En 2026, dans un contexte économique mondial plus structuré mais toujours incertain, les obligations restent l’un des meilleurs outils pour générer des revenus réguliers, préserver son capital et équilibrer un portefeuille d’investissement. Que tu sois débutant ou investisseur expérimenté, bien comprendre comment tirer profit des obligations est essentiel.

Qu’est-ce qu’une obligation et pourquoi investir en 2026 ?

Une obligation est un titre de créance émis par un État, une institution publique ou une entreprise. En achetant une obligation, tu prêtes de l’argent à l’émetteur, qui s’engage à te verser des intérêts réguliers (appelés coupons) et à te rembourser le capital à l’échéance.

En 2026, les obligations sont particulièrement intéressantes car :

Les taux d’intérêt se sont stabilisés, offrant une meilleure visibilité sur les rendements

Elles permettent de réduire la volatilité face aux marchés actions

Elles génèrent des revenus prévisibles, idéals pour une stratégie patrimoniale

4 stratégies pour gagner de l’argent avec les obligations

1. Générer des revenus réguliers

Les coupons obligataires offrent des paiements périodiques (annuels ou semestriels). C’est une excellente source de revenus passifs, notamment pour compléter un salaire ou préparer la retraite.

2. Acheter des obligations à prix décoté

Lorsque les taux montent, certaines obligations se négocient en dessous de leur valeur nominale. Les acheter à prix réduit permet d’augmenter ton rendement total à l’échéance.

3. Mettre en place une stratégie d’échelonnement

L’échelonnement (bond ladder) consiste à investir dans des obligations avec différentes maturités afin de limiter le risque de taux et de réinvestir régulièrement à de meilleures conditions.

4. Gérer le risque de crédit

Les obligations d’État sont généralement plus sûres mais moins rémunératrices. Les obligations d’entreprises offrent souvent des rendements plus élevés, avec un risque légèrement supérieur. L’équilibre entre les deux est clé.

Investir facilement avec les bons outils

Pour investir efficacement, il faut une plateforme fiable. L’application Daba te permet d’investir simplement dans des obligations, de suivre tes rendements et de gérer ton portefeuille en toute transparence, depuis un seul espace.

Pour les investisseurs plus actifs ou avancés, Daba Pro donne accès à des analyses approfondies, des opportunités sélectionnées et des outils professionnels pour optimiser tes décisions.

Se former pour investir intelligemment

Enfin, la connaissance reste ton meilleur allié. Daba Academy propose des formations claires et accessibles sur les obligations, la gestion du risque et les stratégies d’investissement adaptées aux marchés africains et émergents.

En résumé : en 2026, les obligations sont un pilier incontournable pour bâtir un patrimoine solide. Avec la bonne stratégie, les bons outils et une formation continue, elles peuvent devenir une source durable de revenus et de stabilité financière.

As global markets evolve in 2026, bonds remain one of the smartest ways to generate steady income, preserve capital, and diversify your investment portfolio. Whether you’re a beginner investor or building long-term wealth, understanding how to profit from bonds — and using the right tools — can make all the difference.

Understanding Bonds and Why They Matter

Bonds are debt securities issued by governments, municipalities, and corporations to raise capital. When you buy a bond, you’re essentially lending money to the issuer in exchange for periodic interest payments (the coupon) and return of principal at maturity.

In 2026, bonds continue to offer value because:

Interest rates have stabilized after recent economic shifts, improving yield opportunities.

Risk-adjusted returns can outperform volatile equities for income-focused investors.

Diversification benefits help protect portfolios during market downturns.

Strategies to Make Money with Bonds

Here are proven approaches you can use:

1. Invest for Steady Income

Most bonds pay interest regularly — typically semi-annually or annually. These coupon payments are reliable cash flows you can reinvest or use for living expenses.

2. Buy Bonds at a Discount

When interest rates rise, existing bonds may trade below their face value. Buying bonds at a discount increases your total return, as you’ll receive the full face value at maturity.

3. Ladder Your Bond Portfolio

A “bond ladder” staggers maturities so you regularly reinvest at prevailing rates. This strategy manages interest rate risk and provides consistent liquidity.

4. Consider Credit Quality

Higher-rated bonds (like government bonds) are lower risk but often offer lower yields. Corporates may pay higher yields — but with slightly more risk. Balancing credit quality is key.

Use the Right Platform

Investing efficiently starts with the right tools. The Daba App makes buying, selling, and tracking bonds simple — whether you’re investing in government securities or corporate notes. Its intuitive interface helps you monitor yields, maturities, and your income flows in real time.

If you’re a serious investor seeking advanced features — like institutional-grade analytics and deeper market insights — Daba Pro equips you with enhanced research tools and priority access to curated bond offerings.

Build Your Knowledge

Not sure where to start? The Daba Academy offers structured courses on bonds, risk management, yield curves, and fixed-income strategies. Learning foundational concepts empowers you to make smarter investment decisions.

Le rendement d’une obligation est essentiellement le retour qu’un investisseur reçoit sur son investissement, généralement exprimé en pourcentage et calculé de plusieurs manières.

Les rendements des obligations sont un concept crucial dans le monde de la finance et de l’investissement. Ils représentent le retour qu’un investisseur peut s’attendre à gagner en détenant une obligation.

Comprendre les rendements des obligations est essentiel tant pour les investisseurs individuels qu’institutionnels, car ils jouent un rôle significatif dans les décisions d’investissement et l’analyse économique.

Explorons plus en détail le concept des rendements obligataires.

Qu’est-ce qu’une Obligation ?

Avant d’aborder les rendements, il est important de comprendre ce qu’est une obligation. Une obligation est essentiellement un prêt consenti par un investisseur à un emprunteur, typiquement un gouvernement ou une entreprise.

Lorsque vous achetez une obligation, vous prêtez de l’argent à l’émetteur pour une période spécifique, connue sous le nom de terme jusqu’à l’échéance. En retour, l’émetteur promet de vous verser des paiements d’intérêts réguliers et de vous rembourser le montant principal à l’échéance de l’obligation.

Par exemple, le gouvernement nigérian pourrait émettre une obligation à 10 ans d’une valeur nominale de 100 000 nairas. Un investisseur qui achète cette obligation prête effectivement 100 000 nairas au gouvernement nigérian pour une durée de 10 ans.

Les Bases du Rendement Obligataire

Le rendement d’une obligation est essentiellement le retour qu’un investisseur reçoit sur son investissement. Il est généralement exprimé en pourcentage et peut être calculé de plusieurs façons. La forme la plus simple de rendement est le rendement du coupon, qui est le paiement d’intérêts annuel divisé par la valeur nominale de l’obligation.

Par exemple, si notre obligation du gouvernement nigérian verse 5 000 nairas d’intérêts annuels, son rendement du coupon serait de 5 % (5 000 / 100 000). Cependant, ce calcul de base ne raconte pas toute l’histoire, car il ne tient pas compte des variations du prix de marché de l’obligation ni de la valeur temporelle de l’argent.

Rendement Actuel

Le rendement actuel offre une image plus précise du retour d’une obligation basé sur son prix de marché actuel. Il est calculé en divisant le paiement d’intérêts annuel par le prix de marché actuel de l’obligation.

Supposons que notre obligation du gouvernement nigérian se négocie maintenant à 95 000 nairas sur le marché secondaire. Le rendement actuel serait d’environ 5,26 % (5 000 / 95 000). Ce rendement plus élevé reflète le fait que l’obligation se négocie à un prix inférieur à sa valeur nominale.

Rendement à l’Échéance

Le rendement à l’échéance (YTM) est considéré comme la mesure la plus complète du rendement d’une obligation. Il prend en compte le prix de marché actuel, la valeur nominale, le taux de coupon et le temps restant jusqu’à l’échéance. Le YTM représente le rendement total qu’un investisseur recevrait s’il détenait l’obligation jusqu’à son échéance, en supposant que tous les paiements d’intérêts sont réinvestis au même taux.

Le calcul du YTM est plus complexe et nécessite souvent l’utilisation de logiciels financiers ou de calculatrices. Pour notre exemple d’obligation nigériane, si elle se négocie à 95 000 nairas avec 5 ans restants jusqu’à l’échéance, son YTM pourrait être d’environ 6,2 %, en supposant que tous les paiements sont réinvestis à ce taux.

La Relation Entre les Prix des Obligations et les Rendements

L’un des concepts les plus importants à comprendre concernant les rendements obligataires est leur relation inverse avec les prix des obligations. Lorsque les prix des obligations augmentent, les rendements diminuent, et vice versa. Cette relation est cruciale pour comprendre le comportement des obligations sur le marché.

Par exemple, si les taux d’intérêt au Kenya augmentent, les obligations nouvellement émises offriront des taux de coupon plus élevés pour attirer les investisseurs. Cela rend les obligations existantes avec des taux de coupon plus bas moins attractives, entraînant une baisse de leurs prix et une hausse de leurs rendements.

Facteurs Affectant les Rendements des Obligations

Plusieurs facteurs peuvent influencer les rendements des obligations :

Taux d’Intérêt : Comme mentionné, les changements dans les taux d’intérêt en vigueur affectent directement les rendements des obligations. Lorsque la Banque Centrale du Nigeria augmente les taux d’intérêt, par exemple, les rendements des obligations augmentent généralement.

Qualité de Crédit : Les obligations émises par des entités ayant des notations de crédit plus faibles (comme certaines obligations d’entreprise) offrent généralement des rendements plus élevés pour compenser le risque accru de défaut. Par exemple, une obligation émise par une entreprise sud-africaine stable de premier plan pourrait avoir un rendement inférieur à celui émis par une entreprise ghanéenne plus petite et moins établie.

Maturité : En général, les obligations à plus long terme offrent des rendements plus élevés que les obligations à court terme pour compenser le risque accru associé au prêt d’argent sur une période plus longue.

Conditions Économiques : Des facteurs économiques tels que l’inflation, la croissance du PIB et la stabilité politique peuvent tous influencer les rendements des obligations. Par exemple, lors de périodes de forte inflation au Zimbabwe, les rendements des obligations pourraient augmenter pour compenser les investisseurs pour la diminution du pouvoir d’achat de l’argent.

Offre et Demande : L’offre globale d’obligations sur le marché et la demande des investisseurs peuvent influencer les rendements. S’il y a une forte demande pour les obligations gouvernementales marocaines, par exemple, leurs rendements pourraient diminuer.

La courbe de rendement est une représentation graphique des rendements des obligations ayant différentes maturités. Dans un environnement économique normal, la courbe de rendement s’incline vers le haut, les obligations à plus long terme offrant des rendements plus élevés que les obligations à court terme. Cela est souvent considéré comme un signe de bonne santé économique.

Cependant, parfois, la courbe de rendement peut devenir “inversée”, où les rendements à court terme sont plus élevés que ceux à long terme. Cela est souvent perçu comme un indicateur potentiel d’une récession imminente. Par exemple, si les bons du Trésor nigérians à court terme commençaient à offrir des rendements plus élevés que les obligations gouvernementales nigérianes à 10 ans, cela pourrait signaler une incertitude économique.

Pourquoi les Rendements des Obligations Comptent

Les rendements des obligations sont importants pour plusieurs raisons :

Décisions d’Investissement : Les rendements aident les investisseurs à comparer différentes obligations et à prendre des décisions d’investissement éclairées. Un investisseur en Égypte pourrait comparer les rendements des obligations gouvernementales égyptiennes avec celles des obligations d’entreprise pour décider où allouer ses fonds.

Indicateur Économique : Les rendements des obligations, en particulier ceux des obligations gouvernementales, sont souvent utilisés comme indicateurs de la santé économique et du sentiment des investisseurs. Des rendements faibles sur les obligations gouvernementales sud-africaines, par exemple, pourraient indiquer la confiance des investisseurs dans la stabilité économique du pays.

Politique Monétaire : Les banques centrales prêtent une grande attention aux rendements des obligations lors de la prise de décisions en matière de politique monétaire. La Banque du Ghana, par exemple, pourrait considérer les rendements des obligations gouvernementales ghanéennes lorsqu’elle décide d’ajuster les taux d’intérêt.

Financement des Entreprises : Les rendements des obligations influencent le coût d’emprunt des entreprises. Si les rendements sont bas, il est moins coûteux pour les entreprises d’émettre des obligations et de lever des capitaux, ce qui peut stimuler la croissance économique.

Taux Hypothécaires : Dans de nombreux pays, les taux hypothécaires sont souvent liés aux rendements des obligations gouvernementales. Des changements dans les rendements des obligations gouvernementales kenyanes, par exemple, pourraient influencer les taux d’intérêt offerts sur les hypothèques au Kenya.

Utilisation des Rendements des Obligations dans les Stratégies d’Investissement

Les investisseurs peuvent utiliser les rendements des obligations de diverses manières :

Génération de Revenus : Les obligations à rendements plus élevés peuvent fournir un flux de revenus régulier. Des retraités en Namibie, par exemple, pourraient investir dans des obligations d’entreprise à haut rendement pour compléter leurs revenus de pension.

Diversification de Portefeuille : En incluant des obligations avec différents rendements dans un portefeuille, les investisseurs peuvent équilibrer le risque et le rendement. Un investisseur sud-africain pourrait combiner des obligations d’entreprise à haut rendement avec des obligations gouvernementales à rendement plus faible pour diversifier son portefeuille.

Stratégies Basées sur la Courbe de Rendement : Des investisseurs sophistiqués pourraient utiliser des stratégies basées sur la forme de la courbe de rendement. Par exemple, si un investisseur s’attend à ce que la courbe de rendement au Nigeria s’accentue, il pourrait vendre des obligations à court terme et acheter des obligations à long terme.

Comprendre Correctement les Rendements des Obligations

Les rendements des obligations sont un concept fondamental en finance, fournissant des informations cruciales sur le retour des investissements obligataires et les conditions économiques générales.

Que vous soyez un investisseur individuel au Kenya envisageant d’ajouter des obligations à votre portefeuille, ou un analyste financier en Afrique du Sud évaluant les tendances économiques, comprendre les rendements des obligations est essentiel.

Rappelez-vous que, bien que des rendements plus élevés puissent sembler attractifs, ils s’accompagnent souvent de risques plus élevés. Il est important de considérer vos objectifs d’investissement, votre tolérance au risque et le contexte économique global lors de l’interprétation et de l’action sur les informations relatives aux rendements obligataires.

Comme pour tout investissement, il est conseillé de consulter un professionnel financier avant de prendre des décisions d’investissement importantes basées sur les rendements des obligations ou tout autre indicateur financier.

The yield of a bond is essentially the return an investor receives on their investment, usually expressed as a percentage and calculated in several ways.

Bond yields are a crucial concept in the world of finance and investing. They represent the return an investor can expect to earn from holding a bond.

Understanding bond yields is essential for both individual and institutional investors, as they play a significant role in investment decisions and economic analysis.

Let’s explore the concept of bond yields in more detail.

What is a Bond?

Before diving into yields, it’s important to understand what a bond is. A bond is essentially a loan made by an investor to a borrower, typically a government or corporation.

When you buy a bond, you’re lending money to the issuer for a specific period, known as the term to maturity. In return, the issuer promises to pay you regular interest payments and return the principal amount when the bond matures.

For example, the Nigerian government might issue a 10-year bond with a face value of 100,000 Naira. An investor who purchases this bond is effectively lending 100,000 Naira to the Nigerian government for 10 years.

Bond Yield Basics

The yield of a bond is essentially the return an investor receives on their investment. It’s usually expressed as a percentage and can be calculated in several ways. The simplest form of yield is the coupon yield, which is the annual interest payment divided by the bond’s face value.

For instance, if our Nigerian government bond pays 5,000 Naira in annual interest, its coupon yield would be 5% (5,000 / 100,000). However, this basic calculation doesn’t tell the whole story, as it doesn’t account for changes in the bond’s market price or the time value of money.

Current Yield

The current yield provides a more accurate picture of a bond’s return based on its current market price. It’s calculated by dividing the annual interest payment by the bond’s current market price.

Let’s say our Nigerian government bond is now trading at 95,000 Naira in the secondary market. The current yield would be approximately 5.26% (5,000 / 95,000). This higher yield reflects the fact that the bond is trading at a discount to its face value.

Yield to Maturity

Yield to Maturity (YTM) is considered the most comprehensive measure of a bond’s yield. It takes into account the current market price, face value, coupon rate, and time to maturity. YTM represents the total return an investor would receive if they held the bond until it matures, assuming all interest payments are reinvested at the same rate.

Calculating YTM is more complex and often requires financial software or calculators. For our Nigerian bond example, if it’s trading at 95,000 Naira with 5 years left to maturity, its YTM might be around 6.2%, assuming all payments are reinvested at this rate.

The Relationship Between Bond Prices and Yields

One of the most important concepts to grasp about bond yields is their inverse relationship with bond prices. When bond prices go up, yields go down, and vice versa. This relationship is crucial for understanding how bonds behave in the market.

For example, if interest rates in Kenya rise, newly issued bonds will offer higher coupon rates to attract investors. This makes existing bonds with lower coupon rates less attractive, causing their prices to fall and their yields to rise.

Factors Affecting Bond Yields

Several factors can influence bond yields:

Interest Rates: As mentioned, changes in prevailing interest rates directly affect bond yields. When the Central Bank of Nigeria raises interest rates, for instance, bond yields typically increase.

Credit Quality: Bonds issued by entities with lower credit ratings (like some corporate bonds) typically offer higher yields to compensate for the increased risk of default. For example, a bond issued by a stable South African blue-chip company might have a lower yield than one issued by a smaller, less established Ghanaian company.

Maturity: Generally, longer-term bonds offer higher yields than shorter-term bonds to compensate for the increased risk associated with lending money for a longer period.

Economic Conditions: Economic factors such as inflation, GDP growth, and political stability can all impact bond yields. For instance, during periods of high inflation in Zimbabwe, bond yields might rise to compensate investors for the eroding purchasing power of money.

Supply and Demand: The overall supply of bonds in the market and the demand from investors can influence yields. If there’s high demand for Moroccan government bonds, for example, their yields might decrease.

The yield curve is a graphical representation of the yields of bonds with different maturities. In a normal economic environment, the yield curve slopes upward, with longer-term bonds offering higher yields than shorter-term bonds. This is often seen as a sign of economic health.

However, sometimes the yield curve can become “inverted,” where short-term yields are higher than long-term yields. This is often viewed as a potential indicator of an upcoming recession. For instance, if short-term Nigerian treasury bills started offering higher yields than 10-year Nigerian government bonds, it might signal economic uncertainty.

Why Bond Yields Matter

Bond yields are important for several reasons:

Investment Decisions: Yields help investors compare different bonds and make informed investment decisions. An investor in Egypt might compare the yields of Egyptian government bonds with corporate bonds to decide where to allocate their funds.

Economic Indicator: Bond yields, especially government bond yields, are often used as indicators of economic health and investor sentiment. Low yields on South African government bonds, for example, might indicate investor confidence in the country’s economic stability.

Monetary Policy: Central banks pay close attention to bond yields when making monetary policy decisions. The Bank of Ghana, for instance, might consider the yields on Ghanaian government bonds when deciding whether to adjust interest rates.

Corporate Financing: Bond yields influence the cost of borrowing for corporations. If yields are low, it’s cheaper for companies to issue bonds and raise capital, which can stimulate economic growth.

Mortgage Rates: In many countries, mortgage rates are often linked to government bond yields. Changes in the yields of Kenyan government bonds, for example, might influence the interest rates offered on mortgages in Kenya.

Using Bond Yields in Investment Strategies

Investors can use bond yields in various ways:

Income Generation: Bonds with higher yields can provide a steady stream of income. Retirees in Namibia, for instance, might invest in high-yield corporate bonds to supplement their pension income.

Portfolio Diversification: By including bonds with different yields in a portfolio, investors can balance risk and return. A South African investor might combine high-yield corporate bonds with lower-yield government bonds for diversification.

Yield Curve Strategies: Sophisticated investors might use strategies based on the shape of the yield curve. For example, if an investor expects the yield curve in Nigeria to steepen, they might sell short-term bonds and buy long-term bonds.

Getting Bond Yields Right

Bond yields are a fundamental concept in finance, providing crucial information about the return on bond investments and broader economic conditions.

Whether you’re an individual investor in Kenya considering adding bonds to your portfolio, or a financial analyst in South Africa assessing economic trends, understanding bond yields is essential.

Remember, while higher yields might seem attractive, they often come with higher risk. It’s important to consider your investment goals, risk tolerance, and the broader economic context when interpreting and acting on bond yield information.

As with all investments, it’s advisable to consult with a financial professional before making significant investment decisions based on bond yields or any other financial metric.

There are not many places to look but up in the new year for African tech stakeholders after what turned out to be a tough 2023 for startups globally.

This year, budgets and valuations were cut, business models revised, layoffs were frequent, and some startups shuttered as the harsh realities of a funding downturn, mismanagement, and fraud took their toll on African tech.

It’s time to take stock of the last 12 months in what’s been a rollercoaster year. Read on to discover the major themes in Africa’s tech ecosystem.

The venture funding market shrinks

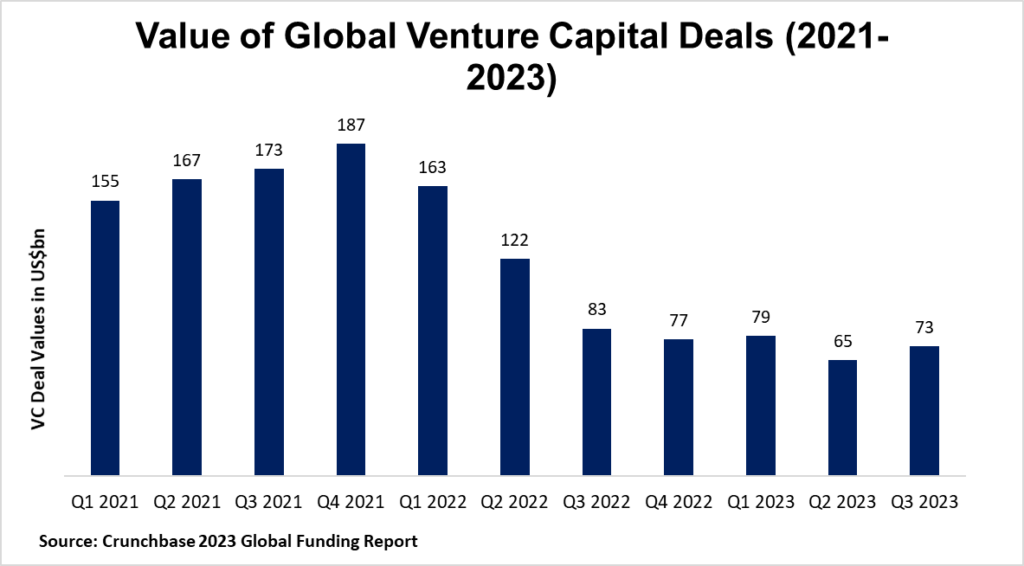

The exuberance of 2022’s VC landscape gave way to a stark reality in 2023, with funding plummeting by around half globally in the first half of the year.

This dramatic shift coincided with hikes in interest rates, which had a chilling effect on fundraising. For every 1% hike in interest rates, there was an alarming 3.2% decline in VC capital.

This tightening environment not only reduced the pool of VC money available to startups but also made debt financing, a potential alternative, a less viable option due to higher borrowing costs.

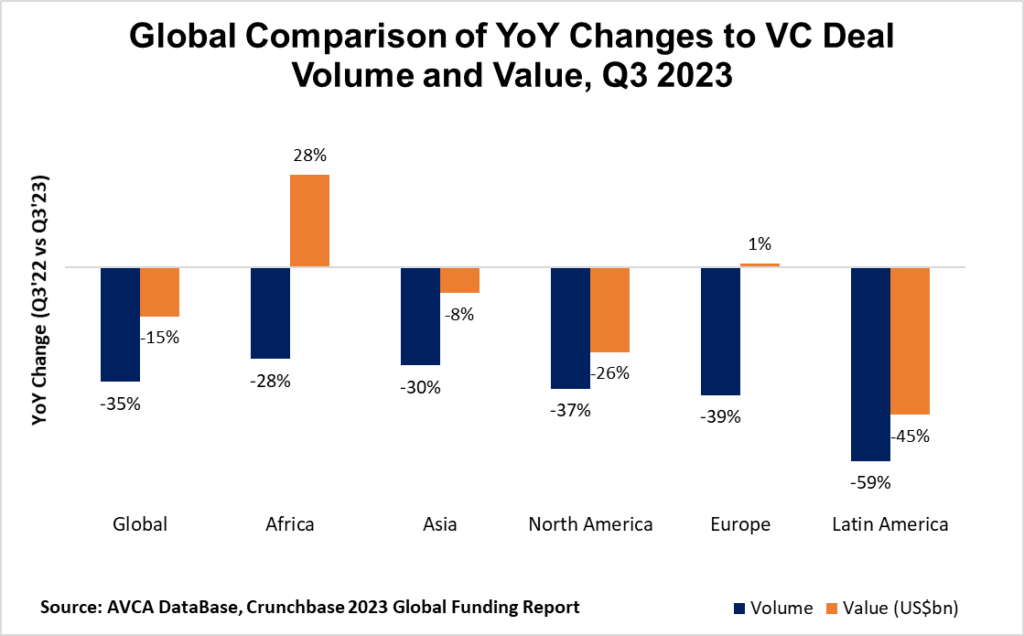

After a bullish 2022 in which Africa was the only continent to record growth in venture funding values, there was no escaping the downturn this year.

The funding winter reached the continent in the H1 2023. Startup funding plunged to just over $1bn, a stark drop from $3.5bn the year before, per AVCA data.

Investors completed 263 deals – a 40% reduction in both deal volume and funding compared to the previous year.

Although African startups staged an impressive comeback in Q3 2023, with funding jumping by 28% compared to the year before.

The general slowdown prompted a reshuffle, with investor focus shifting towards nurturing young startups in their early stages or mature players nearing unicorn status.

Most likely Africa’s VC funding figures fell far from 2022 levels. The final tally as of Q3 2023 to date, per AVCA, stood at $2.95bn – down from the $4.3bn that was raised by the same point last year.

That means Africa’s venture capital industry managed to attract two-thirds (69%) of the capital it accrued by September 2022, and a more disappointing 56% of the total funding last year.

While VC funding is harder to come by, Development Finance Institutions (DFIs)—such as the IFC, BII, US DFC, and Proparco—are becoming more active in the tech startup landscape.

Venture debt & hybrid rounds become more frequent

2023’s funding scorecards are yet to roll out but available estimates suggest the continent’s startups still managed to attract more than $5bn.

Compared to previous years, a higher portion of the total funding is likely to be in the form of venture debt, which has become an alternative source of capital for African startups.

Notable in startup fundraising announcements this year is the growing frequency of mixed equity and debt funding rounds.

Examples include:

Okra Solar’s Series A round ($7.85m equity and $4.15m debt);

Complete Farmer’s pre-Series A funding round ($7m equity and $3.4m debt)

Wetility’s $50m fundraising included a $33m commercial debt package from a consortium of commercial and development banks

While venture debt shines as a catalyst for early-stage ventures, providing crucial working capital to fuel their growth, it’s also increasingly powering expansion for more established startups.

This is the case with:

Mobility FinTech startup Moove Africa. It has raised $325m to date ($150m in equity and over $175m in debt)

Kenyan solar home system provider d.Light’s $125m securitization facility. The company’s total securitized financing is $490m since 2020

An uptick in startup shutdowns, pivots & downsizing

With global macro headwinds seeing investors cut fewer checks and some reportedly renege on commitments, a slew of startups were forced to downsize, pivot, or in many cases, close up shop.

At least 15 African startups shuttered this year, including those with once highly-celebrated status on the continent: 54 Gene, Dash, Sendy, WhereIsMyTransport, Lazerpay, Zumi, Zazuu, Hytch, Okada Books, Pivo, Vibra, Redbird, Bundle Africa, Spire, Qefira.

Combined, these startups raised over $200m in disclosed VC funding while operational.

Meanwhile, others like Copia, MarketForce, and Twiga Foods have had to change the way they operate.

It’s noteworthy that the funding slowdown has hit a certain type of African startups hardest—well-funded ventures chasing growth-at-all-costs strategies.

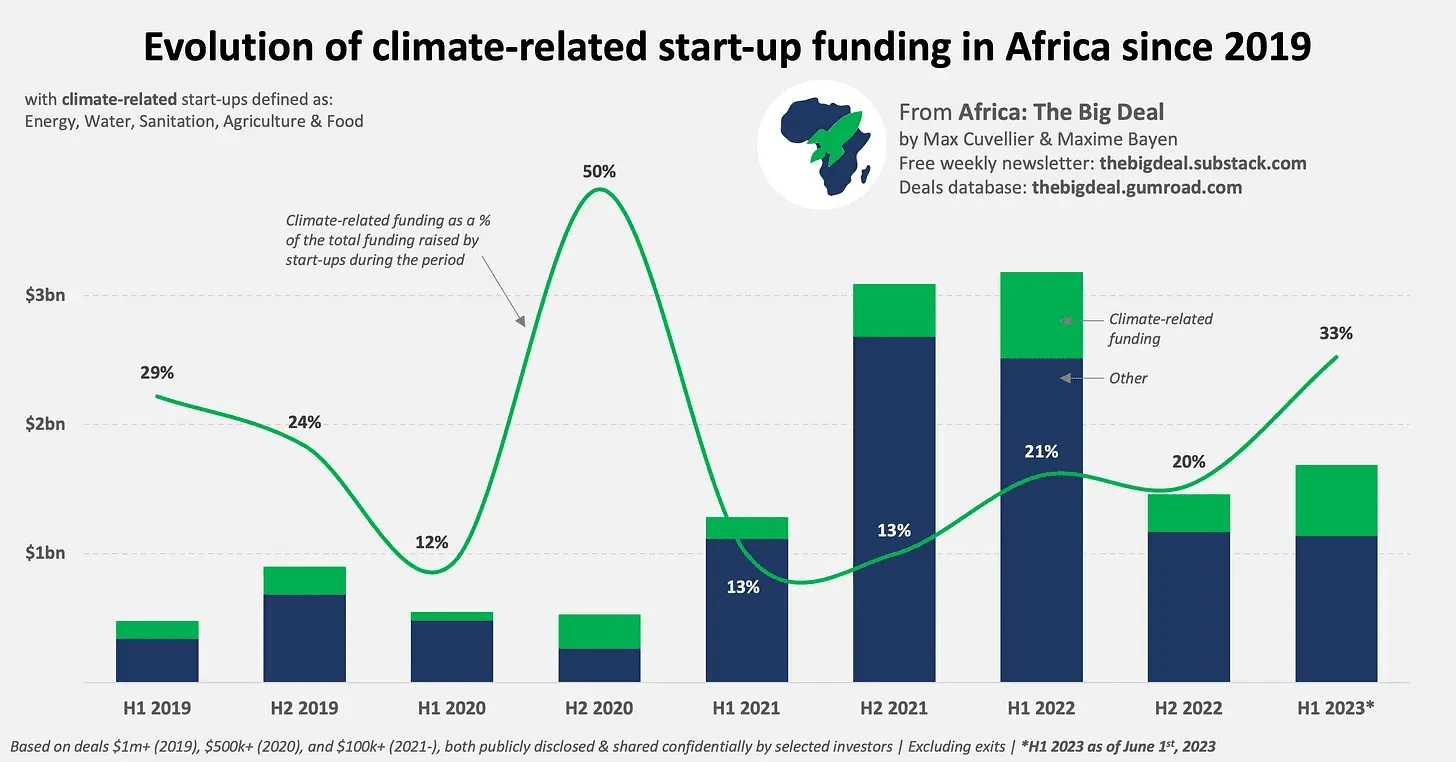

Cleantech/climate-tech now as popular as fintech

The tide is rising for climate tech (comprising innovations across agriculture, clean energy, sustainable materials, environmental sustainability, e-mobility, and nature-based solutions) in Africa.

Last year, funding to the sector grew 3.5 times to over $860m, making it Africa’s most funded after fintech.

It has maintained the second spot so far this year, per AVCA report. Data from Africa: The Big Deal shows the sector accounts for 32% of total VC funding as of Q3, behind fintech’s 35%.

And over the past 12-18 months, several VC firms—among them Satgana, Catalyst Fund, Equator, and EchoVC—have introduced funds to support startups in the sector.

The timing of this surge in climate funding couldn’t be better as Africa grapples with the increasingly severe impacts of climate change, we write in our Pulse54 newsletter, which explores climate tech in general and active players in the sector.

Spotlight on fraud & founder misconduct

Amidst the remarkable growth of Africa’s tech ecosystem, shadows loom over malpractices that impede the full potential and integrity of the continent’s startup landscape.

In 2023 alone, numerous unsettling reports emerged, depicting common themes such as financial misappropriation, deficient or corporate malfeasance, instances of sexual harassment, and the prevalence of toxic work cultures.

Startups like Ghana’s Dash and Float, Egypt’s Capiter, South Africa’s Springleap, and Nigeria-based companies such as PayDay, 54Gene, and Patricia were implicated.

More recently, Tingo was charged by the US SEC, accused of engaging in a “massive fraud” involving “billions of dollars of fictitious transactions,” all under the leadership of CEO Dozy Mmobuosi.

The lessons drawn from the challenges of 2023 underscore the critical need for regulatory clarity to eliminate grey areas in compliance.

Furthermore, investors must prioritize ensuring proper governance to safeguard the integrity of the African startup ecosystem.

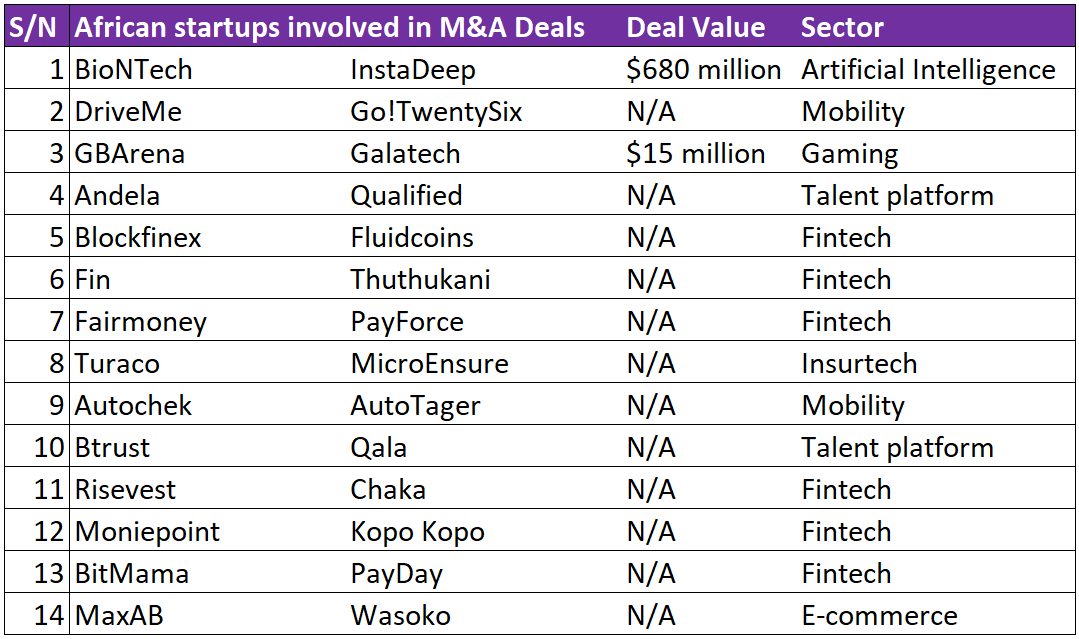

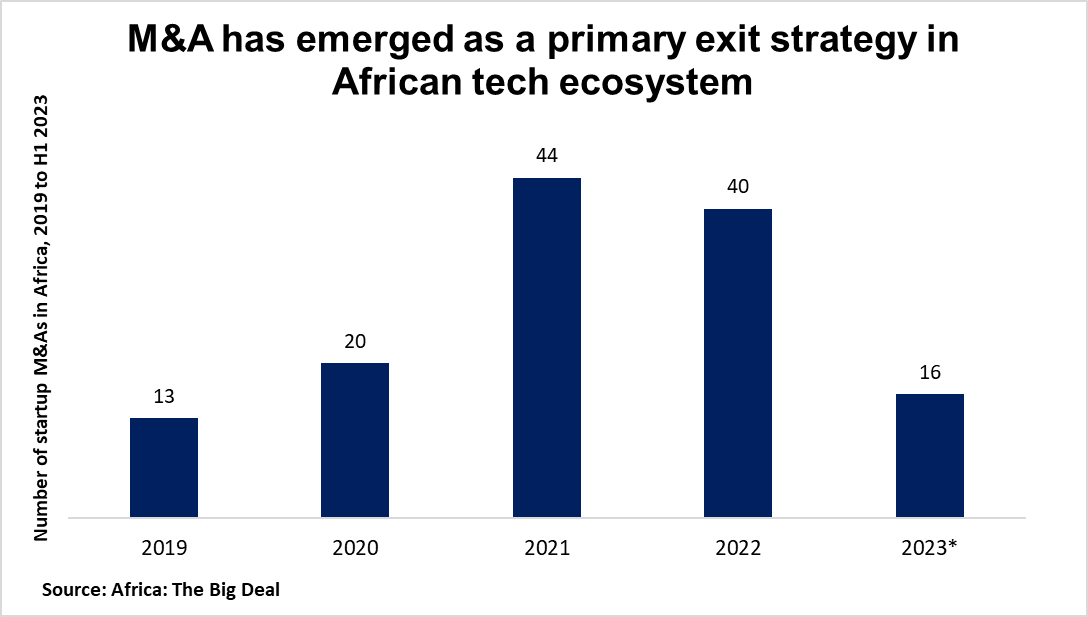

Mergers & acquisitions become a survival strategy

Mergers and acquisitions (M&A) have emerged as a primary exit strategy and, in the current depressed funding environment, a lifeline for African startup founders.

In Q1 2023 alone, seven M&A deals took place in the African startup ecosystem worth over $710m. Tunisia-based InstaDeep’s $682m acquisition in January by Germany’s BioNTech accounted for much of that.

By the end of the year’s first half, there had been at least 16 M&A deals per Big Deal data. About half of them reportedly involve struggling startups.

While this year’s total is likely to be some way off 2022’s 44 deals, one fact remains true: M&As have become a prominent feature of the African tech ecosystem.

Limited funds and the fragmented nature of the African tech market are major drivers.

The presence of numerous small and medium-sized companies across various regions and sectors makes consolidation through M&As a strategic move.

This approach creates larger, more diversified startups that can better compete globally and attract investment.

In addition, African startups are currently viewed as less liquid assets compared to other markets, primarily due to limited exit opportunities.

Thus, as the quest for a reliable path to liquidity in the African tech ecosystem grows, M&As become a viable option for venture capitalists and investors to explore.

Other noteworthy moments and highlights of the year

Starlink, a satellite internet service of Elon Musk-owned SpaceX, became operational in 6 African countries

And digital infrastructure, especially data centers, continues to draw the attention and backing of investors—from telco giants to private equity firms.

Closing Notes

As 2023 hurtles to a close, the question on everyone’s mind is will 2024 be better?

Perceptions of industry performance and expectations for the future vary.

In an era marked by growing concerns about environmental and social issues, sustainable investing has gained significant traction in the global investment community.

Investors worldwide are increasingly looking for opportunities to align their portfolios with their ethical values and contribute to a more sustainable future.

One instrument that has gained prominence in this regard is the social bond, which plays a pivotal role in sustainable investing.

Understanding Social Bonds: What are they?

Social bonds are a subset of sustainable bonds designed to raise capital for projects that have a positive impact on society.

These projects typically address critical social issues such as power/electricity, healthcare, education, affordable housing, and poverty alleviation.

The primary goal of social bonds is to channel funds towards initiatives that improve the well-being and quality of life for individuals and communities.

Unlike traditional bonds, which focus solely on financial returns, social bonds are characterized by their dual objectives of generating financial returns for investors while delivering measurable social benefits.

This makes them a powerful tool for investors who want to make a positive impact on society without sacrificing their financial goals.

Social bonds play a crucial role in sustainable investing for several reasons:

Measurable Impact: Social bonds require issuers to set specific social performance targets, ensuring that the funds raised are directed towards projects that can be quantifiably measured for their social impact. This transparency is a key factor for investors who want assurance that their money is making a real difference.

Diversification: Investing in social bonds allows investors to diversify their portfolios across different sectors and geographies. This diversification can help manage risk while still aligning with sustainability goals.

Market Growth: The market for social bonds has experienced significant growth in recent years. According to data from the International Finance Corporation (IFC), the market for social bonds reached $247 billion in 2020, a more than tenfold increase from 2016. This growth reflects the increasing demand for sustainable investment options.

Social Bonds in Developing Countries

Developing countries often face pressing socio-economic challenges, making social bonds particularly relevant in these regions. Here are a couple of real-life examples illustrating the impact of social bonds:

COVID-19 Response in Latin America: In 2020, the Inter-American Development Bank issued a sustainable development bond aimed at providing financial support to Latin American and Caribbean countries grappling with the COVID-19 pandemic. The bond raised $2 billion and supported healthcare infrastructure, social protection programs, and economic recovery efforts in the region.

Affordable Housing in India: India’s National Housing Bank issues bonds to fund affordable housing projects for low-income individuals and families. The bond not only attracted socially conscious investors but also contributed to addressing India’s housing shortage, a critical social issue.

Investors should consider social bonds for a variety of reasons:

Alignment with Values: Social bonds allow investors to align their investments with their social and environmental values, fostering a sense of purpose in their financial endeavors.

Risk Management: Diversifying into social bonds, like traditional ones, can help spread risk and potentially provide a cushion during equities market downturns.

Positive Impact: By investing in social bonds, individuals and institutions can directly contribute to projects that improve lives and communities.

Social bonds are a potent tool in sustainable investing, offering both financial returns and measurable social impact.

As the market for social bonds continues to grow, investors have the opportunity to make a difference while achieving their financial goals.

Whether it’s supporting healthcare initiatives in Latin America, electricity infrastructure in Cote d’Ivoire, or affordable housing in India, social bonds have the power to transform lives and build a more sustainable future.

Disclaimer:This material has been presented for informational and educational purposes only. The views expressed in the articles above are generalized and may not be appropriate for all investors. The information contained in this article should not be construed as, and may not be used in connection with, an offer to sell, or a solicitation of an offer to buy or hold, an interest in any security or investment product. There is no guarantee that past performance will recur or result in a positive outcome. Carefully consider your financial situation, including investment objective, time horizon, risk tolerance, and fees prior to making any investment decisions. No level of diversification or asset allocation can ensure profits or guarantee against losses. Articles do not reflect the views of DABA ADVISORS LLC and do not provide investment advice to Daba’s clients.