These rounds involve equity financing, where startups offer ownership stakes in exchange for capital, enabling them to scale, innovate, and compete.

Securing funding is a critical step for startups aiming to grow and achieve their business goals. Funding rounds—ranging from Series A to Series E—serve as milestones that reflect the maturity and strategic direction of a company.

These rounds involve equity financing, where startups offer ownership stakes in exchange for capital, enabling them to scale, innovate, and compete in their industries.

In this guide, we demystify the various series of funding and provide clarity on their purposes and nuances.

What is Series Funding?

Series funding refers to stages of investment, each corresponding to a specific phase in a startup’s growth journey.

Starting with seed funding, which helps a startup launch, subsequent rounds (Series A, B, C, and beyond) support scaling, market expansion, and product innovation. These funding rounds not only bring in necessary capital but also validate the startup’s business model and potential.

Pre-Seed and Seed Funding

Pre-seed funding represents the earliest stage of a startup’s journey, often coming from personal savings, friends, family, or angel investors. It helps lay the foundation for a business idea, allowing founders to conduct preliminary market research or develop prototypes.

Seed funding, the first formal equity round, aims to refine the business idea, build the product, and identify the target audience. It supports hiring a core team, developing the product, and initiating go-to-market strategies. Venture capital firms, angel investors, and startup accelerators often participate at this stage.

Series A is the first significant round after seed funding. Startups use this stage to refine their product, scale customer acquisition, and establish a solid business model. Investors look for startups with a proven product-market fit and a clear roadmap for scaling revenue.

Valuations for Series A companies typically range between $10 million and $15 million, and funding amounts vary from $2 million to $15 million or more, depending on industry and market conditions.

Notable players in this round include venture capital firms and sometimes institutional investors. The funds are often used to enhance marketing efforts, expand teams, and further product development.

Series B funding is focused on scaling operations and expanding market presence. At this stage, startups typically have a growing customer base, a refined product, and visible revenue streams. The funds help strengthen operational capabilities, expand into new markets, and build strategic partnerships.

Investors in Series B include existing backers and later-stage venture capital firms. The typical funding amount ranges from $10 million to $30 million, and valuations often fall between $30 million and $60 million.

Series C: Accelerating Expansion

By the time a startup reaches Series C, it is well-established, with significant revenues and market presence. Series C funding is used to scale globally, develop new products, acquire other companies, or enter new markets. It also often serves as a prelude to an IPO or acquisition.

Valuations at this stage typically exceed $100 million, and funding rounds may bring in tens or hundreds of millions of dollars. Investors in Series C often include hedge funds, private equity firms, and large institutional players.

Series D: Fine-Tuning Growth

Series D funding is less common but may occur if a startup needs additional capital for growth or repositioning before an IPO. It often involves complex negotiations and is used to address unmet milestones, support international expansion, or enhance product offerings.

Funding at this stage typically exceeds $100 million, and investors focus on opportunities for strong returns and a clear path to exit.

Series E and Beyond: Preparing for an IPO or Acquisition

Series E funding is rare and usually represents the final stage before going public or being acquired. It is used to stabilize finances, finalize preparations for an IPO, or pursue aggressive market expansion.

At this advanced stage, valuations and funding amounts are substantial, reflecting the company’s maturity and market position.

Key Differences Between Funding Rounds

The primary differences between funding rounds lie in their objectives and investor expectations:

Series A vs. Series B: Series A focuses on establishing a business model and early scaling, while Series B emphasizes scaling proven successes and operational expansion.

Series B vs. Series C: Series B is about scaling within established markets, whereas Series C aims for global expansion, acquisitions, and pre-IPO growth.

Series A vs. Series F: While Series A represents the first major funding round, Series F is an advanced stage often targeting final expansion or specific strategic goals.

Why the Naming Convention?

The naming convention—Series A, B, C, etc.—stems from the type of preferred stock issued during each round. It signifies the progression of a company’s growth and maturity.

The time between Series A and Series B varies but often spans 12 to 24 months. This gap allows startups to achieve the milestones necessary to secure the next round of funding.

Challenges and Risks

While funding rounds provide vital resources for growth, they also come with challenges, including ownership dilution, heightened expectations, and operational pressures. Each round demands a clear strategy, robust metrics, and investor confidence to succeed.

Conclusion

Series funding is a structured approach that aligns a startup’s capital needs with its growth trajectory. Each stage brings unique opportunities and challenges, enabling startups to transform ideas into scalable, sustainable businesses. Understanding these funding dynamics is essential for entrepreneurs seeking to navigate the complex world of startup investments.

Cette collaboration vise à rendre les opportunités d’investissement en Afrique accessibles aux investisseurs accrédités des États-Unis grâce à la plateforme innovante de Fundr.

Miami et New York, États-Unis – Daba, le principal fournisseur d’infrastructures d’investissement multi-actifs en Afrique, a annoncé aujourd’hui un partenariat stratégique avec Fundr, une plateforme d’investissement en startups basée aux États-Unis. Cette collaboration a pour objectif de rendre les opportunités d’investissement en Afrique accessibles aux investisseurs accrédités des États-Unis grâce à la plateforme innovante de Fundr.

Daba propose une gamme complète de produits d’investissement, notamment une application d’investissement pour les investisseurs individuels, des services institutionnels, ainsi que des API pour les entreprises technologiques souhaitant intégrer des produits d’épargne et d’investissement.

La plateforme de Fundr utilise des données et de l’intelligence artificielle pour optimiser la prise de décision, éliminer les biais et augmenter l’efficacité dans l’investissement en phase d’amorçage. Elle collabore avec des investisseurs de toutes tailles pour analyser les opportunités d’investissement, optimiser leur processus d’investissement et fournir des informations approfondies en temps réel sur leurs portefeuilles.

« Ce partenariat avec Fundr s’aligne parfaitement avec notre mission de démocratiser l’investissement en Afrique », a déclaré Boum III Jr, PDG et co-fondateur de Daba. « En tirant parti du réseau d’investisseurs de Fundr, nous pouvons connecter davantage de capitaux mondiaux aux opportunités passionnantes qui émergent à travers le continent africain. »

Lauren Washington, PDG de Fundr, a commenté : « Nous sommes ravis de nous associer à Daba pour offrir des opportunités d’investissement de haute qualité en Afrique sur notre plateforme. Cette collaboration offre à nos investisseurs un accès unique à l’un des marchés à la croissance la plus rapide au monde, diversifiant ainsi davantage leurs portefeuilles. »

L’écosystème du capital-risque en Afrique a connu une croissance remarquable ces dernières années. Selon les données disponibles, le financement du capital-risque en Afrique a augmenté de 1 597 % entre 2015 et 2023, passant de 277 millions de dollars à 4,7 milliards de dollars. Cette montée en flèche de l’activité d’investissement reflète la scène florissante des startups technologiques sur le continent, stimulée par une population jeune et technophile ainsi que par une pénétration croissante des smartphones.

Le dividende démographique de l’Afrique et sa transformation numérique rapide présentent un cas d’investissement convaincant. Avec plus de 60 % de sa population âgée de moins de 25 ans et un nombre d’utilisateurs d’Internet mobile qui devrait atteindre 475 millions d’ici 2025, le continent est prêt pour une innovation continue et une croissance soutenue. Des secteurs tels que la fintech, le commerce électronique et les technologies propres sont particulièrement attractifs, offrant des solutions aux défis locaux et des opportunités de développement à travers les frontières.

Daba et Fundr s’engagent à assurer un processus d’intégration fluide et à fournir un support complet aux investisseurs intéressés par l’exploration de ces nouvelles opportunités. Au fur et à mesure que le partenariat se développe, les deux entreprises prévoient d’organiser des webinaires et des événements communs pour informer les investisseurs sur le marché africain et présenter des startups prometteuses de tout le continent.

À propos de Daba

Fondée en 2021, Daba est la principale plateforme d’investissement et de financement multi-actifs en Afrique. La société se consacre à libérer tout le potentiel d’investissement du continent en offrant une plateforme unifiée permettant aux particuliers et aux institutions d’accéder à des opportunités d’investissement de haute qualité sur les marchés africains.

À propos de Fundr

Fundr est une plateforme d’investissement en startups basée aux États-Unis qui simplifie le processus d’investissement dans les entreprises en phase de démarrage. Grâce à son algorithme intelligent et à ses processus rationalisés, Fundr offre aux investisseurs une diversification instantanée, un accès à des startups sélectionnées et des outils efficaces de gestion de portefeuille.

This collaboration aims to make African investment opportunities accessible to accredited US investors through Fundr’s innovative platform.

Miami and New York, USA – Daba, Africa’s premier multi-asset investment infrastructure provider, today announced a strategic partnership with Fundr, a leading US-based startup investment platform. This collaboration aims to make African investment opportunities accessible to accredited US investors through Fundr’s innovative platform.

Daba offers a comprehensive suite of investment products, including a real investing app for individual investors, institutional services, and APIs for tech companies to integrate savings and investing products.

Fundr’s platform uses data and AI to empower decision-making, remove bias, and increase efficiency in seed investing. It works with investors of all sizes to analyze investment opportunities, optimize their investment process, and provide real-time deep insights into their portfolios.

“This partnership with Fundr aligns perfectly with our mission to democratize investing in Africa,” said Boum III Jr, CEO & Co-founder of Daba. “By leveraging Fundr’s investor network, we can connect more global capital to the exciting opportunities emerging across the African continent.”

Lauren Washington, CEO of Fundr, commented, “We’re thrilled to partner with Daba to bring high-quality African investment opportunities to our platform. This collaboration offers our investors unique access to one of the world’s fastest-growing markets, further diversifying their portfolios.”

The African venture capital ecosystem has seen remarkable growth in recent years. According to available data, venture capital funding in Africa has seen a remarkable surge in recent years, growing by 1,597% from $277 million in 2015 to $4.7 billion in 2023. This surge in investment activity reflects the continent’s burgeoning tech startup scene, driven by a young, tech-savvy population and increasing smartphone penetration.

Africa’s demographic dividend and rapid digital transformation present a compelling investment case. With over 60% of its population under the age of 25 and mobile internet users expected to reach 475 million by 2025, the continent is poised for continued innovation and growth. Sectors such as fintech, e-commerce, and cleantech are particularly attractive, offering solutions to local challenges and opportunities for scaling across borders.

Daba and Fundr are committed to ensuring a smooth integration process and providing comprehensive support to investors interested in exploring these new opportunities. As the partnership develops, both companies plan to host joint webinars and events to educate investors about the African market and showcase promising startups from across the continent.

About Daba

Established in 2021, Daba is Africa’s leading multi-asset investment and financing platform. The company is dedicated to unlocking the continent’s full investment potential by providing a unified platform for individuals and institutions to access high-quality investment opportunities across African markets.

About Fundr

Fundr is a US-based startup investment platform that simplifies the process of investing in early-stage companies. Through its smart algorithm and streamlined processes, Fundr offers investors instant diversification, access to vetted startups, and efficient portfolio management tools.

I have long been a fan of DFS Lab, the “research-driven venture capital in Africa”.

It’s the only VC firm on the continent that consistently shares – publicly and transparently – nuanced, long-form reflections around its investment thesis.

By doing that, they gifted the ecosystem not just with high-quality articles, but new terms/concepts to describe & make sense of tech in Africa.

Kudos to them! 💥

In a world defined by information overload and sensationalism, mental clarity is one of the most underrated qualities we should consciously strive to cultivate.

How do you know what you know? What is the deep meaning of it? If you cut through the noise, what do you see?

Trying to answer these questions – peeling all the layers of opaqueness – most people would find themselves naked.

This is why, drawing inspiration from the Almanack of Naval Ravikant, I am happy to propose – for the first time – the Almanack of DFS Lab: 6 theoretical primitives to make sense of VC investing in Africa.

These are six concepts coined by the firm that I find extremely insightful/useful in my activities as a researcher/investor:

The Frontier Blindspot

Fortune at the middle of the pyramid

The B-side of African Tech

Cyborgs vs Androids

Invested infrastructure

African S-curves

The original articles are all available on the DFS Lab website and Medium page.

My contribution mainly consists of summarizing my understanding of them & complementing them with my own ideas.

Lessgò.

Subscribe

1) The Frontier Blindspot 👀

Premise: The world has developed “intuitions about how technology markets are structured and what successful technology companies look like”. Cool.

However: this learning process took place strictly in the context of Western economies.

Ergo: the same frameworks do not always apply to frontier markets (like Africa).

Thesis: the disconnect between how we think tech is supposed to work versus how it really works – in Africa & other frontier markets – is the Frontier Blindspot! 💥

It is a blindspot because we are partially clueless – how tech markets work or don’t work in Africa has yet to be demonstrated. As we cannot copy-paste, learning happens by trial and error, thorough research, and on-the-ground experience.

What type of bias did we borrow from the Global North when making our assumptions about tech in Africa?

we overestimated the pace of digitalization;

we underestimated the strength of informal markets;

we overlooked the state of infrastructure and consumer purchasing power

When you factor in low-paced digitalization, strong informal markets, and quirky infra, you’ll see that a lot of common startup wisdom about business models, distribution strategies, and growth projections, won’t apply to the continent.

However, local entrepreneurs are still finding unique ways to apply the “modern startup stack” to the specifics of the African environment.

This is where the real opportunities are, and the areas of excitement include:

Physical logistics

SME solution stack

Financial building blocks

Agent networks

Although these things may seem obvious today, I think they are still not obvious to many, and they certainly were not obvious in 2020 (when the article came out).

What I find particularly useful about this piece is stressing the differences in infrastructure and purchasing power. When looking at pitch decks, I try stress the following questions:

what needs to be there for your product to be made, consumed, or delivered? (read: infrastructure)

How many people can buy your product, regularly? How do you know it?

We are about to have a taste of it with the next concept ✨

Who is the African consumer & what is the real size of the African market for digital products?

Hashtag: debunking the (once) popular tag “Nigeria is a market of 200M people” with some rigorous thinking.

Why?

Because population size does not equal market size, we cannot boast “the youngest population in the world” without looking at income brackets too.

Let’s proceed in order.

“Most B2C tech startups are seeking to make money from people’s discretionary spending”

Discretionary spending is the spending power that remains once covered for necessities like food, clothing, and shelter.

The question asked is: among the 200M fellow Nigerians, how many have the discretionary spending for my type of product?

In the image below, we can look at income levels and their percentage of discretionary income (in Africa).

Source: Fortune at the middle of the pyramid

If you are a B2C startup, what is the juiciest segment?

As a fairly coherent group, the people earning between $5-$10 – while comprising only ~10% of the population – have one of the highest discretionary spending power combined.

This is the fortune at the middle of the pyramid: the segment having enough people, with enough discretionary spending power. To the left of the curve, there are a lot of people but with little money; to the right, they have a lot of money but they are too few.

Now, speaking of unit economics: how much does it cost to acquire these customers? Here things get trickier.

In Africa, higher incomes are usually digitally-fluent city dwellers. Their geographical concentration, professional status, and greater online life, make them perfect targets for digital acquisition strategies. The same doesn’t necessarily hold for lower-income prospects: acquiring them is harder and costs more (with traditional digital methods).

To this comes a paradox: if the cost of acquiring a new customer is way more than what you earn from them, you will soon move to serve higher-income consumers. However, if you only serve the +10$ income bracket, at some point, growth will stall and you’ll need to move cross-border (not easy).

What can we learn from all we just stayed?

purely consumer-focused apps that do not focus on necessities (read: targeting discretionary spending) face unique challenges with monetization in Africa. This is because

the largest economic opportunity sits within the 5-10$ bracket, but the cost of acquiring them is high due to lower digital presence.

Moving forward, I think two very important corollaries emerge about “how to be successful”:

build apps focused on necessities, or focused on the business equivalent of “necessities” (restocking, working capital, inventory etc..);

if you target consumers’ discretionary spending, invest in human agent networks, the physical point of entry to most digital experiences for middle-of-the-pyramid Africans.

Personally, whenever I look at the pitch deck of a B2C company:

if they target offline acquisition, it means they are serving the middle of the pyramid;

if they don’t mention offline acquisition, it means they are serving the top of the pyramid.

Hence, I’ll start to wonder. Given the risk and the complexities of moving cross-border, can they make money (read: positive operating profit) before moving cross-border?

Enjoying the article so far? Share it with bruvs and siss 💥

This article draws inspiration from Wang Huiwen, the co-founder of Meituan Dianping, the most successful Chinese food delivery company, turned super-app.

In an issue of the newsletter “The China Playbook”, Huiwen defines the internet industry as made of two sides:

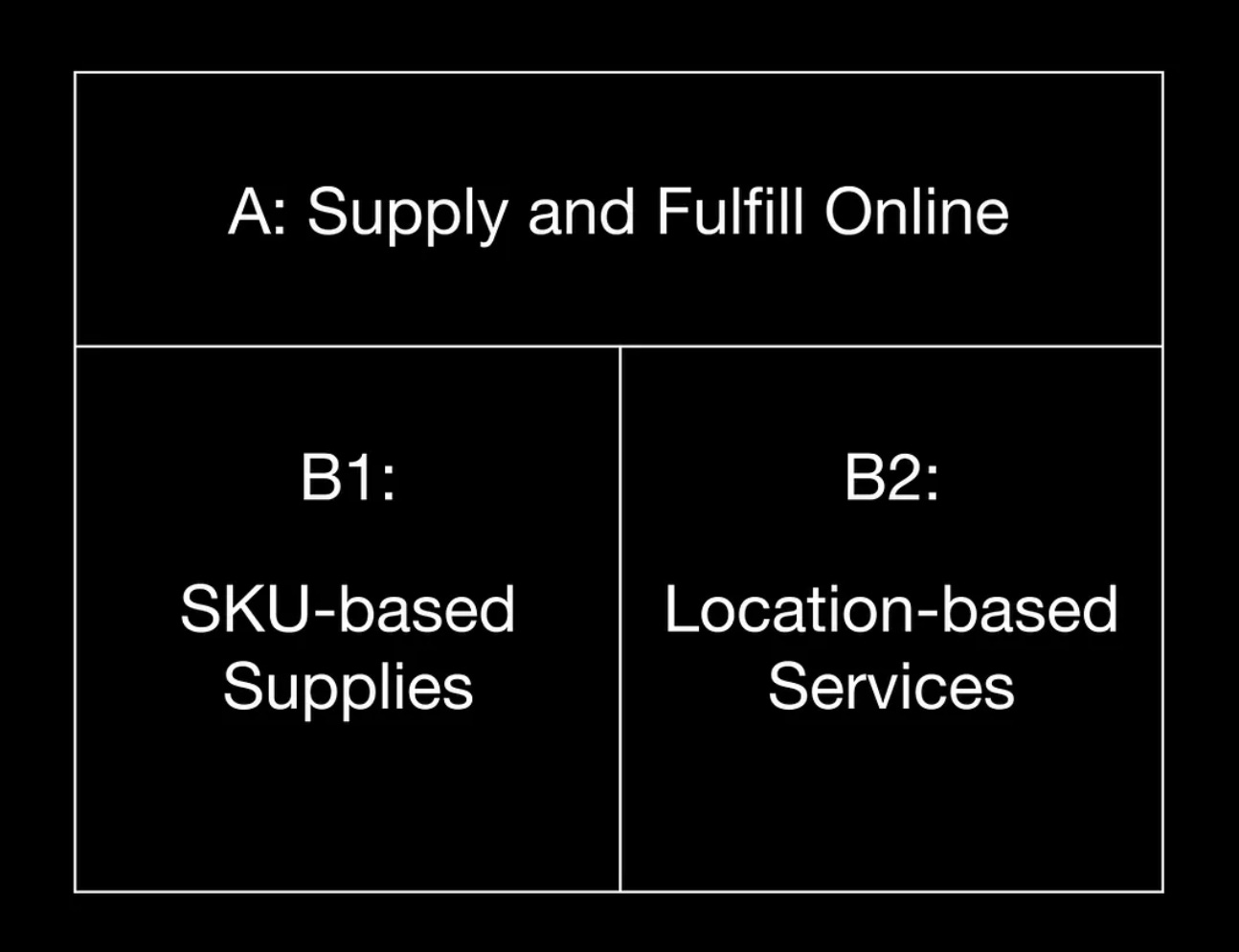

A-side: Supply and Fulfill Online

B-Side: Supply and Fulfill Offline

Side-A is products and services that are “pure internet”, as they can be delivered and consumed entirely online. SaaS (Salesforce), video-games (Voodoo), streaming (Spotify), etc…

Side-B is products and services that are delivered offline and consumed offline. Think of retail (Amazon), mobility (Uber), ticketing (Ticketmaster), etc…

If we have to apply this distinction to African economies, we would see that side-A (online utility) is smaller, compared to side B (offline utility).

The reason is that “fully digital experiences are either inaccessible, unaffordable or don’t cover the primary consumption needs for those in the bottom 95%.”

Ok cool. Let’s have a closer look at the B-side then. The B-side can be further divided into two sub-sections:

B1: SKU-based supplies

B2: location-based services

B1 is companies like Wasoko, Omniretail, and other traditional marketplaces. As digital businesses positioning in between the sourcing & delivery of physical products, their core competencies lie in ”understanding SKUs (stock keeping unit), understanding the supply chain, and understanding pricing”.

B2 is companies like Hubtel and Wahu Mobility. They are location-centric, as the physical location of customers & partners is a key element of their value proposition. For example, a ride-hailing company like Uber will need to recruit drivers in your city and ensure there are enough in your area as you order a ride – otherwise, you won’t be able to access their service. B2 businesses demand a larger offline team to manage operations closer to the customers.

What learnings do we have here?

B1 leverages technology to “improve the efficiency of existing value flows and reorganize pricing power”. On the contrary, “B2 is physical ubiquity”.

Let’s stop here.

In the article, Stephen Deng (DFS Lab MP) expands on the original concept expressed by Meituan Dianping founder.

When Wang Huiwen talks about B2 “location-based businesses”, he is primarily referring to ride-hailing, bike-sharing, and food-delivery, products made accessible by smartphone proliferation, which unlocked & democratized location data. These businesses are useful because you can see your location with your phone, and other people can see it too.

Deng however, twists its meaning for the African context, attaching to it the familiar notion of physical ubiquity: B2 businesses are interesting because of their physical proximity to the customers, mobilizing people and resources last-mile. Other than delivery, one can think of mobile money agents and social commerce as a form of B2 businesses. Their utility comes from their ability to integrate kiosks and people from your neighborhood in their business model. They are relatable, they are next door.

In short, they are more similar to Cyborgs, instead of Androids. What?

You read correctly. The concept of “B-Side of African Tech” is strictly intertwined with that of “Androids vs Cyborgs”, that we explore in the next section (before wrapping up with my two cents on this stuff).

Androids: solutions that replace informal markets with digital, formalized parts and processes

Cyborgs: solutions that enhance informal markets by arming them with digital, formalized parts and processes

Androids use tech to replace a set of existing actors.

Cyborgs use tech to improve the work of a set of existing actors.

Stephen Deng claims that we cannot brute force androids into existence if we are incapable of replacing informal players with significantly better solutions. And if we can’t replace them, we’d better empower them by building cyborgs.

It might seem like a B2C (Android) vs B2B (Cyborgs) play, but it’s more nuanced than that. Examples?

The ultimate Android example is Jumia and all Amazon-inspired B2C marketplaces: “replacing the local market with an online option that is meant to be more convenient, have more options, and is fully digitized”.

However, I think the same holds for many agri-tech platforms (like Complete Farmer or Winich Farms) that aggregate farmers’ produce and facilitate access to market & agro-inputs. In almost every pitch deck you will read about them “cutting out the middlemen”, the set of informal buyers and sellers who move crops to markets, whose commissions eat out farmers’ margins and drive inefficiencies (btw these platforms raised a lot of funds, but it’s not clear to me how much money they are making).

Cyborgs, on the contrary, look like tools that empower small businesses, applying a mix of online and offline. Instead of replacing existing relationships, they “supercharge them with digital optionality when the need arises”.

Both B2-side businesses and Cyborgs, tell the same story: existing structures can be valuable when they are empowered, instead of substituted.

Ok, but empowered how?

In my opinion, an online-offline Cyborg approach, can only be one of two things:

cost-effective offline distribution and/or marketing – agents knocking on doors or setting up shops;

tech-enabled intermediaries/retailers – empowered by a digital backend or specialized hardware.

That’s it!

Moniepoint is Africa’s fastest-growing fintech. Its distribution model? An army of human agents armed with PoS devices, knocking on merchants’ doors. The company revolutionized the capacity for Nigerian businesses to collect digital payments.

→ a Cyborg approach to digital payments.

Retailers’ bookkeeping apps like Oze and supply-chain management tools like Jetstream, both started as digital super-charger of African businesses: I give you tools to better manage invoices and logistics. Fast forward a couple of years, and they both ended up embedding credit and solving the pain of access to capital.

→ a Cyborg approach to digital lending.

I think Cyborg either means giving more “legs and arms” for asset-light digital businesses, or making “legs and arms” (SMBs) more competitive with digital tools.

Digital solution → leave a digital trace → data + learning models → better decision making

Digital solution → relational database & data integration → operational efficiencies

Digital solution → composable software stack → APIs & integrations → new products/services delivered on top of the main product

🪄🪄🪄

More in general, I think that both the “B-Side” and “Android vs Cyborg” arguments tend to over-emphasize the promises of the physical ubiquitous approach, without addressing the elephant in the room: we need more hardware.

A lot of things can be done with your phone, but not everything can be done with your phone, and sometimes, a phone is too much.

Limited storage/memory, weak bandwidth, and high data costs still represent hard limits to app utility for the average African business operator. A phone can do a lot, but not everything.

Safiri is a Tanzanian company equipping bus companies with thermal printers, and customers with digital ticket purchase options. They record transactions “digitally”, and print tickets “physically”. A good blend of digital and physical coming together. No need for Industry 4.0 here, just basic hardware tools.

And yet, I am not seeing enough investors stressing how specialized hardware – as well as consumer hardware – can play its role in the tech landscape.

We need more hardware. We can’t expect to revolutionize the continent simply with apps running on cheap smartphones.

I feel we’ll see major shifts when large-scale hardware manufacturing that truly responds to local business needs comes to fruition.

And yes, somehow, I am still convinced this can be a VC play.

Enjoying the article so far? Subscribe to Data Bites & have more of this 💩Subscribe

The concept is simple, yet powerful: the infrastructure built in the past has a lasting, indelible influence on our present & future.

Economists call it “path dependency”: society builds on top of what has been built, and this process makes us drift toward a trajectory of development and away from others.

In the United States, payment infrastructure has been built “for a time when phones were not as ubiquitous and hard-wired ethernet was increasingly common.”

The proliferation of PoS devices & phone cables (& later fiber cables), gradually made up the physical network on top of which credit cards’ adoption became widespread.

The alternative to cash travels on rails that took a long time to build, but once in place, it is hard to replace. It’s the hidden cost of path dependency: the more we build on top of invested infrastructure, the higher the switching costs to a different system.

“They have since gained ubiquity, and because mobile phone-based services can only offer marginal improvements, the system stays resilient — it is challenging to overcome the inertia of this invested infrastructure”

What is the invested infrastructure in Africa and how will it impact its future?

It is an important question to ask because – as we have seen – companies that leverage invested infrastructure can have a competitive edge, reducing costs and frictions to adoption; those that try to replace it might sink under the weight of high switching costs & behavioral change (although in some cases – boom jackpot 🎰).

If we think of financial infrastructure, in Africa the equivalent of the US card network is a combination of:

a human agent network

phones & SIM cards

tower cells

It hasn’t always been the case. The capillary presence established by telco companies in the continent from the 90s onward, brought along the way important infrastructural development that served as the launchpad to mobile money: financial infrastructure borrowed from the already existing communication infrastructure.

A human agent network could now be used to on-ramp/off-ramp physical cash.

Phones and SIM cards became wallets.

Tower cells relayed information – and now value – across long distances.

Innovation on top of invested infrastructure.

But it’s not over.

As the new payments infrastructure emerged, further developments “up the ladder” could see the light of day: “The combination of USSD-based mobile accounts that worked on every phone and cash-in/cash-out agents in nearly every neighborhood and village proved to be powerful infrastructure on which to build new product offerings”.

The first wave of successful tech businesses on the continent – real “market-creating” innovations – are the product of it.

Examples:

First generation: pay-as-you-go solar (like M-Kopa)

Second generation: digital lending

Access to energy & access to credit. Both are built on top of mobile money infrastructure, built on top of telco’s invested infrastructure.

What lessons can we take home from this chapter?

invested infrastructure matters

it looks different in Africa than in other places

opportunities exist for those who build on top of it + those who make it more efficient

Personally, I find myself asking the question” What’s the invested infrastructure here?”. And not just for payments, but for commerce, logistics, agriculture etc.. In short, it translates to: how things are done now, how much does it cost to switch and who has interest in doing it?

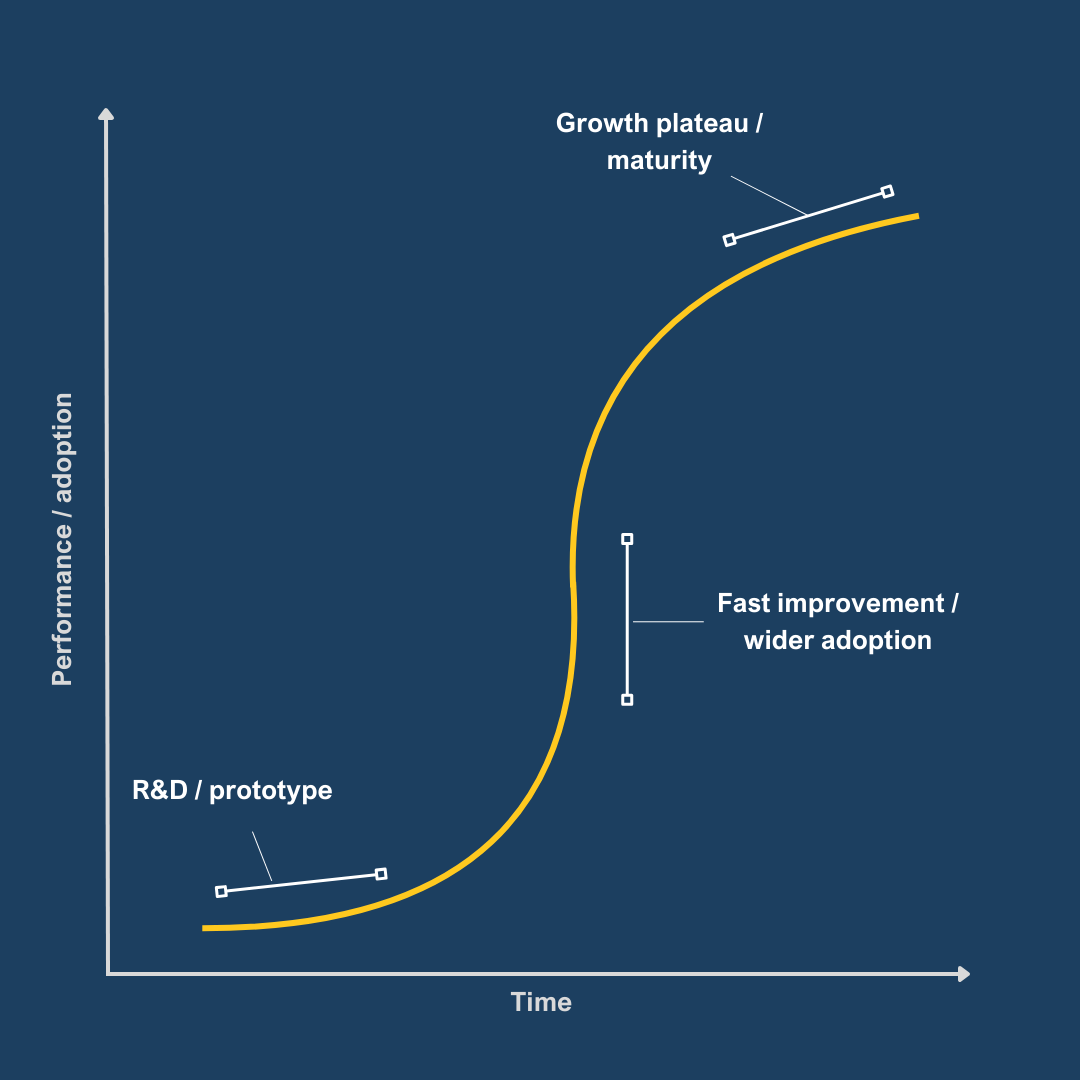

S-curves describe the performance of a new technology – or a technological toolset – over time.

In the beginning, during the R&D and prototyping phase, adoption is minimal and the potential of tech still needs to be validated. The curve is flat and growing slowly. Think of electric cars 15 years ago. It is the territory of university budgets, public finance, and research grants.

When the tech starts showing signs of improvement, it is followed by a steep acceleration in performance and increased adoption. Think of Generative AI one year ago. It is the land of VCs, profiting “by investing in emerging tech before it’s mainstream and exiting when growth plateaus”.

Finally, when a technology is mature, adoption widespread and there is little room for marginal improvements: the tail of the curve flattens. It is the PE and stock market game.

And then, onto the next technology, that will replace the incumbent with the next S-curve. Venture capital funding follows the S-curves cycle, the peak funding being when the curve is at its highest steep.

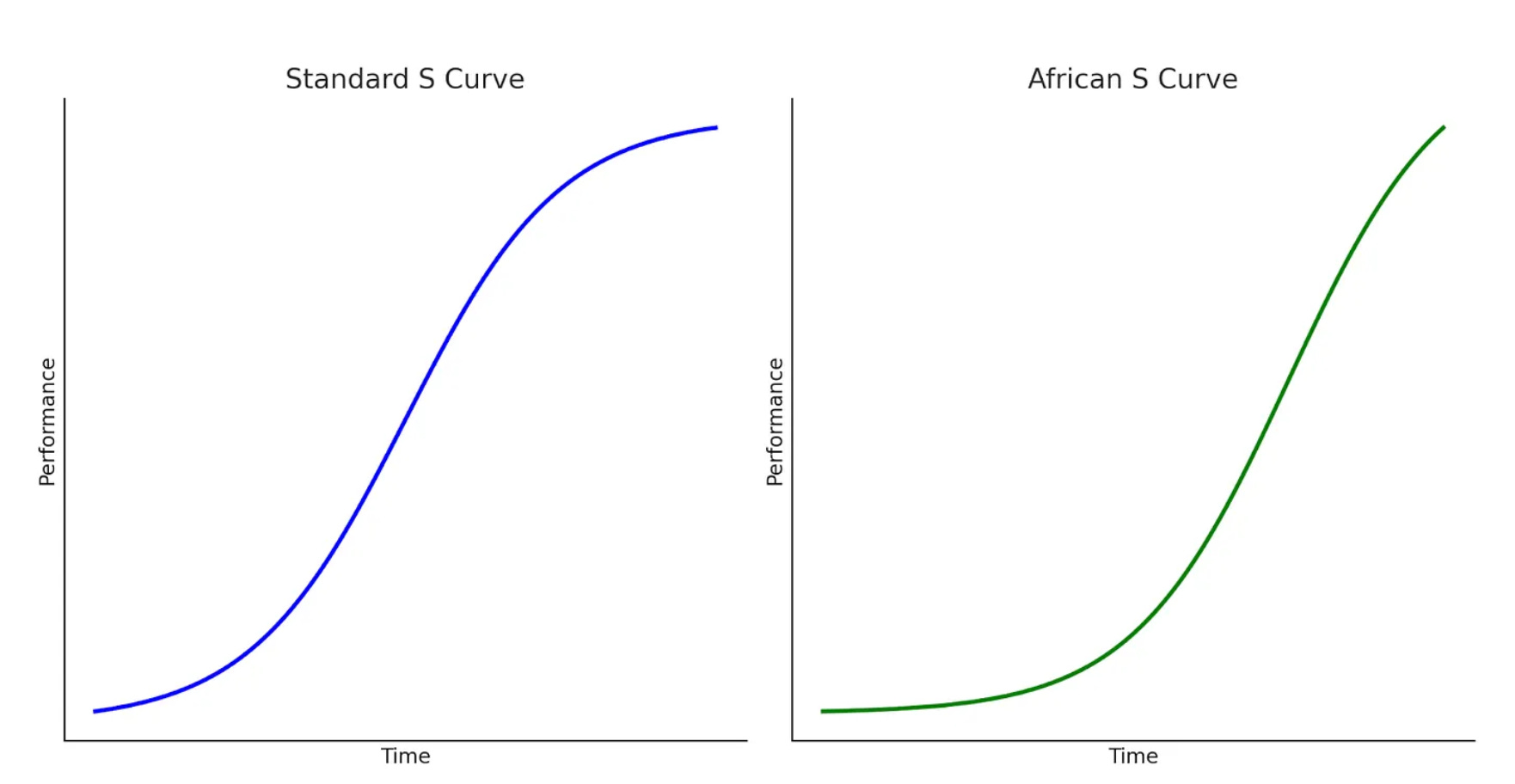

Now: in the wake of funding drought, startup bankruptcies, and crowding away of international investors, what can we say about the shape of the African S-curve?

One: African S curves have much longer tails.

This means that it takes more time for tech in Africa to see widespread adoption. Rather than a limit to technology performance, the problem lies in the lack of market readiness.

Read: “Customers don’t need new tech, or don’t trust new tech, or can’t afford new tech, or don’t have access to infrastructure for new tech, or don’t believe new tech provides enough value vs. old tech”

Two: African S curves have much steeper slopes

On the contrary, once adoption kicks in, the potential for improvements in technology can last for a very long time, going beyond what was once imagined.

The acceleration phase lasts a long time along with its benefits.

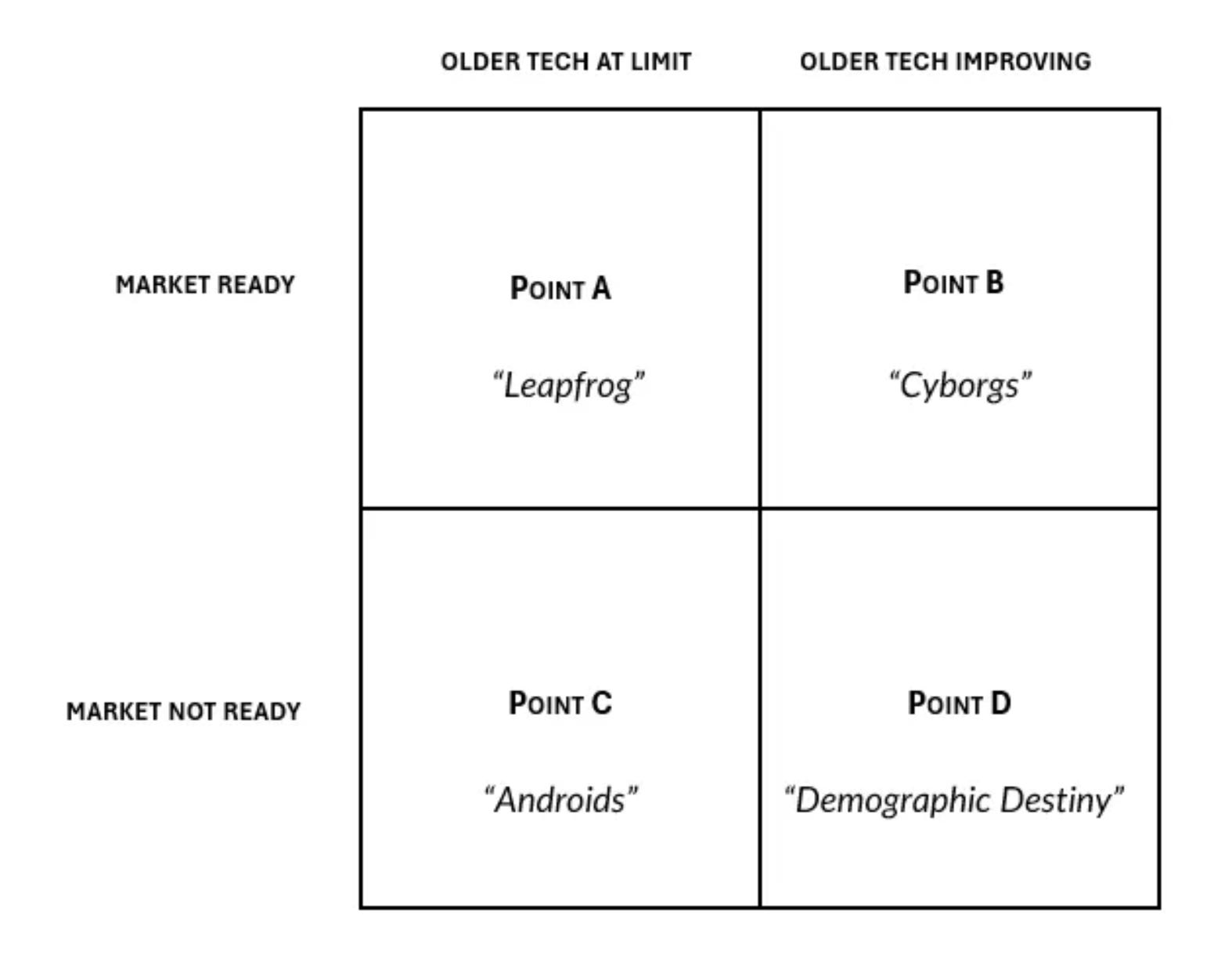

How do we change from one S-curve to the other? When will the new tech replace the old one?

There are 4 different scenarios.

If the old tech is not improving, and the market is ready for a novel solutions, then we’ll have a quick transition. This means heading towards Point A, and what people cheer as Africa’s technology leapfrog.

On the opposite side, if incumbents are delivering increasingly better utility to consumers, who are not ready to change for newcomers, then we’ll have a very gradual and slow transition. Ergo, heading towards Point D.

Many people either bought the point A narrative (technology leapfrog), or buys into point C one. They think old tech is crap, inefficient, and not making any progress. However, the market is not ready for new digital solutions yet. It’s a matter of time.

Stephen Deng, on the contrary, thinks we are heading towards point B. A situation where yes, the market is not ready, but the old tech – and the ecosystem around it – is still improving.

Think of mobile money. It is a fairly old technology ( and USSD codes), but it can still deliver innovation to its users. Telcos are blending digital offerings into their core model; traditional financial services are integrating with the mobile money ecosystem for seamless interactions; new products are developed on top of it every month.

If MoMo is the old tech, the new tech would be close to neo-banks like Djamo. How many customers does one have vs the other?

The shelf life of telecommunications technology has been pretty long. No surprise than that the true champions of tech in the continent are telcos. Companies like MTN, Airtel, Safaricom. This is in stark contrast with the Google, the Meta and the Microsoft of North America.

The main argument is the following: from now on, until we reach point B, a lot of incremental innovations will be built around the existing tech. We need to surf it 🏄🏽♂️

It is what Deng calls the “cybernetic commerce” area, yet another version of the Cyborg thesis.

The most interesting element of this article, to me, is the mental framework that comes with it: how many incremental innovations can still be built on top of the existing rails?

When you look at African markets overall, you’ll see that a lot of problems can be solved with existing technologies. There is no need for a breakthrough.

How to deliver the benefits of tech without losing money: this is the number one skill a founder must have.

This is the end, my friends. I hope you enjoyed the read. Writing this piece I’ve noticed that – as telcos in Africa – my essays have room for improvement. In particular, from now on I will try to deliver:

more real-life examples (what companies, what products etc…) → it helps with mental clarity when you have more than 1/2 examples

more exit simulations (revenues, potential returns) → VC exists where outsized returns exist, and we need to be more rigorous on that.

Contributed by Ajibola Awojobi, founder and CEO of BorderPal.

As the sun rises over Lagos, Adebayo, a young Nigerian fintech entrepreneur, stares at his computer screen. His brow furrowed in concentration and his startup, a mobile money platform to bring financial services to the unbanked, has just secured significant funding from a Silicon Valley venture capital firm. It should be a moment of triumph, but Adebayo feels a gnawing sense of unease. The numbers on his screen tell a troubling story: his company is spending $20 to acquire each new customer, yet the average revenue per user is a mere $7.

Adebayo’s predicament is not unique. Across Africa, fintech startups are grappling with a challenging reality: the cost of customer acquisition often far outweighs the immediate returns. This scenario raises a critical question: Is Africa’s venture capital-backed fintech model sustainable or fundamentally broken?

VCs and the Promise of African Fintech

The African continent has long been considered the next frontier for fintech innovation. With a large unbanked population and rapidly increasing mobile phone penetration, the potential for transformative financial services seemed boundless. Venture capitalists, enticed by the prospect of tapping into a market of over a billion people—half without any formal bank account—have poured billions of dollars into African fintech startups over the past decade.

These investments have fueled remarkable innovations. From mobile money platforms that allow users to send and receive funds with a simple text message, to AI-powered credit scoring systems that enable microloans for small businesses, African fintechs have been at the forefront of financial inclusion efforts.

However, as Adebayo’s experience illustrates, translating these innovations into sustainable businesses has proven to be a formidable challenge.

While Adebayo grapples with his early-stage startup’s challenges, a major African fintech player with a customer base of 300,000 users has just raised a mammoth $150 million, which brings its total funding to nearly $600 million. Based on a customer acquisition cost and revenue per customer established earlier, the economics of this deal seem precarious at best. A quick calculation reveals that the company would have spent around $6 million just to acquire its current user base while generating only $2.1 million. The funding, while impressive, thus raises serious questions about the sustainability of this model and the investors’ expectations.

These scenarios serve as a stark illustration of the broader challenges facing the African fintech sector. It highlights the disconnect between the vast sums of venture capital flowing into the industry and the on-the-ground realities of customer acquisition and revenue generation. For a company to justify such a massive investment, it would need to dramatically increase its user base, significantly reduce its customer acquisition costs, or find ways to generate substantially more revenue per user. Achieving any one of these goals in the complex African market is a tall order; achieving all three simultaneously is unarguably a Herculean task.

The funding also underscores the potential for overvaluation in the African fintech space. While such large investments can provide companies with the runway needed to scale and innovate, they also create immense pressure to deliver returns that may not be realistic given the current state of the market. This pressure could lead to unsustainable growth strategies, prioritizing user acquisition over building a solid economic foundation.

Balancing Profitability & Cost of Growth

The core of the problem lies in the high cost of customer acquisition. According to a McKinsey analysis, some fintech companies in Africa spend up to $20 to onboard a single customer, only to generate $7 in revenue from that customer. This imbalance is staggering and points to deeper structural issues in the market.

Several factors contribute to these high acquisition costs. First, there’s the challenge of digital literacy. Many potential customers, particularly those in rural areas, are unfamiliar with digital financial services. This necessitates extensive education and handholding, driving up the cost of onboarding.

Secondly, Africa’s diverse linguistic and cultural landscape requires tailored marketing approaches for different regions. A strategy that works in urban Lagos may fall flat in rural Tanzania, forcing companies to invest heavily in localized marketing efforts.

Infrastructure challenges also play a significant role. The lack of robust digital infrastructure in many African countries is partly responsible for the high customer acquisition costs. Poor internet connectivity, limited smartphone penetration, and unreliable power supply in some areas make digital onboarding processes more difficult and expensive. Moreover, many consumers are wary of new financial services, requiring significant investments in building trust and credibility.

The high customer acquisition costs are reflected in the overall profitability of digital banks globally. A BCG Consulting analysis revealed that only 13 out of 249 digital banks worldwide, or 5%, are profitable, with 10 of those firms being in the Asia Pacific region. This statistic underscores the challenges digital banks face, particularly in emerging markets like Africa.

This reality presents a conundrum for venture capital firms accustomed to the rapid scaling and quick returns seen in other tech sectors. The traditional VC model, focusing on exponential growth and relatively short investment horizons, may not be well-suited to the realities of building sustainable financial services in Africa.

Rethinking the Model

As awareness of these challenges grows, both entrepreneurs and investors need to rethink their approaches to fintech in Africa, taking into consideration the high cost of acquiring customers and the state of the continent’s digital infrastructure.

One promising avenue is the development of white-label infrastructure. By creating common technological solutions that can be customized and branded by different companies, fintechs can significantly reduce their development costs. This approach could be particularly effective for services like Know Your Customer (KYC) systems or payment processing platforms.

Taking the white-label concept further, an innovative solution is emerging: white-labeled services provided by community leaders with large networks in rural settings. This approach could help fintechs lower the cost of building their customer base. By leveraging the trust and influence of local leaders, companies can reduce the cost of onboarding and education. Word of mouth spreads faster in close-knit communities, potentially accelerating adoption rates and lowering acquisition costs.

Partnerships with established institutions are another strategy gaining traction. By collaborating with banks, telecom companies, or large retailers, fintech startups can leverage existing customer bases and distribution networks, potentially lowering acquisition costs.

Some companies are shifting their focus from B2C to B2B services. Targeting businesses rather than individual consumers could lead to lower acquisition costs and higher average revenue per user. For instance, providing payment processing services to small businesses or offering financial management tools to cooperatives could be more cost-effective than trying to onboard individual users one by one.

There’s also growing interest in impact-focused investment models. These approaches prioritize long-term social impact alongside financial returns, potentially allowing for longer runways and more sustainable growth strategies. Such models might be better suited to the realities of building financial infrastructure in emerging markets.

What Does the Future Hold?

As Adebayo contemplates his startup’s future, he realizes the path forward will require a delicate balance between growth and sustainability. The dream of bringing financial services to millions of unbanked Africans remains as compelling as ever, but the route to achieving that dream may need to be recalibrated.

The future of African fintech likely lies in a more nuanced approach to growth and funding. Rather than pursuing rapid scaling at all costs, successful companies must focus on building sustainable unit economics from the ground up. This might mean slower growth in the short term, but it could lead to more robust and impactful companies in the long run.

This shift may require adjusting their expectations and investment strategies for venture capital firms. Longer investment horizons, more hands-on operational support, and a greater focus on a path to profitability rather than just user growth could become the norm.

The story of African fintech is far from over. The potential for transformative impact remains enormous, and the ingenuity and determination of entrepreneurs like Adebayo continue to drive innovation across the continent.

However, realizing this potential will require a reimagining of the current VC-fintech model. By addressing the challenges of high customer acquisition costs, exploring alternative business models, and fostering more supportive regulatory environments, the industry can evolve into a more sustainable and impactful force for financial inclusion.

As the sun sets on another day of hustle and innovation in Africa’s tech hubs, one thing is clear: the future of fintech on the continent will be shaped not just by technological breakthroughs, but by the ability to create sustainable, profitable businesses that truly serve the needs of Africa’s diverse populations. It’s a challenge that will require patience, creativity, and a willingness to rethink established models – but for those who succeed, the rewards could be transformative, not just for their businesses, but for millions of Africans seeking access to vital financial services.

Contributed by Carine Vavasseur, CEO of Ignite.E via Realistic Optimist.

A growth path

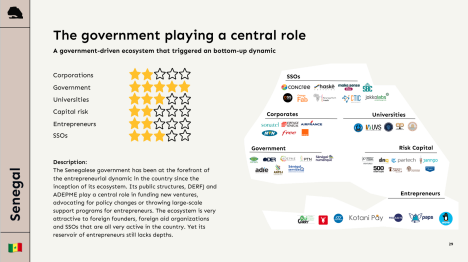

Considered a model of democratic stability in turbulent West Africa, Senegal has recently witnessed the emergence of its own startup ecosystem. Ambitious economic growth objectives, crystalized by the 2012 “Senegal Emergent” plan, led to digital infrastructure improvements, legislative reforms, and collaborations with foreign savoir-faire (StartupBootcamp Afritech, AfricArena, Open Startup Tunisia, La Startup Station, Draper University…).

Following continuous efforts by the Senegalese private sector, the past 5 years have seen the Senegalese government become a driving force behind the ecosystem’s development. This is unlike some of its neighbors such as the Ivory Coast, where the ecosystem evolved more organically. Those governmental efforts are encapsulated in the creation of dedicated agencies such as La Der, where I previously worked, as well as previous existing agencies like ADEPME.

While still young, the ecosystem’s flourishing is concrete. Local champions such as Paps and Chargel have raised significant rounds and are scaling fast. Others like Logidoo, Taaral, or Compact are on their way to significant impact.

Seminal fintech startup Wave, American-funded but African-nurtured and raised, has chosen Senegal as its initial market.

As the ecosystem seeks to elevate and attract foreign investment, deciphering a couple of its specificities is useful.

How VCs should approach Senegal

VCs won’t drastically modify their approach just to invest in Senegal. Not only is the market too small to justify such granularity, but the size of the Senegalese market means any VC investment will have to be pan-African anyway.

That being said, VCs should be cognizant of the different approach to adopt when investing in African startups as a whole. Copy-pasting the investment methodology used for American or European markets is mistaken. Investing in the continent’s startups implies certain subtleties.

The context in which African startups operate is often complex: human/financial resources are rare, and the most pertinent problems to be solved are often at the “bottom of the pyramid”. This implies a tacit impact component, as customers served possess a drastically lower buying power than in California, for example.

When navigating the Senegalese ecosystem, VCs should not hesitate to collaborate. Given the ecosystem’s youth, much of the market data is “declarative” rather than scientifically factual. Trust thus plays a primordial role, and VCs should work together to determine what can be trusted and what can’t.

Since truly VC-backable Senegalese companies are still few, VCs should join forces with the actors propping up and birthing such companies. In Senegal, venture studios such as Haskè Ventures have internalized the creation of promising startups and VCs would lose out by not engaging with them.

A great example is the LionsTech Invest initiative, a local and international investors community and platform that acts as a three-way bridge between investors, startups, and entrepreneur support organizations. Many opportunities and deals happen there.

Both foreign and local investors have a role to play in the ecosystem.

Local investors are crucial because they have inherent local expertise that founders can benefit from. Additionally, engaging local investors quasi-guarantees that the proceeds from any potential exit will get pumped back into Senegal, in one way or another.

That being said, local investors’ coffers are limited and startups will need to raise internationally if they wish to significantly scale. Data shows that the Senegalese startups that have reached the next level have relied on foreign capital to do so.

Implementing the right legislation and incentives to facilitate foreign investment is therefore paramount to the ecosystem’s future development. This also shows the need for supporting and growing business angel networks, another crucial piece of the puzzle.

A healthy mix of both foreign and local investors constitutes standard best practice for most performant ecosystems around the world.

A political risk?

In what is otherwise considered a model of African democracy, the run-up to Senegal’s upcoming election has been eventful, to say the least. This has worried some of the ecosystem’s partners and financiers. They fear that a radical change in government would hurt an ecosystem that is so-called “government-dependent”.

While the government has played an essential role in the ecosystem’s development, I don’t think dependence is the right word. At its inception, the ecosystem was mainly driven by private actors. At that time, around 8 years ago, I was in CTIC Dakar’s management team, francophone West Africa’s first startup hub established in 2011 on a public-private partnership.

Most of the ecosystem-building efforts were, at that time, led by CTIC and players such as Jokkolabs, the OPTIC (under ICT companies’ patronage), individual IT companies, telcos (mainly Sonatel then Tigo), some private companies mainly through their CSR, international NGOs and aid organizations such as GIZ, as well as a few state agencies.

The government’s strong intervention to bolster Senegal’s entrepreneurship ecosystem commenced 5 years ago with DER’s creation. That governmental intervention has been a success and has decidedly elevated the ecosystem to a new stage of maturity.

That gained maturity is precisely why the ecosystem isn’t government-dependent, as some say. Excellent private initiatives have blossomed, and many learning-filled mistakes have been made along the way. Synergies have been tremendously reinforced and have shown concrete results. Even if there is always a need for more collaborations, some of the main interdependencies that needed to be established now exist. They are to be maintained and strengthened.

The government has played its role as a catalyst for better joint impact by not occupying a monopolistic position and making sure that all the players can come together through various initiatives. This has naturally positioned it as a trusted third party.

The future challenge resides in continuing that positive dynamic, regardless of the new or maintained government in power. The Senegalese state will naturally continue to play a major role, in getting regulation and infrastructure up to speed primarily. It will be the ecosystem’s responsibility to continue nudging it in that ecosystem-building direction.

Haskè Ventures

International aid’s presence

International aid organizations have been omnipresent in Senegal’s ecosystem, just as they have in many other African ecosystems. Their presence requires a deep reflection on how the initiatives they finance remain in the ecosystem’s best interest.

There needs to be a clarification of the financed projects’ nomenclature. Today, many Senegalese incubators have aid money as part of their funding mix. However, this has led to incubators mixing startups and SMEs, the latter more in line with aid organizations’ KPIs. Mixing both can cause serious challenges.

Tech startups and SMEs are structurally different and do not require the same financing, benefit from the same mentors, or hold the same scaling ambition. It would be more effective to create programs tailored uniquely to startups, providing them with startup-relevant guidance.

Doing so will require a diversification of these programs’ funding sources, to include more local actors, private investors, and even founders themselves. Successful founders in particular would be the most apt to craft startup-relevant programs.

To sum it all up, while international aid’s presence has been fundamental, it is time to deeply rethink the programs the ecosystem is building for its startups, in their subject matters, their participants, as well as their sources of financing. Supporting this shift is one of our objectives at Ignite.E.

Conclusion

The Senegalese startup ecosystem has come a long way, carried by exceptional private actors and a voluntarist and increasingly implicated government. Much remains to be done by both parties, and it will be up to the first to hold the second up to account regardless of the election results.

VCs investigating Senegal should first determine an adequate, pan-African investment thesis and participate directly or indirectly in building their pipeline of investable startups. To thrive in Senegal and find the best founders, they shouldn’t hesitate to collaborate and engage extensively with the organizations (venture studios, accelerators) fomenting those rockstar companies.

The ecosystem should rethink what programs are truly useful to Senegalese startup founders, and how various funding sources impact the direction these programs take. More

importantly, each ESO should have a clear and strong vision for itself and the ecosystem, with a plan to achieve it and meaningful KPIs to monitor its impact.

Carine Vavasseur is a leading force behind the Senegalese startup ecosystem. She was an ecosystem builder for La Der, Senegal’s President’s initiative aimed at fostering the country’s entrepreneurship and startup scene.

She is now the CEO of Ignite.E, an ecosystem builder within Haskè group (advisory firm and venture studio) with a mandate to build African startup successes through entrepreneurship support organizations’ empowerment.

Le financement de série A représente une étape cruciale dans le parcours d’une startup, fournissant le carburant nécessaire pour développer les opérations et atteindre de nouveaux sommets.

Le financement de série A constitue un jalon important dans le monde du financement des startups. C’est souvent la première grande levée de fonds en capital-risque et marque un point de transition crucial pour les startups.

Mais qu’est-ce que le financement de série A, et pourquoi est-il si important ?

Que vous soyez un entrepreneur cherchant à développer votre entreprise ou un investisseur intéressé par des opportunités de croissance rapide, comprendre le financement de série A est essentiel pour naviguer dans l’écosystème des startups.

Nous plongeons donc dans les complexités du financement de série A, explorant ses caractéristiques, son processus et son impact sur la croissance des startups.

Allons-y.

Qu’est-ce que le Financement de Série A ?

Le financement de série A est généralement la première grande levée de fonds en capital-risque pour les startups.

Il suit habituellement le financement d’amorçage et intervient lorsque une startup a développé une certaine trajectoire – que ce soit une base d’utilisateurs croissante, des chiffres de revenus constants ou d’autres indicateurs clés de performance.

Le “A” dans la série A se réfère à la classe d’actions privilégiées vendues aux investisseurs en échange de leur investissement. Ce tour de table sert souvent de tremplin vers des tours de table ultérieurs (séries B, C, et ainsi de suite) au fur et à mesure que l’entreprise continue de croître.

Caractéristiques Clés du Financement de Série A

Montants Plus Élevés : Les tours de table de série A varient généralement de 2 millions à 15 millions de dollars, bien que cela puisse varier largement en fonction de l’industrie et de l’entreprise spécifique.

Axé sur le Capital-Risque : Bien que les investisseurs providentiels puissent participer, les tours de table de série A sont généralement dirigés par des sociétés de capital-risque.

Traction Requise : Les entreprises cherchant un financement de série A doivent généralement démontrer plus qu’une bonne idée – elles doivent montrer de réels progrès et un potentiel de mise à l’échelle.

Échange d’Équité : Les investisseurs reçoivent des actions privilégiées de l’entreprise en échange de leur investissement.

Sièges au Conseil d’Administration : Les investisseurs de série A prennent souvent des sièges au conseil d’administration pour avoir leur mot à dire dans les décisions stratégiques de l’entreprise.

Le Processus de Financement de Série A

Préparation : Les startups affinent leur modèle commercial, rassemblent des métriques clés et préparent des documents de présentation complets.

Réseautage et Présentation : Les fondateurs se connectent avec des investisseurs potentiels, souvent par le biais d’introductions chaleureuses ou lors d’événements pour startups.

Diligence Raisonnable : Les investisseurs intéressés mènent des recherches approfondies sur la startup, son marché et son équipe.

Négociation de la Feuille de Termes : Si un investisseur décide de procéder, il fournira une feuille de termes décrivant les conditions d’investissement proposées.

Finalisation de l’Accord : Une fois les conditions convenues, les documents juridiques sont rédigés et signés, et les fonds sont transférés.

Pourquoi le Financement de Série A est-il Important ?

Mise à l’Échelle des Opérations : Il fournit le capital nécessaire pour développer l’entreprise au-delà de son marché initial.

Expansion de l’Équipe : Les startups peuvent embaucher des employés clés pour soutenir la croissance.

Développement de Produits : Les fonds peuvent être utilisés pour améliorer le produit ou développer de nouvelles offres.

Expansion du Marché : La série A finance souvent l’expansion géographique ou l’entrée dans de nouveaux segments de marché.

Gain de Crédibilité : Obtenir un financement de série A auprès d’investisseurs réputés peut améliorer la crédibilité d’une startup sur le marché.

Défis et Considérations

Le “Crunch de la Série A” : De nombreuses startups ont du mal à obtenir un financement de série A, ce qui conduit à ce que l’on appelle le “crunch de la série A”.

Attentes Élevées : Les investisseurs de série A attendent des modèles commerciaux plus développés et des chemins plus clairs vers la rentabilité.

Dilution : Les fondateurs doivent être prêts à céder une plus grande partie de l’équité que lors des tours de table précédents.

Changements de Gouvernance : Avec les investisseurs prenant souvent des sièges au conseil d’administration, les fondateurs peuvent avoir moins d’autonomie dans la prise de décision.

Pression pour Croître : Le financement de série A s’accompagne souvent d’attentes de croissance élevée, ce qui peut être stressant pour les fondateurs.

Exemples de l’Écosystème des Startups Africaines

Flutterwave (Nigeria) : Cette startup fintech a levé un tour de série A de 10 millions de dollars en 2017, dirigé par Greycroft Partners et Green Visor Capital. Ce financement a aidé Flutterwave à étendre ses opérations à travers l’Afrique et à développer de nouveaux produits.

Twiga Foods (Kenya) : La plateforme de distribution alimentaire B2B a sécurisé un financement de série A de 10,3 millions de dollars en 2017. Ce tour a permis à Twiga d’améliorer sa technologie et d’étendre sa portée à plus de vendeurs et d’agriculteurs à travers le Kenya.

Andela (Pan-Africain) : L’entreprise de talents technologiques a levé un tour de série C de 40 millions de dollars en 2017, qui, bien que n’étant pas une série A, démontre la trajectoire potentielle pour les startups après la série A.

Comment se Préparer pour un Financement de Série A

Démontrer la Traction : Montrer des preuves claires de croissance, que ce soit en nombre d’utilisateurs, en revenus ou en d’autres métriques pertinentes.

Affiner le Modèle Commercial : Avoir un modèle commercial clair et évolutif avec un chemin vers la rentabilité.

Construire une Équipe Solide : Les investisseurs regardent souvent autant la qualité de l’équipe que le produit.

Développer une Utilisation Claire des Fonds : Avoir un plan spécifique pour l’utilisation du financement de série A pour développer votre entreprise.

Parfaire votre Présentation : Créer une narration convaincante sur la vision de votre entreprise, votre traction et votre potentiel.

Connaître votre Marché : Être prêt à discuter de votre paysage concurrentiel et de votre proposition de valeur unique.

Projections Financières : Avoir des projections financières détaillées et réalistes pour les 3 à 5 prochaines années.

Le Financement de Série A dans le Contexte Africain

Globalement, le paysage du financement de série A en Afrique évolue rapidement. Bien que historiquement, de nombreuses startups africaines devaient chercher des investisseurs internationaux pour les tours de série A, il y a un écosystème croissant de sociétés de capital-risque locales et régionales participant activement à ce stade de financement.

Par exemple, TLcom Capital, une société de capital-risque pan-africaine, a été active dans les tours de série A pour les startups africaines. De même, Partech Africa et Novastar Ventures ont réalisé des investissements significatifs de série A sur le continent.

Cependant, des défis subsistent. Le “crunch de la série A” est particulièrement prononcé en Afrique, de nombreuses startups financées par des semences ayant du mal à sécuriser ce tour crucial suivant. Cela souligne l’importance pour les startups de démontrer une forte traction et des chemins clairs vers la rentabilité pour se démarquer dans un paysage compétitif.

Considérations Uniques pour les Startups Africaines

Défis de Levée de Fonds : Malgré la croissance, les startups africaines rencontrent souvent plus de défis pour lever des fonds de série A par rapport à leurs homologues dans des écosystèmes plus développés.

Investisseurs Internationaux : De nombreux tours de série A pour les startups africaines impliquent des investisseurs internationaux, ce qui peut apporter à la fois des opportunités et des défis.

Perceptions de la Taille du Marché : Les startups peuvent devoir éduquer les investisseurs sur la taille et le potentiel des marchés africains.

Considérations d’Infrastructure : Les investisseurs peuvent avoir des préoccupations concernant les défis d’infrastructure dans certains marchés africains, que les startups doivent aborder.

Focus sur l’Impact : De nombreux investisseurs dans les startups africaines recherchent à la fois des rendements financiers et un impact social positif, ce qui peut influencer les décisions de financement.

La Série A Démystifiée

Le financement de série A représente une étape critique dans le parcours d’une startup, fournissant le carburant nécessaire pour développer les opérations et atteindre de nouveaux sommets.

Bien qu’il s’accomp

agne de son propre lot de défis, réussir à obtenir un financement de série A peut ouvrir la voie à une croissance et à un succès considérables.

Pour les entrepreneurs, comprendre les complexités du financement de série A est crucial pour naviguer dans cette phase importante. Cela nécessite non seulement un excellent produit ou service, mais aussi la capacité de démontrer une traction, d’articuler une vision claire de la croissance et de construire des relations avec les bons investisseurs.

Pour les investisseurs, la série A présente des opportunités de s’impliquer avec des entreprises prometteuses à un stade où leur trajectoire devient claire, mais où il y a encore un potentiel significatif de croissance.

Chez Daba, nous reconnaissons l’importance du financement de série A pour stimuler l’innovation et la croissance économique à travers l’Afrique. Notre plateforme connecte des startups prometteuses avec des investisseurs avisés, facilitant des tours de financement qui peuvent conduire à des résultats transformateurs.

Rappelez-vous, bien que l’obtention d’un financement de série A soit une réalisation significative, ce n’est qu’une étape dans le parcours de la startup. Le succès dépend en fin de compte de l’exécution d’une stratégie de croissance solide, de l’adaptation aux retours du marché et de la construction d’un produit ou service qui apporte véritablement de la valeur à grande échelle.

Avec la bonne approche du financement de série A et un engagement envers la croissance, les startups africaines d’aujourd’hui peuvent devenir les succès mondiaux de demain.

Series A funding represents a critical juncture in a startup’s journey, providing the fuel needed to scale operations and reach new heights.

Series A funding represents a significant milestone in the world of startup financing. It’s often the first major round of venture capital financing and marks a crucial transition point for startups.

But what exactly is Series A funding, and why is it so important?

Whether you’re an entrepreneur looking to scale your business or an investor interested in high-growth opportunities, understanding Series A funding is essential for navigating the startup ecosystem.

Hence, we delve into the intricacies of Series A funding, exploring its characteristics, process, and impact on startup growth.

Let’s get right into it.

What is Series A Funding?

Series A funding is typically the first significant round of venture capital financing for startups.

It usually follows seed funding and comes when a startup has developed a track record of some kind – be it a growing user base, consistent revenue figures, or other key performance indicators.

The “A” in Series A refers to the class of preferred stock sold to investors in exchange for their investment. This round often serves as a stepping stone to later rounds (Series B, C, and so on) as the company continues to grow.

Larger Amounts: Series A rounds typically range from $2 million to $15 million, though this can vary widely depending on the industry and specific company.

Venture Capital Focused: While angel investors might participate, Series A rounds are usually led by venture capital firms.

Traction Required: Companies seeking Series A funding generally need to demonstrate more than just a good idea – they need to show real progress and potential for scaling.

Equity Exchange: Investors receive preferred shares in the company in exchange for their investment.

Board Seats: Series A investors often take board seats to have a say in the company’s strategic decisions.

The Series A Funding Process

Preparation: Startups refine their business model, gather key metrics, and prepare comprehensive pitch materials.

Networking and Pitching: Founders connect with potential investors, often through warm introductions or at startup events.

Due Diligence: Interested investors conduct thorough research on the startup, its market, and its team.

Term Sheet Negotiation: If an investor decides to proceed, they’ll provide a term sheet outlining the proposed investment terms.

Closing the Deal: Once terms are agreed upon, legal documents are drafted and signed, and the funds are transferred.

Why is Series A Funding Important?

Scaling Operations: It provides the capital needed to scale the business beyond its initial market.

Team Expansion: Startups can hire key employees to support growth.

Product Development: Funds can be used to improve the product or develop new offerings.

Market Expansion: Series A often fuels geographical expansion or entry into new market segments.

Credibility Boost: Securing Series A funding from reputable investors can enhance a startup’s credibility in the market.

Challenges and Considerations

The “Series A Crunch”: Many startups struggle to secure Series A funding, leading to what’s known as the “Series A crunch.”

Higher Expectations: Series A investors expect more developed business models and clearer paths to profitability.

Dilution: Founders must be prepared to give up a larger portion of equity than in earlier rounds.

Governance Changes: With investors often taking board seats, founders may have less autonomy in decision-making.

Pressure to Grow: Series A funding often comes with high growth expectations, which can be stressful for founders.

Examples from the African Startup Ecosystem

Flutterwave (Nigeria): This fintech startup raised a $10 million Series A round in 2017, led by Greycroft Partners and Green Visor Capital. This funding helped Flutterwave expand its operations across Africa and develop new products.

Twiga Foods (Kenya): The B2B food distribution platform secured $10.3 million in Series A funding in 2017. This round enabled Twiga to enhance its technology and expand its reach to more vendors and farmers across Kenya.

Andela (Pan-African): The tech talent company raised a $40 million Series C round in 2017, which, while not a Series A, demonstrates the potential trajectory for startups post-Series A.

How to Prepare for Series A Funding

Demonstrate Traction: Show clear evidence of growth, whether it’s in user numbers, revenue, or other relevant metrics.

Refine Your Business Model: Have a clear, scalable business model with a path to profitability.

Build a Strong Team: Investors often look at the quality of the team as much as the product.

Develop a Clear Use of Funds: Have a specific plan for how you’ll use the Series A funding to grow your business.

Perfect Your Pitch: Craft a compelling narrative about your company’s vision, traction, and potential.

Know Your Market: Be prepared to discuss your competitive landscape and your unique value proposition.

Financial Projections: Have detailed, realistic financial projections for the next 3-5 years.

Series A Funding in the African Context

Broadly, the Series A funding landscape in Africa has been evolving rapidly. While historically, many African startups had to look to international investors for Series A rounds, there’s a growing ecosystem of local and regional venture capital firms actively participating in this stage of funding.

For instance, TLcom Capital, a pan-African VC firm, has been active in Series A rounds for African startups. Similarly, Partech Africa and Novastar Ventures have made significant Series A investments in the continent.

However, challenges remain. The “Series A crunch” is particularly pronounced in Africa, with many seed-funded startups struggling to secure this crucial next round. This underscores the importance of startups demonstrating strong traction and clear paths to profitability to stand out in a competitive landscape.

On the back of this, here are some unique considerations for African startups:

Fundraising Challenges: Despite growth, African startups often face more challenges in raising Series A funding compared to their counterparts in more developed ecosystems.

International Investors: Many Series A rounds for African startups involve international investors, which can bring both opportunities and challenges.

Market Size Perceptions: Startups may need to educate investors about the size and potential of African markets.

Infrastructure Considerations: Investors may have concerns about infrastructure challenges in some African markets, which startups need to address.

Impact Focus: Many investors in African startups look for both financial returns and positive social impact, which can influence funding decisions.

Series A Demystified

Series A funding represents a critical juncture in a startup’s journey, providing the fuel needed to scale operations and reach new heights.

While it comes with its own set of challenges, successful Series A funding can set the stage for tremendous growth and success.

For entrepreneurs, understanding the intricacies of Series A funding is crucial for navigating this important phase. It requires not just a great product or service, but also the ability to demonstrate traction, articulate a clear vision for growth, and build relationships with the right investors.

For investors, Series A presents opportunities to get involved with promising companies at a stage where their trajectory is becoming clear, but there’s still significant potential for growth.

At Daba, we recognize the importance of Series A funding in driving innovation and economic growth across Africa. Our platform connects promising startups with savvy investors, facilitating funding rounds that can lead to transformative outcomes.

Remember, while securing Series A funding is a significant achievement, it’s just one step in the startup journey. Success ultimately depends on executing a solid growth strategy, adapting to market feedback, and building a product or service that truly adds value at scale.

With the right approach to Series A funding and a commitment to growth, today’s African startups can become tomorrow’s global success stories.

Que vous soyez un entrepreneur en devenir ou un investisseur cherchant à diversifier ses investissements dans des entreprises en phase de démarrage, comprendre le financement de démarrage est essentiel pour naviguer dans l’écosystème des startups.

Dans le monde dynamique des startups et de l’entrepreneuriat, le terme “financement de démarrage” est fréquemment entendu.

Mais qu’est-ce exactement que le financement de démarrage et pourquoi est-il si crucial pour les nouvelles entreprises ?

Cet article explore les subtilités du financement de démarrage, son importance, ses sources et son impact sur la croissance des startups.

Que vous soyez un entrepreneur en devenir ou un investisseur cherchant à diversifier ses investissements dans des entreprises en phase de démarrage, comprendre le financement de démarrage est essentiel pour naviguer dans l’écosystème des startups.

Qu’est-ce que le financement de démarrage ?

Le financement de démarrage, également appelé capital de démarrage ou argent de démarrage, est souvent le capital initial levé par une startup auprès d’investisseurs institutionnels pour commencer ou poursuivre ses opérations.

Ce financement à un stade précoce se produit généralement lorsque l’entreprise est encore en phase conceptuelle ou vient juste de commencer à fonctionner, souvent après un tour de pré-financement.

La “graine” dans le financement de démarrage est une métaphore appropriée – tout comme une graine a besoin de soins initiaux pour devenir une plante, une startup a besoin de ce coup de pouce financier initial pour transformer son idée en une entreprise viable.

Stade précoce : Le financement de démarrage se produit généralement au tout début du cycle de vie d’une startup.

Montants plus petits : Par rapport aux tours de financement ultérieurs, le financement de démarrage implique généralement des montants de capital plus petits.

Risque élevé, récompense élevée : Les investisseurs à ce stade prennent souvent des risques significatifs, mais peuvent également réaliser des rendements substantiels si la startup réussit.

Preuve de concept : Le financement de démarrage aide souvent les startups à prouver leur concept et à développer un produit minimum viable (MVP).

Sources de financement de démarrage