s funding scorecards are yet to roll out but available estimates suggest the continent’s startups still managed to attract more than $5bn.

Compared to previous years, a higher portion of the total funding is likely to be in the form of venture debt, which has become an alternative source of capital for African startups.

Notable in startup fundraising announcements this year is the growing frequency of mixed equity and debt funding rounds.

Examples include:

Okra Solar’s Series A round ($7.85m equity and $4.15m debt);

Complete Farmer’s pre-Series A funding round ($7m equity and $3.4m debt)

Wetility’s $50m fundraising included a $33m commercial debt package from a consortium of commercial and development banks

While venture debt shines as a catalyst for early-stage ventures, providing crucial working capital to fuel their growth, it’s also increasingly powering expansion for more established startups.

This is the case with:

Mobility FinTech startup Moove Africa. It has raised $325m to date ($150m in equity and over $175m in debt)

Kenyan solar home system provider d.Light’s $125m securitization facility. The company’s total securitized financing is $490m since 2020

An uptick in startup shutdowns, pivots & downsizing

With global macro headwinds seeing investors cut fewer checks and some reportedly renege on commitments, a slew of startups were forced to downsize, pivot, or in many cases, close up shop.

At least 15 African startups shuttered this year, including those with once highly-celebrated status on the continent: 54 Gene, Dash, Sendy, WhereIsMyTransport, Lazerpay, Zumi, Zazuu, Hytch, Okada Books, Pivo, Vibra, Redbird, Bundle Africa, Spire, Qefira.

Combined, these startups raised over $200m in disclosed VC funding while operational.

Meanwhile, others like Copia, MarketForce, and Twiga Foods have had to change the way they operate.

It’s noteworthy that the funding slowdown has hit a certain type of African startups hardest—well-funded ventures chasing growth-at-all-costs strategies.

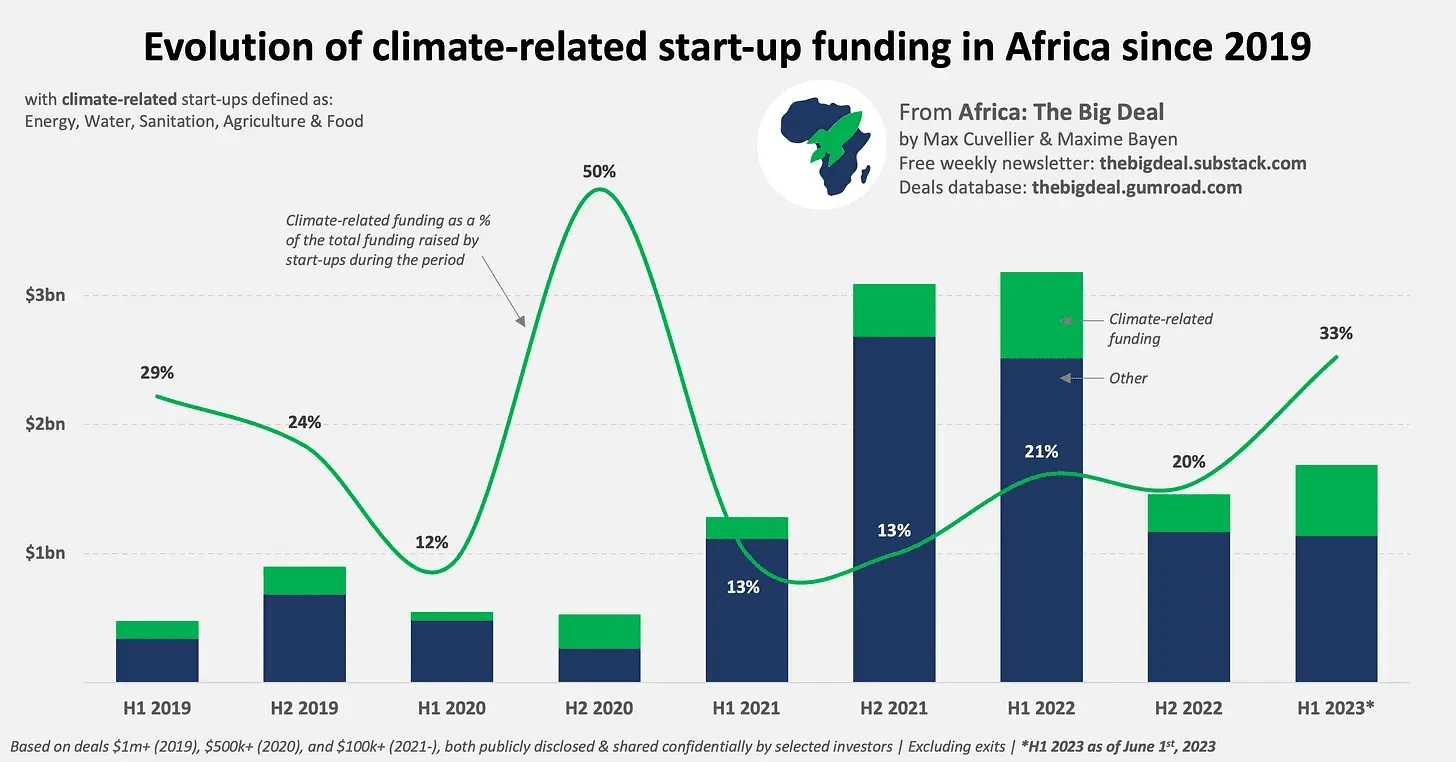

Cleantech/climate-tech now as popular as fintech

The tide is rising for climate tech (comprising innovations across agriculture, clean energy, sustainable materials, environmental sustainability, e-mobility, and nature-based solutions) in Africa.

Last year, funding to the sector grew 3.5 times to over $860m, making it Africa’s most funded after fintech.

It has maintained the second spot so far this year, per AVCA report. Data from Africa: The Big Deal shows the sector accounts for 32% of total VC funding as of Q3, behind fintech’s 35%.

And over the past 12-18 months, several VC firms—among them Satgana, Catalyst Fund, Equator, and EchoVC—have introduced funds to support startups in the sector.

The timing of this surge in climate funding couldn’t be better as Africa grapples with the increasingly severe impacts of climate change, we write in our Pulse54 newsletter, which explores climate tech in general and active players in the sector.

Spotlight on fraud & founder misconduct

Amidst the remarkable growth of Africa’s tech ecosystem, shadows loom over malpractices that impede the full potential and integrity of the continent’s startup landscape.

In 2023 alone, numerous unsettling reports emerged, depicting common themes such as financial misappropriation, deficient or corporate malfeasance, instances of sexual harassment, and the prevalence of toxic work cultures.

Startups like Ghana’s Dash and Float, Egypt’s Capiter, South Africa’s Springleap, and Nigeria-based companies such as PayDay, 54Gene, and Patricia were implicated.

More recently, Tingo was charged by the US SEC, accused of engaging in a “massive fraud” involving “billions of dollars of fictitious transactions,” all under the leadership of CEO Dozy Mmobuosi.

The lessons drawn from the challenges of 2023 underscore the critical need for regulatory clarity to eliminate grey areas in compliance.

Furthermore, investors must prioritize ensuring proper governance to safeguard the integrity of the African startup ecosystem.

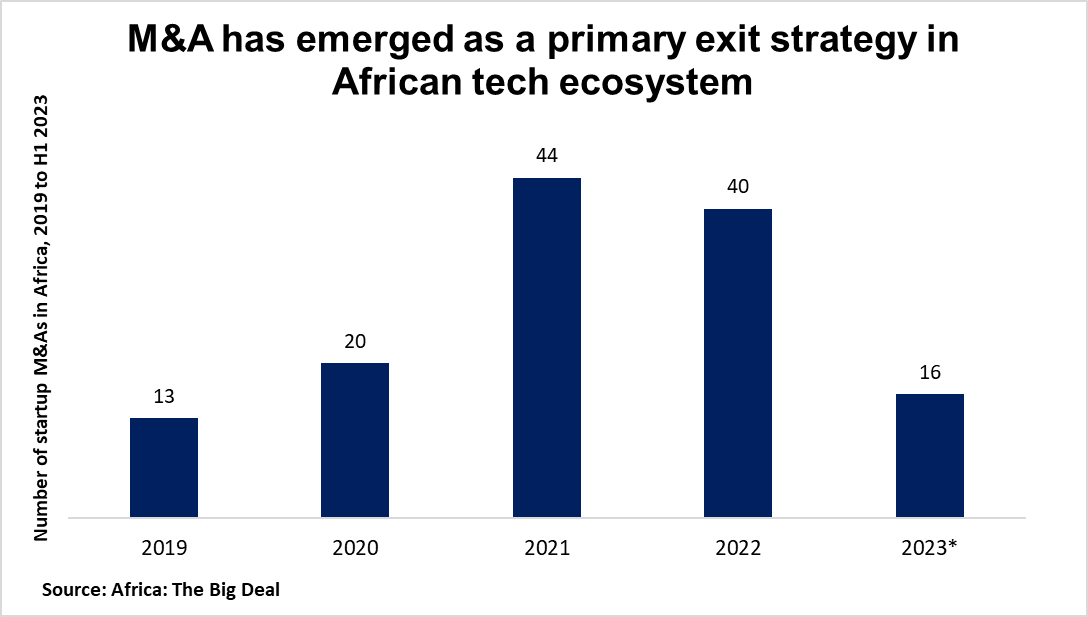

Mergers & acquisitions become a survival strategy

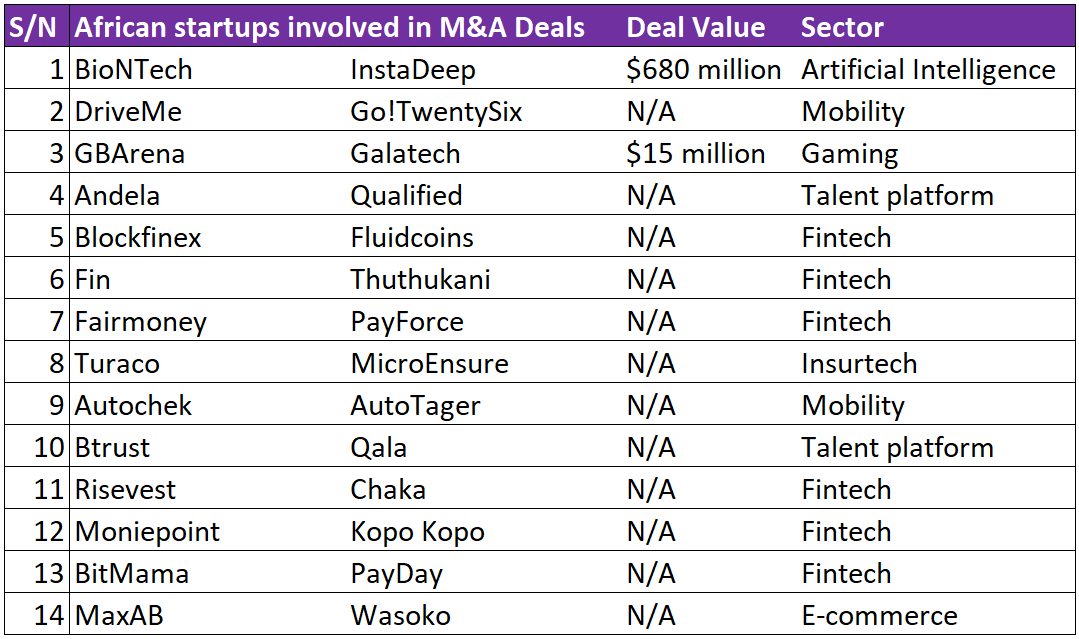

Mergers and acquisitions (M&A) have emerged as a primary exit strategy and, in the current depressed funding environment, a lifeline for African startup founders.

In Q1 2023 alone, seven M&A deals took place in the African startup ecosystem worth over $710m. Tunisia-based InstaDeep’s $682m acquisition in January by Germany’s BioNTech accounted for much of that.

By the end of the year’s first half, there had been at least 16 M&A deals per Big Deal data. About half of them reportedly involve struggling startups.

While this year’s total is likely to be some way off 2022’s 44 deals, one fact remains true: M&As have become a prominent feature of the African tech ecosystem.

Limited funds and the fragmented nature of the African tech market are major drivers.

The presence of numerous small and medium-sized companies across various regions and sectors makes consolidation through M&As a strategic move.

This approach creates larger, more diversified startups that can better compete globally and attract investment.

In addition, African startups are currently viewed as less liquid assets compared to other markets, primarily due to limited exit opportunities.

Thus, as the quest for a reliable path to liquidity in the African tech ecosystem grows, M&As become a viable option for venture capitalists and investors to explore.

Other noteworthy moments and highlights of the year

Starlink, a satellite internet service of Elon Musk-owned SpaceX, became operational in 6 African countries

And digital infrastructure, especially data centers, continues to draw the attention and backing of investors—from telco giants to private equity firms.

Closing Notes

As 2023 hurtles to a close, the question on everyone’s mind is will 2024 be better?

Perceptions of industry performance and expectations for the future vary.

Flagging. That’s how we would describe the African tech startup funding scene in 2023.

Global macro headwinds saw investors cut fewer checks and some reportedly backed down from commitments, forcing a slew of startup shutdowns and downsizing.

While on the surface, it seems Africa’s VC funding figures fell far from 2021 and 2022 levels, available estimates suggest the continent’s startups still managed to attract more than $5 billion.

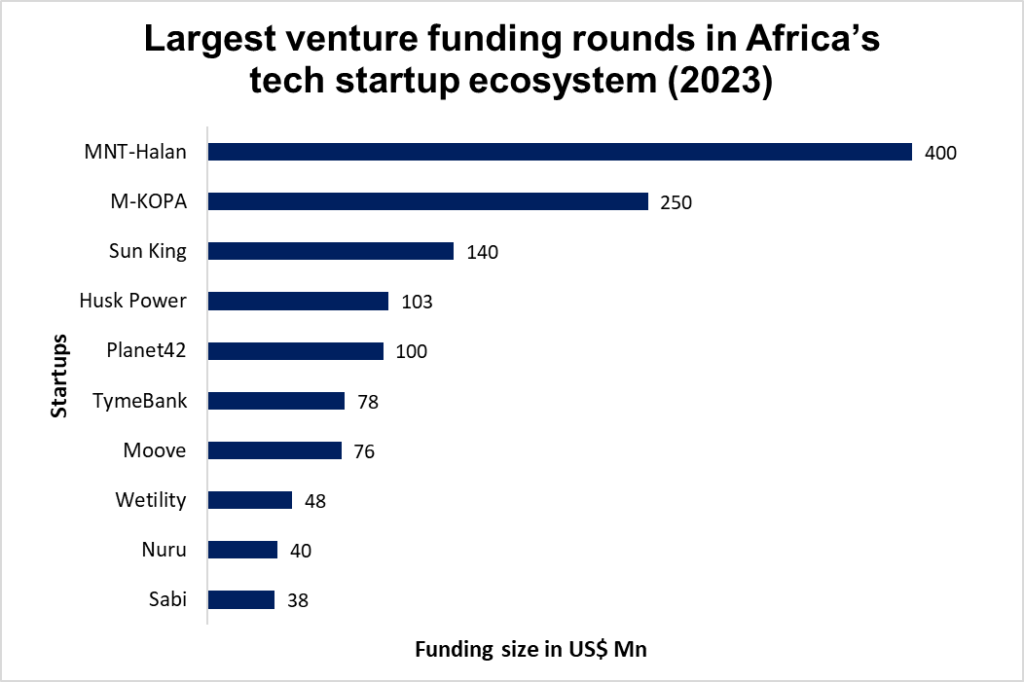

Before the year’s scorecards start to roll out, we take a look at the top 10 largest fundraising rounds in the African tech startup industry this year and the trends they reveal.

Fewer mega-deals (just four >$100m rounds vs nine in 2022):

This signifies a shift towards cautious optimism from investors.

While big bets still happen, they’re rarer, with investors preferring to spread their bets on multiple promising startups.

This could lead to a more sustainable ecosystem, with startups forced to focus on stronger fundamentals and traction before securing large funding rounds.

MNT-Halan‘s $400 million round in Egypt and M-KOPA‘s $250 million in Kenya are rare exceptions, highlighting their established market positions and potential for significant impact.

Fintech takes the top spot but the landscape is more diverse:

Fintech remains a dominant sector due to its potential to address financial inclusion challenges in Africa.

However, other sectors like cleantech and mobility are gaining traction, indicating diversification in investor interest.

This diversification can lead to a more balanced and resilient ecosystem, as the success of the startup scene is not solely dependent on one sector.

The presence of Husk Power, Wetility, Nuru, Planet42, and Moove in the top 10 shows the growing importance of these sectors in attracting investor attention.

The rising prominence of debt + equity rounds:

This hybrid approach combines the flexibility of equity with the stability of debt, offering startups a more tailored financing solution.

It can be particularly useful for startups with strong revenue models but limited access to traditional equity funding.

This trend could democratize access to funding for startups, especially in emerging markets, as it caters to startups at different stages of growth and risk profiles.

MNT-Halan, M-KOPA, Planet42, and Moove all used debt + equity rounds, demonstrating the growing popularity of this approach.

Geographical distribution

The top 10 deals primarily focus on South Africa, Kenya, and Nigeria, showcasing the continued dominance of these countries in the African startup scene.

The Democratic Republic of Congo (DRC) emerged as a surprise entry in the top 10 thanks to Nuru‘s sizable Series B round.

Series B dominance

The majority of deals being Series B raises indicates a focus on mature startups with proven traction and scalability, further highlighting likely investor risk aversion.

Overall, the top 10 fundraising rounds paint a picture of a resilient African tech ecosystem adapting to a challenging global environment.

While mega-deals were scarce, the diversity of sectors, financing models, and geographical representation suggests potential for sustainable growth in the long term.

Stay tuned to our blog for a broader piece that explores standout trends in Africa’s tech landscape in 2023 and our high-conviction themes for the new year—to be published soon!

Venmo, Cash App, and Zelle are familiar names in the world of mobile-based digital payments in the West, having revolutionized how money is transferred and received by millions of people.

But did you know that Africa has been ahead of the game with its own mobile money systems since as far back as 2007?!

That’s right.

Today, we take you on a journey of how Africa became the biggest mobile money player in the world.

Where it all began

Once upon a time, not too long ago, accessing financial services was a challenge for many Africans. Unlike in the U.S. or Europe, traditional banking services were often very limited, especially in remote and rural areas.

But then mobile money.

In 2007, Safaricom, a leading mobile network operator in Kenya, launched a mobile money service called M-Pesa. Little did they know that this innovative concept would spark a digital revolution that would sweep across the continent.

M-Pesa, meaning “mobile money” in Swahili, allowed users to save, send, and receive money using just their mobile phones. This groundbreaking innovation proved to be a game-changer, enabling people without bank accounts to participate in the formal financial system.

In 2007, Safaricom, a leading telecommunications company in Kenya, launched a mobile money service called M-Pesa. Image credit: African Markets

The initial idea behind M-Pesa was to create a convenient way for Kenyans to transfer money securely. The service quickly gained popularity, as people in remote areas, where traditional banking services were scarce, embraced it as a means to conduct financial transactions with ease.

In no time, mobile money took root and started to grow, not only in Kenya but also in neighboring countries.

M-Pesa was launched in Tanzania the following year and is now present in at least 10 countries.

So, what made mobile money so popular?

Well, let’s unravel its magic!

Imagine a scenario: a hardworking individual in a rural village wants to send money to their family in the city.

Historically, this would involve a long and costly journey, with the risk of loss or theft. But with a mobile money account, a few taps on a phone screen can instantly transfer funds to their loved ones, efficiently.

One of the key factors that contributed to the rapid adoption of mobile money was its simplicity: all you needed was a basic mobile phone, and suddenly, you had a bank in the palm of your hand.

No more long queues or complicated paperwork. Money transfers could be done with a few simple clicks.

For deposits and withdrawals, mobile money agents, often found in local shops, act as the bridge between the digital and physical worlds, allowing users to convert cash into digital currency and vice versa.

An M-Pesa agent attends to a user. Image credit: HBS Digital Initiative

By 2010, M-Pesa had acquired 10 million active users and by 2016, it served almost 29.5 million active customers through a network of more than 287,400 agents. In the same year, the service processed around 6 billion transactions, peaking in December at 529 transactions every second.

The success of M-Pesa in Kenya sparked a wave of enthusiasm. As word spread about the convenience and reliability of mobile money, its impact began to reverberate throughout the continent.

Impressed by the service, other African countries eagerly jumped on the mobile money revolution, building theirs in M-Pesa’s image.

Over the next few years, the service spread to countries like Uganda, Ghana, Rwanda, and South Africa as mobile network operators and financial institutions started realizing the immense potential of mobile money.

MTN launched its MoMo service in Uganda in March 2009 and in Rwanda in February 2010. Telesom ZAAD in Somaliland in 2009 and Hormuud launched EVC Plus in Somalia in 2011.

By 2011, more than 100 mobile money services were operating in Africa, reaching people who previously had limited access to formal financial services.

Africa continues to lead global adoption

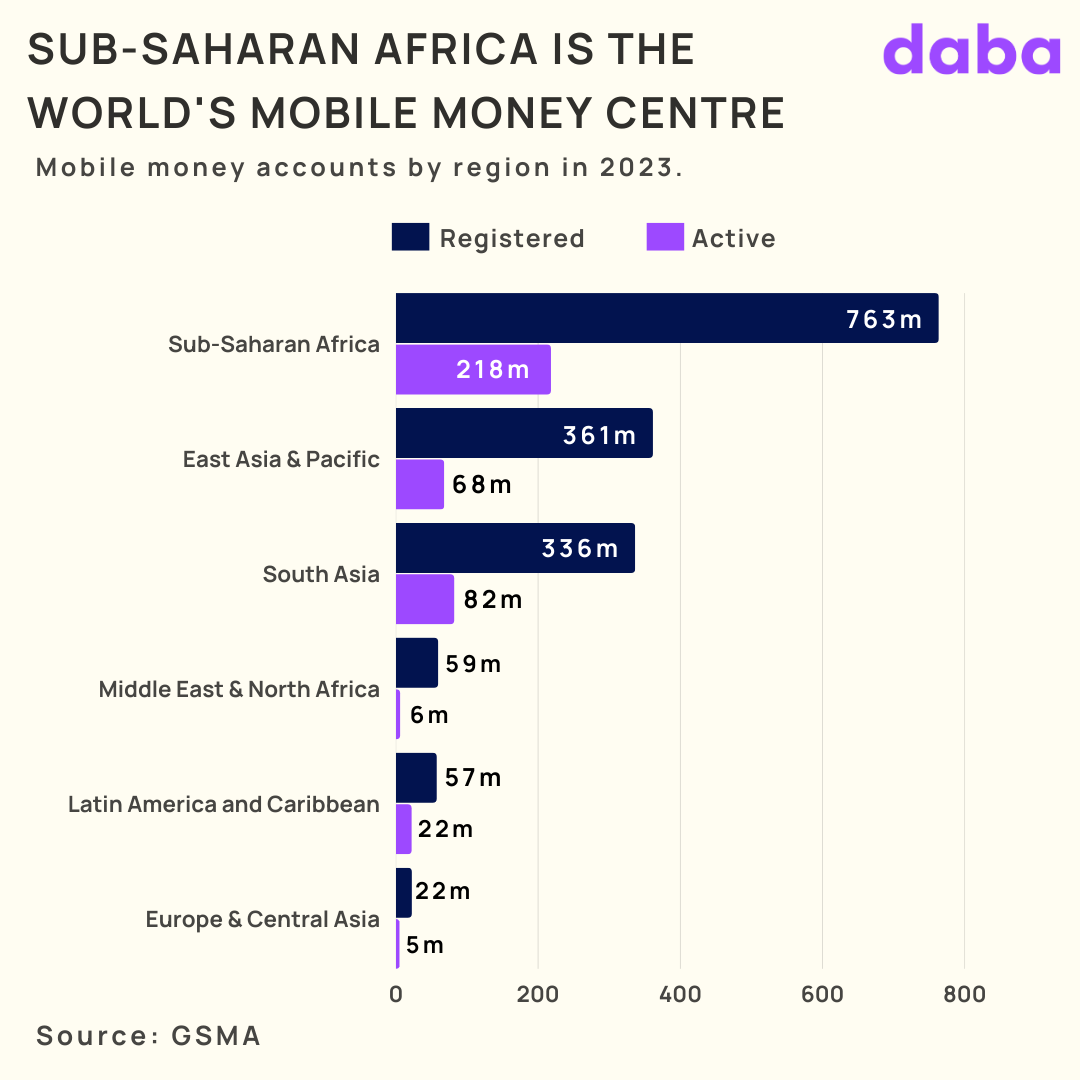

Fast forward to today, more mobile money services have emerged in Africa while mobile money accounts and transaction value on the continent continue to skyrocket.

Africa accounted for up to 70% of the world’s $1 trillion mobile money value in 2021 after mobile money transactions on the continent jumped 39% from $495 billion in 2020 to $701.4 billion.

Last year, that rose a further 22% to a jaw-dropping $836.5 billion (bigger than the GDP of Nigeria, Africa’s largest economy!) but its share of the global $1.26 trillion mobile money value fell to 66.4%.

Per GSMA’s 2023 State of the Industry Report, mobile money is growing faster in sub-Saharan Africa than in other regions except for the Middle East & North Africa.

However, it’s not just about the numbers

Perhaps its greatest achievement, mobile money has brought financial inclusion to millions of Africans who were previously excluded from the formal economy.

Data from the World Bank shows that around 45% of people living in Sub-Saharan don’t have access to a bank account. But mobile phones are widespread across the continent and are helping to bridge the financial gap.

As of 2022, Sub-Saharan Africa had up to 763 million registered mobile money accounts, more than double the figures in the next closest region, and more Africans now enjoy access to a whole range of financial services that were previously out of reach.

The innovative service has empowered women entrepreneurs, allowing them to take charge of their finances and contribute to their families’ well-being; facilitated access to education and healthcare; paved the way for exciting innovations such as mobile banking apps and digital wallets.

Beyond money transfers…

Mobile money services in Africa have also quickly evolved beyond simple person-to-person money transfers and cash in-cash out.

Providers have continually expanded their services, introducing innovative features to meet the diverse needs of their users.

For instance, mobile micro-loans and savings accounts empower individuals to access credit and save money, fostering entrepreneurship.

In Kenya, M-Shwari allows users to save money and access micro-loans directly from their mobile wallets, creating opportunities for entrepreneurs and small business owners.

Partnerships between mobile money providers and other companies have expanded the range of services available, with users now able to pay their electricity and water bills via mobile money and purchase airtime from network operators.

Health organizations have integrated mobile money into their operations, enabling payments for medical services and health insurance premiums.

Despite its transformative effect across the continent so far, it’s clear that the mobile money revolution in Africa is far from over.

Innovations continue to emerge, including interoperability between different mobile money platforms, making transactions even more convenient.

The potential for digital lending, savings, and insurance services on mobile money platforms holds great promise for the future.

As the mobile money landscape continues to evolve, so is the competition. Telecom companies, financial institutions, and fintech startups are all in the race to capture a share of this rapidly expanding market.

This healthy competition will only lead to improved services, lower transaction costs, and increased accessibility for users.

The growth of mobile money in Africa is nothing short of awe-inspiring.

From humble beginnings in Kenya, it has spread like wildfire, empowering individuals, driving economic development, and transforming societies across the continent.

As mobile money continues to evolve and expand its horizons, it remains one shining example of how technology is being harnessed to drive positive change in Africa.

The tide is rising for climate tech in Africa. Fueled by a surge in investor interest, the sector is witnessing a wave of innovation, with over 3,000 startups pitching their solutions for a climate-resilient future.

A new report, “Investing in Climate Tech Innovation in Africa,” by Catalyst Fund, dives into the dynamics of this burgeoning sector, offering invaluable insights for investors, innovators, and stakeholders alike.

If you’re a keen follower of the African tech ecosystem, you must’ve heard of the Paystack, Careem, and Opay Mafia(s) by now.

But have you ever heard of the Jumia Mafia?

For people not familiar with the name, though we hope there’s none, let’s give you a brief introduction to the company.

An e-commerce giant

Jumia started as an online retailer in Nigeria in 2012, co-founded by Jeremy Hodara and Sacha Poignonnec, ex-McKinsey consultants along with Tunde Kehinde and Raphael Kofi Afaedor.

The company has since expanded to at least nine other African countries, where it offers several services, including digital payments and delivery.

In April 2019, the e-commerce operator became the first African startup to list on a major global stock exchange when it debuted on the New York bourse.

One fact about Jumia that’s equally as impressive—as its NYSE IPO or standing as the continent’s largest e-commerce operator—but often overlooked is the impact that the company has had on Africa’s entrepreneurial ecosystem.

Meet the Mafia

Jumia has not only made waves in the African tech industry but also inspired a new generation of entrepreneurs who now run their respective exciting startups.

Some of them include:

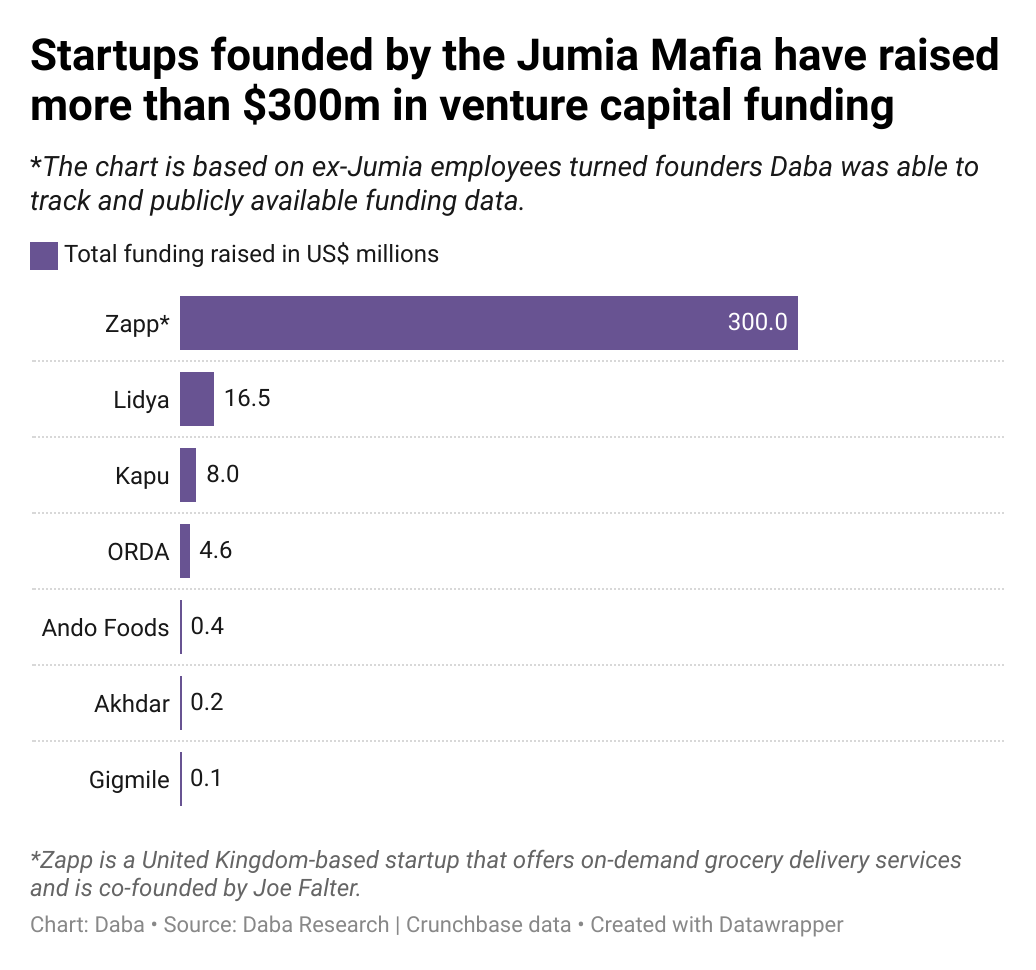

Tunde Kehinde and Ercin Eksin, co-founded Lidya, a Series B startup that provides SMEs with access to finance. The startup uses a credit-scoring system that analyzes a borrower’s online reputation and has raised $16.5 million since its launch.

Raphael Afaedor is another Jumia alumnus who co-founded Kyosk Digital, a platform that connects informal retailers using kiosks and other similar retail outlets directly to FMCG companies.

Maguelone Biau co-founded Twende, a ridesharing company that pools African city dwellers with the most direct, affordable, and reliable transport options.

Kayode Adeyinka is the CEO of Gigmile, a Techstars-backed startup building the services and financial infrastructure for the African gig economy.

Guy Futi runs ORDA, a startup he co-founded that offers cloud-based restaurant software built for African chefs and food business owners, as CEO.

Sam Chappatte’s Kapu is a new e-commerce platform that aims to “reduce the cost of living” in Africa. By sourcing directly from farms & manufacturers, creating a low-cost logistics model & minimal food waste, Kapu says it can sustainably pass on savings to its customers. These customers access even lower prices if they place the order as a group (“pamoja”).

Roger Xavier Macia, a former Chief Commercial Officer at Jumia Senegal, is now the co-founder of Lengo, a startup that combines AI technologies and retailer crowdsourcing to deliver real-time data on consumer goods for FMCGs in Africa.

Marie-Reine Seshie, Jumia’s former Head of Marketing in Ghana, is now the CEO and co-founder of Kola Market. The startup provides digital inventory management, marketing, and sales solutions to SMEs, powered by AI technology.

Omolola Oladunjoye, ex-Chief Commercial Officer at Jumia Nigeria, now runs Penda LLC – a fully integrated social commerce platform across Africa.

Joe Falter, a former executive at Jumia in the UAE for nearly eight years, co-founded Zapp, a startup that provides on-demand grocery delivery services, has raised around $300m, and is backed by some of the world’s leading venture investors.

These are just some of the incredible startups that have been created by former Jumia employees.

Jumia is one of Africa’s earliest tech companies and ranks among the region’s biggest startup success stories.

So it comes as little surprise that former employees and founders have gone on to create their own incredible technology companies, disrupting various industries across the continent.

By sector classification, well over half, or 70% of startups founded by Jumia alumni are either in retail, e-commerce, foodtech, or fintech.

This suggests that Jumia’s early success as an e-commerce giant has created a positive spillover effect, as former employees leverage their experience and networks to create new businesses in related industries such as retail, last-mile delivery & logistics, and digital payments – all crucial components of e-commerce.

Naturally, working in a particular industry provides individuals with valuable insights into the workings of that industry and complementary ones.

Hence, ex-Jumia employees are well-positioned to leverage their expertise and create innovative solutions to meet the needs of consumers in these industries.

And they’re doing so, successfully and with sufficient VC backing.

Collectively, about 14 of such startups we tracked have raised around $330 million in venture capital funding, with over half of them at the seed stage or above.

This shows the talent and expertise that exists within the Jumia ecosystem, which has helped to create a vibrant startup culture out of emerging markets where it operates.

The funding also signals the emergence of a new generation of innovators who are able to attract significant investment and build successful businesses—a positive development for the tech industry.

In addition, it reflects how the African startup ecosystem is becoming increasingly mature and sophisticated, with successful companies spawning new ventures and nurturing the next generation of entrepreneurs.

Altogether, these startups have created around 1,300 direct jobs.

Jumia has served as a springboard for talented individuals who are contributing to the growth of not only Africa’s startup ecosystem but also globally, even after leaving the company.

It’s impressive to see how the e-commerce giant’s success has paved the way for some of Africa’s most brilliant ‘techpreneurs’.

Truly, great companies have the power to inspire incredible founders and fuel the growth of an entire entrepreneurial ecosystem!

By doing so, they help to build a stronger economy and a better future for all.

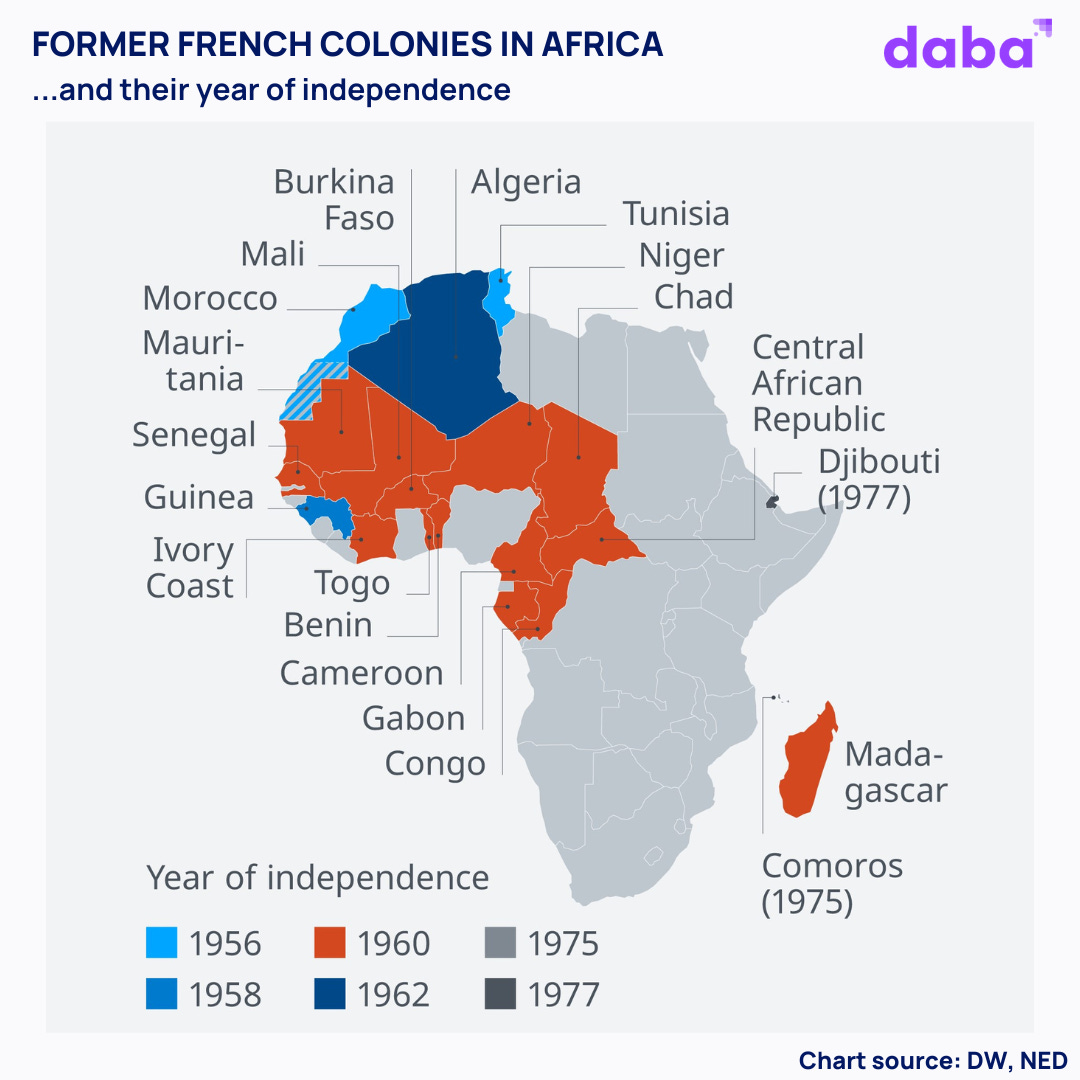

De Senegal à la Côte d’Ivoire, les avancées passionnantes dans le domaine de la technologie façonnent l’avenir en Afrique francophone.

Saviez-vous que l’Afrique abrite le plus grand nombre de locuteurs français au monde ?

Oui, vous avez bien lu.

La langue française, introduite sur le continent par la colonisation de la France et de la Belgique, est aujourd’hui parlée par environ 167 millions de personnes en Afrique en 2023, ce qui représente 51 % de la population mondiale de locuteurs français.

Cette population est répartie dans 29 pays, soit plus de la moitié des 55 pays d’Afrique, s’étendant du Maghreb en Afrique du Nord aux nations subsahariennes du centre et de l’ouest telles que le Sénégal, la Côte d’Ivoire et le Cameroun.

Jusqu’à 21 de ces pays sont désignés comme des “pays francophones”, où le français est soit la langue officielle, soit couramment parlée.

Et, selon certaines estimations, il y aura 700 millions de locuteurs français d’ici 2050, dont 80 % en Afrique.

Selon certaines estimations, il y aura 700 millions de locuteurs français d’ici 2050, dont 80 % en Afrique.

Pourtant, malgré sa prédominance, la région francophone reste souvent dans l’ombre des discussions concernant l’une des tendances les plus marquantes du continent : la montée de l’innovation technologique et des start-ups.

Pendant la majeure partie de la dernière décennie, une grande partie de l’attention et des investissements ont été orientés vers les start-ups des pays anglophones.

Pour mettre les choses en perspective, l’Afrique francophone attire généralement moins de 20 % des investissements en capital-risque annuels de l’Afrique.

Bien au contraire, la région a produit certaines des start-ups les plus remarquables dans les domaines de la technologie financière et des logiciels en Afrique.

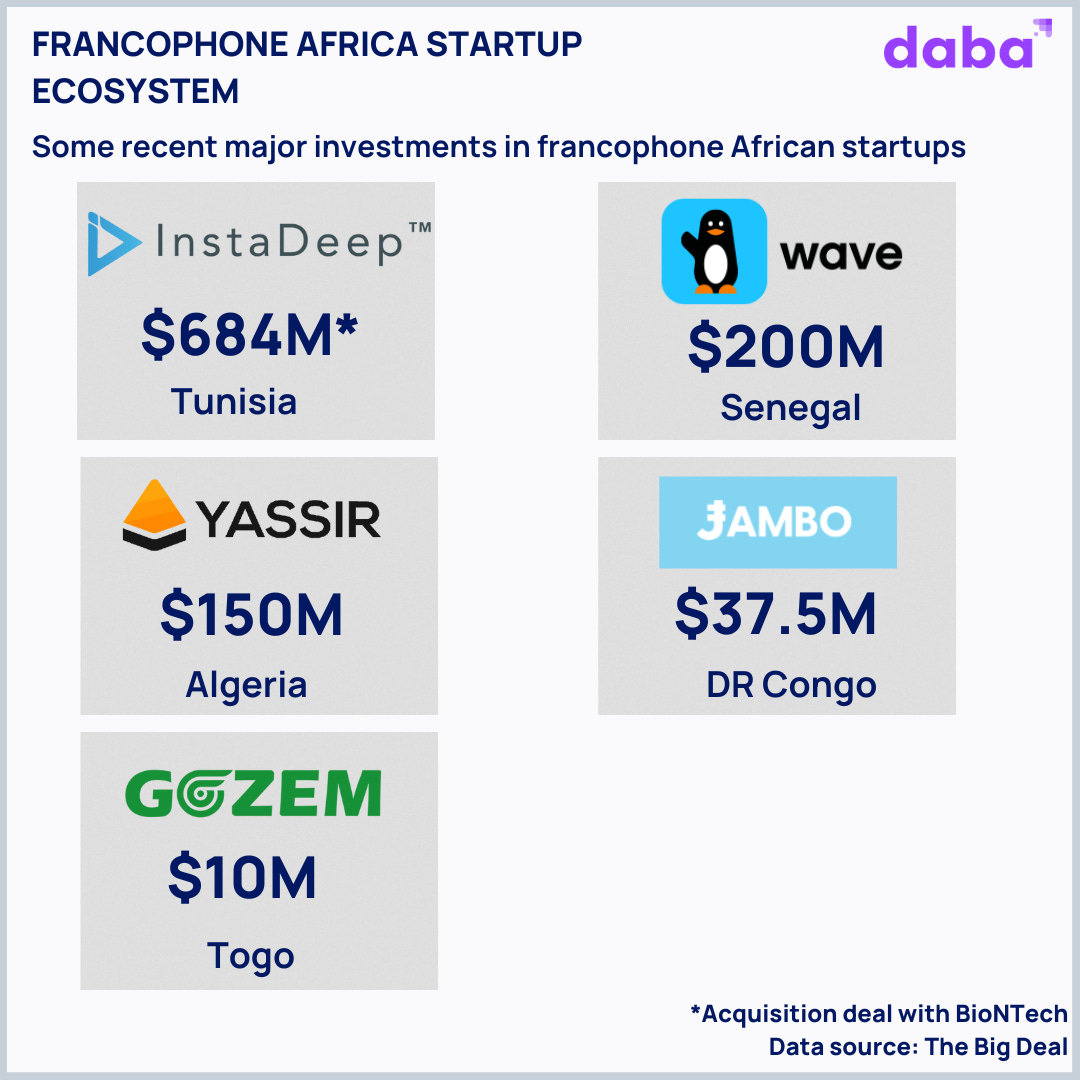

Wave du Sénégal (service de paiement mobile), InstaDeep de la Tunisie (fournisseur de solutions d’intelligence artificielle récemment acquis par BioNTech SE dans le cadre d’une transaction de 684 millions de dollars), Chari du Maroc (une plateforme de commerce électronique pour les petits détaillants), et Yassirde l’Algérie (une super application pour les services à la demande, le transport, la livraison de dernière mile, les services de paiement, etc.) en sont des exemples brillants.

Les barrières linguistiques et les préférences des investisseurs jouent un rôle dans cette disparité.

La plupart des investisseurs en capital-risque actifs en Afrique proviennent des États-Unis et du Royaume-Uni, favorisant les marchés anglophones en raison de leur familiarité.

Pendant ce temps, les investisseurs français sont rares sur la scène des start-ups africaines, ce qui contribue à la répartition inégale des financements.

Une autre raison majeure du retard des financements des start-ups africaines francophones est leur entrée récente sur la scène.

Leur émergence au cours des trois dernières années et leur statut de démarrage entravent les tours de financement plus importants.

En 2021, la fintech sénégalaise Wave a atteint un jalon remarquable en devenant la première start-up du pays à atteindre une valorisation d’un milliard de dollars après avoir levé 200 millions de dollars.

Battre les probabilités : la montée des start-ups francophones

En 2021, la start-up sénégalaise Wave a atteint un jalon remarquable en devenant la première start-up du pays à atteindre une valorisation d’un milliard de dollars après avoir levé 200 millions de dollars.

Elle s’est également distinguée en tant que première licorne en dehors des hubs technologiques traditionnellement dominants tels que le Nigeria, l’Afrique du Sud, l’Égypte et le Kenya, et en tant que pionnière en Afrique francophone.

Le financement dirigé par l’IFC a suscité une attention considérable, suscitant la curiosité concernant les progrès technologiques dans la région plus large.

Depuis lors, les investissements dans les start-ups africaines francophones ont augmenté de manière constante.

Les start-ups africaines ont levé 4,8 milliards de dollars en 2022, le Nigeria étant en tête avec 1,2 milliard de dollars, suivi du Kenya, de l’Égypte et de l’Afrique du Sud.

Cependant, les données d’Africa: The Big Deal, une publication qui suit le financement en capital-risque en Afrique, ont révélé un changement de dynamique au-delà des “Big Four”.

Les pays francophones comme l’Algérie, la Tunisie et le Sénégal ont attiré respectivement 151 millions de dollars, 119 millions de dollars et 112 millions de dollars.

La Côte d’Ivoire a levé 34 millions de dollars, et le Togo a atteint pour la première fois la barre des 10 millions de dollars de financement. Le Mali a également connu sa meilleure année avec 6 millions de dollars.

Bien que les investissements en Afrique centrale francophone restent inférieurs à ceux des autres régions, le Tchad, le Cameroun, le Congo et la RDC ont vu augmenter les flux d’investissements, passant de 24 millions de dollars en 2021 à 50 millions de dollars en 2022.

BioNTech a acquis InstaDeep pour 684 millions de dollars.

Quel est l’avenir des “Francophones” en Afrique ?

Plusieurs tendances indiquent un changement dans les perspectives des entreprises technologiques de l’Afrique francophone.

Julaya (Côte d’Ivoire) : fournit aux entreprises africaines des comptes numériques pour effectuer des paiements et des transactions de paiement mobile à leurs employés et fournisseurs.

Gozem (Togo) : une super application qui propose une gamme de services, notamment le transport, le commerce électronique et les services financiers, dans plusieurs pays d’Afrique francophone.

Daba (pan-africain) : permet aux gens, principalement en Afrique francophone, d’accéder à une large gamme de produits d’investissement, des actions cotées à la Bourse régionale des valeurs mobilières (BRVM) aux obligations et aux fonds communs de placement, en passant par les entreprises en phase de démarrage, le tout via une application mobile.

Jambo (RDC) : se concentre sur l’introduction de la Web3 sur les marchés africains avec pour mission d’intégrer le prochain milliard d’utilisateurs africains.

Hub2 (Côte d’Ivoire) : une start-up fintech de premier plan en matière d’interopérabilité et d’infrastructure de paiement en Afrique francophone, présente dans 14 pays.

Djamo (Côte d’Ivoire) : propose des solutions de banque numérique pour les personnes exclues financièrement.

Auto24 (Côte d’Ivoire) : une entreprise de voitures d’occasion vendues directement aux consommateurs qui offre des solutions novatrices pour garantir des transactions transparentes et sécurisées.

Bizao (Côte d’Ivoire) : numérise les paiements pour les entreprises locales et internationales. Depuis 2019, Bizao a conclu plus de 30 partenariats avec des opérateurs de téléphonie, des banques et des opérateurs de paiement mobile en Afrique.

Oko (Mali) : développe des produits d’assurance récolte basés sur le mobile abordables pour offrir aux petits exploitants agricoles la sécurité financière dont ils ont besoin, quelle que soit l’évolution des conditions climatiques instables. La start-up opère au Mali et en Ouganda et a proposé une assurance à plus de 15 000 agriculteurs.

Paps (Sénégal) : est une entreprise de transport et de logistique alimentée par la technologie qui propose des services de bout en bout pour satisfaire les clients.

Yassir exploite la confiance des utilisateurs pour construire la plus grande super application d’Afrique francophone.

La région offre également un environnement politique plus propice à l’innovation tout en offrant aux start-ups une voie d’expansion régionale relativement aisée en raison de la culture, de la langue, de la réglementation et de la monnaie partagées.

Quatorze pays utilisent le franc CFA, régulé par l’Union économique et monétaire ouest-africaine et la Communauté économique et monétaire de l’Afrique centrale.

La monnaie est arrimée à l’Euro et ne fluctue pas, offrant le type de stabilité des taux de change qui n’est pas disponible ailleurs sur le continent.

Les deux unions représentent 14% de la population totale de l’Afrique et 12% de son PIB.

De plus, la région abrite six des sept économies à la croissance la plus rapide en Afrique subsaharienne, selon le FMI.

Les investisseurs en capital-risque français tels que Saviu, Orange Ventures, Newfund Capital, Proparco, CFAO et AfricInvest soutiennent de plus en plus les start-ups de la région.

Au moins 24 fondateurs de start-up de la région ont levé plus d’un million de dollars en 2022.

Comme de nombreuses start-ups évoluant dans l’espace du commerce électronique B2B sur le continent, Chari numérise le secteur des produits de grande consommation (FMCG) largement fragmenté au Maroc et en Tunisie.

La présence d’un solide système de soutien aux premiers stades de développement sous forme de concours, d’incubateurs, d’accélérateurs, de hubs technologiques et de studios de capital-risque contribue également à la croissance de l’entrepreneuriat dans la région.

Par exemple, Mstudio soutient les entrepreneurs en début de parcours, et en ce qui concerne les concours, l’incubateur technologique Hadina RIMTI organise le Marathon de l’Entrepreneur en Mauritanie.

Pour la formation à l’entrepreneuriat au Mali, des ateliers ont été conçus et menés par les incubateurs locaux CREATEAM et Impact Hub.

Pendant ce temps, Jambar Tech Lab et Traction Camp préparent les entrepreneurs au Sénégal et au Kenya à développer leurs entreprises en partenariat avec des incubateurs sur le terrain, CTIC Dakar & iHub.

De plus, des programmes d’innovation ouverte tels que le hackathon basé au Mali organisé par DoniLab, CREATEAM, Jokkolabs, Teteliso & Impact Hub ont conduit à la conception d’une nouvelle application de mobilité urbaine pour une grande entreprise locale.

Le marché africain francophone, fort de 400 millions de personnes, offre une opportunité distincte alors que son écosystème technologique se développe et que les start-ups attirent davantage l’attention et les investissements régionaux et mondiaux.

Bien que la préparation aux services numériques varie d’un pays à l’autre, les succès récents comme Wave et InstaDeep illustrent le potentiel collectif de la région. Des hubs technologiques au Sénégal aux avancées des fintech en Côte d’Ivoire, les développements technologiques passionnants façonnent l’avenir des entreprises et des services en Afrique francophone autant que dans les régions plus “populaires”.

From Senegal’s hubs to Cote d’Ivoire’s fintech advancements, exciting tech developments are shaping the future in francophone Africa.

Did you know that Africa is home to the largest number of French speakers in the world?

Yes, you read that right.

The French language, brought to the continent through colonialism by France and Belgium, is today spoken by an estimated 167 million people in Africa in 2023, who make up 51% of the global French-speaking population.

This population is spread across 29 countries, more than half of Africa’s 55, extending from the Maghreb in North Africa to sub-Saharan nations in the center and west such as Senegal, Ivory Coast, and Cameroon.

Up to 21 of those countries are known as “francophone countries”, where French is either the official or commonly spoken language.

And, according to some estimates, there will be 700 million French speakers by 2050, 80% of them in Africa.

Yet for all its ubiquity and predominance, the francophone region often remains overshadowed in discussions surrounding one of the continent’s most prominent trends: the surge in technology innovation and startups.

For the better part of the last decade, much of the attention, and investments, have been skewed toward startups in predominantly English-speaking countries.

For context, francophone Africa typically attracts less than 20% of Africa’s annual VC funding.

Far from that, the region has produced some of the most notable fintech and software startups in Africa.

Senegal’s Wave (mobile money service), Tunisia’s InstaDeep(AI solutions provider recently acquired by BioNTech SE in a $684m deal), Morocco’s Chari (an e-commerce platform for small retailers), and Algeria’s Yassir (a super App for on-demand, ride-hailing, last-mile delivery, payment services, and more)are some shining examples.

So why does francophone Africa get sidelined?

Language barriers and investor preferences play a role in this disparity.

Most venture capital investors and firms active in Africa originate from the US and UK, favoring Anglophone markets due to familiarity.

Meanwhile, French investors are scarce in the African startup scene, contributing to the uneven funding distribution.

Another major reason for the lag in francophone African startups’ funding is their recent entry into the scene.

Their emergence in the last three years and early-stage status hinder larger funding rounds.

In 2021, Senegalese fintech Wave achieved a remarkable milestone as the country’s inaugural startup to reach a $1 billion valuation after raising $200 million.

Beating the odds: the rise of francophone startups

In 2021, Senegalese fintech Wave achieved a remarkable milestone as the country’s inaugural startup to reach a $1bn valuation after raising $200m.

Notably, it also stood out as the first unicorn outside of the traditionally dominant tech hubs such as Nigeria, South Africa, Egypt, and Kenya—and the pioneer in French-speaking Africa.

The IFC-led funding received significant attention, sparking curiosity about tech progress in the broader region.

Since then, investment in French-speaking African startups has steadily increased.

African startups raised $4.8bn in 2022, with Nigeria leading with $1.2bn, followed by Kenya, Egypt, and South Africa.

But data from Africa: The Big Deal, a publication that tracks venture funding in Africa, revealed a shift in momentum beyond the “Big Four.”

French-speaking countries like Algeria, Tunisia, and Senegal attracted $151m, $119m, and $112m respectively.

Côte d’Ivoire raised $34m, and Togo reached the $10m funding mark for the first time. Mali also marked its most successful year with $6m.

While investment in central francophone Africa remains lower than in other regions, Chad, Cameroon, Congo, and DRC saw increased investment inflows: from $24m in 2021 to $50m in 2022.

What does the future hold for “the French” in Africa?

Several trends indicate a change in the tech venture fortunes of French-speaking Africa.

For one, the region boasts some of the highest mobile phone adoption rates, which is fueling the rise of even more tech-driven startups. Some of these are:

Julaya (Côte d’Ivoire): provides African businesses with digital accounts to make payments, and disburse mobile money transactions to their employees and suppliers.

Gozem (Togo): a super app that offers a host of services – including transport, e-commerce, and financial services – across several countries in francophone Africa.

Daba (pan-African): enables people, primarily in francophone Africa, access a wide range of investment products, from stocks listed on the regional exchange BRVM, bonds, and mutual funds to early-stage ventures, all through a mobile application.

Jambo (DRC): focused on bringing Web3 to African markets with a mission to onboard the next billion African users.

Hub2 (Côte d’Ivoire): a leading fintech startup in interoperability and payment infrastructure in Francophone Africa, present in 14 countries.

Djamo (Côte d’Ivoire): offers digital banking solutions to people excluded financially.

Auto24 (Côte d’Ivoire): a direct-to-consumer used car company that provides new, innovative solutions to ensure transparent and secure transactions.

Bizao (Côte d’Ivoire): digitizes payments for local and international companies. Since 2019, Bizao has signed over 30 partnerships with telecom operators, banks, and mobile money operators in Africa.

Oko (Mali): develops affordable mobile-based crop insurance products to provide smallholder farmers with the financial security they need, regardless of unstable climate trends. The startup operates in Mali and Uganda and has brought insurance to more than 15,000 farmers.

Paps (Senegal): is a technology-driven transportation and logistics company that offers end-to-end services for customer satisfaction.

BioNTech bought InstaDeep for $684m.

The region also has a more conducive policy environment for innovation while offering startups a relatively easy regional expansion route due to shared culture, language, regulations, and currency.

Fourteen countries use the CFA franc, regulated by the West African Monetary and Economic Union and the Central African Economic and Monetary Community.

The currency is pegged to the Euro and does not fluctuate, providing the kind of foreign exchange stability that’s not available elsewhere on the continent.

Both unions represent 14% of Africa’s total population and 12% of its GDP.

In addition, the region is home to six out of the seven fastest-growing economies in sub-Saharan, per the IMF

French VC investors like Saviu, Orange Ventures, Newfund Capital, Proparco, CFAO, and AfricInvest are also increasingly backing startups in the region.

The presence of a robust early-stage support system in the form of competitions, incubators, accelerators, technological hubs, and venture studios is also contributing to entrepreneurship growth in the region.

Mstudio, for instance, supports early-stage entrepreneurs, and in terms of competitions, tech incubator Hadina RIMTI organizes the Entrepreneur’s Marathon in Mauritania.

For entrepreneurship training in Mali, workshops have been designed and conducted by local incubators CREATEAM and Impact Hub.

Jambar Tech Lab and Traction Camp meanwhile, are getting entrepreneurs in Senegal and Kenya ready to scale their businesses by partnering with incubators on the ground, CTIC Dakar & iHub.

And, open innovation programs like the Mali-based hackathon organized by DoniLab, CREATEAM, Jokkolabs, Teteliso & Impact Hub led to the design of a new urban mobility app for a large local firm.

The 400-million-population-strong francophone African market offers a distinctive opportunity as its tech ecosystem unfolds, and startups attract more attention and capital from regional and global investors.

While readiness for digital services varies across countries, recent successes like Wave and InstaDeep illustrate the region’s collective potential.

From Senegal’s tech hubs to Cote d’Ivoire’s fintech advancements, exciting tech developments are shaping the future of business and services in francophone Africa as much as they are in the more “popular” region.

Dans le paysage commercial dynamique d’aujourd’hui, les startups se sont imposées comme les moteurs de l’innovation, perturbant les industries traditionnelles et façonnant l’avenir.

Ce post vise à démystifier le monde des startups, en éclairant ce qu’elles sont, comment fonctionne l’investissement dans les startups, comment les investisseurs peuvent gagner de l’argent en investissant dans les startups, et le processus de sortie d’un investissement dans une startup.

Qu’est-ce qu’une startup ?

Une startup est une jeune entreprise à ses débuts, généralement fondée par des entrepreneurs avec une idée révolutionnaire ou une solution unique à un problème.

Les startups se caractérisent par leur potentiel de croissance rapide, leur évolutivité et leur vision de perturber ou de créer de nouveaux marchés. Elles opèrent souvent dans des secteurs axés sur la technologie, mais peuvent s’étendre à diverses industries.

Qu’est-ce que l’investissement dans les startups ?

L’investissement dans les startups consiste à fournir un soutien financier à des entreprises en phase de démarrage en échange d’une participation au capital.

Ce processus se déroule généralement lors de différentes phases de financement, où les startups lèvent des capitaux pour stimuler leur croissance. Les investisseurs peuvent participer à ces étapes ou phases de différentes manières, comme l’investissement providentiel, les fonds de capital-risque ou les plateformes de financement participatif.

En règle générale, l’investissement dans les startups se déroule à différentes étapes, notamment le démarrage, la série A, la série B, etc., jusqu’à l’introduction en bourse (IPO) et la sortie, etc., chaque étape représentant une phase distincte de la croissance et du développement d’une startup.

Il est important de noter que toutes les startups ne passent pas par toutes ces étapes, et la chronologie et les besoins de financement peuvent varier considérablement.

Lors de l’investissement dans les startups, la due diligence est cruciale. Les investisseurs analysent en profondeur le modèle commercial de la startup, son potentiel de marché, l’expertise de l’équipe, le paysage concurrentiel et les projections financières.

En menant des recherches approfondies, les investisseurs peuvent identifier les startups prometteuses ayant plus de chances de réussir.

Comment pouvez-vous gagner de l’argent en investissant dans les startups ?

Investir dans les startups offre le potentiel de rendements significatifs, mais comporte également des risques plus élevés par rapport aux voies d’investissement traditionnelles. Voici quelques moyens pour les investisseurs de gagner de l’argent grâce aux investissements dans les startups :

Appréciation du capital : À mesure qu’une startup se développe et atteint des étapes clés, la valeur de ses actions peut augmenter. Les investisseurs qui ont acheté des actions à un stade précoce peuvent bénéficier de l’appréciation du capital lorsque l’entreprise réussit et attire d’autres investissements ou devient publique.

Dividendes ou distribution de bénéfices : Certaines startups peuvent générer des bénéfices à un stade précoce. Dans de tels cas, les investisseurs peuvent recevoir des dividendes ou des distributions de bénéfices, fournissant ainsi un flux de revenus régulier.

Acquisition ou fusion : Les startups dotées de produits ou de technologies convaincants deviennent souvent des cibles d’acquisition attrayantes pour de plus grandes entreprises. Si une startup est acquise ou fusionne avec une autre entreprise, les investisseurs peuvent réaliser un profit de la vente de leurs actions. Par exemple, Instagram, l’application populaire de partage de photos, a été acquise par Facebook en 2012 pour environ 1 milliard de dollars. Cette acquisition a généré des rendements importants pour les investisseurs de première heure.

Introduction en bourse (IPO) : Une autre stratégie de sortie potentielle pour les investisseurs dans les startups est une IPO. Lorsqu’une startup devient publique, les investisseurs peuvent vendre leurs actions sur le marché boursier, réalisant des gains si la valorisation de l’entreprise a augmenté. En 2019, le géant du commerce électronique africain Jumia est entré en bourse, offrant à ses premiers investisseurs la possibilité de sortir et de réaliser des profits.

Marché secondaire : Les investisseurs peuvent vendre leurs actions sur un marché secondaire, où des investisseurs privés achètent et vendent des actions de sociétés non cotées en bourse. Cela permet aux investisseurs de sortir de leurs investissements avant une IPO ou une acquisition. SharesPost et EquityZen sont des exemples de plateformes de marché secondaire qui facilitent l’achat et la vente d’actions de startups.

En conclusion, investir dans les startups peut être une entreprise gratifiante mais risquée. Comprendre la nature des startups, effectuer une due diligence approfondie et diversifier son portefeuille d’investissement sont des étapes essentielles pour réussir dans l’investissement dans les startups.