Investing in an Initial Public Offering (IPO) offers retail investors the chance to get in on the ground floor of a company’s public journey.

For many, IPOs represent an opportunity to buy shares at a lower price before they hit the open market, potentially leading to significant returns as the company grows.

However, understanding how IPOs work and evaluating the risks and rewards are crucial steps before diving in.

Here’s everything you need to know about investing in an IPO.

What Does IPO Mean?

An Initial Public Offering (IPO) occurs when a private company decides to go public by offering shares to the general public for the first time. This process allows a company to raise capital from public investors and provides individuals with the opportunity to buy shares in a company before they are traded on the stock exchange.

IPOs represent a significant milestone for companies, often leading to more capital for expansion, increased visibility, and market credibility. For retail investors, IPOs provide an opportunity to be part of a company’s growth from the outset, potentially reaping substantial rewards as the company grows.

In an IPO, a company collaborates with investment banks to set an initial price for its shares. These shares are offered to institutional and retail investors in what’s called the “primary market.” After this initial sale, the shares begin trading on the stock exchange, where they can be bought and sold in the “secondary market.”

IPOs are generally oversubscribed, meaning that there is more demand for the shares than what is available. This typically causes the price of the stock to rise once it starts trading on the stock market, making IPO investments particularly attractive to early buyers.

The Purpose of an IPO

The primary objective of an IPO is to raise capital. Companies use the funds generated through IPOs to expand operations, invest in new projects, pay off debt, or enhance their market position.

An IPO also provides liquidity to the company’s existing shareholders and founders, allowing them to cash in on their investment.

Moreover, going public increases the company’s transparency and can boost its public profile, making it more appealing to customers, employees, and investors.

Investing in an IPO

Participating in an IPO offers retail investors the chance to buy shares at the initial offering price, which is usually lower than the price after trading begins.

However, it’s essential to note that while IPOs can offer high returns, they also carry risks.

Not every IPO leads to immediate or long-term profits, and some companies may struggle after going public.

Who Can Invest in IPOs?

Traditionally, institutional investors, such as mutual funds and hedge funds, have had first dibs on IPO shares. However, retail investors can also participate, especially with platforms like Daba that make investing in African IPOs more accessible.

With Daba, retail investors can participate in IPOs alongside institutional investors, giving them a chance to invest in the next big growth company from the outset.

If you’re interested in buying an IPO, you can do so through platforms like Daba, which is tailored to African markets. Here’s how you can invest in an IPO using Daba:

Sign up on our platform and verify your account.

Browse available IPOs, such as the recent Orange Côte d’Ivoire and LNB IPOs.

Place your order, specifying the number of shares you wish to buy.

Allocate funds, ensuring you have sufficient capital in your account.

Once the IPO is live, shares are allotted, and if you’re successful, they will appear in your account.

How Is an IPO Priced?

The pricing of an IPO is determined through a process called “book building.” Investment banks work with the company to gauge market demand and set a price range. For example, if a company decides to sell shares for $10 each, and there is substantial demand, the price may be set at the higher end of the range.

In the case of Orange Côte d’Ivoire, shares were initially offered at 10,290 FCFA in January 2023, and as of now, they are trading at 15,300 FCFA. This significant price rise demonstrates the potential of investing in an IPO at the initial offering price, as retail investors could have benefited from the 48% increase in share value.

For investors in the U.S. market, similar IPOs are priced in dollars, often ranging from $10 to $100 per share, depending on the size and financial health of the company.

Is an IPO a Good Investment?

IPOs can be lucrative, but they aren’t guaranteed winners. Some IPOs surge after they hit the market, while others may underperform. Therefore, it’s essential to evaluate each IPO individually. Factors to consider include:

Company Fundamentals: Does the company have a strong business model and consistent revenue growth?

Industry Position: Is the company a leader in its sector, or does it have a competitive edge?

Market Sentiment: Are investors generally optimistic about the company’s future?

In the case of Orange Côte d’Ivoire, the IPO offered retail investors a unique opportunity to invest in a leading telecommunications company in West Africa.

The government of Côte d’Ivoire aimed to promote popular shareholding and help develop the BRVM stock market by making shares accessible to the general public.

Six months after the IPO, investors who bought shares at the debut price had realized a 13% return on their investment.

While the allure of getting in early on a promising company is exciting, it’s crucial to do thorough research. Study the company’s financial health, management team, industry position, and broader economic conditions.

Use platforms like Daba, which provide access to essential research and insights, to make informed decisions. Daba offers news and research on stocks to buy, ensuring investors have the necessary information to assess whether an IPO aligns with their investment goals.

Getting it Right

Investing in an IPO can be a great way to tap into a company’s growth from the start. With platforms like Daba, retail investors have unprecedented access to IPOs across African markets, enabling them to participate in opportunities previously reserved for institutional investors.

While IPOs can offer substantial returns—as demonstrated by the Orange Côte d’Ivoire case study—it’s essential to conduct thorough research and consider the risks before investing.

Venture capital companies work by raising money from various investors, pooling it into a venture fund, and then deploying that capital into startups.

Investing in venture capital (VC) funds has long been a strategy reserved for institutional investors and high-net-worth individuals, but platforms like Daba are democratizing access to these investment opportunities, enabling retail investors to participate in the dynamic world of venture capital.

This article will walk you through the essentials of venture funds and explain why they might be a good fit for your investment portfolio, especially when investing in Africa’s high-growth sectors.

What is a Venture Fund?

A venture fund is a pool of capital collected from investors and used to invest in early-stage companies, particularly startups that show high growth potential. Venture capitalists (VCs) manage these funds and look for innovative companies that can scale quickly and generate significant returns over time.

The key idea is that VC funds provide the necessary capital for startups that are too risky for traditional financing options like bank loans. In return, the fund receives equity in the startup, meaning they own a portion of the company.

What is an Example of Venture Funds?

A real-world example of a successful venture fund is Sequoia Capital, one of the most renowned VC firms globally. Sequoia has invested in companies like Apple, Google, and Airbnb, generating massive returns for their investors.

On the African continent, venture funds like Partech Africa, Launch Africa, Future Africa, and more have been at the forefront, raising substantial amounts to invest in African startups. Funds like these are targeting fast-growing sectors like fintech, climate-tech, healthcare, and logistics, which are vital to Africa’s economic future.

How Do Venture Capital Companies Work?

Venture capital companies work by raising money from various investors, pooling it into a venture fund, and then deploying that capital into startups. Their goal is to help these startups grow into successful businesses.

Once the startups mature, venture capitalists either sell their shares in an Initial Public Offering (IPO) or exit via acquisition, hopefully at a significant profit.

These firms typically take an active role in the companies they invest in, providing guidance, mentorship, and access to networks that can help the startup grow faster.

How Do Venture Funds Raise Money?

Venture funds raise money through limited partners (LPs), who are the investors in the fund. LPs can be institutions like pension funds, endowments, family offices, and even individuals.

The fund managers, also called General Partners (GPs), pitch the investment strategy and fund thesis to these LPs, highlighting the sectors they plan to invest in and the expected returns.

For example, a venture fund like Daba’s VC arm would raise capital by focusing on high-growth industries across Africa, such as fintech, agritech, and logistics.

How Do Venture Funds Make Money?

Venture funds make money through a combination of capital appreciation and management fees.

The primary way is by selling their equity in startups when they either go public or are acquired by larger companies. If a VC fund invested $1 million in a startup and exited the investment for $10 million, that’s a 10x return.

Additionally, venture funds charge management fees, typically around 2% of the total capital they manage, and a “carry” or profit share, often 20% of the profits earned by the fund.

Who Owns a Venture Fund?

Venture funds are owned by the General Partners who manage the fund. The limited partners (investors) own the rights to the returns generated by the fund, but they do not have control over how the fund is managed. GPs make all investment decisions, from which startups to back to when to exit an investment.

Where Do Venture Funds Get Their Money?

Venture funds get their money primarily from LPs, as mentioned earlier. These LPs can include institutional investors, high-net-worth individuals, or, increasingly, retail investors.

Through platforms like Daba, even retail investors can now gain exposure to VC funds, making it easier for everyday investors to benefit from the high returns associated with venture capital.

Who Can Invest in a Venture Fund?

Traditionally, investing in venture capital was restricted to accredited investors—individuals with a high net worth or large institutions.

However, platforms like Daba are changing this by allowing retail investors to invest in VC funds targeting high-growth African startups. This creates an accessible way for individuals to diversify their portfolios with high-risk, high-reward investments.

How to Invest in VC Funds via Daba?

Investing in VC funds through Daba is simple and efficient. Daba provides a platform where retail investors can pool their funds together to invest in curated venture funds focused on African startups.

This allows you to invest in high-growth industries that have the potential to deliver high returns, without needing the substantial capital that traditional VC investments require.

To get started, create an account on Daba, browse the available VC funds, and select the fund that aligns with your investment goals. Daba’s user-friendly platform enables you to track your investment and provides regular updates on the performance of the startups in the portfolio.

Are Venture Funds Good or Bad Investments?

Venture capital is a high-risk, high-reward investment. While it can offer returns that far outpace traditional asset classes like stocks or bonds, it also carries a higher level of risk.

Startups are inherently risky; many fail, but the ones that succeed can deliver astronomical returns.

For example, early investors in Flutterwave, a Nigerian fintech unicorn, have seen significant returns as the company rapidly scaled across Africa and beyond. However, not every investment will be a Flutterwave, so diversification is key.

Investing through platforms like Daba allows you to spread your investment across multiple startups, minimizing risk and maximizing your chances of hitting that next unicorn.

Do Your Homework Before You Invest

Before diving into venture funds, it’s essential to do your homework. Research the fund’s track record, the sectors it focuses on, and the startups in its portfolio. Daba provides transparency and access to research tools, helping you make informed investment decisions.

In conclusion, venture funds offer retail investors the chance to access high-growth opportunities, especially in emerging markets like Africa.

By investing through Daba, you can tap into these opportunities and diversify your portfolio with innovative, high-potential startups. While the risk is higher than traditional investments, the potential rewards can make it a worthy addition to your investment strategy.

Que vous débutiez votre parcours d’investissement ou que vous cherchiez à diversifier votre portefeuille, comprendre les stratégies ETF peut vous aider à prendre des décisions éclairées.

Les fonds négociés en bourse (ETF) ont révolutionné l’investissement, rendant l’accès au marché plus facile que jamais pour les débutants.

Que vous débutiez votre parcours d’investissement ou que vous cherchiez à diversifier votre portefeuille, comprendre les stratégies ETF peut vous aider à prendre des décisions éclairées.

Découvrons dix stratégies ETF particulièrement utiles pour les débutants, en nous concentrant sur le marché ouest-africain et comment les Collections Daba peuvent simplifier votre processus d’investissement.

1. Achat et Conservation

La stratégie la plus simple est souvent la plus efficace. L’investissement à long terme consiste à acheter des ETF et à les conserver pendant une longue période, généralement 10 ans ou plus. Cette approche profite de la tendance générale à la hausse du marché sur le long terme.

Par exemple, vous pouvez investir dans une Collection Daba qui reflète l’indice BRVM Prestige, qui inclut des entreprises ouest-africaines performantes telles qu’Oragroup (ORGT) et Sonatel (SNTS).

En conservant cette collection à long terme, vous pouvez potentiellement bénéficier de la croissance de ces leaders du secteur sans avoir besoin de négocier fréquemment.

L’investissement programmé consiste à investir un montant fixe régulièrement, indépendamment des conditions du marché. Cette approche peut aider à réduire l’impact de la volatilité du marché sur vos investissements.

Avec les Collections Daba, vous pourriez mettre en place un investissement récurrent dans la Collection BRVM Industriel, qui comprend des entreprises comme Nestlé (NTLC) et Air Liquide (SIVC).

En investissant de manière constante, vous achetez plus d’actions lorsque les prix sont bas et moins lorsque les prix sont élevés, réduisant ainsi potentiellement votre coût moyen par action au fil du temps.

3. Allocation d’Actifs

L’allocation d’actifs consiste à diviser vos investissements entre différentes classes d’actifs pour équilibrer les risques et les rendements. Les ETF facilitent cela en offrant une exposition large au marché avec un seul investissement.

Avec les Collections Daba, vous pourriez répartir vos investissements dans différents secteurs de l’économie ouest-africaine.

Par exemple, vous pourriez investir 40% dans la Collection BRVM Industriel, 30% dans la Collection BRVM Agriculture et 30% dans la Collection BRVM Infrastructure. Cette diversification peut protéger votre portefeuille contre la volatilité d’un seul secteur.

4. Rotation Sectorielle

Les investisseurs plus avancés peuvent utiliser la rotation sectorielle, qui consiste à déplacer les investissements entre différents secteurs en fonction des cycles économiques. Bien que cela nécessite une gestion plus active, les Collections Daba simplifient cette approche en regroupant les actions par secteur.

Par exemple, en période de croissance économique, vous pourriez augmenter vos investissements dans la Collection BRVM Industriel.

En période d’incertitude économique, vous pourriez vous tourner vers des secteurs plus défensifs comme la Collection BRVM Distribution, qui comprend des entreprises qui performent bien même en période difficile.

5. Investissement en Dividendes

Pour les investisseurs cherchant un revenu régulier, l’investissement en dividendes peut être une stratégie attrayante. De nombreux ETF se concentrent sur les actions à dividendes élevés, offrant un flux de revenus stable.

Bien que les Collections Daba ne soient pas spécifiquement conçues comme des ETF à dividendes, la Collection BRVM Prestige inclut de nombreuses entreprises établies qui versent souvent des dividendes. En investissant dans cette collection, vous pourriez bénéficier à la fois de l’appréciation du capital et des revenus de dividendes.

6. Investissement Thématique

L’investissement thématique consiste à se concentrer sur des tendances ou des thèmes spécifiques qui, selon vous, façonneront l’avenir. Les Collections Daba offrent plusieurs options thématiques alignées sur les secteurs clés de l’économie ouest-africaine.

Par exemple, si vous croyez au potentiel de croissance de l’agriculture dans la région, vous pourriez investir dans la Collection BRVM Agriculture, qui inclut des entreprises comme Palm (PALC) et SAPH (SPHC).

7. Couverture (Hedging)

La couverture est une stratégie utilisée pour compenser les pertes potentielles d’un investissement en prenant une position opposée dans un autre. Bien que plus complexe, même les débutants peuvent utiliser des stratégies de couverture simples avec des ETF.

Si vous êtes fortement investi dans la Collection BRVM Industriel mais craignez un ralentissement économique, vous pourriez vous couvrir en investissant également dans la Collection BRVM Distribution, qui comprend des entreprises plus résilientes en période de défis économiques.

8. Stratégie Noyau-Satellite

L’approche noyau-satellite consiste à construire un portefeuille avec un noyau stable d’ETF de marché large, complété par des positions satellites dans des ETF plus spécifiques ou spécialisés.

Avec les Collections Daba, vous pourriez utiliser la Collection BRVM Prestige comme votre position de base, représentant les entreprises les plus performantes dans plusieurs secteurs.

Ensuite, ajoutez des positions satellites dans des collections plus spécialisées comme BRVM Agriculture ou BRVM Infrastructure en fonction de vos intérêts spécifiques ou des perspectives du marché.

9. Rééquilibrage

Le rééquilibrage est le processus consistant à réaligner votre portefeuille pour maintenir l’allocation d’actifs souhaitée. Au fil du temps, les performances des investissements diffèrent, et votre portefeuille peut s’écarter de son allocation initiale. Le rééquilibrage régulier aide à gérer les risques.

Avec les Collections Daba, vous pouvez programmer un examen de vos avoirs dans les différentes collections et ajuster si nécessaire pour maintenir l’équilibre désiré entre les secteurs.

10. Sortie Programmé (Dollar-Cost Averaging Out)

Tout comme l’investissement programmé peut être utilisé lors de l’achat, il peut également être utilisé lors de la vente. Cette stratégie, parfois appelée sortie programmée, consiste à vendre un montant fixe de vos investissements à intervalles réguliers.

Cela peut être particulièrement utile lorsque vous approchez d’un objectif financier et souhaitez réduire progressivement votre exposition au marché. Par exemple, si vous avez investi dans la Collection BRVM Industriel pendant des années et approchez de la retraite, vous pourriez commencer à vendre systématiquement de petites portions de vos avoirs au fil du temps.

Les Collections Daba simplifient ces stratégies en offrant des groupes d’actions pré-curés basés sur les indices sectoriels de la BRVM. Cette approche permet aux débutants de mettre en œuvre facilement des stratégies d’investissement sophistiquées sans avoir besoin de recherches approfondies ou d’une expertise en sélection de titres.

N’oubliez pas que ces stratégies peuvent être des outils puissants pour la construction et la gestion de votre portefeuille d’investissements, mais il est important de prendre en compte vos objectifs financiers personnels, votre tolérance au risque et votre horizon d’investissement. Aucune stratégie unique ne convient à tout le monde, et la meilleure approche implique souvent une combinaison de stratégies adaptées à vos besoins individuels.

Whether you’re just starting your investment journey or looking to expand your portfolio, understanding ETF strategies can help you make informed decisions.

Exchange-traded funds (ETFs) have revolutionized investing, making it easier than ever for beginners to enter the market.

Whether you’re just starting your investment journey or looking to expand your portfolio, understanding ETF strategies can help you make informed decisions.

Let’s explore ten ETF strategies that are particularly useful for beginners, with a focus on the West African market and how Daba Collections can simplify your investment process.

1. Buy and Hold

The simplest strategy is often the most effective. Buy-and-hold investing involves purchasing ETFs and holding them for the long term, typically 10 years or more. This approach takes advantage of the market’s general upward trend over time.

For example, you could invest in a Daba Collection that mirrors the BRVM Prestige index, which includes top-performing West African companies like Oragroup (ORGT) and Sonatel (SNTS).

By holding this collection for the long term, you can potentially benefit from the growth of these industry leaders without the need for frequent trading.

2. Dollar-Cost Averaging

Dollar-cost averaging is a strategy where you invest a fixed amount regularly, regardless of market conditions. This approach can help reduce the impact of market volatility on your investments.

With Daba Collections, you could set up a recurring investment in the BRVM Industrial Collection, which includes companies like Nestlé (NTLC) and Air Liquide (SIVC).

By consistently investing, you’ll buy more shares when prices are low and fewer when prices are high, potentially lowering your average cost per share over time.

3. Asset Allocation

Asset allocation involves dividing your investments across different asset classes to balance risk and reward. ETFs make this easy by offering broad market exposure in a single investment.

Using Daba Collections, you could allocate your investments across different sectors of the West African economy.

For instance, you might invest 40% in the BRVM Industrial Collection, 30% in the BRVM Agriculture Collection, and 30% in the BRVM Infrastructure Collection. This diversification can help protect your portfolio from the volatility of any single sector.

4. Sector Rotation

More advanced investors might use sector rotation, moving investments between different sectors based on economic cycles. While this requires more active management, Daba Collections makes it easier by grouping stocks into sector-based collections.

For example, during an economic boom, you might shift more of your investment into the BRVM Industrial Collection.

During times of economic uncertainty, you might rotate into more defensive sectors like the BRVM Distribution Collection, which includes companies that tend to perform well even in challenging economic conditions.

5. Dividend Investing

For investors seeking regular income, dividend investing can be an attractive strategy. Many ETFs focus on high-dividend stocks, providing a steady stream of income.

While Daba Collections aren’t specifically designed as dividend ETFs, the BRVM Prestige Collection includes many established companies that often pay dividends. By investing in this collection, you could potentially benefit from both capital appreciation and dividend income.

6. Thematic Investing

Thematic investing involves focusing on specific trends or themes that you believe will shape the future. Daba Collections offers several thematic options aligned with key sectors in the West African economy.

For instance, if you believe in the growth potential of agriculture in the region, you could invest in the BRVM Agriculture Collection, which includes companies like Palm (PALC) and SAPH (SPHC).

7. Hedging

Hedging is a strategy used to offset potential losses in one investment by taking an opposite position in another. While more complex, even beginners can use simple hedging strategies with ETFs.

If you’re heavily invested in the BRVM Industrial Collection but are concerned about potential economic downturns, you might hedge by also investing in the BRVM Distribution Collection, which includes companies that tend to be more resilient during economic challenges.

8. Core-Satellite Strategy

The core-satellite approach involves building a portfolio with a stable “core” of broad-market ETFs, supplemented by “satellite” positions in more specific or specialized ETFs.

With Daba Collections, you could use the BRVM Prestige Collection as your core holding, representing the top-performing companies across sectors.

Then, add satellite positions in more specialized collections like BRVM Agriculture or BRVM Infrastructure based on your specific interests or market outlook.

9. Rebalancing

Rebalancing is the process of realigning your portfolio to maintain your desired asset allocation. As different investments perform differently over time, your portfolio can drift from its original allocation. Regular rebalancing helps manage risk.

With Daba Collections, you could set a schedule to review your holdings across different collections and adjust as needed to maintain your desired balance between sectors.

10. Dollar-Cost Averaging Out

Just as dollar-cost averaging can be used when buying into investments, it can also be used when selling. This strategy sometimes called reverse dollar-cost averaging, involves selling a fixed dollar amount of your investments at regular intervals.

This can be particularly useful when you’re approaching a financial goal and want to gradually reduce your market exposure. For instance, if you’ve been investing in the BRVM Industrial Collection for years and are nearing retirement, you might start systematically selling small portions of your holdings over time.

Daba Collections simplifies these strategies by offering pre-curated groups of stocks based on BRVM sector indexes. This approach allows beginners to easily implement sophisticated investment strategies without the need for extensive research or stock-picking expertise. By using Collections, you can gain exposure to a diverse range of top-performing West African companies across multiple sectors with just a few taps on your phone.

Remember, while these strategies can be powerful tools for building and managing your investment portfolio, it’s important to consider your personal financial goals, risk tolerance, and investment horizon. No single strategy is right for everyone, and the best approach often involves a combination of strategies tailored to your individual needs.

Cette collaboration vise à rendre les opportunités d’investissement en Afrique accessibles aux investisseurs accrédités des États-Unis grâce à la plateforme innovante de Fundr.

Miami et New York, États-Unis – Daba, le principal fournisseur d’infrastructures d’investissement multi-actifs en Afrique, a annoncé aujourd’hui un partenariat stratégique avec Fundr, une plateforme d’investissement en startups basée aux États-Unis. Cette collaboration a pour objectif de rendre les opportunités d’investissement en Afrique accessibles aux investisseurs accrédités des États-Unis grâce à la plateforme innovante de Fundr.

Daba propose une gamme complète de produits d’investissement, notamment une application d’investissement pour les investisseurs individuels, des services institutionnels, ainsi que des API pour les entreprises technologiques souhaitant intégrer des produits d’épargne et d’investissement.

La plateforme de Fundr utilise des données et de l’intelligence artificielle pour optimiser la prise de décision, éliminer les biais et augmenter l’efficacité dans l’investissement en phase d’amorçage. Elle collabore avec des investisseurs de toutes tailles pour analyser les opportunités d’investissement, optimiser leur processus d’investissement et fournir des informations approfondies en temps réel sur leurs portefeuilles.

« Ce partenariat avec Fundr s’aligne parfaitement avec notre mission de démocratiser l’investissement en Afrique », a déclaré Boum III Jr, PDG et co-fondateur de Daba. « En tirant parti du réseau d’investisseurs de Fundr, nous pouvons connecter davantage de capitaux mondiaux aux opportunités passionnantes qui émergent à travers le continent africain. »

Lauren Washington, PDG de Fundr, a commenté : « Nous sommes ravis de nous associer à Daba pour offrir des opportunités d’investissement de haute qualité en Afrique sur notre plateforme. Cette collaboration offre à nos investisseurs un accès unique à l’un des marchés à la croissance la plus rapide au monde, diversifiant ainsi davantage leurs portefeuilles. »

L’écosystème du capital-risque en Afrique a connu une croissance remarquable ces dernières années. Selon les données disponibles, le financement du capital-risque en Afrique a augmenté de 1 597 % entre 2015 et 2023, passant de 277 millions de dollars à 4,7 milliards de dollars. Cette montée en flèche de l’activité d’investissement reflète la scène florissante des startups technologiques sur le continent, stimulée par une population jeune et technophile ainsi que par une pénétration croissante des smartphones.

Le dividende démographique de l’Afrique et sa transformation numérique rapide présentent un cas d’investissement convaincant. Avec plus de 60 % de sa population âgée de moins de 25 ans et un nombre d’utilisateurs d’Internet mobile qui devrait atteindre 475 millions d’ici 2025, le continent est prêt pour une innovation continue et une croissance soutenue. Des secteurs tels que la fintech, le commerce électronique et les technologies propres sont particulièrement attractifs, offrant des solutions aux défis locaux et des opportunités de développement à travers les frontières.

Daba et Fundr s’engagent à assurer un processus d’intégration fluide et à fournir un support complet aux investisseurs intéressés par l’exploration de ces nouvelles opportunités. Au fur et à mesure que le partenariat se développe, les deux entreprises prévoient d’organiser des webinaires et des événements communs pour informer les investisseurs sur le marché africain et présenter des startups prometteuses de tout le continent.

À propos de Daba

Fondée en 2021, Daba est la principale plateforme d’investissement et de financement multi-actifs en Afrique. La société se consacre à libérer tout le potentiel d’investissement du continent en offrant une plateforme unifiée permettant aux particuliers et aux institutions d’accéder à des opportunités d’investissement de haute qualité sur les marchés africains.

À propos de Fundr

Fundr est une plateforme d’investissement en startups basée aux États-Unis qui simplifie le processus d’investissement dans les entreprises en phase de démarrage. Grâce à son algorithme intelligent et à ses processus rationalisés, Fundr offre aux investisseurs une diversification instantanée, un accès à des startups sélectionnées et des outils efficaces de gestion de portefeuille.

This collaboration aims to make African investment opportunities accessible to accredited US investors through Fundr’s innovative platform.

Miami and New York, USA – Daba, Africa’s premier multi-asset investment infrastructure provider, today announced a strategic partnership with Fundr, a leading US-based startup investment platform. This collaboration aims to make African investment opportunities accessible to accredited US investors through Fundr’s innovative platform.

Daba offers a comprehensive suite of investment products, including a real investing app for individual investors, institutional services, and APIs for tech companies to integrate savings and investing products.

Fundr’s platform uses data and AI to empower decision-making, remove bias, and increase efficiency in seed investing. It works with investors of all sizes to analyze investment opportunities, optimize their investment process, and provide real-time deep insights into their portfolios.

“This partnership with Fundr aligns perfectly with our mission to democratize investing in Africa,” said Boum III Jr, CEO & Co-founder of Daba. “By leveraging Fundr’s investor network, we can connect more global capital to the exciting opportunities emerging across the African continent.”

Lauren Washington, CEO of Fundr, commented, “We’re thrilled to partner with Daba to bring high-quality African investment opportunities to our platform. This collaboration offers our investors unique access to one of the world’s fastest-growing markets, further diversifying their portfolios.”

The African venture capital ecosystem has seen remarkable growth in recent years. According to available data, venture capital funding in Africa has seen a remarkable surge in recent years, growing by 1,597% from $277 million in 2015 to $4.7 billion in 2023. This surge in investment activity reflects the continent’s burgeoning tech startup scene, driven by a young, tech-savvy population and increasing smartphone penetration.

Africa’s demographic dividend and rapid digital transformation present a compelling investment case. With over 60% of its population under the age of 25 and mobile internet users expected to reach 475 million by 2025, the continent is poised for continued innovation and growth. Sectors such as fintech, e-commerce, and cleantech are particularly attractive, offering solutions to local challenges and opportunities for scaling across borders.

Daba and Fundr are committed to ensuring a smooth integration process and providing comprehensive support to investors interested in exploring these new opportunities. As the partnership develops, both companies plan to host joint webinars and events to educate investors about the African market and showcase promising startups from across the continent.

About Daba

Established in 2021, Daba is Africa’s leading multi-asset investment and financing platform. The company is dedicated to unlocking the continent’s full investment potential by providing a unified platform for individuals and institutions to access high-quality investment opportunities across African markets.

About Fundr

Fundr is a US-based startup investment platform that simplifies the process of investing in early-stage companies. Through its smart algorithm and streamlined processes, Fundr offers investors instant diversification, access to vetted startups, and efficient portfolio management tools.

Les membres du bloc régional comprennent les huit pays francophones de l’Afrique de l’Ouest et offrent des leçons pour les efforts d’intégration régionale sur le continent.

L’Union Économique et Monétaire Ouest-Africaine, communément connue sous son acronyme français UEMOA ou son acronyme anglais WAEMU (West African Economic and Monetary Union), est une organisation régionale importante en Afrique de l’Ouest.

Cet article fournit un aperçu de l’UEMOA, abordant les aspects clés de sa structure, de ses fonctions et de son impact sur l’intégration régionale.

Combien de pays font partie de l’UEMOA ?

L’UEMOA comprend huit États membres : le Bénin, le Burkina Faso, la Côte d’Ivoire, la Guinée-Bissau, le Mali, le Niger, le Sénégal et le Togo.

L’union a été officiellement établie le 10 janvier 1994, en s’appuyant sur les fondations de l’Union Monétaire Ouest-Africaine (UMOA) créée en 1962. La Guinée-Bissau a rejoint en 1997, portant le groupe initial de sept à huit membres.

Quel est le but et les fonctions de l’UEMOA ?

L’objectif principal de l’UEMOA est de promouvoir l’intégration économique entre ses États membres. Elle vise à créer un espace économique harmonisé et intégré en Afrique de l’Ouest, assurant la libre circulation des personnes, des capitaux, des biens, des services et des facteurs de production.

L’union s’efforce d’améliorer la compétitivité des économies membres dans le cadre d’un marché ouvert et compétitif, tout en simplifiant et harmonisant l’environnement juridique dans la région.

Les fonctions clés de l’UEMOA incluent :

La coordination des politiques économiques et monétaires

La mise en œuvre de politiques sectorielles communes

L’harmonisation de la législation, notamment en matière de fiscalité

La création d’un marché commun

La coordination des politiques macroéconomiques nationales

Quelle est la monnaie de l’UEMOA ?

Les pays de l’UEMOA partagent une monnaie commune, le franc CFA de l’Afrique de l’Ouest (XOF).

Cette monnaie est arrimée à l’euro, un héritage des liens coloniaux de la région avec la France. La Banque Centrale des États de l’Afrique de l’Ouest (BCEAO) gère la politique monétaire pour tous les membres de l’UEMOA.

L’utilisation d’une monnaie commune vise à faciliter le commerce et l’investissement au sein de l’union en éliminant les risques de change et en réduisant les coûts de transaction.

Cependant, cela signifie également que les pays membres ne peuvent pas ajuster indépendamment leurs politiques monétaires pour faire face à des défis économiques spécifiques à leur pays.

Le franc CFA est arrimé à l’euro, un héritage des liens coloniaux de la région avec la France.

Différences entre l’UEMOA et la CEDEAO

Alors que l’UEMOA se concentre sur l’intégration économique et monétaire entre ses huit membres francophones, la Communauté Économique des États de l’Afrique de l’Ouest (CEDEAO) est un groupe régional plus large qui comprend tous les pays de l’UEMOA plus sept autres.

La CEDEAO vise une coopération régionale et une intégration plus larges, au-delà des seules questions économiques.

Les différences clés incluent :

Portée : L’UEMOA se concentre principalement sur l’intégration économique et monétaire, tandis que la CEDEAO a un mandat plus large incluant la coopération politique et la sécurité.

Adhésion : L’UEMOA compte 8 membres, tous utilisant le franc CFA, tandis que la CEDEAO compte 15 membres avec diverses monnaies.

Niveau d’intégration : L’UEMOA a atteint une intégration économique plus profonde, y compris une monnaie commune et des politiques économiques harmonisées, tandis que la CEDEAO travaille encore à atteindre ces objectifs.

L’UEMOA offre plusieurs avantages potentiels à ses États membres :

Stabilité monétaire : La monnaie commune et la politique monétaire partagée visent à assurer la stabilité des prix et des taux d’inflation faibles dans toute la région.

Facilitation du commerce : L’élimination des risques de change et la réduction des coûts de transaction devraient théoriquement promouvoir le commerce intra-régional.

Coordination des politiques économiques : Des politiques économiques harmonisées peuvent conduire à des environnements d’affaires plus stables et prévisibles dans toute la région.

Pouvoir de négociation collectif : En tant que bloc, les pays de l’UEMOA peuvent avoir une position de négociation plus forte dans les affaires économiques internationales.

Développement des infrastructures régionales : L’union peut coordonner et financer des projets d’infrastructure régionaux qui bénéficient à plusieurs États membres.

Un élément important de l’intégration financière de l’UEMOA est la Bourse Régionale des Valeurs Mobilières (BRVM).

Établie en 1998 et ayant son siège à Abidjan, en Côte d’Ivoire, la BRVM est une bourse régionale unique au monde servant les huit pays membres de l’UEMOA. C’est la seule bourse au monde qui dessert plusieurs pays avec une monnaie commune.

La BRVM joue un rôle crucial dans l’écosystème financier de l’UEMOA en offrant une plateforme permettant aux entreprises de lever des capitaux et aux investisseurs d’échanger des titres dans toute la région. Elle propose une variété d’instruments financiers, y compris des actions, des obligations et d’autres titres.

La bourse fonctionne en français, reflétant la langue prédominante de la région de l’UEMOA, et toutes les transactions sont effectuées dans la monnaie commune du franc CFA.

Malgré son potentiel, la BRVM fait face à des défis typiques des marchés frontières, notamment une liquidité limitée et un nombre relativement restreint de sociétés cotées. Cependant, elle représente une étape significative vers l’intégration financière au sein de l’UEMOA et a le potentiel de devenir un outil de plus en plus important pour mobiliser des capitaux pour le développement régional.

À mesure que l’UEMOA poursuit son intégration économique, le rôle de la BRVM dans la facilitation de l’investissement transfrontalier et la fourniture d’une plateforme régionale pour la levée de capitaux est susceptible de croître en importance.

Leçons de l’UEMOA en matière d’intégration régionale

L’expérience de l’UEMOA offre plusieurs leçons importantes pour les efforts d’intégration régionale :

Une union monétaire à elle seule ne suffit pas : Malgré le partage d’une monnaie commune, les pays de l’UEMOA n’ont pas vu l’augmentation attendue du commerce ou de l’investissement intra-régional. Cela suggère que d’autres obstacles, tels que l’infrastructure inadéquate et les procédures douanières complexes, jouent un rôle important dans l’entrave à l’intégration économique régionale.

La diversité économique est importante : Les pays de l’UEMOA ont des structures économiques similaires, souvent en concurrence sur les mêmes marchés d’exportation plutôt que de se compléter. Cela limite le potentiel de commerce intra-régional et de diversification économique.

Les dépendances extérieures persistent : Les liens économiques continus de la région avec la France et l’ancrage à l’euro ont été critiqués pour limiter la souveraineté économique et la flexibilité.

La volonté politique est cruciale : Une intégration réussie nécessite un engagement politique soutenu de la part de tous les États membres pour mettre en œuvre et faire respecter les politiques convenues.

Équilibrer les intérêts nationaux et régionaux : L’expérience de l’UEMOA souligne les défis consistant à aligner les priorités économiques nationales diverses sur les objectifs d’intégration régionale.

Besoin d’une approche globale : Une intégration régionale efficace nécessite de s’attaquer simultanément à plusieurs facteurs, notamment le développement des infrastructures, l’harmonisation des réglementations et la suppression des barrières non tarifaires.

Importance de la surveillance et de l’application : La mise en œuvre des politiques et des accords régionaux doit être constamment surveillée et appliquée pour atteindre les résultats escomptés.

Malgré son existence de longue date, l’UEMOA fait face à plusieurs défis. Le commerce intra-régional reste relativement faible, et les économies des membres continuent d’être fortement dépendantes des exportations de matières premières vers les marchés en dehors de l’Afrique. La région est également confrontée à des problèmes de sécurité, en particulier dans la région du Sahel, qui affectent les activités économiques et les efforts d’intégration.

À l’avenir, l’UEMOA travaille à approfondir l’intégration grâce à des initiatives telles que la création d’une bourse régionale et les efforts pour harmoniser les lois commerciales. L’union se concentre également de plus en plus sur la coopération en matière de sécurité, reconnaissant le lien entre la stabilité et le développement économique.

En conclusion, l’UEMOA représente une tentative ambitieuse d’intégration économique régionale en Afrique de l’Ouest. Bien qu’elle ait obtenu certains succès, notamment en matière de stabilité monétaire, l’expérience de l’union souligne les complexités de l’intégration régionale.

Alors que l’Afrique se dirige vers une intégration continentale plus large grâce à des initiatives telles que la Zone de libre-échange continentale africaine (ZLECAf), les leçons de l’UEMOA seront précieuses pour façonner des stratégies efficaces de coopération économique et de développement à travers le continent.

The regional bloc’s members include the eight francophone West African countries and offers lessons for regional integration efforts on the continent.

The West African Economic and Monetary Union, commonly known by its French acronym UEMOA (Union Économique et Monétaire Ouest-Africaine) or its English acronym WAEMU, is a significant regional organization in West Africa.

This article provides an overview of WAEMU, addressing key aspects of its structure, functions, and impact on regional integration.

How Many Countries are in the WAEMU?

WAEMU comprises eight member states: Benin, Burkina Faso, Côte d’Ivoire, Guinea-Bissau, Mali, Niger, Senegal, and Togo.

The union was officially established on January 10, 1994, building upon the foundation of the West African Monetary Union (UMOA) created in 1962. Guinea-Bissau joined in 1997, expanding the initial group of seven to eight members.

What is the Purpose and Functions of WAEMU?

WAEMU’s primary objective is to foster economic integration among its member states. It aims to create a harmonized and integrated economic space in West Africa, ensuring the free movement of people, capital, goods, services, and factors of production.

The union works towards enhancing the competitiveness of member economies within an open and competitive market framework, while also streamlining and harmonizing the legal environment across the region.

WAEMU countries share a common currency, the West African CFA franc (XOF).

This currency is pegged to the euro, a legacy of the region’s colonial ties to France. The Central Bank of West African States (BCEAO) manages the monetary policy for all WAEMU members.

The use of a common currency is intended to facilitate trade and investment within the union by eliminating exchange rate risks and reducing transaction costs.

However, it also means that member countries cannot independently adjust their monetary policies to address country-specific economic challenges.

The CFA Franc is pegged to the euro, a legacy of the region’s colonial ties to France.

Differences Between WAEMU and ECOWAS

While WAEMU is focused on economic and monetary integration among its eight francophone members, the Economic Community of West African States (ECOWAS) is a larger regional group that includes all WAEMU countries plus seven others.

ECOWAS aims for broader regional cooperation and integration beyond just economic matters.

The key differences include:

Scope: WAEMU focuses primarily on economic and monetary integration, while ECOWAS has a broader mandate including political cooperation and security.

Membership: WAEMU has 8 members, all of which use the CFA franc, while ECOWAS has 15 members with various currencies.

Depth of integration: WAEMU has achieved deeper economic integration, including a common currency and harmonized economic policies, while ECOWAS is still working towards these goals.

An important element of WAEMU’s financial integration is the Bourse Régionale des Valeurs Mobilières (BRVM), or Regional Securities Exchange.

Established in 1998 and headquartered in Abidjan, Côte d’Ivoire, the BRVM is a unique regional stock exchange serving all eight WAEMU member countries. It’s the only stock exchange in the world that serves multiple countries with a common currency.

The BRVM plays a crucial role in WAEMU’s financial ecosystem by providing a platform for companies to raise capital and for investors to trade securities across the region. It lists a variety of financial instruments, including stocks, bonds, and other securities.

The exchange operates in French, reflecting the predominant language of the WAEMU region, and all transactions are conducted in the common CFA franc currency.

Despite its potential, the BRVM faces challenges typical of frontier markets, including limited liquidity and a relatively small number of listed companies. However, it represents a significant step towards financial integration within WAEMU and has the potential to become an increasingly important tool for mobilizing capital for regional development.

As WAEMU continues to pursue economic integration, the role of the BRVM in facilitating cross-border investment and providing a regional platform for capital raising is likely to grow in importance.

WAEMU’s experience offers several important lessons for regional integration efforts:

Currency union alone is not sufficient: Despite sharing a common currency, WAEMU countries have not seen the expected boost in intra-regional trade or investment. This suggests that other barriers, such as inadequate infrastructure and complex customs procedures, play a significant role in hindering regional economic integration.

Economic diversity matters: WAEMU countries have similar economic structures, often competing in the same export markets rather than complementing each other. This limits the potential for intra-regional trade and economic diversification.

External dependencies persist: The region’s continued economic ties to France and the euro peg have been criticized as limiting economic sovereignty and flexibility.

Political will is crucial: Successful integration requires sustained political commitment from all member states to implement and enforce agreed-upon policies.

Balancing national and regional interests: The experience of WAEMU highlights the challenges of aligning diverse national economic priorities with regional integration goals.

Need for comprehensive approach: Effective regional integration requires addressing multiple factors simultaneously, including infrastructure development, harmonization of regulations, and removal of non-tariff barriers.

Importance of monitoring and enforcement: The implementation of regional policies and agreements needs to be consistently monitored and enforced to achieve desired outcomes.

Despite its long-standing existence, WAEMU faces several challenges. Intra-regional trade remains relatively low, and member economies continue to be heavily dependent on commodity exports to markets outside Africa. The region also grapples with security issues, particularly in the Sahel, which impact economic activities and integration efforts.

Looking ahead, WAEMU is working on deepening integration through initiatives like the creation of a regional stock exchange and efforts to harmonize business laws. The union is also increasing its focus on security cooperation, recognizing the link between stability and economic development.

In conclusion, WAEMU represents an ambitious attempt at regional economic integration in West Africa. While it has achieved some successes, particularly in maintaining monetary stability, the union’s experience underscores the complexities of regional integration.

As Africa moves towards broader continental integration through initiatives like the African Continental Free Trade Area (AfCFTA), the lessons from WAEMU will be valuable in shaping effective strategies for economic cooperation and development across the continent.

I have long been a fan of DFS Lab, the “research-driven venture capital in Africa”.

It’s the only VC firm on the continent that consistently shares – publicly and transparently – nuanced, long-form reflections around its investment thesis.

By doing that, they gifted the ecosystem not just with high-quality articles, but new terms/concepts to describe & make sense of tech in Africa.

Kudos to them! 💥

In a world defined by information overload and sensationalism, mental clarity is one of the most underrated qualities we should consciously strive to cultivate.

How do you know what you know? What is the deep meaning of it? If you cut through the noise, what do you see?

Trying to answer these questions – peeling all the layers of opaqueness – most people would find themselves naked.

This is why, drawing inspiration from the Almanack of Naval Ravikant, I am happy to propose – for the first time – the Almanack of DFS Lab: 6 theoretical primitives to make sense of VC investing in Africa.

These are six concepts coined by the firm that I find extremely insightful/useful in my activities as a researcher/investor:

The Frontier Blindspot

Fortune at the middle of the pyramid

The B-side of African Tech

Cyborgs vs Androids

Invested infrastructure

African S-curves

The original articles are all available on the DFS Lab website and Medium page.

My contribution mainly consists of summarizing my understanding of them & complementing them with my own ideas.

Lessgò.

Subscribe

1) The Frontier Blindspot 👀

Premise: The world has developed “intuitions about how technology markets are structured and what successful technology companies look like”. Cool.

However: this learning process took place strictly in the context of Western economies.

Ergo: the same frameworks do not always apply to frontier markets (like Africa).

Thesis: the disconnect between how we think tech is supposed to work versus how it really works – in Africa & other frontier markets – is the Frontier Blindspot! 💥

It is a blindspot because we are partially clueless – how tech markets work or don’t work in Africa has yet to be demonstrated. As we cannot copy-paste, learning happens by trial and error, thorough research, and on-the-ground experience.

What type of bias did we borrow from the Global North when making our assumptions about tech in Africa?

we overestimated the pace of digitalization;

we underestimated the strength of informal markets;

we overlooked the state of infrastructure and consumer purchasing power

When you factor in low-paced digitalization, strong informal markets, and quirky infra, you’ll see that a lot of common startup wisdom about business models, distribution strategies, and growth projections, won’t apply to the continent.

However, local entrepreneurs are still finding unique ways to apply the “modern startup stack” to the specifics of the African environment.

This is where the real opportunities are, and the areas of excitement include:

Physical logistics

SME solution stack

Financial building blocks

Agent networks

Although these things may seem obvious today, I think they are still not obvious to many, and they certainly were not obvious in 2020 (when the article came out).

What I find particularly useful about this piece is stressing the differences in infrastructure and purchasing power. When looking at pitch decks, I try stress the following questions:

what needs to be there for your product to be made, consumed, or delivered? (read: infrastructure)

How many people can buy your product, regularly? How do you know it?

We are about to have a taste of it with the next concept ✨

Who is the African consumer & what is the real size of the African market for digital products?

Hashtag: debunking the (once) popular tag “Nigeria is a market of 200M people” with some rigorous thinking.

Why?

Because population size does not equal market size, we cannot boast “the youngest population in the world” without looking at income brackets too.

Let’s proceed in order.

“Most B2C tech startups are seeking to make money from people’s discretionary spending”

Discretionary spending is the spending power that remains once covered for necessities like food, clothing, and shelter.

The question asked is: among the 200M fellow Nigerians, how many have the discretionary spending for my type of product?

In the image below, we can look at income levels and their percentage of discretionary income (in Africa).

Source: Fortune at the middle of the pyramid

If you are a B2C startup, what is the juiciest segment?

As a fairly coherent group, the people earning between $5-$10 – while comprising only ~10% of the population – have one of the highest discretionary spending power combined.

This is the fortune at the middle of the pyramid: the segment having enough people, with enough discretionary spending power. To the left of the curve, there are a lot of people but with little money; to the right, they have a lot of money but they are too few.

Now, speaking of unit economics: how much does it cost to acquire these customers? Here things get trickier.

In Africa, higher incomes are usually digitally-fluent city dwellers. Their geographical concentration, professional status, and greater online life, make them perfect targets for digital acquisition strategies. The same doesn’t necessarily hold for lower-income prospects: acquiring them is harder and costs more (with traditional digital methods).

To this comes a paradox: if the cost of acquiring a new customer is way more than what you earn from them, you will soon move to serve higher-income consumers. However, if you only serve the +10$ income bracket, at some point, growth will stall and you’ll need to move cross-border (not easy).

What can we learn from all we just stayed?

purely consumer-focused apps that do not focus on necessities (read: targeting discretionary spending) face unique challenges with monetization in Africa. This is because

the largest economic opportunity sits within the 5-10$ bracket, but the cost of acquiring them is high due to lower digital presence.

Moving forward, I think two very important corollaries emerge about “how to be successful”:

build apps focused on necessities, or focused on the business equivalent of “necessities” (restocking, working capital, inventory etc..);

if you target consumers’ discretionary spending, invest in human agent networks, the physical point of entry to most digital experiences for middle-of-the-pyramid Africans.

Personally, whenever I look at the pitch deck of a B2C company:

if they target offline acquisition, it means they are serving the middle of the pyramid;

if they don’t mention offline acquisition, it means they are serving the top of the pyramid.

Hence, I’ll start to wonder. Given the risk and the complexities of moving cross-border, can they make money (read: positive operating profit) before moving cross-border?

Enjoying the article so far? Share it with bruvs and siss 💥

This article draws inspiration from Wang Huiwen, the co-founder of Meituan Dianping, the most successful Chinese food delivery company, turned super-app.

In an issue of the newsletter “The China Playbook”, Huiwen defines the internet industry as made of two sides:

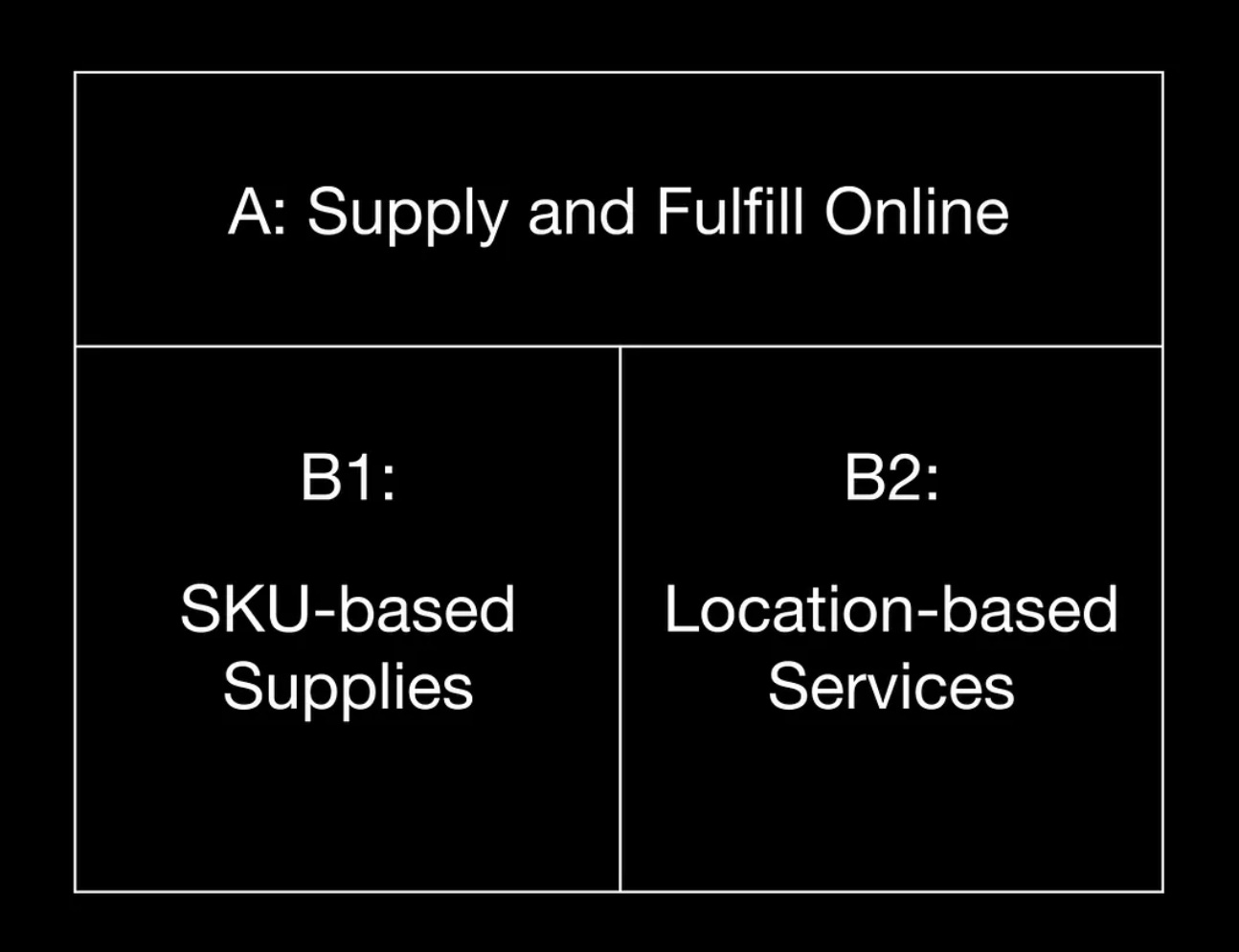

A-side: Supply and Fulfill Online

B-Side: Supply and Fulfill Offline

Side-A is products and services that are “pure internet”, as they can be delivered and consumed entirely online. SaaS (Salesforce), video-games (Voodoo), streaming (Spotify), etc…

Side-B is products and services that are delivered offline and consumed offline. Think of retail (Amazon), mobility (Uber), ticketing (Ticketmaster), etc…

If we have to apply this distinction to African economies, we would see that side-A (online utility) is smaller, compared to side B (offline utility).

The reason is that “fully digital experiences are either inaccessible, unaffordable or don’t cover the primary consumption needs for those in the bottom 95%.”

Ok cool. Let’s have a closer look at the B-side then. The B-side can be further divided into two sub-sections:

B1: SKU-based supplies

B2: location-based services

B1 is companies like Wasoko, Omniretail, and other traditional marketplaces. As digital businesses positioning in between the sourcing & delivery of physical products, their core competencies lie in ”understanding SKUs (stock keeping unit), understanding the supply chain, and understanding pricing”.

B2 is companies like Hubtel and Wahu Mobility. They are location-centric, as the physical location of customers & partners is a key element of their value proposition. For example, a ride-hailing company like Uber will need to recruit drivers in your city and ensure there are enough in your area as you order a ride – otherwise, you won’t be able to access their service. B2 businesses demand a larger offline team to manage operations closer to the customers.

What learnings do we have here?

B1 leverages technology to “improve the efficiency of existing value flows and reorganize pricing power”. On the contrary, “B2 is physical ubiquity”.

Let’s stop here.

In the article, Stephen Deng (DFS Lab MP) expands on the original concept expressed by Meituan Dianping founder.

When Wang Huiwen talks about B2 “location-based businesses”, he is primarily referring to ride-hailing, bike-sharing, and food-delivery, products made accessible by smartphone proliferation, which unlocked & democratized location data. These businesses are useful because you can see your location with your phone, and other people can see it too.

Deng however, twists its meaning for the African context, attaching to it the familiar notion of physical ubiquity: B2 businesses are interesting because of their physical proximity to the customers, mobilizing people and resources last-mile. Other than delivery, one can think of mobile money agents and social commerce as a form of B2 businesses. Their utility comes from their ability to integrate kiosks and people from your neighborhood in their business model. They are relatable, they are next door.

In short, they are more similar to Cyborgs, instead of Androids. What?

You read correctly. The concept of “B-Side of African Tech” is strictly intertwined with that of “Androids vs Cyborgs”, that we explore in the next section (before wrapping up with my two cents on this stuff).

Androids: solutions that replace informal markets with digital, formalized parts and processes

Cyborgs: solutions that enhance informal markets by arming them with digital, formalized parts and processes

Androids use tech to replace a set of existing actors.

Cyborgs use tech to improve the work of a set of existing actors.

Stephen Deng claims that we cannot brute force androids into existence if we are incapable of replacing informal players with significantly better solutions. And if we can’t replace them, we’d better empower them by building cyborgs.

It might seem like a B2C (Android) vs B2B (Cyborgs) play, but it’s more nuanced than that. Examples?

The ultimate Android example is Jumia and all Amazon-inspired B2C marketplaces: “replacing the local market with an online option that is meant to be more convenient, have more options, and is fully digitized”.

However, I think the same holds for many agri-tech platforms (like Complete Farmer or Winich Farms) that aggregate farmers’ produce and facilitate access to market & agro-inputs. In almost every pitch deck you will read about them “cutting out the middlemen”, the set of informal buyers and sellers who move crops to markets, whose commissions eat out farmers’ margins and drive inefficiencies (btw these platforms raised a lot of funds, but it’s not clear to me how much money they are making).

Cyborgs, on the contrary, look like tools that empower small businesses, applying a mix of online and offline. Instead of replacing existing relationships, they “supercharge them with digital optionality when the need arises”.

Both B2-side businesses and Cyborgs, tell the same story: existing structures can be valuable when they are empowered, instead of substituted.

Ok, but empowered how?

In my opinion, an online-offline Cyborg approach, can only be one of two things:

cost-effective offline distribution and/or marketing – agents knocking on doors or setting up shops;

tech-enabled intermediaries/retailers – empowered by a digital backend or specialized hardware.

That’s it!

Moniepoint is Africa’s fastest-growing fintech. Its distribution model? An army of human agents armed with PoS devices, knocking on merchants’ doors. The company revolutionized the capacity for Nigerian businesses to collect digital payments.

→ a Cyborg approach to digital payments.

Retailers’ bookkeeping apps like Oze and supply-chain management tools like Jetstream, both started as digital super-charger of African businesses: I give you tools to better manage invoices and logistics. Fast forward a couple of years, and they both ended up embedding credit and solving the pain of access to capital.

→ a Cyborg approach to digital lending.

I think Cyborg either means giving more “legs and arms” for asset-light digital businesses, or making “legs and arms” (SMBs) more competitive with digital tools.

Digital solution → leave a digital trace → data + learning models → better decision making

Digital solution → relational database & data integration → operational efficiencies

Digital solution → composable software stack → APIs & integrations → new products/services delivered on top of the main product

🪄🪄🪄

More in general, I think that both the “B-Side” and “Android vs Cyborg” arguments tend to over-emphasize the promises of the physical ubiquitous approach, without addressing the elephant in the room: we need more hardware.

A lot of things can be done with your phone, but not everything can be done with your phone, and sometimes, a phone is too much.

Limited storage/memory, weak bandwidth, and high data costs still represent hard limits to app utility for the average African business operator. A phone can do a lot, but not everything.

Safiri is a Tanzanian company equipping bus companies with thermal printers, and customers with digital ticket purchase options. They record transactions “digitally”, and print tickets “physically”. A good blend of digital and physical coming together. No need for Industry 4.0 here, just basic hardware tools.

And yet, I am not seeing enough investors stressing how specialized hardware – as well as consumer hardware – can play its role in the tech landscape.

We need more hardware. We can’t expect to revolutionize the continent simply with apps running on cheap smartphones.

I feel we’ll see major shifts when large-scale hardware manufacturing that truly responds to local business needs comes to fruition.

And yes, somehow, I am still convinced this can be a VC play.

Enjoying the article so far? Subscribe to Data Bites & have more of this 💩Subscribe

The concept is simple, yet powerful: the infrastructure built in the past has a lasting, indelible influence on our present & future.

Economists call it “path dependency”: society builds on top of what has been built, and this process makes us drift toward a trajectory of development and away from others.

In the United States, payment infrastructure has been built “for a time when phones were not as ubiquitous and hard-wired ethernet was increasingly common.”

The proliferation of PoS devices & phone cables (& later fiber cables), gradually made up the physical network on top of which credit cards’ adoption became widespread.

The alternative to cash travels on rails that took a long time to build, but once in place, it is hard to replace. It’s the hidden cost of path dependency: the more we build on top of invested infrastructure, the higher the switching costs to a different system.

“They have since gained ubiquity, and because mobile phone-based services can only offer marginal improvements, the system stays resilient — it is challenging to overcome the inertia of this invested infrastructure”

What is the invested infrastructure in Africa and how will it impact its future?

It is an important question to ask because – as we have seen – companies that leverage invested infrastructure can have a competitive edge, reducing costs and frictions to adoption; those that try to replace it might sink under the weight of high switching costs & behavioral change (although in some cases – boom jackpot 🎰).

If we think of financial infrastructure, in Africa the equivalent of the US card network is a combination of:

a human agent network

phones & SIM cards

tower cells

It hasn’t always been the case. The capillary presence established by telco companies in the continent from the 90s onward, brought along the way important infrastructural development that served as the launchpad to mobile money: financial infrastructure borrowed from the already existing communication infrastructure.

A human agent network could now be used to on-ramp/off-ramp physical cash.

Phones and SIM cards became wallets.

Tower cells relayed information – and now value – across long distances.

Innovation on top of invested infrastructure.

But it’s not over.

As the new payments infrastructure emerged, further developments “up the ladder” could see the light of day: “The combination of USSD-based mobile accounts that worked on every phone and cash-in/cash-out agents in nearly every neighborhood and village proved to be powerful infrastructure on which to build new product offerings”.

The first wave of successful tech businesses on the continent – real “market-creating” innovations – are the product of it.

Examples:

First generation: pay-as-you-go solar (like M-Kopa)

Second generation: digital lending

Access to energy & access to credit. Both are built on top of mobile money infrastructure, built on top of telco’s invested infrastructure.

What lessons can we take home from this chapter?

invested infrastructure matters

it looks different in Africa than in other places

opportunities exist for those who build on top of it + those who make it more efficient

Personally, I find myself asking the question” What’s the invested infrastructure here?”. And not just for payments, but for commerce, logistics, agriculture etc.. In short, it translates to: how things are done now, how much does it cost to switch and who has interest in doing it?

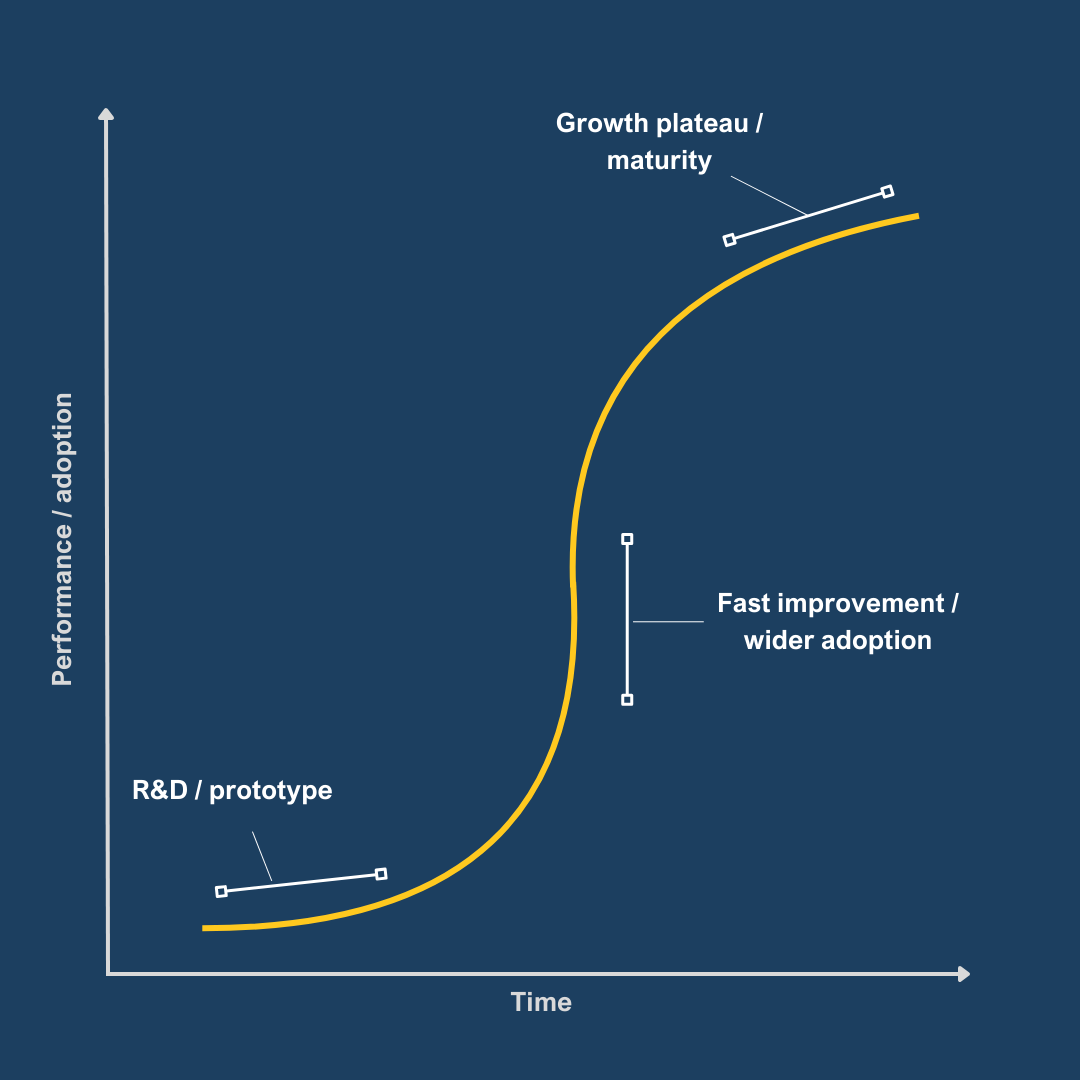

S-curves describe the performance of a new technology – or a technological toolset – over time.

In the beginning, during the R&D and prototyping phase, adoption is minimal and the potential of tech still needs to be validated. The curve is flat and growing slowly. Think of electric cars 15 years ago. It is the territory of university budgets, public finance, and research grants.

When the tech starts showing signs of improvement, it is followed by a steep acceleration in performance and increased adoption. Think of Generative AI one year ago. It is the land of VCs, profiting “by investing in emerging tech before it’s mainstream and exiting when growth plateaus”.

Finally, when a technology is mature, adoption widespread and there is little room for marginal improvements: the tail of the curve flattens. It is the PE and stock market game.

And then, onto the next technology, that will replace the incumbent with the next S-curve. Venture capital funding follows the S-curves cycle, the peak funding being when the curve is at its highest steep.

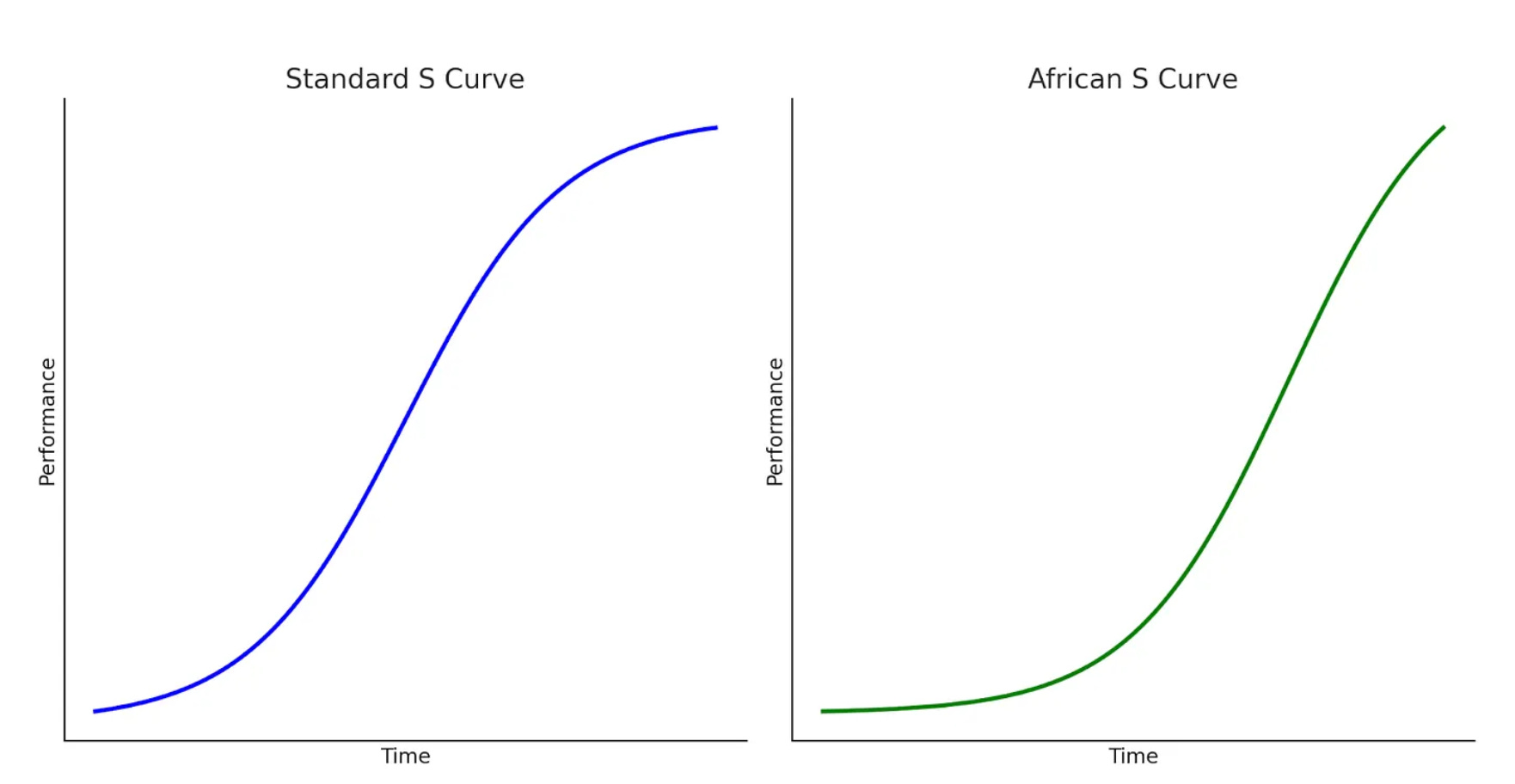

Now: in the wake of funding drought, startup bankruptcies, and crowding away of international investors, what can we say about the shape of the African S-curve?

One: African S curves have much longer tails.

This means that it takes more time for tech in Africa to see widespread adoption. Rather than a limit to technology performance, the problem lies in the lack of market readiness.

Read: “Customers don’t need new tech, or don’t trust new tech, or can’t afford new tech, or don’t have access to infrastructure for new tech, or don’t believe new tech provides enough value vs. old tech”

Two: African S curves have much steeper slopes

On the contrary, once adoption kicks in, the potential for improvements in technology can last for a very long time, going beyond what was once imagined.

The acceleration phase lasts a long time along with its benefits.

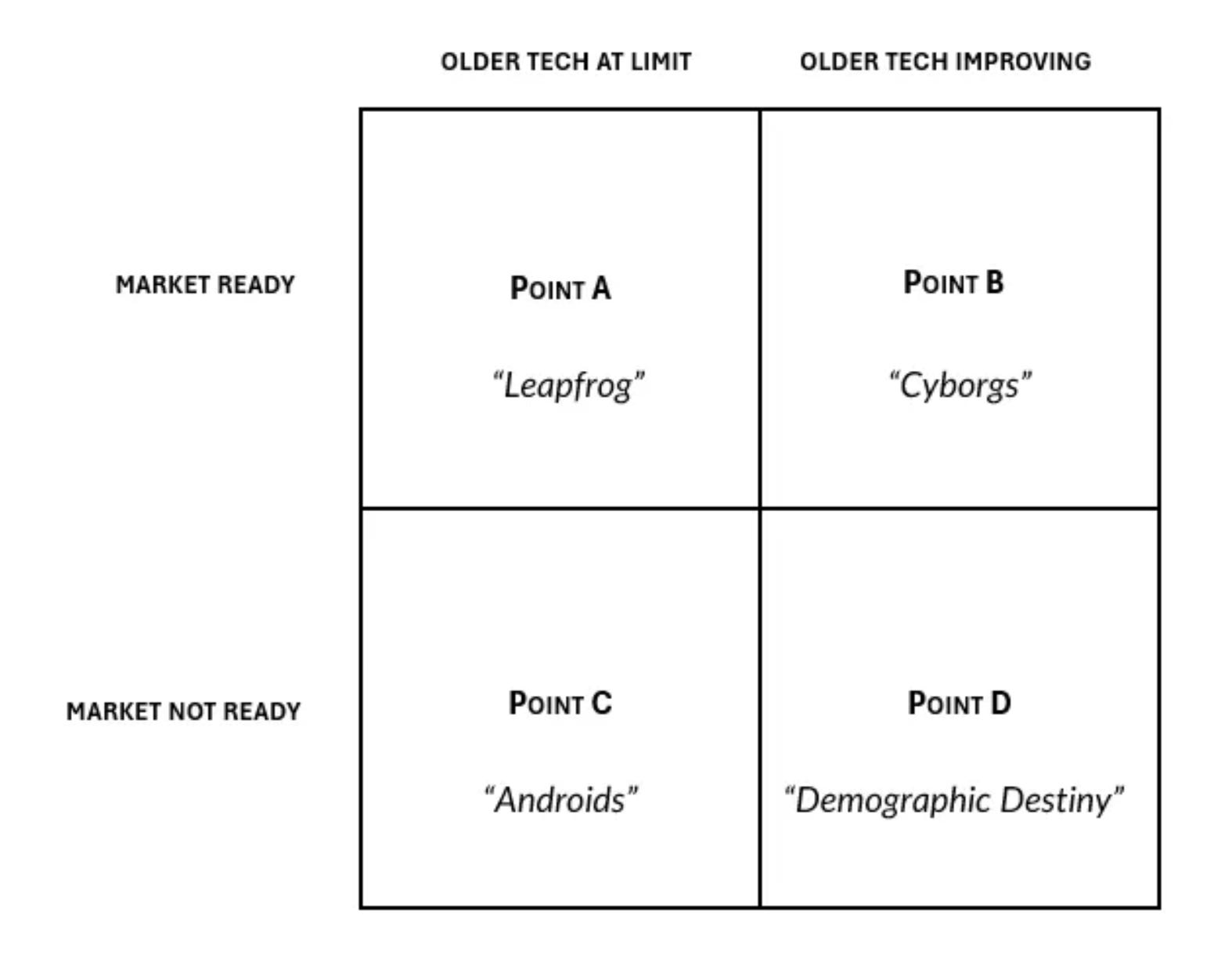

How do we change from one S-curve to the other? When will the new tech replace the old one?

There are 4 different scenarios.

If the old tech is not improving, and the market is ready for a novel solutions, then we’ll have a quick transition. This means heading towards Point A, and what people cheer as Africa’s technology leapfrog.

On the opposite side, if incumbents are delivering increasingly better utility to consumers, who are not ready to change for newcomers, then we’ll have a very gradual and slow transition. Ergo, heading towards Point D.

Many people either bought the point A narrative (technology leapfrog), or buys into point C one. They think old tech is crap, inefficient, and not making any progress. However, the market is not ready for new digital solutions yet. It’s a matter of time.

Stephen Deng, on the contrary, thinks we are heading towards point B. A situation where yes, the market is not ready, but the old tech – and the ecosystem around it – is still improving.

Think of mobile money. It is a fairly old technology ( and USSD codes), but it can still deliver innovation to its users. Telcos are blending digital offerings into their core model; traditional financial services are integrating with the mobile money ecosystem for seamless interactions; new products are developed on top of it every month.

If MoMo is the old tech, the new tech would be close to neo-banks like Djamo. How many customers does one have vs the other?

The shelf life of telecommunications technology has been pretty long. No surprise than that the true champions of tech in the continent are telcos. Companies like MTN, Airtel, Safaricom. This is in stark contrast with the Google, the Meta and the Microsoft of North America.

The main argument is the following: from now on, until we reach point B, a lot of incremental innovations will be built around the existing tech. We need to surf it 🏄🏽♂️

It is what Deng calls the “cybernetic commerce” area, yet another version of the Cyborg thesis.

The most interesting element of this article, to me, is the mental framework that comes with it: how many incremental innovations can still be built on top of the existing rails?

When you look at African markets overall, you’ll see that a lot of problems can be solved with existing technologies. There is no need for a breakthrough.

How to deliver the benefits of tech without losing money: this is the number one skill a founder must have.

This is the end, my friends. I hope you enjoyed the read. Writing this piece I’ve noticed that – as telcos in Africa – my essays have room for improvement. In particular, from now on I will try to deliver:

more real-life examples (what companies, what products etc…) → it helps with mental clarity when you have more than 1/2 examples

more exit simulations (revenues, potential returns) → VC exists where outsized returns exist, and we need to be more rigorous on that.

Contributed by Ajibola Awojobi, founder and CEO of BorderPal.

As the sun rises over Lagos, Adebayo, a young Nigerian fintech entrepreneur, stares at his computer screen. His brow furrowed in concentration and his startup, a mobile money platform to bring financial services to the unbanked, has just secured significant funding from a Silicon Valley venture capital firm. It should be a moment of triumph, but Adebayo feels a gnawing sense of unease. The numbers on his screen tell a troubling story: his company is spending $20 to acquire each new customer, yet the average revenue per user is a mere $7.

Adebayo’s predicament is not unique. Across Africa, fintech startups are grappling with a challenging reality: the cost of customer acquisition often far outweighs the immediate returns. This scenario raises a critical question: Is Africa’s venture capital-backed fintech model sustainable or fundamentally broken?

VCs and the Promise of African Fintech

The African continent has long been considered the next frontier for fintech innovation. With a large unbanked population and rapidly increasing mobile phone penetration, the potential for transformative financial services seemed boundless. Venture capitalists, enticed by the prospect of tapping into a market of over a billion people—half without any formal bank account—have poured billions of dollars into African fintech startups over the past decade.

These investments have fueled remarkable innovations. From mobile money platforms that allow users to send and receive funds with a simple text message, to AI-powered credit scoring systems that enable microloans for small businesses, African fintechs have been at the forefront of financial inclusion efforts.

However, as Adebayo’s experience illustrates, translating these innovations into sustainable businesses has proven to be a formidable challenge.

While Adebayo grapples with his early-stage startup’s challenges, a major African fintech player with a customer base of 300,000 users has just raised a mammoth $150 million, which brings its total funding to nearly $600 million. Based on a customer acquisition cost and revenue per customer established earlier, the economics of this deal seem precarious at best. A quick calculation reveals that the company would have spent around $6 million just to acquire its current user base while generating only $2.1 million. The funding, while impressive, thus raises serious questions about the sustainability of this model and the investors’ expectations.